|

시장보고서

상품코드

2063721

의약품용 에이전트형 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Agentic AI In Pharmaceuticals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

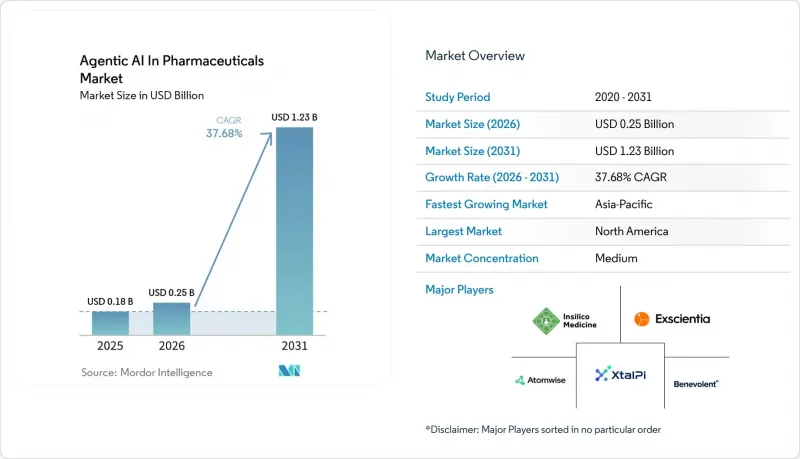

Mordor Intelligence에 의하면, 의약품용 에이전트형 인공지능(AI) 시장 규모는 2025년 1억 8,000만 달러로 평가되었습니다. 2026년에는 2억 5,000만 달러로 확대되어 2031년까지 12억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 37.68%를 나타낼 전망입니다.

본 보고서는 용도(신약 개발 및 선도 화합물 선정, 선도 화합물 최적화, 기타), 도입 형태(On-Premise, 클라우드 기반, 하이브리드), 최종 사용자(대형 제약사, 기타), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의약품용 에이전트형 인공지능(AI) 시장 동향 및 인사이트

연구개발비용 부담 증가로 인해 AI 주도 신약 개발이 추진되고 있습니다.

2024년 기준으로, 단일 분자에 대한 표적 선정부터 승인에 이르기까지의 실제 비용은 평균 26억 달러에 달했으며, 2상 임상시험의 실패율은 60%에 육박했습니다. AI 우선 플랫폼은 in silico를 통해 ADMET 위험을 예측함으로써 전임상 개발 기간을 30-50% 단축할 수 있으며, 합성 전에 유망성이 낮은 후보 화합물을 걸러낼 수 있게 됩니다. Recursion과 바이엘(선급금 5,000만 달러) 및 슈뢰딩거와 일라이 릴리(5,000만 달러)와 같은 제휴 사례는 후원 기업들이 외부 AI 역량에 대한 투자에서 충분한 경제적 이점을 발견하고 있음을 보여줍니다. 전임상 작업을 1개월 단축할 때마다 특허 독점 기간이 그만큼 연장되며, 블록버스터 자산의 경우 최고 매출 연도의 매출액이 5,000만-1억 달러 증가합니다. AI 도입에 뒤처지는 기업은 불과 6개월의 지연만으로도 시장의 주도권이 바뀔 가능성이 있는 치료 분야에서 선점 우위를 잃을 위험에 처하게 됩니다.

고품질 생물학적 데이터 세트의 이용 가능성 증대

2025년에는 공개 데이터 저장소에 수록된 실험적으로 규명된 단백질 구조가 20만 건을 넘어섰고, 여기에 더해 AlphaFold 3가 2억 건 이상의 좌표를 예측함에 따라, 파운데이션 모델이 대상 간에 일반화되는 데 필요한 코퍼스가 제공되었습니다. 실세계 데이터(REW) 플랫폼은 현재 북미와 유럽의 1억 5,000만 명 환자의 익명화된 의료 기록을 집계하고 있으며, 이를 통해 AI 모델은 기존의 3상 임상시험에서는 간과되었던 바이오마커와 치료 반응 간의 연관성을 밝혀낼 수 있게 되었습니다. 연합 학습 네트워크는 원시 데이터를 이동시키지 않고 20개 이상의 대학 병원을 연결하여, 개인정보 보호법을 준수하면서도 통계적 유효성을 유지하고 있습니다. 또한, 아시아·태평양 지역에서는 2025년 임상시험 건수가 25% 급증하며 규모가 확대되고 있습니다.

데이터 개인정보 보호 및 사이버 보안에 대한 우려로 인해 데이터 공유가 제한되고 있습니다.

2024년에 발생한 클라우드 설정 오류로 인해, 익명 처리된 유럽 환자들의 유전자형이 유출되었습니다. 이로 인해 GDPR(EU 개인정보보호규정)에 따라 2,000만 유로의 벌금이 부과되었으며, EU 내 임상시험 의뢰사의 30%가 On-Premise형 스토리지로 되돌아갈 수밖에 없게 되었습니다. HIPAA의 데이터 유출 통지 의무는 평판 리스크를 높이고 있습니다. 2024년 미국에서 발생한 의료 데이터 유출 사고의 평균 비용은 1,090만 달러에 달했습니다. 스폰서들은 벤더들에게 최소 5,000만 달러 규모의 사이버 보험 가입을 점점 더 요구하고 있으며, 이로 인해 많은 초기 단계 AI 스타트업들이 투자 대상 목록에서 제외되고 있습니다. 차등 프라이버시는 위험을 완화할 수 있지만, 모델의 정확도를 최대 10퍼센트 포인트까지 떨어뜨리기 때문에 규제상의 제재가 성능 저하를 상회하는 경우에만 용인될 수 있는 효율성 저하입니다.

부문별 분석

임상시험 설계 및 피험자 모집 시장은 2031년까지 연평균 성장률(CAGR) 39.34%를 나타낼 것으로 예측되며, 2025년 매출의 38.44%를 차지한 신약 개발 분야를 앞지를 것으로 보입니다. AI를 활용한 환자 분류로 인해 선별 검사 실패율이 20-30퍼센트 포인트 감소하여, 프로토콜 준수 비용을 직접 절감합니다. 중간 바이오마커 측정을 도입한 적응형 설계를 통해, 제3상 임상시험의 피험자 등록 수를 4분의 1로 줄이면서 통계적 검출력을 유지하고 개발 일정을 앞당길 수 있습니다. 임상시험용 의약품 분야에서 에이전틱 AI 시장 규모는 2031년까지 5억 2,000만 달러에 달할 것으로 예상되며, 이는 임상시험 후원사들이 데이터 기반 피험자 등록 시스템으로 전환하고 있음을 보여줍니다.

제조 공정의 최적화와 의약품 안전성 감시는 2025년 총 지출에서 15% 미만을 차지했습니다. GMP 감사관이 자동 바이오리액터의 미세 조정마다 인과관계를 입증할 것을 요구하기 때문에 설명 가능성은 여전히 가장 큰 장애물로 남아 있습니다. 규제 당국이 강화 학습 컨트롤러에 대한 승인 기준을 공식적으로 정한 후에는 도입이 확대될 것으로 예상되지만, 현재 보급률은 여전히 신약 개발 및 임상 분야에 비해 뒤처져 있습니다.

지역별 분석

북미는 Recursion, Schrodinger, Relay Therapeutics와 같은 AI 네이티브 기업의 존재는 물론, 2026년 1월 FDA와 EMA가 지침을 발표한 이후 규제 측면에서 선점 우위를 바탕으로 2025년 매출의 50.76%를 차지했습니다. 미국 내 의약품 AI 분야에 대한 벤처 자금 조달 규모는 2024년에 42억 달러에 달했으며, 이를 통해 스타트업 기업들이 초기 단계에서 라이선스 계약 없이도 사업을 확장할 수 있게 되었습니다. 캐나다는 넉넉한 연구개발 세액 공제의 혜택을 누리고 있지만, 미국 수준에 필적하는 국내 고객 기반을 갖추지 못하고 있으며, 멕시코는 규제 현대화가 시급한 미성숙한 상태에 있습니다.

아시아태평양은 중국의 양자 컴퓨팅 인프라에 대한 보조금과, 인도의 임상시험 비용이 미국(환자 1인당 약 1만 5,000달러)에 비해 현저히 낮은 평균 약 2,000달러인 점에 힘입어, 2031년까지 연평균 성장률(CAGR) 40.12%를 나타낼 것으로 예측됩니다. 일본 PMDA(의약품 및 의료기기 종합기구)의 지침안에서는 희귀질환에 대한 AI를 활용한 계층화가 허용됨에 따라, 그동안 수행할 수 없었던 연구가 가능해졌습니다. 한편, 한국에서는 5,000억 원(3억 7,500만 달러) 규모의 이니셔티브를 통해 민관 협력형 AI·제약 프로젝트가 지원되고 있습니다. 호주는 뒤처져 있지만, 2026년 2월에 FDA와의 규제 조화가 이루어진다면 따라잡을 가능성이 있습니다.

유럽에서는 GDPR(EU 개인정보보호규정)에 따른 동의 획득의 문턱으로 인해 다기관 승인까지 걸리는 기간이 18개월에 달하는 등 여전히 제약을 받고 있습니다. 그럼에도 불구하고, 영국, 프랑스, 독일의 각 거점에서는 BenevolentAI와 Owkin이 주도하는 연방 학습(federated learning) 시범 사업이 진행되고 있습니다. 중동 걸프 국가들은 경제 다각화의 일환으로 AI 연구에 자금을 지원하고 있지만, 견고한 모델 훈련을 수행하기에는 충분한 환자 수가 부족합니다. 남아프리카는 유전적 다양성이 풍부한 임상시험 코호트를 제공하고 있지만, AI 공급업체의 수는 적으며, 라틴아메리카에서는 통화 변동과 규제 정책의 변화로 인해 성장이 저해되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

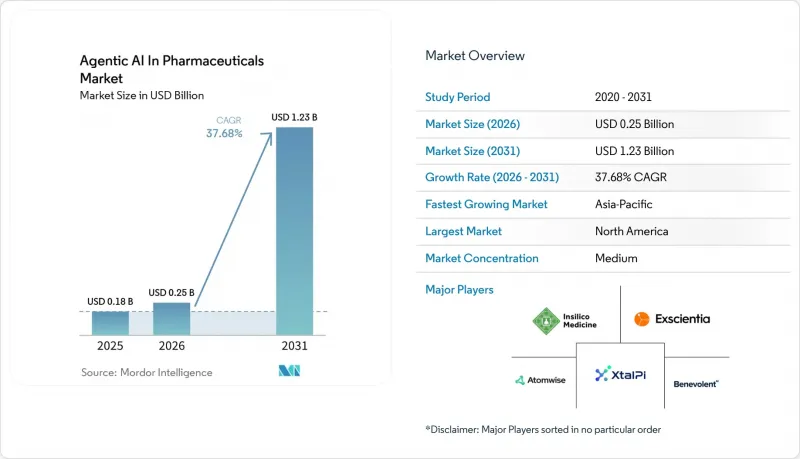

KTH 26.06.24According to Mordor Intelligence, the agentic AI in pharmaceuticals market size is expected to grow from USD 0.18 billion in 2025 to USD 0.25 billion in 2026 and is forecasted to reach USD 1.23 billion by 2031, registering a 37.68% CAGR over 2026-2031.

This report is Segmented by Application (Drug Discovery and Lead Identification, Lead Optimization, and Others), Deployment Mode (On-Premise, Cloud-Based, Hybrid), End User (Large Pharmaceutical Companies, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Agentic AI In Pharmaceuticals Market Trends and Insights

Escalating R&D Cost Pressures Driving AI-Led Discovery

The out-of-pocket cost of bringing a single molecule from target nomination to approval averaged USD 2.6 billion in 2024, with Phase II failure rates near 60%. AI-first platforms can trim preclinical timelines by 30-50% by predicting ADMET liabilities in silico, letting teams cull weak candidates before synthesis. Partnerships such as Recursion-Bayer (USD 50 million upfront) and Schrodinger-Eli Lilly (USD 50 million) demonstrate that sponsors perceive enough economic upside to fund external AI capabilities.Each month removed from preclinical work extends patent exclusivity by the same duration, translating into USD 50-100 million in peak-year sales for blockbuster assets. Firms slow to deploy AI risk forfeiting first-mover advantage in therapeutic areas where even a six-month delay can shift market leadership.

Rising Availability of High-Quality Biological Data Sets

Public data stores surpassed 200,000 experimentally solved protein structures in 2025, while AlphaFold 3 predicted coordinates for 200 million more, providing the corpus that foundation models require to generalize across targets. Real-world evidence platforms now aggregate anonymized health records for 150 million patients across North America and Europe, allowing AI models to surface biomarker-response links invisible in traditional Phase III trials. Federated-learning networks connect 20+ academic medical centers without moving raw data, ensuring compliance with privacy laws yet preserving statistical power, and Asia-Pacific adds scale through a 25% surge in 2025 trial volume.

Data-Privacy and Cybersecurity Concerns Limit Data Sharing

A 2024 cloud misconfiguration exposed anonymized European patient genotypes, drew EUR 20 million in GDPR fines, and pushed 30% of EU sponsors back to on-premise storage. HIPAA's breach-notification mandates elevate reputational risk; the average U.S. healthcare data breach cost USD 10.9 million in 2024. Sponsors increasingly require vendors to carry at least USD 50 million in cyber-insurance, barring many early-stage AI startups from procurement lists. Differential privacy can mitigate exposure but erodes model accuracy by up to 10 percentage points, an efficiency hit acceptable only when regulatory penalties outweigh performance loss.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Encouragement for AI-Driven Trial Design

- Integration of Agentic AI With Self-Driving Laboratories

- Skill Gap in Validating and Deploying Complex AI Agents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical-trial design and recruitment is expected to grow at 39.34% CAGR through 2031, eclipsing drug discovery, which held 38.44% of 2025 revenues. AI-based patient stratification lowers screen-failure rates by 20-30 percentage points, directly trimming per-protocol costs. Adaptive designs embracing interim biomarker reads cut Phase III enrollment by one-quarter, preserving statistical power while accelerating timelines. The agentic AI in pharmaceuticals market size for clinical-trial applications is projected to reach USD 0.52 billion by 2031, underscoring sponsors' pivot toward data-driven enrollment systems.

Manufacturing-process optimization and pharmacovigilance together represented <15% of 2025 outlays. Explainability remains the chief barrier, because GMP auditors insist upon causal chains for every automated bioreactor tweak. Uptake should rise after regulators formalize acceptance criteria for reinforcement-learning controllers, but current penetration still lags discovery and clinical segments.

Geography Analysis

North America generated 50.76% of 2025 revenue on the strength of AI-native players like Recursion, Schrodinger, and Relay Therapeutics plus regulatory first-mover advantage after the January 2026 FDA-EMA principles. U.S. venture funding for pharmaceutical AI hit USD 4.2 billion in 2024, enabling startups to scale without early licensing deals. Canada benefits from generous R&D tax credits but lacks the domestic customer base to match U.S. scale, and Mexico remains nascent pending regulatory modernization.

Asia-Pacific is expected to grow at a 40.12% CAGR through 2031, driven by China's subsidies for quantum-computing infrastructure and India's significantly lower clinical trial costs, averaging about USD 2,000 per patient compared to approximately USD 15,000 in the United States. Japan's PMDA draft guidance allows AI-guided stratification for rare diseases, unlocking previously unviable studies, while South Korea's KRW 500 billion (USD 375 million) initiative underwrites public-private AI-pharma projects. Australia trails but may catch up after regulatory harmonization with the FDA in February 2026.

Europe remains constrained by GDPR consent hurdles that stretch multi-site approval times to 18 months. Nonetheless, hubs in the United Kingdom, France, and Germany anchor federated-learning pilots by BenevolentAI and Owkin. Middle Eastern Gulf states fund AI research as part of economic diversification but lack sufficient patient volumes for robust model training. South Africa offers genetically diverse trial cohorts yet hosts few AI vendors, and Latin American growth is stymied by currency volatility and shifting regulatory stances.

- Atomwise Inc.

- Benevolent AI

- BioAge Labs

- Cloud Pharmaceuticals

- Cyclica Inc.

- DeepCure

- Envisagenics

- Evaxion Biotech

- Healx

- Iktos

- Insilico Medicine

- Owkin

- Peptone

- Relay Therapeutics

- Schrodinger Inc.

- Valo Health

- Verge Genomics

- XtalPi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating R&D Cost Pressures Driving AI-Led Discovery

- 4.2.2 Rising Availability of High-Quality Biological Data Sets

- 4.2.3 Regulatory Encouragement for AI-Driven Trial Design

- 4.2.4 Integration of Agentic AI With Self-Driving Laboratories

- 4.2.5 Foundation Models Targeting Rare-Disease Biology

- 4.2.6 Blockchain-Secured Data Marketplaces for Federated Learning

- 4.3 Market Restraints

- 4.3.1 Data-Privacy and Cybersecurity Concerns Limit Data Sharing

- 4.3.2 Skill Gap in Validating and Deploying Complex AI Agents

- 4.3.3 Synthetic-Data Feedback Loops Risk Model Collapse

- 4.3.4 Explainability Gaps in GMP Environments Delay Compliance

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Drug Discovery and Lead Identification

- 5.1.2 Lead Optimization

- 5.1.3 Pre-clinical Development

- 5.1.4 Clinical-Trial Design and Recruitment

- 5.1.5 Manufacturing-Process Optimization

- 5.1.6 Pharmacovigilance and Safety Monitoring

- 5.1.7 Others

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.2.3 Hybrid

- 5.3 By End User

- 5.3.1 Large Pharmaceutical Companies

- 5.3.2 Small and Mid-Size Biotech Firms

- 5.3.3 Contract Research Organizations

- 5.3.4 Academic and Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Atomwise Inc.

- 6.3.2 BenevolentAI

- 6.3.3 BioAge Labs

- 6.3.4 Cloud Pharmaceuticals

- 6.3.5 Cyclica Inc.

- 6.3.6 DeepCure

- 6.3.7 Envisagenics

- 6.3.8 Evaxion Biotech

- 6.3.9 Healx

- 6.3.10 Iktos

- 6.3.11 Insilico Medicine

- 6.3.12 Owkin

- 6.3.13 Peptone

- 6.3.14 Relay Therapeutics

- 6.3.15 Schrodinger Inc.

- 6.3.16 Valo Health

- 6.3.17 Verge Genomics

- 6.3.18 XtalPi

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment