|

시장보고서

상품코드

2063746

혈관 영상 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vascular Imaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

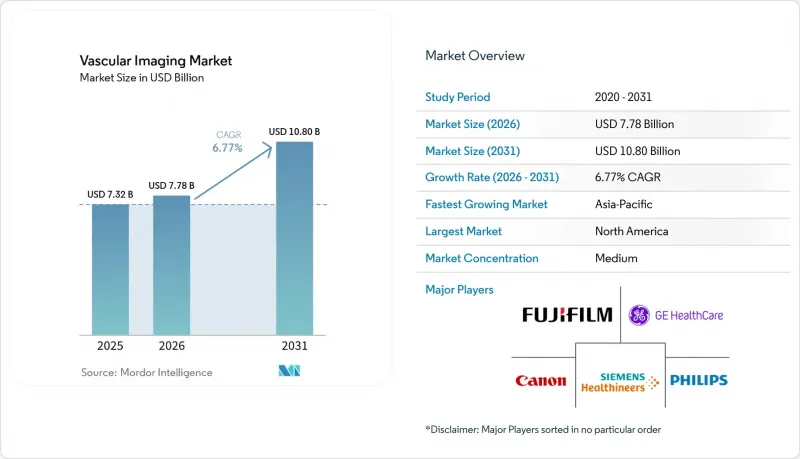

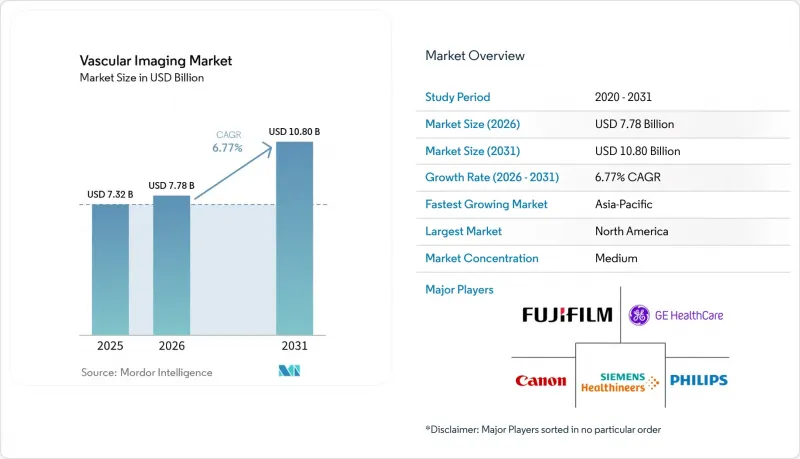

Mordor Intelligence에 의하면, 혈관 영상 시장 규모는 2025년 73억 2,000만 달러에서 2026년에는 77억 8,000만 달러로 확대되어 2031년까지 108억 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 6.77%로 성장할 전망입니다.

본 보고서는 모달리티(초음파/도플러, CTA, X선 혈관조영술/DSA 등), 시술 유형(관상동맥 조영술/PCI, 말초동맥, 신경혈관 등), 적응증(죽상동맥경화증/CAD 및 PAD, 동맥류성 질환 등), 최종 사용자(병원, 진단센터 등), 지역(북미 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 혈관 영상 시장 동향 및 인사이트

심혈관 질환(CVD) 및 말초동맥질환(PAD)의 부담 증가로 인해 혈관 진단 및 모니터링에 대한 수요가 증가하고 있습니다.

지침의 통일적인 개정에 따라, 65세 이상 성인을 대상으로 한 발목-팔 상완 혈압비(ABI) 선별 검사 및 증상이 있는 말초동맥질환에 대한 듀플렉스 초음파 검사 또는 CT 혈관조영술이 의무화됨에 따라, 전 세계적으로 진단 대상자가 실질적으로 두 배로 증가했습니다. 유럽의 지침에 따르면, 만성 사지 허혈의 경우 치료 전 CTA 또는 MRA를 필수로 규정하고 있으며, 이에 따라 모든 혈관 재건 워크플로우에 영상 진단이 포함되어 있습니다. 일본과 한국에서 경동맥 듀플렉스 검사의 연속적인 시행에 대한 보험 급여가 적용됨에 따라, 이전에는 일회성이었던 수익이 지속적인 수익으로 바뀌었습니다. 검사 건수의 누적적 증가는 영상 진단 기기의 가격이 점차 하락하고 있는 상황에서도 혈관 영상 시장 성장에 대한 확실한 견인력을 유지하고 있습니다.

저침습적 혈관내 치료로의 전환에 따라, 수술 중 영상 진단 건수가 증가

현재 복부 동맥류의 혈관내 치료술은 전체 증례의 약 80%를 차지하며, 흉부 EVAR(혈관내 동맥류 치료술)은 B형 박리의 최대 80%를 치료하고 있으며, 두 경우 모두 3상 영상 촬영, 수술 전 CTA, 콘빔 CT 융합 및 수술 후 혈관조영술이 필요합니다. 2024년에는 복잡한 PCI 이행 건수가 전년 대비 12% 증가했습니다. 또한, 무작위 임상시험 결과, OCT 안내를 통해 표적 혈관의 시술 실패율이 28% 감소하는 것으로 나타났으며, 이는 가이드라인에서 혈관 내 영상 진단의 중요성이 더욱 부각되는 계기가 되고 있습니다. 2025년 말까지 북미의 하이브리드 수술실 도입 대수는 1,200대를 넘어설 전망이며, EVAR 1건당 조영제 사용량을 30-40% 줄임으로써 그 활용이 확대되고 있습니다. 이러한 시술 중 수요가, 설비 투자 예산이 엄격해졌음에도 불구하고, 혈관 영상 시장에서 꾸준한 지출을 뒷받침하고 있습니다.

기술자 부족으로 인해 스캔 능력이 제한되고 대기 시간이 길어짐

2025년에는 CT 기술자의 결원율이 19.4%, 심혈관 중재술 담당자의 결원율이 17.4%를 나타낼 것으로 예측되며, 채용까지 걸리는 기간의 중앙값이 94일로 늘어남에 따라 스캐너 도입이 지연되고 있습니다. 유럽의 방사선사 부족은 2024년에 1만 2,000명에 달할 전망이며, 브렉시트로 인한 인재 유출로 인해 영국의 대동맥 영상 진단 대기 시간이 길어지고 있습니다. 초음파 검사사의 교차 교육이나 AI 자동 위치 조정 시스템 도입은 부분적인 완화책에 불과하며, 혈관 영상 진단 시장에서 인적 자원의 한계를 여실히 드러내고 있습니다.

부문별 분석

애보트의 ‘Ultreon 3.0’과 Conavi의 하이브리드 IVUS-OCT가 관강 분석을 자동화하고 판독 시간을 35% 단축함에 따라, 혈관 내 영상 진단은 연평균 성장률(CAGR) 8.22%로 가장 빠른 모달리티 확대를 기록할 것으로 예측됩니다. 초음파 혈관 영상 시장 규모는 2025년에 40.24%의 점유율을 차지하며 여전히 현장 진단(Point-of-Care) 분야의 도입을 주도하고 있지만, 자본 집약도는 광자 계수 CT로 이동하고 있으며, 각 업체들은 0.2mm의 해상도와 듀얼 에너지 감산을 약속하고 있습니다. 초음파의 휴대성과 방사선 피폭이 전혀 없습니다는 장점은 연평균 5.8%의 성장률을 유지하고 있지만, 프리미엄 CT 및 혈관조영 시스템으로의 이익률 이동은 분명합니다.

컴퓨터 단층촬영 혈관조영술(CTA)의 혈관 영상 시장 점유율은 2025년에 상당한 수준에 도달할 것으로 보이며, AI 재구성 기술의 발전에 따라 상승세를 보이고 있습니다. 한편, X선 혈관조영술은 천장형 C-암과 3D 융합 소프트웨어를 결합한 하이브리드 수술실(OR) 수요 증가로 인해 혜택을 보고 있습니다. 자기공명혈관조영술(MRA)은 진단이 어려운 신장 혈관 및 경동맥 사례군을 포괄하고 있으며, 핵의학은 매출의 5% 미만을 차지하는 연구 분야로서의 위치를 유지하고 있습니다.

TEVAR(경피적 혈관내 대동맥 치환술)의 치료 적용 범위가 확대되고, 콘빔 CT 융합 기술을 통해 조영제 사용량이 30-40% 감소함에 따라, 대동맥 및 동맥류 영상 진단 시장은 연평균 8.65%의 성장률을 보이고 있습니다. 관상동맥 조영술은 미국 내 5,000개에 달하는 카테터실과, 복잡한 PCI(경피적 관상동맥 성형술) 시 가이드라인에서 의무화하고 있는 IVUS(경혈관 초음파) 및 OCT(광간섭 단층촬영) 덕분에 여전히 최대의 수익원을 유지하고 있습니다. 말초동맥 조영술은 새로운 PAD(말초동맥질환) 선별 검사 권고에 따라 그 시행이 가속화되고 있는 반면, 신경혈관 유도술은 24시간 이내 혈전 제거술의 적응증 확대와 ‘도어-투-그로인(door-to-groin)’ 시간을 58분으로 단축하는 AI 트리아지의 혜택을 받고 있습니다.

수술 중 콘빔 CT를 통해 가능해진 단일 단계 EVAR는 30일 이내 재입원율을 8.4%에서 2.9%로 낮추었으며, 스캐너 교체 주기를 뒷받침하는 비용 절감 효과를 입증하고 있습니다. CTPA를 통한 위험도 분류가 모든 응급실에서 일상화됨에 따라, 심부정맥혈전증의 영상 진단 일관성이 높아지고 있으며, 이는 혈관 영상 진단 시장의 깊이를 더하고 있습니다.

지역별 분석

북미는 1,200개의 하이브리드 수술실, FFR-CT의 조기 보험 적용, 그리고 5,000개가 넘는 카테터실 도입 실적을 바탕으로 2025년 매출의 39.35%를 차지하고 있습니다. 그러나 기술 인력 부족으로 인해 선택적 CTA의 대기 시간이 2023년 12일에서 2025년에는 18일로 늘어났으며, 이에 따라 AI 워크플로우 도구를 통해 해소될 수 있는 잠재적 수요가 발생하고 있습니다.

아시아태평양은 중국의 1조 위안(1,500억 달러) 규모의 병원 건설 계획과 인도의 국내 CT 및 초음파 장비 제조를 지원하는 생산 연계형 인센티브(PLI)에 힘입어, 지역별 최고 수준인 9.12%의 연평균 성장률(CAGR)을 기록하고 있습니다. 유나이티드 이미징은 광자 계수형 시스템의 가격을 기존 제조업체보다 25% 낮게 책정한 결과, 2024년 4분기까지 중국 주요 도시에서 신규 CT 도입 시장의 18%를 점유했습니다. 일본은 OCT의 보험 환급액을 56% 인상하여, 고가 제품의 도입 추세를 강화했습니다.

유럽 시장의 큰 비중을 차지하는 업체들은 MDR/IVDR에 따른 구조조정에 직면해 있으며, 이로 인해 구형 기기의 40%가 시장에서 철수할 위험에 처해 있고, 규정 준수 비용이 30% 상승하고 있습니다. 이러한 상황은 인증 기관과 탄탄한 관계를 맺고 있는 공급업체에 유리하게 작용하고 있습니다. 중동 및 아프리카은 소규모 기반에서 성장하고 있으며, 사우디아라비아의 640억 달러 규모 ‘비전 2030’ 계획에 따른 지출이 GCC(걸프협력회의) 회원국들 수요를 뒷받침하고, 2024년 6월에는 이 지역 최초로 광자 계수형 CT가 도입되었습니다. 남미 시장의 5% 점유율은 안정적이며, 브라질과 아르헨티나에서는 환율 변동의 영향을 상쇄하기 위해 재생형 혈관조영 시스템이 도입되었습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the vascular imaging market size is expected to increase from USD 7.32 billion in 2025 to USD 7.78 billion in 2026 and reach USD 10.80 billion by 2031, growing at a CAGR of 6.77% over 2026-2031.

This report is Segmented by Modality (Ultrasound/Doppler, CTA, X-Ray Angiography/DSA, and More), Procedure Type (Coronary Angiography/PCI, Peripheral Arterial, Neurovascular, and More), Application (Atherosclerosis/CAD & PAD, Aneurysmal Disorders, and More), End User (Hospitals, Diagnostic Centers, and More), and Geography (North America, and More). Market Forecasts are Provided in Terms of Value (USD).

Global Vascular Imaging Market Trends and Insights

CVD and PAD Burden Elevates Demand for Vascular Diagnostics and Monitoring

Concerted guideline updates now mandate ankle-brachial index screening for adults over 65 and duplex or CT angiography for symptomatic peripheral arterial disease, effectively doubling the diagnostic pool worldwide. European recommendations position pre-intervention CTA or MRA as compulsory for chronic limb-threatening ischemia, embedding imaging into every revascularization workflow. Serial carotid duplex reimbursements in Japan and South Korea establish recurring revenue that was previously episodic. Cumulative procedure growth maintains a clear pull on the vascular imaging market even as modality pricing edges downward.

Shift Toward Minimally Invasive Endovascular Procedures Increases Intraprocedural Imaging Volumes

Endovascular aneurysm repair now addresses roughly 80% of abdominal cases and thoracic EVAR treats up to 80% of type B dissections, each case requiring triple-phase imaging, pre-operative CTA, cone-beam CT fusion, and completion angiography. Complex PCI volumes climbed 12% year-over-year in 2024, while randomized evidence shows OCT guidance lowers target-vessel failure by 28%, driving guideline elevation of intravascular imaging. Hybrid operating rooms surpassed 1,200 installs in North America by late 2025 and cut contrast volume 30%-40% per EVAR, expanding utilization. These intraprocedural needs power resilient spending within the vascular imaging market despite capital-budget scrutiny.

Technologist Shortages Cap Scanning Capacity and Extend Wait Times

Vacancy rates reached 19.4% for CT technologists and 17.4% for cardiovascular interventional roles in 2025, lengthening median hiring time to 94 days and delaying scanner purchases. European radiographer deficits hit 12,000 positions in 2024, with Brexit-related workforce exits worsening U.K. aortic-imaging queues. Cross-training sonographers and deploying AI auto-positioning offers only partial relief, underscoring a human-capital ceiling on the vascular imaging market.

Other drivers and restraints analyzed in the detailed report include:

- CT, Ultrasound, and AI Advances Improve Diagnostic Yield and Throughput in Vascular Pathways

- Reimbursement Tailwinds for CCTA + FFR-CT and Intravascular Imaging Codes Accelerate Adoption

- Radiation Dose and Iodinated Contrast Safety/Availability Concerns Limit CT and Angiography Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intravascular imaging is forecast to post the fastest modality expansion at 8.22% CAGR as Abbott's Ultreon 3.0 and Conavi's hybrid IVUS-OCT automate lumen analytics and cut interpretation time 35%. The vascular imaging market size for ultrasound commanded 40.24% share in 2025 and still drives point-of-care adoption, but capital intensity is pivoting to photon-counting CT where vendors promise 0.2 mm resolution and dual-energy subtraction. Ultrasound's portability and zero radiation sustain 5.8% annual growth, yet margin migration to premium CT and angiography systems is unmistakable.

The vascular imaging market share for computed-tomography angiography reached a significant percentage share in 2025 and rises in tandem with AI reconstruction, while X-ray angiography benefits from hybrid-OR demand that pairs ceiling C-arms with 3D fusion software. Magnetic resonance angiography consolidates difficult renal and carotid cohorts, and nuclear medicine retains a research niche below a 5% revenue threshold.

Aortic and aneurysm imaging grows 8.65% annually as TEVAR treatment windows widen and cone-beam CT fusion lowers contrast burden 30%-40%. Coronary angiography maintains dominant revenue owing to 5,000 U.S. cath labs and guideline-mandated IVUS/OCT for complex PCI. Peripheral arterial angiography accelerates on new PAD screening recommendations, while neurovascular guidance benefits from 24-hour thrombectomy eligibility and AI triage that cuts door-to-groin time to 58 minutes.

Single-stage EVAR enabled by intraoperative cone-beam CT reduces 30-day readmissions from 8.4% to 2.9% and illustrates the cost-avoidance case sustaining scanner replacement cycles. Deep-vein-thrombosis imaging gains consistency as CTPA risk-stratification routines enter every emergency department, bolstering vascular imaging market depth.

Geography Analysis

North America controls 39.35% of 2025 revenue thanks to 1,200 hybrid ORs, early FFR-CT reimbursement, and an installed base exceeding 5,000 cath labs. Yet technologist vacancies lengthen elective CTA wait times from 12 days in 2023 to 18 days in 2025, creating latent demand buffered by AI workflow tools.

Asia-Pacific delivers the fastest regional CAGR at 9.12%, driven by China's CNY 1 trillion (USD 0.15 trillion) hospital build-out and India's Production-Linked Incentive that subsidizes domestic CT and ultrasound manufacturing. United Imaging captured 18% of new CT installs in tier-1 Chinese cities by Q4 2024 after pricing photon-counting systems 25% below incumbents. Japan lifted the OCT reimbursement 56%, reinforcing premium adoption curves.

Europe's significant share faces MDR/IVDR attrition that places 40% of legacy devices at withdrawal risk and lifts compliance cost 30%, favoring vendors with deep notified-body ties. The Middle East and Africa grow off a small base, Saudi Arabia's USD 64 billion Vision 2030 spend anchors GCC demand and delivered the region's first photon-counting CT in June 2024. South America's 5% share is steady, with Brazil and Argentina adopting refurbished angiography systems to offset currency volatility.

- Abbott Laboratories

- Boston Scientific

- Bracco

- Canon

- Conavi Medical

- Esaote

- FUJIFILM (SonoSite)

- GE Healthcare

- Guerbet

- Infraredx (a Nipro Company)

- Koninklijke Philips (Philips Healthcare)

- Mindray

- Samsung Group

- Shimadzu

- Siemens Healthineers

- Terumo

- United Imaging Healthcare

- Ziehm Imaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CVD And PAD Burden Elevates Demand for Vascular Diagnostics and Monitoring

- 4.2.2 Shift Toward Minimally Invasive Endovascular Procedures Increases Intraprocedural Imaging Volumes

- 4.2.3 CT/Ultrasound/AI Advances Improve Diagnostic Yield and Throughput in Vascular Pathways

- 4.2.4 Reimbursement Tailwinds for CCTA + FFRCT And Intravascular Imaging Codes Accelerate Adoption

- 4.2.5 Outpatient ASC/OBL Shift and Hybrid OR Buildouts Expand Angiography/Ultrasound Installed Base

- 4.2.6 Spectral/Low-Iodine CT Protocols Broaden Eligibility for Renal-Risk And Calcified Patients

- 4.3 Market Restraints

- 4.3.1 Technologist Shortages Cap Scanning Capacity and Extend Wait Times

- 4.3.2 Radiation Dose and Iodinated Contrast Safety/Availability Concerns Limit CT/Angiography Use

- 4.3.3 High Capital and Lifecycle Costs Constrain Adoption in Resource-Limited Settings

- 4.3.4 EU MDR/IVDR Compliance Burden Slows Product Refresh and Availability in Europe

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Modality

- 5.1.1 Ultrasound / Doppler

- 5.1.2 Computed Tomography Angiography (CTA)

- 5.1.3 X-ray Angiography / Digital Subtraction Angiography (DSA)

- 5.1.4 Magnetic Resonance Angiography (MRA)

- 5.1.5 Intravascular Imaging (IVUS / OCT / NIRS)

- 5.1.6 Nuclear Medicine (SPECT / PET vascular applications)

- 5.2 By Procedure Type

- 5.2.1 Coronary angiography / PCI guidance

- 5.2.2 Peripheral arterial angiography & interventions (lower/upper extremity)

- 5.2.3 Neurovascular angiography & EVT guidance

- 5.2.4 Aortic/EVAR/TEVAR imaging

- 5.2.5 Venous thromboembolism imaging (DVT/PE pathways)

- 5.2.6 Carotid and cerebrovascular duplex/CTA/MRA

- 5.3 By Application

- 5.3.1 Atherosclerosis / CAD & PAD

- 5.3.2 Aneurysmal disorders

- 5.3.3 Vasculitis & large-vessel inflammation

- 5.3.4 Deep vein thrombosis & pulmonary embolism

- 5.3.5 Arteriovenous malformations & fistulas

- 5.3.6 Tumor vascularity and pre-op planning

- 5.4 By End User

- 5.4.1 Hospitals (Tertiary/Community)

- 5.4.2 Diagnostic Imaging Centers

- 5.4.3 Ambulatory Surgery Centers

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Abbott Laboratories

- 6.3.2 Boston Scientific

- 6.3.3 Bracco Imaging

- 6.3.4 Canon Medical Systems

- 6.3.5 Conavi Medical

- 6.3.6 Esaote

- 6.3.7 FUJIFILM (SonoSite)

- 6.3.8 GE HealthCare

- 6.3.9 Guerbet

- 6.3.10 Infraredx (a Nipro Company)

- 6.3.11 Koninklijke Philips (Philips Healthcare)

- 6.3.12 Mindray

- 6.3.13 Samsung Medison

- 6.3.14 Shimadzu Corporation

- 6.3.15 Siemens Healthineers

- 6.3.16 Terumo

- 6.3.17 United Imaging Healthcare

- 6.3.18 Ziehm Imaging

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment