|

시장보고서

상품코드

2063812

LED 에피텍셜 웨이퍼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)LED Epitaxial Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

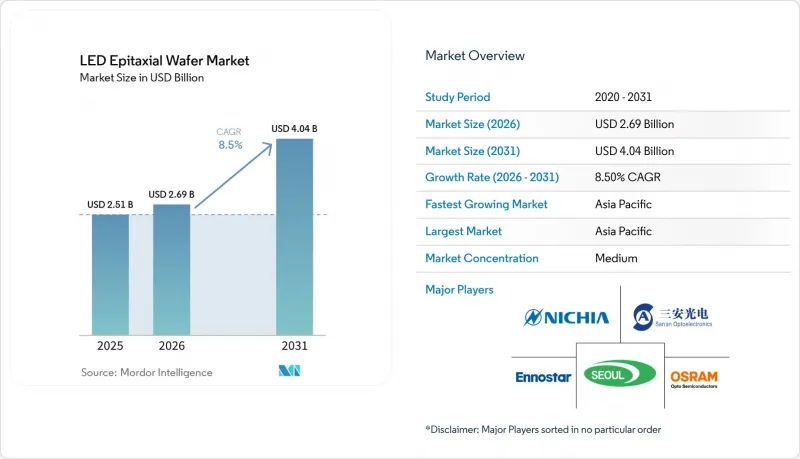

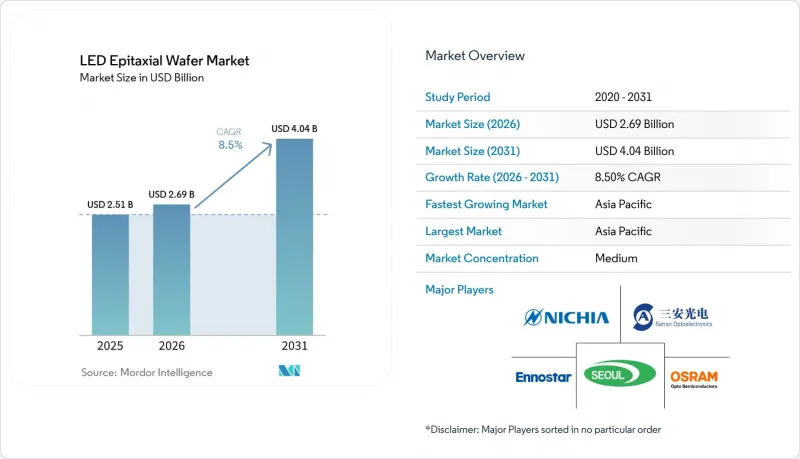

Mordor Intelligence에 의하면, LED 에피텍셜 웨이퍼 시장 규모는 2025년 25억 1,000만 달러로 평가되었습니다. 2026년 26억 9,000만 달러에서 2031년까지 40억 4,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 8.5%를 나타낼 것으로 예측됩니다.

본 보고서는 재료 시스템(GaN 기반 에피텍셜 웨이퍼, Al-In-Ga-N 기반 에피텍셜 웨이퍼 등), 기판 유형(사파이어, 실리콘 등), 웨이퍼 직경(100mm 이하, 150mm, 기타), 용도(일반 조명, 자동차용 조명 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 LED 에피텍셜 웨이퍼 시장 동향 및 분석

미니 LED 및 마이크로 LED 디스플레이 생산 확대

각 패널 제조업체들은 미니 LED 백라이트 및 직접 뷰형 마이크로 LED 프로젝트를 빠른 속도로 추진하고 있습니다. 이러한 프로젝트에서는 수천 개에 달하는 서브픽셀에 걸친 색상 편차를 줄이기 위해, 매우 정밀한 파장 비닝 처리가 적용된 웨이퍼가 필수적입니다. TCL CSOT는 Prima 지분의 80%를 보유함으로써, 1만 니트 비디오월용 웨이퍼를 월 6,000제곱미터 규모로 안정적으로 공급받고 있습니다. 한편, AUO의 4.5세대 생산라인은 삼성으로부터 114인치 TV 주문을 수주했으며, 소니 모빌리티용 차량용 패널 공급 계약을 확보했습니다.(1) 인피니온이 시제한 300mm GaN 샘플에서는 웨이퍼 1장당 칩 수가 2.3배로 증가했으며, 이는 규모의 경제가 디스플레이 등급의 균일성 목표와 어떻게 조화를 이루고 있는지를 보여줍니다.(2)

백열등을 단계적으로 폐지하는 정부의 에너지 효율 규제

미국 에너지부는 2028년 7월부터 시행될 ‘1와트당 120루멘’ 기준을 최종 확정했으며, 이에 따라 백열전구와 할로겐 전구가 사실상 금지됩니다. 미국 10개 주에서 시행 중인 소형 형광등 병행수입 금지 조치와 IEC 62717에 따른 엄격한 루멘 유지율 기준으로 인해, 조명 기구 OEM 제조업체들은 고효율 LED 모듈로의 전환을 강요받고 있으며, 결함이 없는 GaN 웨이퍼에 대한 수요가 증가하고 있습니다. 중국의 보조금 제도는 1와트당 130루멘을 초과하는 램프에 장려금을 지급하고 있으며, 국내 제조업체들은 재료 비용을 최소화할 수 있는 대구경 GaN-on-Si 라인으로의 전환을 추진하고 있습니다.

MOCVD 반응기 및 에피택시 장비에 대한 대규모 설비 투자

최신 200mm GaN MOCVD 챔버의 가격은 300만 달러 이상이며, 실용적인 생산 라인을 구축하려면 최소 10대의 챔버가 필요하기 때문에 신규 진입 장벽이 높아지고 있습니다. Veeco Instruments는 2026년 3월 Lumina의 신규 주문을 수주했는데, 이는 차세대 에피택시 장비에 대한 끊임없는 수요를 여실히 보여주고 있습니다. 그러나 12-18개월에 달하는 재인증 주기로 인해 투자 회수가 지연되고 있으며, 특히 인건비와 규정 준수 비용이 프로젝트 예산을 부풀리는 유럽과 미국에서는 이러한 현상이 두드러집니다. 따라서 중소규모 기업들은 틈새 파장 분야에 집중하거나, 과잉 생산 능력을 보유한 중국의 팹으로부터 생산 능력을 라이선스 받는 경향을 보이고 있습니다.

부문별 분석

GaN 기반 웨이퍼는 형광체 변환형 백색 램프, RGB 백라이트 및 자동차용 헤드램프용 청색 발광에 힘입어 2025년 시장 규모의 64.8%를 차지했습니다. AlGaN은 2025년 LED 에피텍셜 웨이퍼 시장 규모에서 미미한 비중을 차지하는 데 그쳤으나, 병원 및 공공 기관이 무수은 살균 기술을 의무화함에 따라 2031년까지 연평균 성장률(CAGR)이 11.14%를 기록하며 해당 부문 전체를 상회하는 속도로 성장하고 있습니다. HAI Solutions, Surfacide 및 UV Smart의 각 장치에 대한 FDA 승인은 좁은 밴드갭을 가진 AlGaN만이 충족할 수 있는 성능 기준을 설정하고 있습니다. GaN은 여전히 일반 조명 및 Mini-LED 백라이트 분야에서 루멘당 비용이 가장 낮으며, 70%의 매출 점유율을 유지하고 있습니다. AlInGaP는 자동차 신호등이나 옥외 간판 분야에서 여전히 중요한 위치를 차지하고 있지만, 재고 관리를 효율화하는 형광체 변환형 대체재로 인해 점진적인 대체가 진행되고 있습니다.

AlGaN 웨이퍼에는 30%를 초과하는 알루미늄 함유율이 필요하며, 이로 인해 격자 불일치가 악화되어 칩당 양자 효율이 3-5밀리와트로 떨어지기 때문에 통합 제조업체들은 멀티칩 어레이 설계를 채택할 수밖에 없습니다. GaN 공급업체들은 공정 성숙도와 MOCVD 시스템의 방대한 도입 실적을 무기로, 시장 점유율을 지키기 위한 적극적인 가격 전략을 펼치고 있습니다. 서울세미컨덕터가 보유한 풍부한 특허를 바탕으로 한 WICOP 플랫폼은 와이어 본딩이 필요 없는 GaN 칩을 채택하여, 자동차용 Mini-LED 클러스터의 방열 경로를 개선하고 있습니다. AlInGaP의 미래는 특수한 원적외선 원예용 조명 기구와, 직접적인 적색 발광을 통해 스토크스 손실을 피할 수 있는 광통신 모듈에 달려 있습니다.

사파이어사는 결정 품질과 확립된 연마 공정 덕분에 2025년 매출의 57.54%를 유지했으나, 200mm GaN-on-Si 슬라이스가 한 번의 제조 과정에서 2.3배 많은 다이를 생산하여 루멘당 비용을 대폭 절감함에 따라, 실리콘이 그 격차를 좁혀가고 있습니다. 2025년에 웨이퍼 관세를 50%로 두 배로 인상한 섹션 301 관세로 인해, 북미의 통합 기업들은 현지 실리콘 공급업체로 전환하기 시작했으며, 이러한 전환이 가속화되었습니다. 실리콘 기반 GaN은 직경 200mm라는 큰 크기, 낮은 웨이퍼 원가, 기존 CMOS 팹과의 호환성을 제공하며, 사파이어의 성장률을 능가하는 12.36%의 연평균 성장률(CAGR)을 뒷받침하는 유력한 경쟁자입니다. 실리콘 카바이드는 웨이퍼 가격이 500-1,000달러로 고가임에도 불구하고, 극한의 전류 밀도가 요구되는 고출력 프로젝터나 의료용 내시경 분야에서 뛰어난 열전도성이 높이 평가되어 프리미엄 수요를 확보하고 있습니다.

GaN-on-Si는 수율에 영향을 미치는 뒤틀림(bow) 문제에 직면해 있지만, 범용 전구의 설계 여유 범위 내에서는 70%의 다이 이용률도 허용됩니다. 사파이어는 가혹한 열 사이클을 견뎌내는 자동차용 및 실외용 조명 기구에서 뛰어난 성능을 발휘합니다. 실리콘 카바이드는 미션 크리티컬한 용도에서 여전히 틈새 시장용이긴 하지만 없어서는 안 될 선택지입니다. AlInGaP-on-GaAs가 GaN 플랫폼으로 전환됨에 따라, 갈륨 비소 생산량은 감소하고 있습니다. 이를 통해 공통 기판 위에 다색 모듈을 배치함으로써 패키지 통합을 간소화하고 있습니다.

지역별 분석

아시아태평양은 2025년에 LED 에피텍셜 웨이퍼 시장 매출의 73%를 차지했으며, 중국, 대만, 한국의 클러스터가 보조금 프로그램 하에서 MOCVD 장비군을 확대함에 따라 2031년까지 연평균 성장률(CAGR) 11.35%를 유지할 전망입니다. 중국 공업정보화부는 1와트당 130루멘을 초과하는 램프에 대해 환급금을 지급하고 있으며, 재료 비용을 절감하기 위해 사파이어에서 GaN-on-Si로의 전환을 가속화하고 있습니다. 대만의 에피스타(Epistar)와 렉스타(Lextar)는 웨이퍼 성장과 다운스트림 공정인 패키징 및 미니 LED 패널 조립을 결합한 통합 허브의 중심에 자리 잡고 있습니다. 한국의 삼성과 LG이노텍은 차세대 TV 및 자동차용 디스플레이와 관련된 마이크로 LED 시범 생산 라인에 투자하고 있습니다.

북미 시장 점유율은 다소 낮지만, 항공우주, 방위, 의료기기 분야의 프리미엄 가격 덕분에 상대적으로 큰 비중을 차지하고 있습니다. 2025년 1월에 발효된 섹션 301 관세로 인해 웨이퍼 수입 관세가 두 배로 증가함에 따라, 각 통합 제조업체들은 가격 변동 위험을 헤지하기 위해 국내산 실리콘 슬라이스를 조달하거나 장기 사파이어 계약을 협상하고 있습니다. 미국 에너지부가 2028년에 도입할 예정인 효율 기준에 따라, 주거용 및 상업용 조명 기기의 지속적인 교체 주기가 보장됨에 따라 고효율 GaN 웨이퍼 수요는 견조한 추세를 보일 전망입니다.

유럽도 비슷한 길을 걷고 있으며, EU는 할로겐 램프의 단계적 폐지를 완료하는 동시에, 에코디자인 지침에 따라 커넥티드 조명을 추진하고 있습니다. 독일과 프랑스의 자동차 제조업체들은 ECE 빔 패턴 기준을 충족하기 위해 결함이 없는 웨이퍼가 필요한 매트릭스 헤드램프 주문을 앞당기고 있습니다. 중동의 수직 농장, 남미의 상수도 유틸리티, 아프리카의 Off-grid 태양광 발전 설비가 주도하는 세계 기타 지역은 아직 발전 단계에 있지만 유망한 신흥 시장이며, 비용 중시 경향으로 인해 GaN-on-Si 기판이나 지역 기후 제약에 맞추어 조정된 소구경 AlGaN 웨이퍼가 선호되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the lED epitaxial wafer market size is projected to expand from USD 2.51 billion in 2025 and USD 2.69 billion in 2026 to USD 4.04 billion by 2031, registering an 8.5% CAGR between 2026 and 2031.

This report is Segmented by Material System (GaN-Based Epitaxial Wafers, Alingap Epitaxial Wafers, and More), Substrate Type (Sapphire, Silicon, and More), Wafer Diameter (Up To 100 Mm, 150 Mm, and More), Application (General Lighting, Automotive Lighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global LED Epitaxial Wafer Market Trends and Insights

Proliferation of Mini and Micro-LED Display Manufacturing

Panel makers are fast-tracking Mini-LED backlighting and direct-view Micro-LED projects, which depend on wafers with extremely tight wavelength binning to reduce color shift across thousands of sub-pixels. TCL CSOT's 80% stake in Prima secures 6,000 square-meter monthly wafer supply for 10,000-nit video walls, while AUO's 4.5-generation line has locked 114-inch television orders from Samsung and in-vehicle panels for Sony Mobility.[1] Infineon's 300 millimeter GaN sample run delivered 2.3 times more chips per wafer, illustrating how scale economics are converging with display-grade uniformity targets.[2]

Government Energy-Efficiency Regulations Phasing Out Incandescent Lighting

The United States Department of Energy finalized a 120 lumens-per-watt mandate that takes effect in July 2028, effectively prohibiting incandescent and halogen bulbs. Parallel bans on compact fluorescents in ten U.S. states and strict lumen-maintenance rules under IEC 62717 are pushing fixture OEMs toward high-efficacy LED modules, boosting demand for defect-free GaN wafers. China's subsidy program rewards >130 lumens-per-watt lamps, steering domestic makers toward large-diameter GaN-on-Si lines that minimize material cost.

High Capital Expenditure for MOCVD Reactors and Epitaxy Tools

A modern 200 millimeter GaN MOCVD chamber costs upward of USD 3 million, and a viable line requires at least ten chambers, lifting entry barriers for new ventures. Veeco Instruments booked fresh Lumina orders in March 2026 that highlight the constant need for next-generation epitaxy hardware, yet the 12-18 month re-qualification cycle postpones payback, especially in Europe and the United States, where labor and compliance inflate project budget. Smaller firms, therefore, gravitate toward niche wavelengths or license capacity from over-built Chinese fabs.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of UV-C LED Diodes for Disinfection Post-COVID-19

- Automotive Headlamp Migration to Matrix LED and ADB Systems

- Yield Challenges for Larger (200 mm) GaN Wafers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GaN-based wafers captured 64.8% of the 2025 value, underpinned by blue emission for phosphor-converted white lamps, RGB backlights, and automotive headlamps. AlGaN accounted for a modest portion of the LED epitaxial wafer market size in 2025, yet its 11.14% CAGR through 2031 outpaces the sector as hospitals and utilities mandate mercury-free sterilization technologies. FDA clearances for HAI Solutions, Surfacide, and UV Smart devices set performance bars that only tight-bandgap AlGaN can meet. GaN still delivers the lowest cost per lumen for general illumination and Mini-LED backlights, protecting a 70% revenue share. AlInGaP maintains relevance in automotive signaling and outdoor signage, but faces gradual substitution by phosphor-converted alternatives that streamline inventory.

AlGaN wafers require aluminum fractions exceeding 30%, which exacerbates lattice mismatch and lowers quantum efficiency to 3-5 milliwatts per chip, obligating integrators to design multi-chip arrays. GaN suppliers counter with process maturity and a vast installed base of MOCVD systems, enabling aggressive price moves that defend share. Seoul Semiconductor's patent-rich WICOP platform uses GaN chips without wire bonds, improving thermal paths for automotive Mini-LED clusters. AlInGaP's future rests on specialized far-red horticultural fixtures and light-based communication modules where direct red output avoids Stokes losses.

Sapphire retained 57.54% of 2025 revenue thanks to crystalline quality and established polishing routes, yet silicon is closing the gap as 200 millimeter GaN-on-Si slices deliver 2.3 times more die per run, slashing cost per lumen. Section 301 tariffs that doubled wafer duties to 50% in 2025 nudged North American integrators toward local silicon suppliers, accelerating adoption. Silicon-based GaN is the natural challenger, offering a larger 200 mm diameter, lower raw-wafer cost, and compatibility with existing CMOS fabs, underpinning a 12.36% CAGR that overtakes sapphire growth. Silicon carbide earns premium demand in high-power projectors and medical scopes where extreme current densities warrant its superior thermal conductivity, despite USD 500-1,000 wafer prices.

GaN-on-Si experiences bow challenges that hit yields, but design margins in commodity bulbs tolerate 70% die utilization. Sapphire excels in automotive and outdoor luminaires that endure harsh thermal cycling. Silicon carbide remains a niche yet vital option for mission-critical applications. Gallium arsenide volumes are declining as AlInGaP-on-GaAs migrates to GaN platforms, aligning multi-color modules on a common substrate to simplify package integration.

Geography Analysis

Asia-Pacific generated 73% of the LED epitaxial wafer market revenue in 2025 and will maintain an 11.35% CAGR through 2031 as Chinese, Taiwanese, and South Korean clusters scale MOCVD fleets under subsidy programs. China's Ministry of Industry and Information Technology offers rebates for lamps above 130 lumens per watt, hastening the transfer from sapphire to GaN-on-Si to trim material cost. Taiwan's Epistar and Lextar anchor an integrated hub that pairs wafer growth with downstream packaging and Mini-LED panel assembly. South Korea's Samsung and LG Innotek channel investment into Micro-LED pilot lines tied to next-generation televisions and automotive displays.

North America accounts for a modest share yet captures outsized value on premium pricing for aerospace, defense, and medical devices. Section 301 tariffs that took effect in January 2025 doubled wafer import duties, prompting integrators to source domestic silicon slices or negotiate long-term sapphire contracts to hedge volatility. The United States Department of Energy's looming 2028 efficacy mandate ensures a continued replacement cycle in residential and commercial fixtures, keeping demand for high-efficiency GaN wafers resilient.

Europe follows a similar path as the EU completes its halogen phase-out while championing connected lighting under Ecodesign directives. German and French automakers front-load orders for matrix headlamps that need defect-free wafers to satisfy ECE beam patterns. Rest of the World, led by Middle East vertical farms, South American water utilities, and African off-grid solar installations, remains a nascent but promising frontier where cost sensitivity favors GaN-on-Si substrates and small-diameter AlGaN wafers tailored to regional climate constraints.

- Nichia Corporation

- Osram Opto Semiconductors GmbH

- Ennostar Corporation

- San'an Optoelectronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, a division of Smart Global Holdings, Inc.

- Lumileds Holding B.V.

- LG Innotek Co., Ltd.

- HC Semitek Corporation

- Samsung Electronics Co., Ltd. (LED Business)

- Genesis Photonics Inc.

- Lextar Electronics Corporation

- Aledia SA

- Plessey Semiconductors Ltd.

- Bridgelux, Inc.

- II-VI Incorporated

- Opto Tech Corporation

- Changelight Co., Ltd.

- Epileds Technologies Inc.

- Toyoda Gosei Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Mini and Micro-LED Display Manufacturing

- 4.2.2 Government Energy-Efficiency Regulations Phasing Out Incandescent Lighting

- 4.2.3 Rapid Adoption of UV-C LED Diodes for Disinfection Post-COVID-19

- 4.2.4 Automotive Headlamp Migration to Matrix LED and ADB Systems

- 4.2.5 Surge in Demand for Horticultural Lighting in Controlled-Environment Agriculture

- 4.2.6 Expansion of GaN-on-Si Technology Lowering Cost per Lumen

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for MOCVD Reactors and Epitaxy Tools

- 4.3.2 Yield Challenges for Larger (200 mm) GaN Wafers

- 4.3.3 Supply Chain Dependence on Limited Sapphire Substrate Suppliers

- 4.3.4 Intense Price Erosion Squeezing Mid-Tier Manufacturers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material System

- 5.1.1 GaN-based Epitaxial Wafers

- 5.1.2 AlInGaP Epitaxial Wafers

- 5.1.3 AlGaN Epitaxial Wafers

- 5.2 By Substrate Type

- 5.2.1 Sapphire

- 5.2.2 Silicon

- 5.2.3 Silicon Carbide (SiC)

- 5.2.4 Gallium Arsenide (GaAs)

- 5.3 By Wafer Diameter

- 5.3.1 Upto 100 mm

- 5.3.2 150 mm

- 5.3.3 200 mm and Above

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.2 Automotive Lighting

- 5.4.3 Displays and Backlighting

- 5.4.4 UV Sterilization

- 5.4.5 Industrial and Specialty Lighting

- 5.5 By Geography

- 5.5.1 North America

- 5.5.2 Europe

- 5.5.3 Asia-Pacific

- 5.5.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Osram Opto Semiconductors GmbH

- 6.4.3 Ennostar Corporation

- 6.4.4 San'an Optoelectronics Co., Ltd.

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Cree LED, a division of Smart Global Holdings, Inc.

- 6.4.7 Lumileds Holding B.V.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 HC Semitek Corporation

- 6.4.10 Samsung Electronics Co., Ltd. (LED Business)

- 6.4.11 Genesis Photonics Inc.

- 6.4.12 Lextar Electronics Corporation

- 6.4.13 Aledia SA

- 6.4.14 Plessey Semiconductors Ltd.

- 6.4.15 Bridgelux, Inc.

- 6.4.16 II-VI Incorporated

- 6.4.17 Opto Tech Corporation

- 6.4.18 Changelight Co., Ltd.

- 6.4.19 Epileds Technologies Inc.

- 6.4.20 Toyoda Gosei Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment