|

시장보고서

상품코드

2063716

치과용 에어 어브레이전 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Dental Air Abrasion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

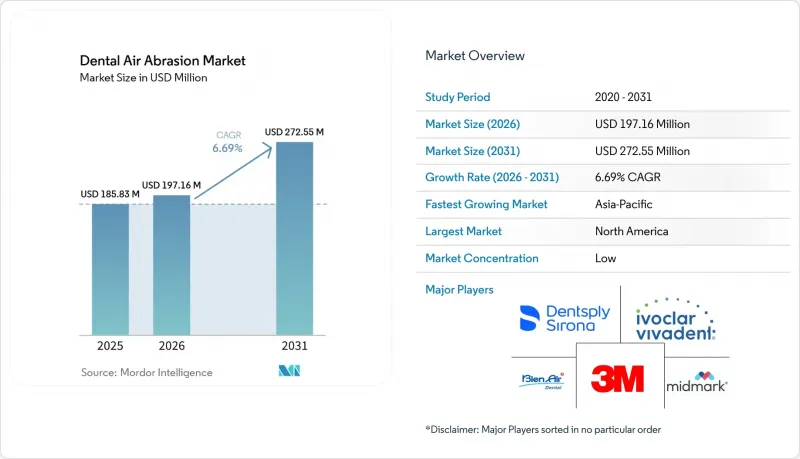

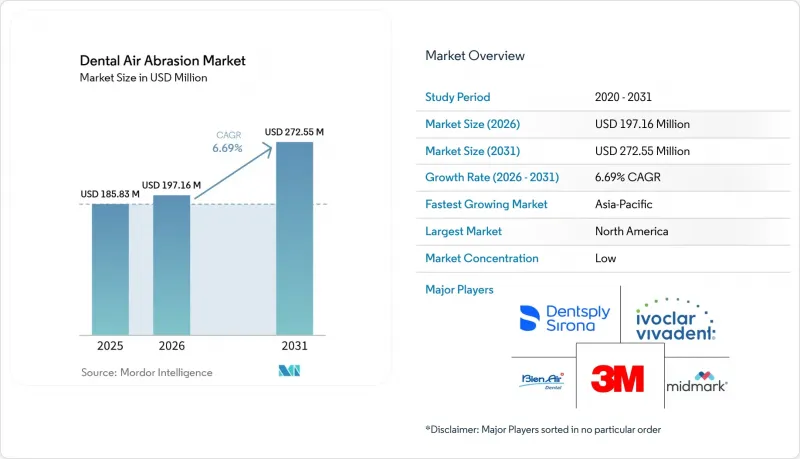

Mordor Intelligence에 의하면, 치과용 에어 어브레이전 시장 규모는 2025년에 1억 8,583만 달러로 평가되었습니다. 2026년에 1억 9,716만 달러에서 2031년까지 2억 7,255만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.69%를 나타낼 전망입니다.

본 보고서는 기기 유형(휴대용, 고정형), 제어 기술(기계식, 디지털식), 용도(충치 형성, 예방 처치, 본딩, 디본딩, 기타), 연마용 매체(알루미늄 산화물, 글리신/에리스리톨, 생체활성), 최종 사용자(클리닉, 병원, 학술 기관, 모바일), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 치과용 에어 어브레이전 시장 동향 및 인사이트

저침습적이고 드릴을 사용하지 않는 치과 치료에 대한 관심 증가

에어 어브레이전은 회전 버에 의한 진동, 열, 음향적 스트레스 없이 초기 법랑질 병변을 제거하며, 2024년 메타분석에 따르면 환자의 불안 점수를 42% 감소시켰습니다. 2025년에 발표된 미국치과의사협회(ADA)의 지침은 클래스 I 및 II 병변에 대한 이 치료법을 권장하고 있으며, 보험 급여의 균등화가 이 치료법의 도입을 가속화하고 있습니다. 이 기술을 도입한 치과에서는 선택적 실런트 시술의 수락률이 두 자릿수 증가를 기록하고 있으며, 시술의 복잡성을 높이지 않으면서도 의자 시간당 수익을 향상시키고 있습니다.

소아 및 불안 증상을 보이는 환자 치료에서의 도입 확대

2025년 연구 결과에 따르면, 6-12세 소아의 68%가 드릴 대신 에어 어브레이전을 선택한 것으로 나타났으며, 이를 통해 마취 없이 수복이 가능해져 진정제 사용량을 31% 줄일 수 있었습니다. 이러한 온화한 감각적 특성은 고령자나 특별한 관리가 필요한 환자층에게도 유익하며, 환자의 협조 태도를 중시하는 의료 종사자들 사이에서 치과용 에어 어브레이전 시장의 확대로 이어지고 있습니다.

소규모 진료소의 막대한 초기 투자 비용과 소모품 비용

도입용 시스템의 가격은 8,000-1만 5,000달러이며, 시술 1회당 분말과 칩 비용으로 약 3달러가 추가되므로, 진료 보수가 낮은 지역에서는 이익률이 압박을 받게 됩니다. 리스 모델도 존재하지만, 많은 경영자들은 벤더 종속이나 사용료 인상을 우려하고 있어, 가격에 민감한 지역에서는 구매가 미뤄지고 있습니다.

부문별 분석

2025년 기준으로, 고정형 데스크톱 시스템은 치과용 에어 어브레이전 시장의 57.32% 점유율을 차지했습니다. 이러한 시스템은 정밀한 유량 제어를 유지하며, 대규모 민간 치과에서 대량의 수복 시술을 수행할 때 선호하여 채택하고 있습니다. 연평균 성장률(CAGR) 6.98%로 성장하고 있는 휴대용 무선 장치는 원격 진료 및 기업 내 현장 검진을 가능하게 하고 있습니다. 배터리 비용의 감소와 MEMS 압력 센서 기술의 발전 덕분에, 현재는 60 psi의 출력을 90분 동안 유지할 수 있게 되어, 충전 전에 소아용 실런트를 30회 도포할 수 있게 되었습니다.

진료소에서는 환자 유치 기회를 확대하기 위한 팝업 형식의 건강 증진 행사에 휴대용 키트를 활용하고 있습니다. 캐나다와 호주의 공중보건 기관들은 원주민 지역사회를 지원하는 순회 진료팀에 이러한 서비스를 포함시키고 있습니다. 규제 당국은 현장용 장치에도 동일한 안전 기준을 적용하고 있어, 의사결정자가 보조금을 배정할 때 신뢰성을 높여주고 있습니다.

기계식 공압 장치는 입증된 신뢰성과 저렴한 유지보수 비용 덕분에 2025년에는 매출의 58.94%를 차지했습니다. 그러나 보험사나 규제 당국이 추적 가능한 진료 데이터를 요구하는 가운데, 스마트 기기 시장은 연평균 성장률(CAGR) 7.09%로 확대되고 있습니다. 미국 한 서비스 기관의 조사에 따르면, 통합 시스템을 도입함으로써 진료 기록 작성 시간이 40% 단축되고, 연마제 폐기량이 18% 감소했으며, 대량의 시술을 수행하는 사업자의 소모품 지출이 절감되었습니다.

원격 진단, 펌웨어 업데이트 및 자동 사용 기록은 가동률을 높이고 의료법상 법적 보호를 강화합니다. 요금 체계가 품질 지표로 전환됨에 따라, 법랑질의 과도한 절삭을 억제하는 스마트한 압력 조절 기능이 차별화 요소가 됩니다.

지역별 분석

북미는 보험 적용 범위 확대와 미국치과의사협회(ADA)의 권고를 바탕으로, 2025년에는 치과용 에어 어브레이전 시장에서 37.23%의 점유율을 확보했습니다. 캐나다의 공공 프로그램에서는 원주민 지원 활동에 휴대용 시스템을 도입하여 국민건강보험 제도를 지원하고 있습니다. 멕시코에서는 신흥 중산층이 심미 치과용 본딩에 대한 수요를 주도하고 있지만, 제조업체들은 가격 면에서 지속적인 압박을 받고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.87%를 기록하며 가장 빠른 성장세를 보이고 있습니다. 중국의 ‘제14차 5개년 계획’에서는 마을 진료소를 대상으로 한 저침습 키트에 보조금이 지급되고 있는 반면, 인도의 학교 대상 치아 코팅 캠페인에서는 휴대용 에어 어브레이전을 사용하여 5,000만 명의 어린이를 대상으로 하고 있습니다. 일본에서는 임플란트를 많이 식립한 고령자들이 치아 표면을 손상시키지 않는 바이오필름 제거를 필요로 하고 있으며, NSK 등 국내 기업들이 전용 생산 라인에 투자하고 있습니다. 호주에서는 외딴 지역 사회에 물자를 공급하는 데 항공 운송에 의존하고 있으며, 배터리 시스템으로 인해 항공기의 적재량이 제한되고 있습니다.

유럽에서는 독일과 영국의 성숙한 민간 수요에 더해, 프랑스와 스페인에서는 정부 주도의 예방 시범 사업이 전개되고 있습니다. GCC 국가들에서는 고급 클리닉 체인의 차별화를 도모하기 위해 에어 어브레이전의 표준화가 추진되고 있습니다. 남미에서는 도입 현황에 차이가 있습니다. 브라질에서는 아마존 지역 지역사회를 대상으로 하천 이동식 설비에 자금을 지원하고 있으나, 재정 상황의 변동으로 인해 도입 규모는 제한되고 있습니다. 한편, 아르헨티나의 의료 관광 시장에서는 미용 패키지의 일환으로 에어 어브레이전 시술이 활성화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the dental air abrasion market size is projected to be USD 185.83 million in 2025, USD 197.16 million in 2026, and reach USD 272.55 million by 2031, growing at a CAGR of 6.69% from 2026 to 2031.

This report is Segmented by Device Type (Portable, Stationary), Control Technology (Mechanical, Digital), Application (Cavity Prep, Prophylaxis, Bonding, Debonding, Other), Abrasive Media (Aluminum-Oxide, Glycine/Erythritol, Bio-Active), End User (Clinics, Hospitals, Academic, Mobile), and Geography (North America, Europe, Asia-Pacific, MEA, South America). The Market Forecasts are in Value (USD).

Global Dental Air Abrasion Market Trends and Insights

Rising Preference for Minimally Invasive Drill-Free Dentistry

Air abrasion removes early enamel lesions without the vibration, heat, or acoustic stress of rotary burs, trimming patient anxiety scores by 42% in a 2024 meta-analysis. American Dental Association guidelines issued in 2025 endorse the modality for Class I and II lesions, creating reimbursement parity that accelerates uptake. Practices adopting the technique record double-digit gains in elective sealant acceptance, improving revenue per chair hour without adding operative complexity.

Growing Adoption in Pediatric and Anxious Patient Care

A 2025 trial showed that 68% of children aged 6-12 chose air abrasion over drills, allowing restorations without anesthesia and cutting sedation use by 31%. The gentler sensory profile also benefits geriatric and special-needs cohorts, broadening the Dental air abrasion market among caregivers focused on behavioral compliance.

High Capital and Consumable Costs for Smaller Practices

Entry systems cost USD 8 000-15 000, and each procedure adds roughly USD 3 in powder and tips, squeezing margins where reimbursement is low. Leasing models exist, yet many owners worry about vendor lock-in and rising per-use fees, delaying purchases in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Integration with Digital Dentistry and CAD/CAM Workflows

- Expansion of Portable Cordless Units in Outreach Dentistry

- Limited Cutting Efficiency for Deep Lesions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stationary desktop systems held 57.32% dental air abrasion market share in 2025. They maintain precise flow control that large private practices favor for bulk restorative throughput. Portable cordless units, expanding at a 6.98% CAGR, unlock remote programs and corporate on-site screenings. Declining battery costs and MEMS pressure sensors now allow 60 psi output for 90 minutes, supporting 30 pediatric sealants before a recharge.

Clinics leverage portable kits for pop-up wellness events that broaden patient funnels. Public health agencies in Canada and Australia embed them in fly-in teams serving Indigenous communities. Regulatory bodies apply the same safety standards to field units, giving decision makers confidence to allocate grant funding.

Mechanical pneumatic devices controlled 58.94% of revenue in 2025 owing to proven reliability and affordable maintenance. Yet smart devices rise at 7.09% CAGR as insurers and regulators request traceable procedural data. A U.S. service organization found that integrated systems cut charting time 40% and reduced abrasive waste 18%, trimming consumables spend for high-volume operators.

Remote diagnostics, firmware updates, and automatic usage logs bolster uptime and medico-legal defense. As fee schedules evolve toward quality metrics, smart pressure modulation that curbs enamel over-ablation becomes a differentiator.

Geography Analysis

North America secured 37.23% of the dental air abrasion market share in 2025 on the strength of insurance parity and ADA endorsement. Public programs in Canada roll portable systems into Indigenous outreach, supporting universal coverage. Mexico's emerging middle class drives cosmetic bonding demand yet keeps price pressure on manufacturers.

Asia-Pacific posts the quickest growth at 6.87% CAGR through 2031. China's Five-Year Health Plan subsidizes minimally invasive kits for township clinics, while India's school sealant campaign targets 50 million children with portable air abrasion. Japan's implant-heavy elderly population needs low-scratch biofilm removal; domestic firms such as NSK invest in dedicated production lines. Australia relies on fly-in provisions for remote communities, where battery systems reduce aircraft payload.

Europe combines mature private demand in Germany and the United Kingdom with government-sponsored prevention pilots in France and Spain. GCC countries standardize air abrasion to differentiate premium clinic chains. South America shows patchy adoption: Brazil funds riverine mobile units for Amazon communities, though fiscal swings temper volume; Argentina's medical tourism market promotes air abrasion in aesthetic packages.

- 3M

- A-dec

- Acteon Group

- Bien Air

- Crystalmark Dental Systems

- Danville Materials

- Dentsply Sirona

- DentalEZ Group

- EMS Dental

- Ivoclar Vivadent

- KaVo Kerr (Envista)

- Midmark

- NSK Ltd.

- Shofu Dental

- TPC Advanced Technology

- Ultradent Products

- Velopex International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Preference for Minimally-Invasive, Drill-Free Dentistry

- 4.2.2 Growing Adoption in Pediatric and Anxious-Patient Care

- 4.2.3 Integration with Digital Dentistry & CAD/CAM Workflows

- 4.2.4 Expansion of Portable/Cordless Units in Outreach Dentistry

- 4.2.5 Regulatory Push for Aerosol-Reduction & Infection Control

- 4.2.6 Emergence of Bio-Active Abrasive Media Enabling Remineralisation

- 4.3 Market Restraints

- 4.3.1 High Capital and Consumable Costs for Smaller Practices

- 4.3.2 Limited Cutting Efficiency Versus Rotary Drills for Deep Lesions

- 4.3.3 Aerosol Safety Concerns Amid Strict Post-COVID Regulations

- 4.3.4 Competition From Alternative Technologies

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Device Type

- 5.1.1 Portable Air Abrasion Units

- 5.1.2 Stationary / Desktop Air Abrasion Units

- 5.2 By Control Technology

- 5.2.1 Mechanical (Pneumatic) Devices

- 5.2.2 Digitally-Controlled / Smart Devices

- 5.3 By Application

- 5.3.1 Cavity Preparation

- 5.3.2 Stain & Plaque Removal / Prophylaxis

- 5.3.3 Surface Conditioning for Bonding & Sealants

- 5.3.4 Orthodontic Debonding & Enamel Cleansing

- 5.3.5 Other Applications (Implant Maintenance, Peri-implantitis Management, etc.)

- 5.4 By Abrasive Media

- 5.4.1 Aluminum-oxide Powders

- 5.4.2 Glycine / Erythritol Low-abrasive Powders

- 5.4.3 Bio-active / Remineralising Powders

- 5.5 By End User

- 5.5.1 Dental Clinics

- 5.5.2 Hospitals

- 5.5.3 Academic & Research Institutes

- 5.5.4 Mobile & Community Dentistry Services

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East & Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East & Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global Level Overview, Market-Level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 3M

- 6.3.2 A-dec Inc.

- 6.3.3 ACTEON Group

- 6.3.4 Bien-Air Dental

- 6.3.5 Crystalmark Dental Systems

- 6.3.6 Danville Materials

- 6.3.7 Dentsply Sirona

- 6.3.8 DentalEZ Group

- 6.3.9 EMS Dental

- 6.3.10 Ivoclar Vivadent

- 6.3.11 KaVo Kerr (Envista)

- 6.3.12 Midmark Corporation

- 6.3.13 NSK Ltd.

- 6.3.14 Shofu Dental

- 6.3.15 TPC Advanced Technology

- 6.3.16 Ultradent Products

- 6.3.17 Velopex International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment