|

시장보고서

상품코드

2063656

출혈성 질환 검사 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Bleeding Disorder Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

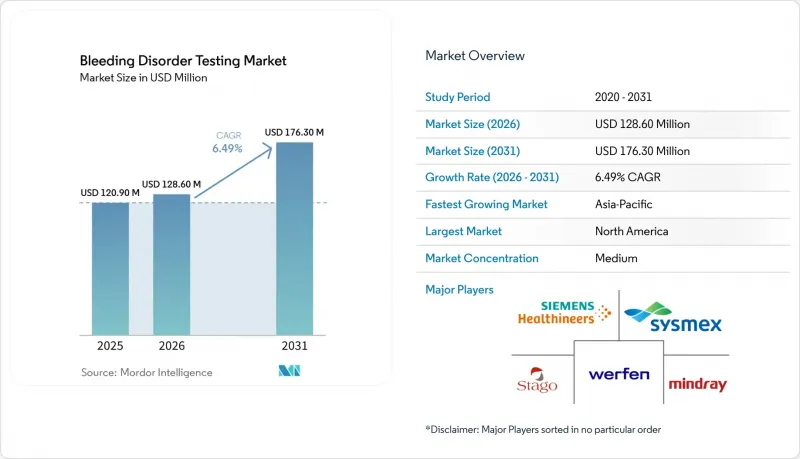

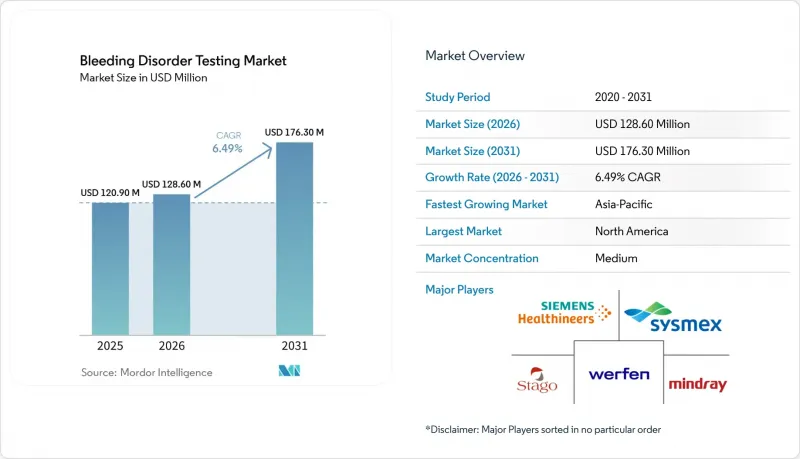

Mordor Intelligence에 의하면, 출혈성 질환 검사 시장 규모는 2025년 1억 2,090만 달러로 평가되었습니다. 2026년에는 1억 2,860만 달러로 확대되어 2031년까지 1억 7,630만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.49%를 나타낼 전망입니다.

본 보고서는 질환별(A형 혈우병, B형 혈우병, 폰 빌레브란트병, 기타), 기술별(응고 검사, 분자진단, 현장 진단, 기타), 제품(시약, 기기, 소프트웨어), 최종 사용자(병원, 검사실, HTC, POC/재택, 연구), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 출혈성 질환 검사 시장 동향 및 인사이트

지침에 따른 검사 도입 및 품질 보증 프로그램

2025년, 각국의 학회는 검사 매뉴얼을 개정하여, 에미시주맙 치료를 받고 있는 환자에 대해 발색법을 이용한 검사와 표준화된 억제 인자 선별 검사 주기를 의무화했습니다. 유럽의 검사 기관들은 영국혈액학회(BSH)의 2024년판 폰 빌레브란트병 지침에 따라 GPIbM 또는 GPIbR 분석법으로 전환함에 따라, 시약의 재조성이 촉진되었습니다. 외부 품질 보증 제도에 참여하는 검사실에서는 현재 규정 준수가 보험 급여 적격성과 직접적으로 연계되어 있어, 추적 가능한 교정 및 ISO 15189 인증 도입이 촉진되고 있습니다. 내장된 사전 분석 검사를 통해 검체 재채취가 40% 감소하고, 유전자 치료 모니터링에 따른 법의학적 위험이 낮아집니다. 조화로운 프로토콜이 보급됨에 따라, 검사실 간 결과의 호환성이 향상되고, 다기관 공동 연구의 운영이 원활해집니다.

자동화 및 통합형 응고 검사 플랫폼으로의 전환

검사 건수가 많은 시설에서는 바코드 검증, 원심 분리, 데이터 관리를 통합한 워크셀을 도입하여 수작업 공정을 70% 줄이고, 야간 무인 운전을 가능하게 하고 있습니다. 새로 출시된 분석 장치는 지혈, 생화학, 면역 측정 결과를 하나의 대시보드에 통합하여 응급실의 검사 결과 보고 시간을 30% 단축합니다. RFID를 활용한 시약 추적을 통해 전사 오류가 해소되고, 유통기한이 지난 재고가 감소합니다. 하루 200건 이상의 지혈 검사 검체를 처리하는 검사실에서는 주로 인건비 절감과 폐기물 감소를 통해 18개월 이내에 투자 비용을 회수할 수 있습니다. 또한, 자동화를 통해 검체 처리가 표준화되어 정확도 시험 결과도 향상됩니다.

실험실 간 측정 변동 및 방법 간 불일치

2024년 정확도 관리 시험에서는 시약 로트 간의 편차와 광로의 차이로 인해, 동일한 혈장을 사용한 검사실 간에도 제VIII인자(FVIII) 결과에 30% 이상의 변동이 나타났습니다. 이러한 편차는 불필요한 투여량 증량을 초래할 수밖에 없게 하여, 환자 1인당 연간 5만 달러의 추가 비용을 발생시킬 가능성이 있습니다. 폰 빌레브란트 인자 검사에서는 이러한 불일치가 더욱 두드러집니다. 조사 방법의 혼용으로 인해 제2형 환자의 18%에서 진단이 14개월 더 지연되고 있습니다. 임상시험에서 중앙 검사실에 업무를 위탁할 경우 콜드체인 물류에 최대 50만 달러의 비용이 소요되므로, 공급업체들은 시약 비용을 30% 인상하는 한편, 교정 편차를 억제하는 잠금식 카트리지 시스템 개발을 추진하고 있습니다.

부문별 분석

출혈성 질환 검사 시장이 틈새 시장인 억제 인자 모니터링에서 광범위한 예방적 감시 체계로 전환되는 가운데, 혈우병 A는 2025년 매출의 48.19%를 차지했으며, 검사 대상 환자 수는 전 세계적으로 4만 명으로 급증했습니다. 폰 빌레브란트병은 가장 빠르게 증가하는 질환으로, GPIb 활성 측정법으로 인해 진단 누락이 많았던 2형 변이가 밝혀짐에 따라 연평균 성장률(CAGR) 7.98%로 확대되고 있습니다. 출혈성 질환 검사 시장 규모는 RNA 간섭 요법의 승인과 함께 분기별로 제9인자 및 항트롬빈 검사가 의무화됨에 따라 확대되고 있습니다. 분자 패널 검사를 통해 희귀 인자 결핍증의 74%에서 원인이 되는 돌연변이를 특정할 수 있게 되면서, 진단은 표현형에서 유전자형으로 전환되고 있습니다.

유전자 치료의 도입으로 인해 평생에 걸친 검사 빈도가 변화하고 있습니다. 3개월 동안은 매월, 그 이후에는 분기마다 제VIII인자 및 제IX인자의 수치를 측정하는 방식으로, 간헐적인 억제인자 선별 검사를 대체하고 있습니다. 이러한 모니터링 강화가 혈우병 치료 센터의 성장 전망을 뒷받침하고 있습니다. 이 센터는 신속한 검사 결과 제공과 임상적 감독을 수행하고 있으며, 이는 분산형 검사실에서는 실현하기 어려운 일입니다. 신생아 선별검사의 확대 역시 기준선 검사 건수를 더욱 끌어올리고 있습니다.

2025년 매출 중 응고 검사가 42.16%를 차지했으며, 그 중심은 활성화 부분 트롬보플라스틴 시간(APTT) 및 프로트롬빈 시간(PT) 검사입니다. 그러나 에미시주맙의 사용이 확대됨에 따라, 발색법을 이용한 제VIII인자 측정법이 원스테이지법을 점차 대체하고 있습니다. 분자진단은 가장 빠르게 성장하는 기술 분야로, 차세대 염기서열 분석(NGS) 패널을 통해 검사 결과 회신 기간이 8주에서 3주로 단축됨에 따라 연평균 8.35%의 성장률을 보이고 있습니다. 현장 진단용 응고 측정 장치는 병상에서 투여량을 조절할 수 있게 함으로써 일정한 시장 점유율을 확보하고 있지만, 보험 급여 제도의 격차로 인해 미국 내 보급은 제한적입니다.

직접 비교 시험 결과, 고급 분석 기기들 간의 정확도는 동등한 것으로 나타났으며, 용혈을 조기에 감지하는 시각적 결함 센서를 도입함으로써 정확도가 더욱 향상되었습니다. 전국적인 유전체 이니셔티브를 통해 유전성 질환 패널에 대한 지원이 이루어짐에 따라, 분자 플랫폼을 활용한 출혈성 질환 검사 시장 규모가 확대될 것으로 전망됩니다. 폐쇄형 시스템의 시약 카트리지는 제조업체에 대한 종속성을 강화하여 소모품 매출액 대비 장비 매출액 비율을 높이고 있습니다.

지역별 분석

아시아태평양은 가장 빠르게 성장하는 지역으로, 연평균 성장률(CAGR)은 8.33%로 예측됩니다. 이는 혈우병 유병률이 2023년 10만 명당 2.57명에서 2030년에는 3.12명으로 증가함에 따라, 진단 지연이 뚜렷해질 것이기 때문입니다. 억제 물질 스크리닝을 의무화하는 정부 지침에 더해, 합리적인 가격의 국산 분석 장비 덕분에 중국과 인도에서 시장 침투가 가속화되고 있습니다. 인도적 목적으로 응고 인자를 제공함으로써, 분기별로 제VIII인자 및 제IX인자의 최저 농도 검사를 정기적으로 실시하게 되어 소모품 수요가 더욱 증가하고 있습니다.

북미는 2025년 매출의 39.17%를 차지했으며, VWF 활성 분석 1회당 45달러의 메디케어 환급과 발색성 모니터링이 필요한 유전자 치료 임상시험의 집중적인 실시가 이를 뒷받침했습니다. 그러나 사전 승인 절차로 인해 검사가 최대 10일간 지연되면서, 투여량 조정 주기가 길어지고 있습니다. 유럽은 GPIb 시약의 채택을 촉진한 2024년 VWF 관련 권고안에 힘입어 상당한 시장 점유율을 유지했으나, 브렉시트로 인해 공급 리드타임이 6주로 늘어남에 따라 90일 분량의 재고 완충량을 확보할 수밖에 없게 되었습니다.

중동 및 아프리카 및 남미도 상당한 점유율을 차지하고 있으며, 이 지역의 성장은 일본 및 호주의 세계 트레이닝 허브와 제휴를 맺은 도시 지역의 혈액 검사 센터(HTC)에 집중되어 있습니다. 신생아 선별검사 및 등록 보고가 공중보건상의 의무로 자리 잡음에 따라, 신흥 지역의 출혈성 질환 검사 시장 점유율은 상승할 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the bleeding disorder testing market size is expected to increase from USD 120.90 million in 2025 to USD 128.60 million in 2026 and reach USD 176.30 million by 2031, growing at a CAGR of 6.49% over 2026-2031.

This report is Segmented by Disorder (Hemophilia A, Hemophilia B, Von Willebrand Disease, Others), Technology (Coagulation Assays, Molecular Diagnostics, Point-Of-Care, Others), Product (Reagents, Instruments, Software), End User (Hospitals, Laboratories, Htcs, POC/Home, Research), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are in Value (USD).

Global Bleeding Disorder Testing Market Trends and Insights

Guideline-Mandated Testing Adoption and Quality Assurance Programs

Global societies updated laboratory manuals in 2025, requiring chromogenic assays for emicizumab-treated patients and standardized inhibitor screening intervals. European laboratories responded to the British Society for Hematology's 2024 Von Willebrand guidance by switching to GPIbM or GPIbR assays, triggering reagent reformulation. Laboratories enrolling in external quality schemes now link compliance directly to reimbursement eligibility, pushing adoption of traceable calibration and ISO 15189 accreditation. Embedded pre-analytical checks lower repeat collection by 40% and shrink medicolegal exposure in gene-therapy monitoring. As harmonized protocols spread, inter-laboratory result portability improves, easing multicenter trial logistics.

Shift to Automation and Integrated Coagulation Platforms

High-volume sites deploy workcells that integrate barcode verification, centrifugation, and data management, cutting manual touchpoints by 70% and enabling overnight lights-out runs. Newly launched analyzers consolidate hemostasis, chemistry, and immunoassay results on one dashboard, trimming emergency-department turnaround times by 30%. RFID reagent tracking eliminates transcription errors and reduces expired inventory. Return on investment arrives within 18 months for labs processing more than 200 hemostasis samples daily, largely through labor savings and decreased waste. Automation also standardizes specimen handling and boosts proficiency-test performance.

Inter-Lab Assay Variability and Lack of Harmonization Across Methods

Proficiency testing in 2024 showed Factor VIII results swinging by ≥30% among labs using identical plasma because of reagent lot drift and differing optical paths. Such noise can force unnecessary dose escalations, adding USD 50,000 per patient annually. Von Willebrand testing is even more discordant; mixed methodologies delay diagnosis an extra 14 months in 18% of Type 2 cases. Central-lab mandates in clinical trials add up to USD 0.5 million in cold-chain logistics, prompting vendors to develop locked-cartridge systems that raise reagent costs by 30% but cap calibration variance.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Point-of-Care PT/INR Self-Testing and Near-Patient Hemostasis

- Asia-Pacific Diagnostic Capacity Build-Out and Installed-Base Expansion

- Pre-Analytical Errors and Specimen Handling Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hemophilia A generated 48.19% of 2025 revenue as the bleeding disorder testing market transitioned from niche inhibitor monitoring to broad prophylaxis surveillance, swelling the testable population to 40,000 patients worldwide. Von Willebrand Disease represents the fastest-growing disorder, advancing at a 7.98% CAGR as GPIb activity assays expose underdiagnosed Type 2 variants. The bleeding disorder testing market size for Hemophilia B rises with RNA-interference therapy approvals that mandate quarterly Factor IX and antithrombin checks. Molecular panels now identify causal mutations in 74% of rare factor deficiencies, shifting diagnosis from phenotype to genotype.

Gene-therapy adoption alters lifetime testing cadence: monthly Factor VIII/IX levels for three months, then quarterly, replacing episodic inhibitor screens. Intensified monitoring underpins the projected growth of hemophilia treatment centers, which deliver rapid turnaround and clinical oversight that decentralized labs struggle to match. Widening newborn screening further lifts baseline volumes.

Coagulation assays held 42.16% of 2025 revenue, anchored by activated partial thromboplastin time and prothrombin time screens. Yet chromogenic Factor VIII methods are overtaking one-stage tests as emicizumab adoption spreads. Molecular diagnostics is the fastest technology segment, climbing 8.35% annually as next-generation sequencing panels shrink turnaround from eight weeks to three. Point-of-care coagulometers capture a modest share by enabling bedside dose titration, though reimbursement gaps limit U.S. uptake.

Head-to-head trials show comparable precision between premium analyzers, with incremental gains tied to visual defect sensors that flag hemolysis earlier. The bleeding disorder testing market size for molecular platforms is forecast to widen as nationwide genomic initiatives subsidize hereditary-disease panels. Closed-system reagent cartridges reinforce manufacturer lock-in, elevating consumable-to-instrument revenue ratios.

Geography Analysis

Asia-Pacific is the fastest region, projected at an 8.33% CAGR, as the prevalence recognition of hemophilia shifts from 2.57 per 100,000 in 2023 toward 3.12 by 2030, revealing a diagnostic backlog. Government guidelines mandating inhibitor screens, plus affordable domestic analyzers, accelerate market penetration in China and India. Humanitarian factor donations translate into recurring quarterly Factor VIII/IX trough tests, deepening consumable demand.

North America commanded 39.17% revenue in 2025, buoyed by USD 45 Medicare reimbursement per VWF activity assay and a high density of gene-therapy trials that require chromogenic monitoring. Nonetheless, prior authorizations delay testing up to 10 days and elongate dose-adjustment cycles. Europe held a significant share, guided by 2024 VWF recommendations that spurred GPIb reagent adoption, although Brexit extended supply lead times to six weeks and forced 90-day inventory buffers.

Middle East & Africa and South America represented notable shares, with growth clustered in urban HTCs that partner with global training hubs in Japan and Australia. The bleeding disorder testing market share across emerging regions will climb as newborn screening and registry reporting become routine public-health mandates.

- Abbott Laboratories

- BioMedica Diagnostics

- Chrono-Log

- Danaher

- Diagnostica Stago

- Erba Diagnostics Mannheim

- F. Hoffmann-La Roche

- HORIBA Medical

- HYPHEN BioMed

- International Technidyne

- Maccura Biotechnology

- SCLAVO Diagnostics International

- Sekisui Diagnostics

- SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- Siemens Healthineers

- Sysmex

- Technoclone

- Thermo Fisher Scientific

- Trinity Biotech

- WerfenLife, S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Guideline-Mandated Testing Adoption and Quality Assurance Programs

- 4.2.2 Shift to Automation and Integrated Coagulation Platforms

- 4.2.3 Expansion of Point-Of-Care PT/INR Self-Testing and Near-Patient Hemostasis

- 4.2.4 APAC Diagnostic Capacity Build-Out and Installed-Base Expansion

- 4.2.5 Emicizumab-Driven Shift to Bovine Chromogenic FVIII Assays and Inhibitor Methods

- 4.2.6 Modernization of VWD Activity Testing (GPIB-Based Assays) and Harmonization

- 4.3 Market Restraints

- 4.3.1 Inter-Lab Assay Variability and Lack of Harmonization Across Methods

- 4.3.2 Pre-Analytical Errors and Specimen Handling Constraints

- 4.3.3 Limited FDA Clearance for Preferred VWD Activity Assays in the U.S.

- 4.3.4 High Costs and Reimbursement Friction for Advanced Tests and Gene-Therapy Era Pathways

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disorder (Indication)

- 5.1.1 Hemophilia A

- 5.1.2 Hemophilia B

- 5.1.3 Von Willebrand Disease (Type 1/2A/2B/2M/2N/3)

- 5.1.4 Other Bleeding Disorders

- 5.2 By Technology

- 5.2.1 Coagulation Assays

- 5.2.2 Molecular Diagnostics

- 5.2.3 Point-of-care Coagulometers

- 5.2.4 Others

- 5.3 By Product

- 5.3.1 Reagents & assay kits

- 5.3.2 Instruments

- 5.3.3 Software & connectivity

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Independent/clinical laboratories

- 5.4.3 Hemophilia treatment centers

- 5.4.4 Point-of-care/home monitoring

- 5.4.5 Research & academia

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott Laboratories

- 6.3.2 BioMedica Diagnostics

- 6.3.3 Chrono-Log

- 6.3.4 Danaher Corporation

- 6.3.5 Diagnostica Stago

- 6.3.6 Erba Diagnostics Mannheim

- 6.3.7 F. Hoffmann-La Roche

- 6.3.8 HORIBA Medical

- 6.3.9 HYPHEN BioMed

- 6.3.10 International Technidyne

- 6.3.11 Maccura Biotechnology

- 6.3.12 Sclavo Diagnostics

- 6.3.13 Sekisui Diagnostics

- 6.3.14 SHENZHEN MINDRAY BIO-MEDICAL ELECTRONICS CO., LTD.

- 6.3.15 Siemens Healthineers

- 6.3.16 Sysmex Corporation

- 6.3.17 Technoclone

- 6.3.18 Thermo Fisher Scientific

- 6.3.19 Trinity Biotech

- 6.3.20 WerfenLife, S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment