|

시장보고서

상품코드

2063750

신경영양성 각막염 치료 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Neurotrophic Keratitis Treatment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

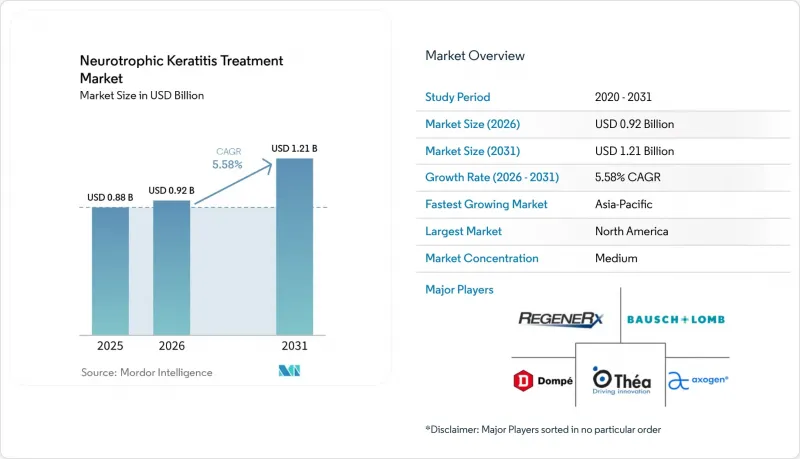

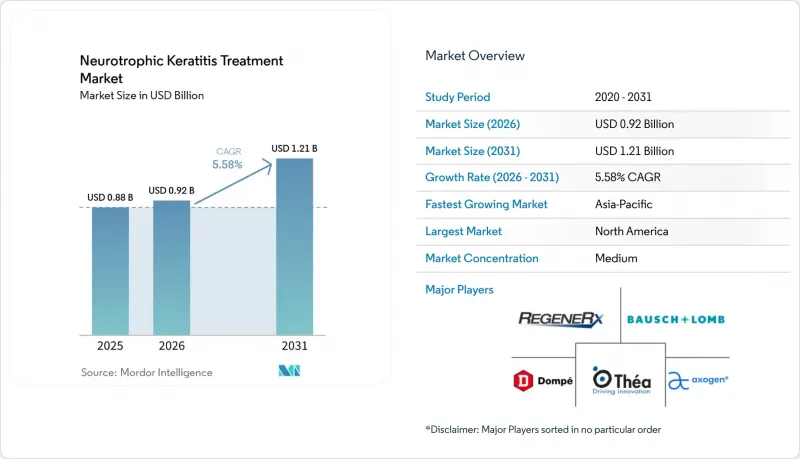

Mordor Intelligence에 의하면, 신경영양성 각막염 치료 시장 규모는 2025년 8억 8,000만 달러로 평가되었습니다. 2026년 9억 2,000만 달러에서 2031년까지 12억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.58%를 나타낼 것으로 예측됩니다.

본 보고서는 치료 유형별(약제 및 인공눈물, 재조합 인간 신경성장인자 점안액, 항생제, 콘택트렌즈), 질환 단계별(1기, 2기, 3기), 판매 채널별(병원 약국, 소매 약국, 온라인 약국), 지역별(북미, 유럽, 아시아태평양, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 신경영양성 각막염 치료 시장 동향 및 인사이트

최초로 승인된 치료제인 세네게르민(rhNGF)에 대한 접근성 확대

중국에서 진행된 세네게르민의 제4상 임상 데이터에 따르면, 8주 시점에서 84.6%의 상피 폐쇄가 보고되었으며, 56주 시점의 지속률은 90.9%에 달하고, 주요 임상시험 결과를 뛰어넘는 유효성이 입증되었습니다. 독점 기간 종료 후 바이오시밀러 개발은 빠르게 진행되고 있지만, 2-8도의 보관 요건과 15일간의 폐기 규정에 따라 전문 약국 인프라를 갖춘 제조업체들은 공급 측면에서 우위를 유지하고 있습니다. 메디케어 파트 D는 8주간의 치료 과정(11만 8,230달러)을 보장하지만, 사전 승인으로 인해 30-60일의 지연이 발생하기 때문에 병원 측에서는 환자에게 약물 복용 준수를 적극적으로 지도하도록 권고받고 있습니다. 유럽의 보험사들은 국가별로 리베이트 협상을 진행 중이며, CADTH는 95%의 가격 인하를 요구하고 있어 비용 대비 효과 문제를 둘러싼 마찰이 발생하고 있음을 시사하고 있습니다. KB801 등의 유전자 치료는 주 2회 투여를 약속하고 있어, 간병인의 부담과 콜드체인 비용을 모두 대폭 줄일 가능성이 있습니다.

증가하는 NK 위험 인자(HSV/HZO, 당뇨병)

인도에는 1억 100만 명의 당뇨병 환자가 있으며, 이 수치는 2045년까지 1억 3,400만 명에 달할 가능성이 있습니다. 당뇨병성 각막병증은 이 인구 집단 중 47-64%에 영향을 미치고 있으며, 이는 신경영양성 각막염의 유병률과 직접적인 관련이 있습니다. HSV와 HZO는 전 세계적으로 신경병성 각막 손상의 주요 원인으로 남아 있으며, HZO의 발병률은 50세 이후 10년마다 두 배로 증가하고 있습니다. 전반적으로, 현재 신경영양성 각막염 환자의 31.59%가 당뇨병을 동반하고 있으며, 이는 시력 예후의 악화와 상관관계가 있어, 2024-2025년 임상시험에서 81-90%의 치유율을 달성한 국소 인슐린 등의 보조 요법에 대한 수요를 촉진하고 있습니다. 라식 수술 건수가 회복됨에 따라, 수술 후 감각 둔화가 신경영양성 각막염 치료 시장을 더욱 확대시킬 가능성이 있습니다.

rhNGF 요법의 높은 비용과 비용 대비 효과 문제

CADTH는 QALY당 100만 캐나다 달러를 초과하는 증분 비용-효과 비율을 산출하고, 95%의 가격 인하가 이루어진 경우에만 보험 적용을 권고했습니다. 독일의 G-BA는 ‘기타 혜택’을 인정했으나, 가격 인하를 강력히 요구하고 있는 반면, 프랑스에서는 병원 예산 상한선이 적용되고 있습니다. 경제적으로 여유가 있는 보험 가입자를 제외하고는 하루 6회 투여로 인해 많은 고령 환자가 간병인의 도움이 필요하게 되어 숨겨진 비용이 발생합니다. 바이오시밀러가 가격을 낮출 가능성은 있지만, 엄격한 콜드체인 프로토콜과 독자적인 충전 및 마무리 능력이 상품화되는 데 걸림돌이 되고 있습니다.

부문별 분석

2025년, 인공눈물은 신경영양성 각막염 치료 시장에서 45.82%의 점유율을 유지했습니다. 이러한 우위는 고가의 생물학적 제제가 승인되기 전에 90일간의 시험 사용을 의무화하는 지불자 주도형 단계적 치료 방식에 기인하며, 이러한 주기가 소매 채널에서의 판매량을 유지하고 있습니다. 콘택트렌즈 세척액과 관련된 신경영양성 각막염 치료 시장 규모는 2026년부터 2031년까지 연평균 성장률(CAGR) 5.87%로 확대될 것으로 전망됩니다. 이는 BostonSight사의 PROSE 및 EyePrint사의 공막용 기기가 구제 요법에서 1차 선택 보호 요법으로 전환됨에 따라, 재생 의학 승인을 기다리는 동안 손상된 각막을 보호할 수 있는 액체 저류층을 형성하기 위함입니다. 재조합 인간 신경성장인자는 2024년에 10억 달러의 매출을 기록했으나, 하루 6회 투여 일정과 11만 8,230달러의 가격 책정으로 인해, 중국 실세계 데이터에서 84.6%의 치료 중단률이 입증되었음에도 불구하고 광범위한 보급은 제한되고 있습니다.

항생제는 여전히 보조적인 역할을 하고 있으며, 결손이 2mm를 초과하는 경우에 예방 차원에서 처방되지만, 매출에서 차지하는 비중은 여전히 낮은 임베디드니다. 유전자 치료는 만성적인 점안약 치료를 대체할 준비가 되어 있습니다. Krystal Biotech사의 KB801은 2025년 7월부터 투여를 시작했으며, 복제 불가능한 HSV-1 벡터를 사용하여 주 2회 NGF 발현을 실현하고 있어, 편의성의 기준을 재정의할 가능성이 있습니다. 초기 데이터가 세네게르민의 치료 효과를 재현한다면, 지불 주체의 판단 기준은 급격히 변화할 것이며, 인공눈물에 대한 의존도가 낮아짐과 동시에 신경영양성 각막염 치료 시장에서 비용 대비 효과의 기준치 평가 방식도 바뀔 가능성이 있습니다.

지역별 분석

2025년 신경영양성 각막염 치료 시장에서 북미는 매출의 38.95%를 차지했습니다. 메디케어 파트 D는 질병의 경과를 장기화시키는 30-60일간의 사전 승인이 필요함에도 불구하고, 세네게르민을 적용 대상으로 하고 있습니다. 캐나다 CADTH의 승인은 대폭적인 가격 인하를 조건으로 하고 있어, 퀘벡주와 온타리오주를 제외한 다른 주에서는 도입이 제한적입니다. 멕시코의 사립 병원에서는 의료 관광을 온 환자들을 대상으로 세네게르민을 처방하고 있지만, 본인 부담금이 부담스러워 국내에서는 여전히 보급이 더딘 실정입니다.

유럽은 매출액 면에서 북미에 뒤처져 있지만, 유럽의약품청(EMA)의 조기 승인 및 돔페사의 이탈리아 내 유통 거점의 혜택을 받고 있습니다. 독일의 G-BA는 세네게르민에 ‘기타 혜택’이 있다고 인정했으며, 추가 리베이트를 요구하고 있는 반면, 프랑스는 희귀질환 치료제 예산에 대해 병원별로 엄격한 상한선을 설정하고 있습니다. EU 의료기기 규정(MDR) 2017/745는 미국산 의료기기 시장 진입을 지연시켰지만, 유럽의 조직 은행들이 규모를 확대하도록 촉진하여 양막 공급의 병목 현상을 부분적으로 해소했습니다.

아시아태평양은 인도의 당뇨병 환자 수의 급증과 중국에서 진행된 제4상 rhNGF 임상시험의 긍정적인 결과(이는 NMPA 승인의 길을 열어줄 것으로 예상)에 힘입어 연평균 성장률(CAGR) 5.71%로 가장 빠르게 성장할 것으로 전망됩니다. 일본과 한국에서는 규제 당국의 승인을 기다리는 단계이지만, 이미 국민건강보험의 지원을 받아 신경 재생 치료가 진행되고 있으며, rhNGF나 유전자 치료가 승인되면 누적된 수요가 표면화될 것입니다. 중동 및 아프리카에서는 검사 체계의 미비나 보험금 지급 제한으로 인해 여전히 제약을 받고 있지만, 브라질과 아르헨티나에서는 민간 보험사를 통해 점차 보급이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the neurotrophic keratitis treatment market size is projected to expand from USD 0.88 billion in 2025 and USD 0.92 billion in 2026 to USD 1.21 billion by 2031, registering a CAGR of 5.58% between 2026 to 2031.

This report is Segmented by Therapy Type (Drugs-Artificial Tears, Recombinant Human Nerve Growth Factors Eye Drops, Antibiotics, Contact Lens), Disease Stage (Stage I, Stage II, Stage III), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Neurotrophic Keratitis Treatment Market Trends and Insights

Expanding Access to Cenegermin (rhNGF) as First Approved Therapy

Cenegermin's real-world Phase IV data from China reported 84.6% epithelial closure at week 8, with 90.9% durability at week 56, validating efficacy beyond the pivotal trials. Post-exclusivity biosimilar pursuit is rapid, yet the two-to-eight-degree storage requirement and 15-day discard rule maintain a supply moat for manufacturers with specialty pharmacy infrastructure. Medicare Part D covers the USD 118,230 eight-week course, but prior authorization imposes 30-60-day delays, nudging hospitals to counsel patients aggressively on adherence. European payers negotiate country-specific rebates, and CADTH has demanded 95% price cuts, signaling cost-effectiveness friction. Gene therapies such as KB801 promise twice-weekly dosing, potentially collapsing both caregiver burden and cold-chain expense.

Rising NK Risk Factors (HSV/HZO, Diabetes)

India hosts 101 million people with diabetes, a figure that could reach 134 million by 2045; diabetic keratopathy affects 47-64% of this population, feeding directly into neurotrophic keratitis prevalence. HSV and HZO continue to underpin neuropathic corneal damage worldwide, and HZO incidence doubles every decade after age 50. Collectively, 31.59% of neurotrophic keratitis patients now carry a diabetes comorbidity, correlating with worse visual outcomes and catalyzing demand for adjuncts like topical insulin, which achieved 81-90% healing in 2024-2025 trials. As LASIK volumes rebound, postoperative hypoesthesia could further enlarge the neurotrophic keratitis treatment market.

High Cost and Cost-Effectiveness Headwinds for rhNGF Therapy

CADTH calculated an incremental cost-effectiveness ratio above CAD 1 million per QALY and advised reimbursement only after a 95% price cut. Germany's G-BA conferred an "additional benefit" label but is pressing for discounts, while France enforces hospital budget ceilings. Outside wealthy payers, six-times-daily administration imposes hidden expenses because many elderly patients require caregiver assistance. Biosimilars may erode price, yet stringent cold-chain protocols and proprietary fill-finish capabilities remain barriers to commoditization.

Other drivers and restraints analyzed in the detailed report include:

- Increased Diagnosis Via Esthesiometry and In Vivo Confocal Microscopy

- Wider Payer Recognition of Amniotic Membrane Devices

- Underdiagnosis and Late Presentation Due to Asymptomatic Onset

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Artificial tears retained 45.82% of neurotrophic keratitis treatment market share in 2025. Their dominance stems from payer-driven step therapy that forces a 90-day trial before higher-cost biologics receive approval, a cycle that perpetuates volume within retail channels. The neurotrophic keratitis treatment market size tied to contact lens solutions is projected to climb at a 5.87% CAGR over 2026-2031 as BostonSight PROSE and EyePrint scleral devices migrate from salvage to first-line protection, establishing a fluid reservoir that shields damaged corneas while awaiting regenerative therapy authorization. Recombinant human nerve growth factor delivered USD 1 billion sales in 2024, yet its six-times-daily regimen and USD 118,230 price tag restrict broad uptake despite proven 84.6% closure rates in Chinese real-world data.

Antibiotics remain ancillary, prescribed prophylactically when defects exceed 2 mm, but they occupy a small revenue slice. Gene therapies are poised to displace chronic eye-drop regimens; Krystal Biotech's KB801 began dosing in July 2025 and uses a replication-defective HSV-1 vector to provide twice-weekly NGF expression, potentially redefining convenience standards. Should early data replicate cenegermin's healing outcomes, payer calculus could shift quickly, reducing artificial-tear dependence and altering how the neurotrophic keratitis treatment market evaluates cost-benefit thresholds.

Geography Analysis

North America commanded 38.95% of 2025 revenue in the neurotrophic keratitis treatment market, with Medicare Part D covering cenegermin despite 30-60-day prior authorization that elongates disease course. Canada's CADTH approval is conditional on steep discounts, limiting provincial uptake outside Quebec and Ontario. Mexico's private hospitals carry cenegermin for inbound medical tourists but domestic adoption stays muted due to out-of-pocket burden.

Europe lags North America in revenue yet benefits from an earlier EMA nod and Dompe's Italian distribution center. Germany's G-BA labeled cenegermin as conferring "additional benefit" yet is pressing for further rebates, and France imposes tight hospital caps on orphan-drug budgets. EU MDR 2017/745 has slowed U.S. device entry but spurred European tissue banks to scale, partly offsetting supply bottlenecks in amniotic membrane.

Asia-Pacific is forecast to grow fastest at a 5.71% CAGR, propelled by India's surging diabetes load and China's positive Phase IV rhNGF data that pave the way for NMPA clearance. Japan and South Korea await regulatory filings yet already perform neurotization with national insurance support, creating pent-up demand once rhNGF or gene therapy clears approval. Middle East and Africa remain constrained by testing gaps and reimbursement limits, whereas Brazil and Argentina show gradual uptake via private insurers.

- AxoGen, Inc.

- Bausch + Lomb

- BioTissue, Inc.

- BostonSight

- BRIM Biotechnology, Inc.

- CooperVision Specialty EyeCare / Blanchard

- Dompe farmaceutici S.p.A.

- EyePrint Prosthetics

- Katena Products / IOP Ophthalmics

- Krystal Biotech, Inc.

- Laboratoires Thea

- Recordati Rare Diseases / MimeTech S.r.l.

- RegeneRx Biopharmaceuticals, Inc.

- SynergEyes, Inc.

- Visionary Optics

- Vital Tears

- X-Cel Specialty Contacts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Access to Cenegermin (rhNGF) as First Approved NK Therapy

- 4.2.2 Rising NK Risk Factors (HSV/HZO, Diabetes) Expanding the Treatable Pool

- 4.2.3 Increased Diagnosis via Esthesiometry and In Vivo Confocal Microscopy

- 4.2.4 Wider Payer Recognition of Amniotic Membrane Devices in Refractory NK

- 4.2.5 Minimally Invasive/Endoscopic Corneal Neurotization Enabling Eligibility

- 4.2.6 Centralized Autologous Serum/PRP Supply Chains Improving Availability

- 4.3 Market Restraints

- 4.3.1 High Cost and Cost-Effectiveness Headwinds for rhNGF Therapy

- 4.3.2 Underdiagnosis and Late Presentation Due to Asymptomatic Early NK

- 4.3.3 Cold-Chain and Complex Administration Burden for rhNGF Eye Drops

- 4.3.4 Coverage Restrictions Delaying Amniotic Membrane Use Until Failure of SOC

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy Type

- 5.1.1 Drugs-Artificial Tears

- 5.1.2 Recombinant Human Nerve Growth Factors Eye Drops

- 5.1.3 Antibiotics

- 5.1.4 Contact Lens

- 5.2 By Disease Stage

- 5.2.1 Stage I

- 5.2.2 Stage II

- 5.2.3 Stage III

- 5.3 By Distribution Channel

- 5.3.1 Hospital pharmacies

- 5.3.2 Retail pharmacies

- 5.3.3 Online pharmacies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 AxoGen, Inc.

- 6.3.2 Bausch + Lomb

- 6.3.3 BioTissue, Inc.

- 6.3.4 BostonSight

- 6.3.5 BRIM Biotechnology, Inc.

- 6.3.6 CooperVision Specialty EyeCare / Blanchard

- 6.3.7 Dompe farmaceutici S.p.A.

- 6.3.8 EyePrint Prosthetics

- 6.3.9 Katena Products / IOP Ophthalmics

- 6.3.10 Krystal Biotech, Inc.

- 6.3.11 Laboratoires Thea

- 6.3.12 Recordati Rare Diseases / MimeTech S.r.l.

- 6.3.13 RegeneRx Biopharmaceuticals, Inc.

- 6.3.14 SynergEyes, Inc.

- 6.3.15 Visionary Optics

- 6.3.16 Vital Tears

- 6.3.17 X-Cel Specialty Contacts

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment