|

시장보고서

상품코드

2063659

IT 가시성 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)IT Observability Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

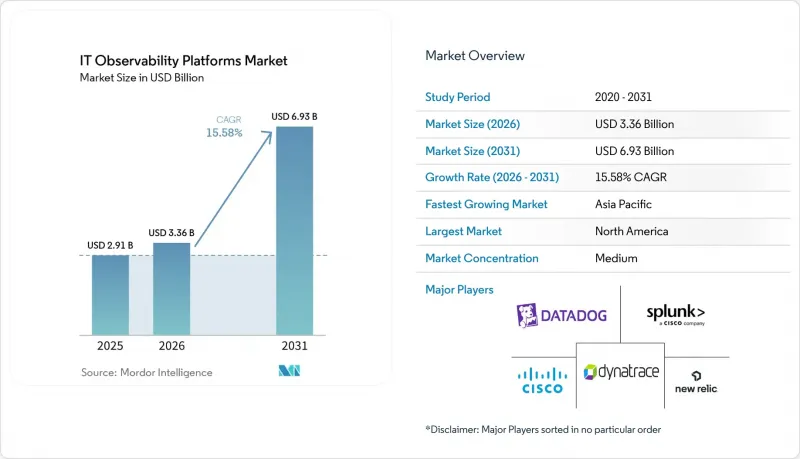

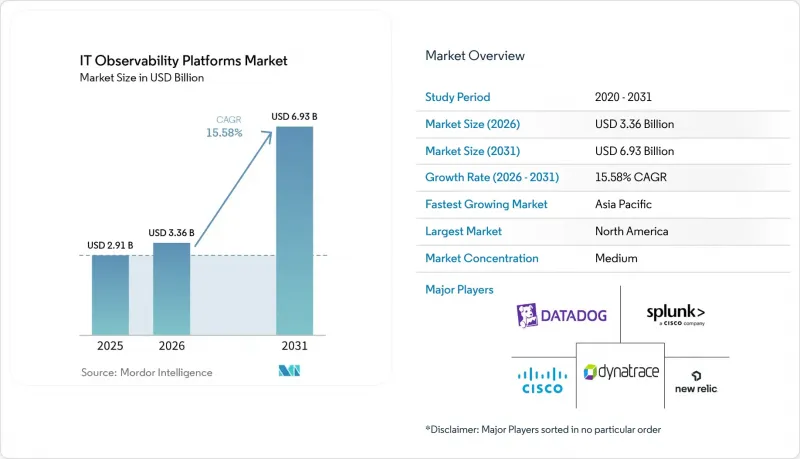

Mordor Intelligence에 의하면, IT 가시성 플랫폼 시장 규모는 2025년 29억 1,000만 달러로 평가되었습니다. 2026년에는 33억 6,000만 달러로 확대되어 2031년까지 69억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 15.58%를 나타낼 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 용도(용도 성능 모니터링, 인프라 모니터링 등), 최종 사용자 산업(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 미디어 및 엔터테인먼트 등), 조직 규모(대기업 및 중소기업), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 IT 가시성 플랫폼 시장 동향 및 인사이트

클라우드 네이티브 아키텍처의 도입 확대

Kubernetes 클러스터, 서버리스 함수, 서비스 메시는 기존의 호스트 중심 모니터링을 무력화시키는 일시적인 리소스를 생성합니다. 벤더들은 현재 페타바이트 규모의 트레이스 수집이 가능한 탄력적인 수집 파이프라인을 구축하고 있는 반면, 아시아태평양의 기업들은 클라우드 네이티브 가시성을 통해 78%의 긍정적 ROI를 보고하고 있습니다. LogicMonitor의 2025년 릴리스에서는 GPU 사용 현황과 지속가능성 목표를 연계하는 비용 최적화 대시보드가 추가되었으며, FinOps 및 GreenOps 지표가 통합되었습니다. 통합된 텔레메트리 시스템이 없는 조직에서는 41%의 사례에서 매주 서비스 중단으로 인해 심각한 영향을 받고 있으며, 이는 풀스택 시스템을 도입한 기업의 24%에 비해 거의 두 배에 달하는 수치입니다. 클라우드 네이티브의 성숙도가 높아짐에 따라 IT 가시성 플랫폼에 대한 수요가 가속화되고 있으며, 이러한 촉진요인의 중기적인 견고성이 확고해지고 있습니다.

예측적 인사이트를 위한 AI와 ML의 통합

AIOps는 단순한 경보 상관 분석에서 자율적인 문제 해결로 점차 전환되고 있습니다. 2026년에 출시된 ScienceLogic의 ‘Skylar Advisor’는 티켓과 문서를 종합적으로 분석하고, 해결 방안을 제안하거나 실행함으로써 평균 해결 시간(MTTR)을 단축합니다. Elastic의 ‘AI SOC Engine’은 가시성과 보안 텔레메트리 데이터를 통합하여, 팀이 자연어로 인시던트를 조사할 수 있도록 지원합니다. 유럽에서는 2025년에 AI 모니터링 도입률이 50%로 급증했으며, 프랑스가 62%로 1위를 차지했습니다. 제조업 사례 연구에 따르면, IT 데이터와 운영 데이터를 결합한 예측 유지보수를 통해 ROI가 2.6배에 달하는 것으로 나타났습니다. 이러한 뚜렷한 생산성 향상 효과는 IT 가시성 플랫폼 시장에 미치는 단기적인 영향을 설명해 줍니다.

텔레메트리 저장 및 수집 비용의 높음

텔레메트리 데이터의 양은 매년 250% 이상 증가하고 있지만, 예산의 70%는 한 번도 조회되지 않는 로그에 소비되고 있어 재무 모델에 부담을 주고 있습니다. Elastic의 조사에 따르면, 2025년에는 공공 기관의 97%가 중복된 파이프라인으로 인해 예상치 못한 청구 문제를 겪었습니다. 각 벤더사는 현재 지능형 샘플링 및 콜드 스토리지 계층을 제공하고 있지만, 거버넌스의 성숙도는 뒤처져 있습니다. Sumo Logic의 2024년판 Flex 라이선싱은 수집 및 쿼리 가격 책정을 분리함으로써 청구액의 급증을 억제하지만, 그럼에도 불구하고 프로세스 변경이 필요합니다. 경제성이 개선되지 않는 한, 일부 기업은 플랫폼 업그레이드를 미룰 가능성이 있으며, 이는 단기적인 성장을 저해할 것입니다.

부문별 분석

서비스 매출은 연평균 성장률(CAGR) 18.28%로 확대되고 있으며, 이는 IT 가시성 플랫폼 시장 전체의 성장률을 상회하고 있습니다. 2025년에는 솔루션이 지출의 67.63%를 차지했으나, 기업들은 멀티클라우드 텔레메트리 통합을 효율화하고 AIOps 워크플로를 자동화하기 위해 전문 서비스 및 관리형 서비스를 점점 더 우선시하고 있습니다. 예를 들어, LogicMonitor의 AWS 마이그레이션 프로그램은 복잡한 IT 환경 관리에 있어 벤더 주도의 전문 지식에 대한 수요가 증가하고 있음을 보여줍니다. 또한, 생성형 AI 기술을 도입하는 정부 기관들은 모델의 드리프트를 모니터링하고 규정 준수를 보장하기 위한 자문 패키지를 요구하고 있으며, 이는 해당 시장에서 서비스 이용 확대를 더욱 촉진하고 있습니다.

매니지드 서비스는 효과적인 IT 가시성을 확보하는 데 필요한 사내 전문 지식이 부족한 경우가 많은 중소기업에게 특히 매력적입니다. 데이터 가져오기, 스토리지, 지원을 포함하는 종량제 번들 플랜은 이러한 기업들이 설비 투자에 따른 장벽을 극복할 수 있도록 돕는 동시에 도입 기간을 대폭 단축합니다. 또한, EU 데이터법에 따른 규정 준수 요건은 감사, 데이터 마스킹, 거버넌스와 관련된 서비스에 새로운 기회를 창출하고 있습니다. 오픈 코어 플랫폼이 소프트웨어 비용을 지속적으로 절감하는 가운데, 서비스 수익은 벤더들에게 전략적인 헤지 수단으로 부상하고 있으며, 라이선스 수익의 성장세가 둔화되더라도 IT 가시성 플랫폼 시장 규모가 계속 확대되는 데 기여하고 있습니다.

용도 성능 모니터링은 2025년 매출의 43.12%를 차지했지만, AI 운영은 연평균 성장률(CAGR) 22.49%라는 급속한 성장을 기록하며 용도 분야 내에서 가장 빠르게 성장하는 부문으로 자리매김하고 있습니다. AWS 마켓플레이스에서 제공되는 Edwin AI는 알림의 잡음을 최대 90%까지 줄일 수 있는 에이전트 기반 자동화의 대표적인 사례입니다. 평균 해결 시간(MTTR)이 30분을 초과하는 문제로 어려움을 겪고 있는 기업에서는 인시던트를 효율적으로 분류하고 스크립트를 자율적으로 실행하기 위해 AIOps 솔루션 도입이 확대되고 있으며, 이를 통해 운영 효율을 높이고 가동 중단 시간을 줄이고 있습니다.

한편, 로그 관리 분야에서는 Sumo Logic이 무제한 데이터 수집 모델을 도입함에 따라 가격의 상품화가 진행되고 있습니다. 이러한 변화로 인해 해당 부문의 초점은 분석 속도와 성능 향상으로 옮겨가고 있습니다. Honeycomb이 2026년 3월에 출시한 ‘Metrics’ 기능의 일반 공개는 통합 텔레메트리로의 전환 과정에서 중요한 이정표이며, 이 회사가 AI 주도 예산 시장에서 더 큰 점유율을 확보하는 기반이 될 것입니다. 한편, 플랫폼이 보안 정보 및 이벤트 관리(SIEM) 기능과 가시성 도구를 통합함에 따라 보안 및 규정 준수 모니터링의 중요성이 점점 더 커지고 있습니다. 이러한 통합은 종합적이고 원활한 솔루션에 대한 수요가 지속적으로 증가하는 광범위한 IT 가시성 플랫폼 시장에서 이어지고 있는 융합 추세를 여실히 보여주고 있습니다.

지역별 분석

2025년에는 하이퍼스케일 클라우드 제공업체의 등장과 정착된 DevOps 문화에 힘입어 북미가 36.74%라는 가장 큰 점유율을 차지했습니다. 해당 지역에서 영향이 큰 서비스 중단으로 인한 비용의 중앙값은 시간당 200만 달러로 추정되며, 이는 첨단 솔루션에 대한 지속적인 투자를 촉진하고 있습니다. 풀스택 플랫폼은 이러한 손실을 대폭 줄일 수 있는 능력을 이미 입증했으며, 많은 기업이 50%의 감축을 달성했다고 보고하고 있습니다. 또한, 각 벤더들이 정부의 엄격한 요건을 충족하기 위해 FedRAMP 인증 취득을 적극적으로 추진하고 있는 만큼, 미국 연방 정부 시장이 지출의 주요 원동력이 되고 있습니다.

유럽에서는 시장에 대한 규제의 영향이 두드러집니다. GDPR(EU 개인정보보호규정)의 시행 및 향후 시행될 데이터 관련 법률에 따라, 기업은 텔레메트리 흐름을 효과적으로 관리해야 할 의무가 있으며, 그 결과 마스킹 기능과 감사 추적 기능을 기본으로 탑재한 플랫폼에 대한 수요가 증가하고 있습니다. 프랑스는 이 분야에서 선두를 달리고 있으며, 연간 예산의 중앙값이 200만 달러에 육박해 유럽에서 가장 높은 지출 수준을 보이고 있습니다. 반면, 독일에서는 여전히 신중한 태도가 나타나고 있으며, 기업의 28%가 관측 가능성의 가치 제안에 대해 불확실성을 느끼고 있습니다. 그 결과, 유럽 전역의 벤더들은 이러한 우려를 해소하고 도입률을 높이기 위해 도구 통합 및 ROI 대시보드에 주력하고 있습니다.

아시아태평양은 성장세가 가장 두드러진 지역으로, 연평균 성장률(CAGR)은 19.61%로 성장을 지속하고, 있습니다. 이 지역의 성장은 중국, 인도, 일본 등 여러 국가에서 제정된 디지털 주권법에 힘입고 있습니다. 이러한 법률들은 국내 데이터 저장을 의무화하고 있으며, 하이브리드 솔루션의 도입을 촉진하고 있습니다. 특히 주목할 점은 해당 지역의 조직 중 78%가 투자 대비 효과(ROI)가 긍정적이라고 보고했으며, 62%는 이미 AI 기반 감시 시스템을 도입하고 있다는 사실입니다. 인도 및 인도네시아의 스타트업 기업들은 레거시 도구를 뛰어넘어 클라우드 네이티브 아키텍처를 빠르게 도입하고 있으며, 비교적 낮은 수준에서 출발해 IT 가시성 플랫폼 시장의 성장을 주도하고 있습니다. 남미, 중동 및 아프리카 등의 신흥 지역도 통신 인프라의 현대화와 공공 부문의 디지털화 추진에 힘입어 성장을 이루고 있습니다. 그러나 기술 부족이나 예산 제약과 같은 문제들로 인해, 이러한 지역에서 시장 침투는 여전히 제한받고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the iT observability platforms market size is expected to increase from USD 2.91 billion in 2025 to USD 3.36 billion in 2026 and reach USD 6.93 billion by 2031, growing at a CAGR of 15.58% over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Application (Application Performance Monitoring, Infrastructure Monitoring, and More), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Media and Entertainment, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global IT Observability Platforms Market Trends and Insights

Growing Adoption of Cloud-Native Architectures

Kubernetes clusters, serverless functions, and service meshes create ephemeral resources that break traditional host-centric monitoring. Vendors now build elastic ingestion pipelines capable of petabyte-scale trace capture, while enterprises in Asia-Pacific report a 78% positive ROI from cloud-native observability. LogicMonitor's 2025 release added cost-optimization dashboards that correlate GPU usage with sustainability targets, aligning FinOps and GreenOps metrics. Organizations lacking unified telemetry suffer weekly high-impact outages in 41% of cases, almost double the 24% rate among full-stack adopters. As cloud-native maturity rises, demand for IT Observability Platforms accelerates, cementing this driver's medium-term strength.

Integration of AI and ML for Predictive Insights

AIOps is shifting from simple alert correlation toward autonomous remediation. ScienceLogic's Skylar Advisor, launched in 2026, reasons across tickets and documentation to recommend or execute fixes, shrinking mean time to resolution. Elastic's AI SOC Engine fuses observability and security telemetry, letting teams interrogate incidents in natural language. Europe saw AI monitoring adoption jump to 50% in 2025, with France leading at 62%. Manufacturing case studies show a 2.6X ROI when predictive maintenance combines IT and operational data. The clear productivity payoff explains the short-term impact on the IT Observability Platforms market.

High Telemetry Storage and Ingestion Costs

Telemetry volumes climb by more than 250% each year, yet 70% of budgets go to logs that are never queried, straining financial models. Elastic found 97% of public-sector bodies faced surprise bills in 2025 due to verbose pipelines. Vendors now offer intelligent sampling and cold-storage tiers, but governance maturity lags. Sumo Logic's 2024 Flex Licensing, which decouples ingestion from query pricing, reduces bill shock yet still demands process change. Unless economics improve, some enterprises may delay platform upgrades, capping near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Standardization Around OpenTelemetry Reducing Vendor Lock-In

- Expansion of DevOps and Site Reliability Engineering Practices

- Talent Shortage in Cloud and Observability Skill Sets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is growing at a 18.28% CAGR, outpacing overall IT Observability Platforms market growth. In 2025, solutions accounted for 67.63% of spending; however, enterprises are increasingly prioritizing professional and managed services to streamline multi-cloud telemetry integration and automate AIOps workflows. For instance, LogicMonitor's AWS migration program highlights the growing demand for vendor-led expertise in managing complex IT environments. Additionally, government agencies adopting generative AI technologies are seeking advisory packages to monitor model drift and ensure compliance, further driving the uptake of services in this market.

Managed services are particularly appealing to SMEs that often lack the in-house expertise required for effective IT observability. Consumption-based bundles, which include ingestion, storage, and support, help these businesses overcome capital expenditure barriers while significantly reducing deployment timelines. Furthermore, compliance requirements under the EU Data Act are creating new opportunities for services related to audit, data masking, and governance. As open-core platforms continue to lower software costs, service revenue is emerging as a strategic hedge for vendors, helping ensure the IT Observability Platforms market size continues to expand even if license revenue growth stabilizes.

Application performance monitoring accounted for 43.12% of 2025 revenue, yet AI operations are experiencing rapid growth, with a compound annual growth rate (CAGR) of 22.49%, making it the fastest-growing segment among applications. Edwin AI, available in the AWS Marketplace, is a prime example of agentic automation that can reduce alert noise by up to 90%. Enterprises struggling with mean time to resolution (MTTR) exceeding 30 minutes are increasingly adopting AIOps solutions to efficiently triage incidents and execute scripts autonomously, thereby improving operational efficiency and reducing downtime.

Log management, on the other hand, is undergoing pricing commoditization following Sumo Logic's introduction of an unlimited ingestion model. This shift has redirected the segment's focus toward improving the speed and performance of analytics. Honeycomb's planned general availability of its Metrics feature in March 2026 marks a significant milestone in its transition to unified telemetry, positioning the company to capture a larger share of AI-driven budgets. Meanwhile, security and compliance monitoring are becoming increasingly critical as platforms integrate Security Information and Event Management (SIEM) capabilities with observability tools. This integration highlights the ongoing convergence trend within the broader IT Observability Platforms market, where the demand for comprehensive and seamless solutions continues to grow.

Geography Analysis

North America accounted for the largest share of 36.74% in 2025, driven by the presence of hyperscale cloud providers and a well-established DevOps culture. The region's median high-impact outage costs, estimated at USD 2 million per hour, have encouraged continuous investments in advanced solutions. Full-stack platforms have already demonstrated their ability to significantly reduce these losses, with many enterprises reporting a 50% reduction. Additionally, the United States federal market has been a key driver of spending, as vendors actively pursue FedRAMP authorizations to meet stringent government requirements.

Europe demonstrates a strong regulatory influence on the market. The implementation of GDPR and the upcoming Data Act mandate that companies manage telemetry flows effectively, thereby increasing demand for platforms equipped with built-in masking and audit-trail capabilities. France leads the region with median annual budgets nearing USD 2 million, reflecting the highest spending levels in Europe. In contrast, Germany remains more cautious, with 28% of firms still uncertain about the value proposition of observability. As a result, vendors across the continent are focusing on tool consolidation and ROI dashboards to address these concerns and enhance adoption rates.

Asia-Pacific is the fastest-growing geography, with a compound annual growth rate (CAGR) of 19.61%. The region's growth is fueled by digital sovereignty laws in countries such as China, India, and Japan, which require data storage within the country and have prompted the adoption of hybrid solutions. Notably, 78% of organizations in the region report positive returns on investment (ROI), and 62% have already implemented AI-driven monitoring systems. Startups in India and Indonesia are rapidly adopting cloud-native architectures, bypassing legacy tools and driving the expansion of the IT Observability Platforms market from a relatively low base. Emerging regions, including South America, the Middle East, and Africa, are also experiencing growth, driven by telecom modernization and public-sector digitalization initiatives. However, challenges such as skills shortages and budget constraints continue to limit market penetration in these areas.

- Datadog, Inc.

- New Relic, Inc.

- Splunk Inc.

- Dynatrace, Inc.

- Cisco Systems, Inc. (AppDynamics)

- Elastic N.V.

- Grafana Labs, Inc.

- Honeycomb, Inc.

- Lightstep, Inc. (ServiceNow)

- LogicMonitor, Inc.

- ScienceLogic, Inc.

- Sumo Logic, Inc.

- Broadcom Inc. (DX Unified)

- Riverbed Technology LLC

- Nexthink SA

- StackState B.V.

- Acceldata, Inc.

- Atatus, Inc.

- Auvik Networks Inc.

- SolarWinds Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Native Architectures

- 4.2.2 Integration of AI and ML for Predictive Insights

- 4.2.3 Standardization Around OpenTelemetry Reducing Vendor Lock-In

- 4.2.4 Expansion of DevOps and Site Reliability Engineering Practices

- 4.2.5 Shift Toward Consumption-Based Pricing Models

- 4.2.6 Rising Demand for Real-Time Security and Compliance Monitoring

- 4.3 Market Restraints

- 4.3.1 High Telemetry Storage and Ingestion Costs

- 4.3.2 Talent Shortage in Cloud and Observability Skill Sets

- 4.3.3 Tool-Chain Sprawl Complicating Unified Visibility

- 4.3.4 Vendor Lock-In Concerns Limiting Portability

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions (Platforms/Tools)

- 5.1.2 Services

- 5.1.2.1 Consulting and Advisory

- 5.1.2.2 Integration and Deployment

- 5.1.2.3 Support and Maintenance

- 5.2 By Application

- 5.2.1 Application Performance Monitoring

- 5.2.2 Infrastructure Monitoring

- 5.2.3 Log Management and Analytics

- 5.2.4 Security and Compliance Monitoring

- 5.2.5 Digital Experience Monitoring

- 5.3 By End-user Industry

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Retail and E-commerce

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Media and Entertainment

- 5.3.8 Other End-user Industries

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Datadog, Inc.

- 6.4.2 New Relic, Inc.

- 6.4.3 Splunk Inc.

- 6.4.4 Dynatrace, Inc.

- 6.4.5 Cisco Systems, Inc. (AppDynamics)

- 6.4.6 Elastic N.V.

- 6.4.7 Grafana Labs, Inc.

- 6.4.8 Honeycomb, Inc.

- 6.4.9 Lightstep, Inc. (ServiceNow)

- 6.4.10 LogicMonitor, Inc.

- 6.4.11 ScienceLogic, Inc.

- 6.4.12 Sumo Logic, Inc.

- 6.4.13 Broadcom Inc. (DX Unified)

- 6.4.14 Riverbed Technology LLC

- 6.4.15 Nexthink SA

- 6.4.16 StackState B.V.

- 6.4.17 Acceldata, Inc.

- 6.4.18 Atatus, Inc.

- 6.4.19 Auvik Networks Inc.

- 6.4.20 SolarWinds Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment