|

시장보고서

상품코드

2063821

VRAM : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)VRAM - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

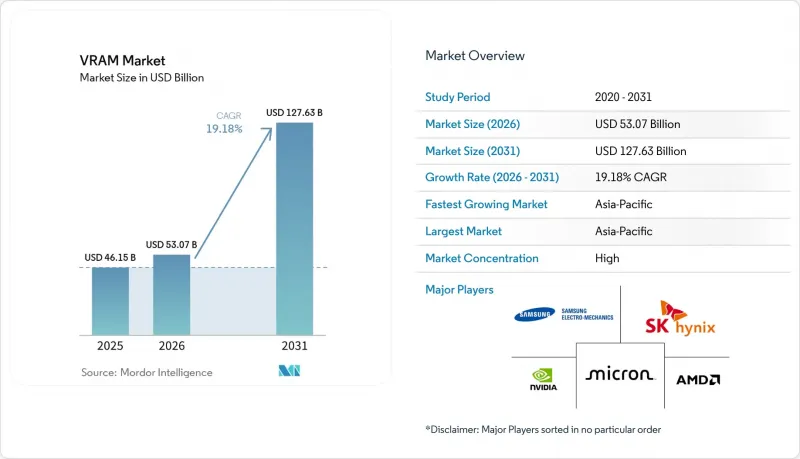

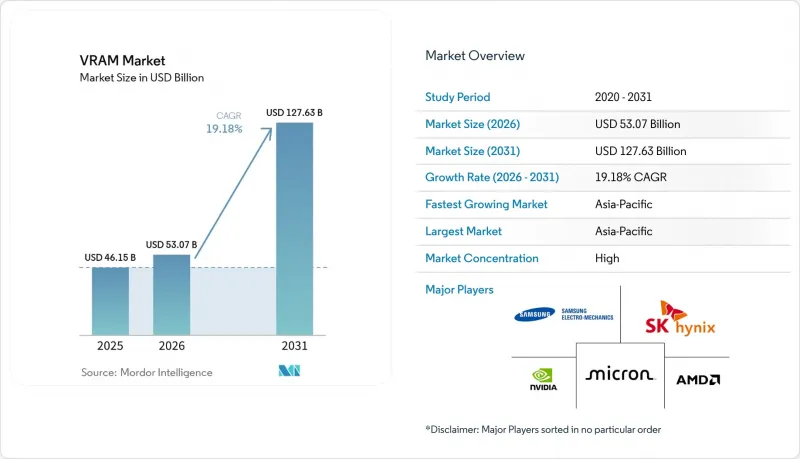

Mordor Intelligence에 의하면, VRAM 시장 규모는 2025년에 461억 5,000만 달러로 평가되었습니다. 2026년 530억 7,000만 달러에서 2031년까지 1,276억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 19.18%를 나타낼 전망입니다.

본 보고서는 메모리 아키텍처(GDDR 기반 VRAM 및 HBM 기반 VRAM), VRAM 용량(8GB 이하, 8-16GB, 16-32GB, 32-64GB, 64GB 이상), 용도(게임, 데이터센터 및 AI, 전문 시각화, 엣지 AI 및 임베디드), 그리고 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

세계의 VRAM 시장 동향 및 인사이트

하이퍼스케일 데이터센터에서 AI 훈련 워크로드의 폭발적인 증가

대규모 언어 모델이 점점 더 복잡해짐에 따라, 모든 플래그십 가속기에는 더 대규모의 HBM 스택 통합이 요구되고 있습니다. 현재 단일 하이엔드 GPU에는 로직 다이보다 더 비싼 메모리가 탑재되어 있으며, 클라우드 제공업체들이 수년에 걸쳐 용량을 예약함에 따라 스팟 시장의 유연성은 상실되었습니다. 그 결과 발생한 수요 급증은 메모리 제조업체들에게 지속적인 가격 결정력을 부여하여, VRAM 시장을 기존의 DRAM 시장의 호황과 불황의 변동에서 분리시키고 있습니다. 따라서 AI급 데이터센터에 대한 설비 투자는 HBM 제조업체들에게 장기적인 수익 전망을 더욱 견고하게 만들어 주고 있습니다.

4K/8K 게이밍 및 레이 트레이싱 GPU의 대중화

현재 소비자용 GPU는 초고해상도 텍스처나 레이 트레이싱 가속을 위한 데이터 구조를 버퍼링해야 하기 때문에 이에 따라 기본 사양의 그래픽 카드 용량은 16GB 이상으로 늘어났습니다. 콘솔 제품 주기의 중반에 이루어지는 모델 업데이트가 GDDR 출하량을 지탱하는 한편, 워크스테이션용 모델의 경우 실시간 엔지니어링 워크로드를 처리하기 위해 해당 기술을 96GB까지 확장하고 있습니다. HBM 공급 부족으로 인해 공급업체들은 수익성이 높은 스택을 우선적으로 공급할 수밖에 없게 되었고, 이는 간접적으로 GDDR 공급 부족을 초래하여 2027년 말까지 견조한 가격 유지에 기여하고 있습니다.

HBM 공급 병목 현상과 팹 리드타임 장기화

적층 메모리를 위한 첨단 패키징 기술은 여전히 시장에서 가장 큰 병목 현상으로 남아 있습니다. 이 문제를 해결하기 위한 신규 시설 건설에는 2년 가까이 소요되며, 그 후 고객 인증 절차에 6개월 이상이 추가로 소요됩니다. 이처럼 일정이 장기화되면서, 업계가 생산 능력 확대를 위해 사상 최고 수준의 설비 투자를 진행하고 있음에도 불구하고 공급 부족 현상이 계속되고 있습니다. 게다가, 최신 HBM3E 레이어에서 확인된 70% 미만의 수율이 생산 리스크를 악화시키고 있습니다. 설상가상으로, 고성능 수요에 부응하기 위해 GDDR에서 HBM으로 웨이퍼 생산을 전환함에 따라 중급 GPU공급이 더욱 부족해져 시장에 또 다른 문제를 야기하고 있습니다.

부문별 분석

HBM 탑재 기기는 2025년 출하 대수에서 차지하는 비중은 작았으나, 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 19.38%라는 최고 수준의 성장세를 기록할 것으로 전망됩니다. 이러한 성장 추세는 하이퍼스케일 AI 플랫폼이 복잡한 워크로드와 대규모 데이터 처리를 수행하기 위해 필수적인 테라바이트급 대역폭을 우선시하고 있음을 반영합니다. 이러한 플랫폼들은 HBM이 가져다주는 획기적인 성능 향상 덕분에 기가바이트당 비용 상승을 감수할 의향이 있음을 보여주고 있습니다. 삼성은 2026년에 상용 HBM4 출하를 시작하여 스택당 3.3 TB/s를 달성했습니다. 이로 인해 GDDR 대체 제품과의 성능 격차가 크게 벌어졌으며, 고성능 컴퓨팅 분야에서 HBM의 입지가 더욱 공고해졌습니다.

GDDR 기술은 여전히 62.73%의 시장 점유율을 유지하고 있으며, 데스크톱 게임, 전문가용 시각화, 그리고 급속히 확대되고 있는 8K 컨텐츠 제작 수요와 같은 분야에서 여전히 필수적인 역할을 하고 있습니다. GDDR7의 최대 32 Gbps 전송 속도가 도입됨에 따라, 이 기술의 유용성은 더욱 확대될 것이며, 비용과 성능을 모두 중시하는 시장에서 지속적인 채택이 보장될 것입니다. 비디오용 랜덤 액세스 메모리 시장의 이러한 다양화로 인해 HBM에 의한 시장 독점이 방지되고, 고성능 솔루션과 비용 효율적인 솔루션 간의 균형이 유지되고 있습니다.

지역별 분석

아시아태평양은 VRAM 공급망의 제조 거점으로서 지배적인 위치를 차지하고 있으며, 2025년에는 매출 점유율의 67.17%를 차지했습니다. 이 지역은 한국 및 대만의 파운드리 기업들로부터 막대한 투자의 혜택을 받고 있으며, 이들 기업은 2026년까지 1,000억 달러 이상을 투자해 HBM 클린룸 시설 및 첨단 패키징 역량 확충을 추진하고 있습니다. 이러한 노력을 통해 해당 지역은 20.14%라는 견실한 예상 연평균 성장률(CAGR)을 유지할 수 있을 것으로 전망됩니다. 또한, 인도와 동남아시아 국가들의 AI 인프라가 급속히 발전함에 따라 현지 소비를 견인하고 있으며, 이는 수출 주도형 성장을 더욱 뒷받침할 뿐만 아니라 세계의 VRAM 시장에서 해당 지역의 리더십을 공고히 하고 있습니다.

북미는 국내 DRAM 웨이퍼 생산량이 극히 적음에도 불구하고, 하이퍼스케일 기업의 수입을 포함하면 최대 소비 지역으로 부상하고 있습니다. 150억 달러 이상의 보조금과 대출을 제공하는 ‘CHIPS법’은 해당 지역 내 웨이퍼 및 패키징 생산 능력의 현지화를 목표로 하고 있습니다. 그러나 2028년까지는 생산량이 크게 증가할 것으로 예상되지 않습니다. SK하이닉스는 인디애나주에 첨단 패키징 시설을 설립하기 위해 4억 5,800만 달러의 보조금과 최대 5억 달러의 대출을 확보했습니다. 이는 리드 타임을 단축하여 미국의 하이퍼스케일러에 서비스를 제공하는 것을 목적으로, HBM의 조립 및 테스트 역량을 확충하는 것을 목표로 하고 있습니다. 한편, 북미의 클라우드 서비스 제공업체들은 여전히 태평양을 가로지르는 공급망에 크게 의존하고 있어, 지정학적 긴장으로 인한 혼란의 영향을 받기 쉬운 상황에 놓여 있습니다. 이러한 의존 관계는 잠재적 위험을 줄이기 위해 공급원을 다각화하는 것이 얼마나 중요한지를 여실히 보여주고 있습니다.

유럽은 제조 능력 면에서 뒤처져 있지만, 자동차용 첨단 운전자 보조 시스템(ADAS)이나 산업용 로봇 등의 분야에서 VRAM에 대한 수요가 증가하고 있습니다. ‘유럽 칩법’과 같은 노력을 통해 현지 시범 생산 라인 구축을 위한 자금이 배정되고 있지만, 본격적인 HBM 생산이 이루어지지 않고 있어 해당 지역이 세계 공급망에 기여하는 정도는 여전히 제한적입니다. 한편, 남미 및 중동 및 아프리카은 주로 게임 및 초급 전문가용 워크로드 수요에 힘입어, 공급량은 비교적 적음에도 불구하고 세계 VRAM 시장에서 꾸준한 성장을 보이고 있으며, 업계 동향에서 입지를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the vRAM market size was valued at USD 46.15 billion in 2025 and is estimated to grow from USD 53.07 billion in 2026 to reach USD 127.63 billion by 2031, at a CAGR of 19.18% during the forecast period (2026-2031).

This report is Segmented by Memory Architecture (GDDR-Based VRAM, and HBM-Based VRAM), VRAM Capacity (≤8 GB, 8-16 GB, 16-32 GB, 32-64 GB, and Above 64 GB), Application (Gaming, Data Center and AI, Professional Visualization, and Edge AI and Embedded), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global VRAM Market Trends and Insights

Explosive AI Training Workloads in Hyperscale Data Centers

Rising complexity in large language models is forcing every flagship accelerator to integrate ever-larger HBM stacks. A single high-end GPU now carries memory that costs more than its logic die, and multi-year capacity reservations by cloud providers have removed spot-market flexibility. The resulting demand shock gives memory makers durable pricing power and decouples the VRAM market from historic DRAM boom-bust swings. Capital spending on AI-class data centers, therefore, reinforces long-run revenue visibility for HBM producers.

Mainstream Adoption of 4K/8K Gaming and Ray-Tracing GPUs

Consumer GPUs must now buffer ultra-high-resolution textures and ray-tracing acceleration data structures, lifting baseline card capacities to 16 GB and above. Mid-cycle console refreshes sustain a floor under GDDR shipments, while workstation variants stretch the same technology to 96 GB for real-time engineering workloads. Tight HBM supply is pushing suppliers to prioritize higher-margin stacks, indirectly tightening GDDR availability and supporting firm pricing through late 2027.

Persistent HBM Supply Bottlenecks and Long Fab Lead-Times

Advanced packaging capacity for stacked memory remains the most significant bottleneck in the market. Building new facilities to address this issue takes nearly 2 years, followed by an additional 6 months or more for customer qualification processes. This prolonged timeline has resulted in persistent shortages, even as the industry records record levels of capital investment to expand capacity. Furthermore, sub-70% yields observed in the latest HBM3E layers exacerbate production risks. To make matters worse, reallocating wafer starts from GDDR to HBM to meet high-performance demands has further constrained the availability of mid-range GPUs, creating additional challenges for the market.

Other drivers and restraints analyzed in the detailed report include:

- Transition to GDDR7 and HBM3E Memory Standards

- Edge AI Growth in Automotive ADAS and Industrial Robots

- High Cost Differential Between HBM and Conventional GDDR

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

HBM-based devices accounted for a smaller share of shipments in 2025, yet are forecast to post a leading 19.38% CAGR between 2026 and 2031. This growth trajectory reflects hyperscale AI platforms' prioritization of terabyte-scale bandwidth, which is critical for handling complex workloads and large-scale data processing. These platforms are willing to absorb the higher cost per gigabyte due to the significant performance benefits HBM offers. Samsung began commercial HBM4 shipments in 2026, delivering 3.3 TB/s per stack, significantly widening the performance gap over GDDR alternatives and further solidifying HBM's position in high-performance computing applications.

GDDR technology, while still holding 62.73% market share, remains indispensable for applications such as desktop gaming, professional visualization, and the rapidly growing demand for 8K content creation. The introduction of GDDR7, with its up to 32 Gbps transfer rates, extends the technology's relevance and ensures its continued adoption in cost-sensitive and performance-driven markets. This diversification within the video random access memory market prevents HBM from monopolizing the segment, maintaining a balance between high-performance and cost-effective solutions.

Geography Analysis

Asia-Pacific holds a dominant position as the manufacturing backbone of the VRAM supply chain, accounting for 67.17% of the revenue share in 2025. The region benefits from the significant investments made by Korean and Taiwanese foundries, which are allocating over USD 100 billion in 2026 to expand HBM clean-room facilities and advanced packaging capabilities. These efforts are expected to help the region maintain a robust forecasted CAGR of 20.14%. Additionally, the rapid development of AI infrastructure in countries like India and Southeast Asia is driving local consumption, further supporting export-led growth and solidifying the region's leadership in the global VRAM market.

North America, despite having minimal domestic DRAM wafer production, emerges as the largest consumer block when hyperscale imports are included. The CHIPS Act, which provides over USD 15 billion in grants and loans, aims to localize wafer and packaging capacity within the region. However, significant production volumes are not anticipated before 2028. SK hynix secured USD 458 million in grants and up to USD 500 million in loans to establish an advanced packaging facility in Indiana, targeting HBM assembly and test capacity to serve U.S. hyperscalers with reduced lead times. In the meantime, North American cloud providers remain heavily dependent on trans-Pacific supply chains, which are susceptible to disruptions caused by geopolitical tensions. This reliance underscores the importance of diversifying supply sources to mitigate potential risks.

Europe, while lagging in fabrication capabilities, is witnessing a growing demand for VRAM in applications such as automotive advanced driver-assistance systems (ADAS) and industrial robotics. Initiatives like the European Chips Act have allocated funding to establish local pilot production lines, but the absence of full-scale HBM production continues to limit the region's contribution to the global supply chain. Meanwhile, South America and the Middle East and Africa contribute smaller volumes, primarily driven by demand in gaming and entry-level professional workloads. Although these regions exhibit relatively modest growth, they maintain steady progress within the global VRAM market, ensuring their relevance in the broader industry landscape.

- Samsung Electronics Co. Ltd.

- SK Hynix Inc.

- Micron Technology Inc.

- NVIDIA Corporation

- Advanced Micro Devices Inc.

- Intel Corporation

- Qualcomm Technologies Inc.

- Taiwan Semiconductor Manufacturing Company Limited

- GLOBALFOUNDRIES Inc.

- ASE Technology Holding Co. Ltd.

- Rambus Inc.

- Cadence Design Systems Inc.

- Synopsys Inc.

- Winbond Electronics Corporation

- ChangXin Memory Technologies Inc.

- Nanya Technology Corporation

- Powerchip Semiconductor Manufacturing Corp.

- GigaDevice Semiconductor Inc.

- Arm Limited

- Kioxia Corporation

- Broadcom Inc.

- Marvell Technology Inc.

- IBM Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive AI Training Workloads in Hyperscale Data Centers

- 4.2.2 Mainstream Adoption of 4K/8K Gaming and Ray-Tracing GPUs

- 4.2.3 Transition to GDDR7 and HBM3E Memory Standards

- 4.2.4 Edge AI Growth in Automotive ADAS and Industrial Robots

- 4.2.5 Government CHIPS Incentives Accelerating Domestic Memory Fabs

- 4.2.6 On-Package Compute-in-Memory Architectures Reducing Latency

- 4.3 Market Restraints

- 4.3.1 Persistent HBM Supply Bottlenecks and Long Fab Lead-Times

- 4.3.2 High Cost Differential Between HBM and Conventional GDDR

- 4.3.3 Geopolitical Export Controls on Advanced Memory Technologies

- 4.3.4 Integrated Graphics Performance Cannibalizing Entry-Level GPUs

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Memory Architecture

- 5.1.1 GDDR-based VRAM

- 5.1.2 HBM-based VRAM

- 5.2 By VRAM Capacity

- 5.2.1 <= 8 GB

- 5.2.2 8-16 GB

- 5.2.3 16-32 GB

- 5.2.4 32-64 GB

- 5.2.5 Above 64 GB

- 5.3 By Application

- 5.3.1 Gaming

- 5.3.2 Data Center and AI

- 5.3.3 Professional Visualization

- 5.3.4 Edge AI and Embedded

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Southeast Asia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Samsung Electronics Co. Ltd.

- 6.4.2 SK Hynix Inc.

- 6.4.3 Micron Technology Inc.

- 6.4.4 NVIDIA Corporation

- 6.4.5 Advanced Micro Devices Inc.

- 6.4.6 Intel Corporation

- 6.4.7 Qualcomm Technologies Inc.

- 6.4.8 Taiwan Semiconductor Manufacturing Company Limited

- 6.4.9 GLOBALFOUNDRIES Inc.

- 6.4.10 ASE Technology Holding Co. Ltd.

- 6.4.11 Rambus Inc.

- 6.4.12 Cadence Design Systems Inc.

- 6.4.13 Synopsys Inc.

- 6.4.14 Winbond Electronics Corporation

- 6.4.15 ChangXin Memory Technologies Inc.

- 6.4.16 Nanya Technology Corporation

- 6.4.17 Powerchip Semiconductor Manufacturing Corp.

- 6.4.18 GigaDevice Semiconductor Inc.

- 6.4.19 Arm Limited

- 6.4.20 Kioxia Corporation

- 6.4.21 Broadcom Inc.

- 6.4.22 Marvell Technology Inc.

- 6.4.23 IBM Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment