|

시장보고서

상품코드

2063832

인실리코 신약 개발 분야 인공지능(AI) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI In In-Silico Drug Development - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

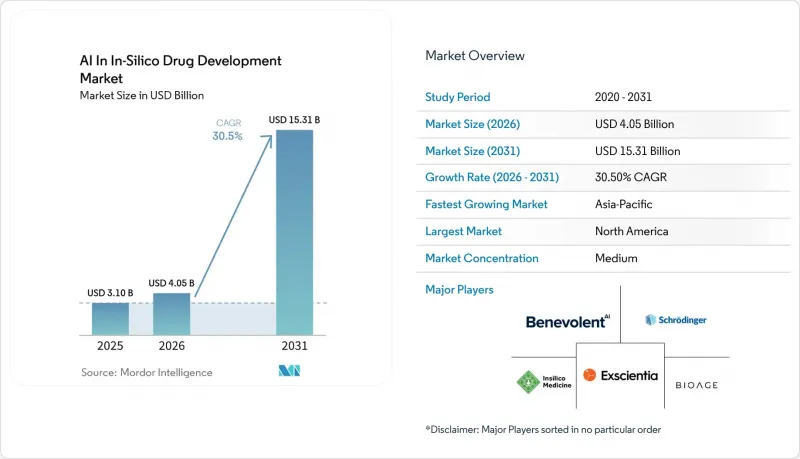

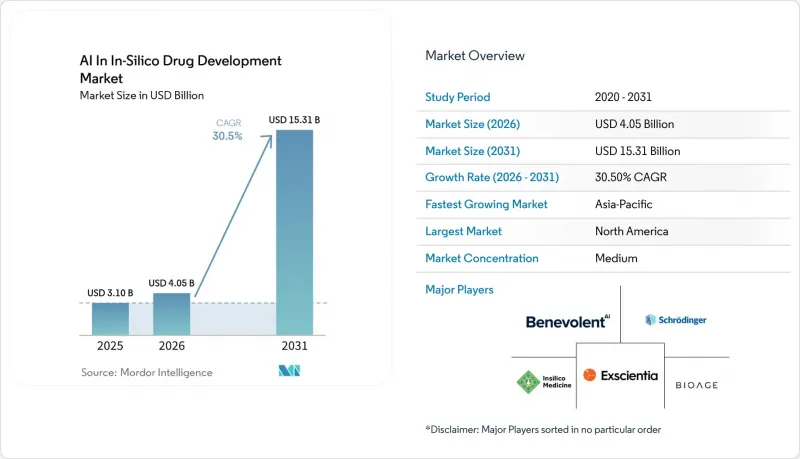

Mordor Intelligence에 의하면, 인실리코 신약 개발 분야 인공지능(AI) 시장 규모는 2025년 31억 달러로 평가되었습니다. 2026년에는 40억 5,000만 달러로 확대되어 2031년까지 153억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 30.5%를 나타낼 것으로 전망됩니다.

본 보고서는 개발 단계(표적 특정, 유망 화합물 발견, 랜드모어), AI 기술(머신러닝, 딥러닝 등), 약물 유형(저분자 화합물, 바이오의약품, 기타), 치료 분야(종양학, 신경학 등), 최종 사용자(제약·바이오기술, CRO, 학술 기관), 배포 방식(클라우드, On-Premise), 지역(북미 등)에 따라 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 인실리코 신약 개발 분야 인공지능(AI) 시장 동향 및 인사이트

클라우드 네이티브 고성능 컴퓨팅이 보급되면서

탄력적인 GPU 클러스터에 대한 광범위한 접근 덕분에 AI 연구에 따른 경제적 장벽이 낮아지고 있습니다. 여러 제약사에서 도입해 운영 중인 NVIDIA의 BioNeMo는 대규모 단백질 언어 모델의 훈련 시간을 절반으로 줄이고, 추론 속도를 6배로 높였습니다. 한편, 덴마크의 Gefion 슈퍼컴퓨터를 통해 Orbis Medicines는 불과 며칠 만에 1,400억 개의 매크로사이클을 분석할 수 있었습니다. 온디맨드형 인프라로의 전환에 따라 고정 자본 지출이 변동비로 전환됨에 따라, 중견 바이오기술 기업도 수십억 분자 규모의 가상 스크리닝을 수행할 수 있게 되었습니다. 이는 5년 전까지만 해도 상위 10개 제약사에만 국한되었던 역량입니다. 2026년 4월에 시작될 예정인 FDA의 시범 프로그램에서는 아스트라제네카와 앰젠의 임상시험에서 얻은 실시간 클라우드 데이터를 활용했으며, 이를 통해 관리 프로세스의 효율을 20-40% 높였습니다. 이러한 비용 대비 효과가 높은 컴퓨팅 기술과 규제 당국의 지원이 결합되어, AI를 활용한 인실리코 신약 개발의 지속적인 성장을 이끌고 있습니다.

제약 업계, 신속한 표적 검증을 위해 AI 도입

데이터 기반 검증 기법을 통해 개발상의 누락이 초기 단계로 옮겨가고 있습니다. 1,700만 건의 익명화된 환자 기록을 활용하는 Valo Health사의 Opal 플랫폼은 유전학적 근거에 기반한 프로그램을 우선시하고 있습니다. 이 회사는 노보노르디스크와의 제휴를 확대하여 20개의 심혈관 및 대사계 표적을 대상으로 하고 있으며, 그 잠재적 가치는 최대 46억 달러에 달할 전망입니다. Recursion사는 표현형 매핑을 위해 1조 장이 넘는 iPS 세포 이미지를 활용하여 SAR(구조-활성 상관관계) 및 독성 평가를 효율화함으로써, REC-4881의 표적 규명부터 1b/2상 임상시험 진행까지의 과정을 2년 미만으로 단축했습니다. 이러한 사례들은 AI를 활용한 인실리코 신약 개발 시장에서 의사 결정과 개발 일정이 어떻게 변화하고 있는지를 여실히 보여주고 있습니다.

현행 모델의 편향이 미개척 대상 영역에서의 성능을 제한합니다.

공개된 양성 데이터의 영향을 받는 현행 모델은 미개척 표적에 대응하는 데 있어 과제를 안고 있습니다. 실패로 끝나는 전임상 프로그램의 약 90%는 공유 저장소에 포함되어 있지 않습니다. 이러한 격차로 인해 스폰서들은 같은 문제에 반복적으로 직면할 수밖에 없습니다. 2025년 5월, Recursion사는 2상 임상시험 결과가 불충분한 것으로 판명됨에 따라 REC-994의 개발을 중단했으며, 편향된 데이터 세트에 의존할 경우 발생할 수 있는 위험을 여실히 드러냈습니다. AI를 활용한 인실리코 신약 개발 시장에서 전이성을 향상시키기 위해서는 부정적인 결과를 통합하기 위한 컨소시엄을 설립하는 것이 매우 중요해질 가능성이 있습니다.

부문별 분석

2025년, 리드 최적화는 AI를 활용한 인실리코 신약 개발 시장의 33.33%를 차지했으며, AI를 활용한 SAR(구조-활성 상관관계) 및 다변수 최적화의 즉각적인 이점이 부각되었습니다. 일부 종양학 프로그램에서 단편 기반 솔루션을 통해 합성 반복 횟수가 20회 이상에서 불과 몇 회로 대폭 감소했습니다. 이 부문의 심화는 시장 규모를 확대할 뿐만 아니라, 스폰서 측의 효능 및 선택성에 대한 투자 확대도 촉진하고 있습니다. 한편, 전임상 단계의 후보 화합물 선정은 연평균 성장률(CAGR) 33.30%로 빠르게 진행되고 있으며, 2031년까지 그 격차를 좁힐 것으로 예측됩니다. 통합 플랫폼은 설계, ADME-Tox 예측, 제조 가능성 평가를 연속적인 루프로 통합함으로써 프로세스를 효율화하고, IND 신청을 가속화하고 있습니다.

2025년에는 성숙한 지도 학습 모델, 지식 그래프, 그리고 신약 개발 워크플로우에 원활하게 통합된 그라디언트 부스팅 앙상블을 통해 머신러닝이 매출의 46.45%를 차지했습니다. 물리학 강화 신경망과 그래프 임베딩은 이 기술의 상용화 준비가 완료되었음을 보여줍니다. 시장에서 머신러닝에 대한 의존도는 신규 시장 진출기업이 재현하기 어려운 독자적인 과거 SAR 데이터 및 결정 구조 데이터에 의해 더욱 강화되고 있습니다.

강화 학습은 자율적인 탐색을 통해 설계와 분석 간의 격차를 해소함으로써 연평균 성장률(CAGR) 32.16%를 기록하며 성장세를 이어가고 있습니다. 트랜스포머 엔진을 통해 구조 예측의 커버리지가 인간 프로테옴의 76%까지 향상되었습니다. 대규모 언어 모델은 수많은 치료 관련 과제에서 벤치마크를 뛰어넘고 있습니다. 폐루프형 로봇공학이 표준화됨에 따라, 강화 학습 에이전트는 ‘동작 제안’에서 ‘실시간 가설 생성’ 및 ‘실험실 내 실행’으로 진화하고 있으며, 이는 해당 기술의 장기적인 시장 잠재력을 높이고 있습니다.

지역별 분석

2025년, 북미는 매출의 40.25%를 차지했습니다. 이는 FDA의 지침, 실리콘밸리의 하드웨어 생태계, 그리고 보스턴과 솔트레이크시티의 신약 개발 클러스터를 활용한 것입니다. 벤처 자금 조달은 여전히 집중되는 양상을 보였으며, 주요 기업들이 대규모 추가 자금 조달을 단행했습니다. FDA의 실시간 임상시험 모니터링 및 AI 지침안 등을 포함한 해당 지역의 명확한 정책은 계속해서 전 세계 파트너들의 관심을 끌고 있으며, AI를 활용한 인실리코 신약 개발 분야에서 북미의 중심적 역할을 강화하고 있습니다.

유럽은 엄격한 규제 감독과 민관 협력을 바탕으로 한 연합 데이터 이니셔티브에 힘입어 20% 중반대의 점유율을 유지했습니다. EMA의 AIM-NASH 인증과 예정된 EU AI법은 알고리즘 승인을 위한 명확하고 엄격한 절차를 제시하고 있습니다. 안전장치가 마련된 AI 기금이나 GDPR(EU 개인정보보호규정)을 준수하는 병원 파트너십과 같은 노력은 데이터 개인정보 보호 기준을 유지하면서 AI를 의료 분야에 통합하려는 노력을 여실히 보여주고 있습니다.

아시아태평양은 가장 높은 성장률을 나타낼 것으로 예상되며, 2031년까지의 연평균 성장률(CAGR)은 33.98%로 전망됩니다. 중국의 ‘디지털·지능형 변혁 계획’은 국가 대출과 지방 자치단체의 보조금을 바탕으로, 2027년까지 100개의 디지털 의약품 공장과 10개의 대규모 모델 플랫폼을 설립하는 것을 목표로 하고 있습니다. 일본에서는 고령화가 진행됨에 따라 생산성 향상이 요구되고 있으며, 대기업들의 투자가 촉진되고 있습니다. 인도에서는 클라우드 네이티브 다변수 최적화 플랫폼의 도입으로 제네릭 의약품에서 혁신적인 의약품으로의 전환이 가능해지면서, 해당 지역의 인실리코 의약품 개발 분야 AI 시장이 더욱 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the aI in in-Silico drug development market size is expected to increase from USD 3.10 billion in 2025 to USD 4.05 billion in 2026 and reach USD 15.31 billion by 2031, growing at a CAGR of 30.5% over 2026-2031.

This report is Segmented by Application Stage (Target ID, Hit Discovery, Land More), AI Technology (Machine Learning, Deep Learning, and More), Drug Type (Small Molecule, Biologics, Other), Therapeutic Area (Oncology, Neurology, and More), End User (Pharma/Biotech, Cros, Academic), Deployment Mode (Cloud, On-Premise), and Geography (North America, and More). Market Forecasts are in Value (USD).

Global AI In In-Silico Drug Development Market Trends and Insights

Cloud-Native High-Performance Computing Gains Traction

Widespread access to elastic GPU clusters is reducing the financial barriers to AI research. NVIDIA's BioNeMo, operational at several pharmaceutical firms, cuts training latency for extensive protein language models by half and increases inference speed six-fold. Meanwhile, Denmark's Gefion supercomputer enabled Orbis Medicines to analyze 140 billion macrocycles in just a few days. The shift to on-demand infrastructure transforms fixed capital expenses into flexible costs, allowing mid-tier biotech firms to conduct billion-molecule virtual screenings, a capability previously limited to the top 10 pharmaceutical companies five years ago. The FDA's pilot program, set for April 2026, is now utilizing real-time cloud data from AstraZeneca and Amgen trials, streamlining administrative processes by 20 to 40 percent. This combination of cost-effective computing and regulatory support is driving sustained growth in the AI in in-silico drug development market.

Pharmaceuticals Embrace AI for Swift Target Validation

Data-driven validation methods are shifting attrition to the earliest stages. Valo Health's Opal platform, which leverages 17 million de-identified patient records, is prioritizing genetically-backed programs. The company has expanded its partnership with Novo Nordisk to include 20 cardiometabolic targets, with a potential value of up to USD 4.6 billion. Recursion, using over a trillion induced pluripotent stem-cell images for phenotypic mapping, accelerated REC-4881's progression from target identification to Phase 1b-2 in under two years by streamlining SAR and toxicity evaluations.These examples highlight how AI-driven strategies are transforming decision-making and timelines in the AI in in-silico drug development market.

Bias in Current Models Limits Performance on Underexplored Targets

Current models, influenced by publicly available positive data, face challenges in addressing underexplored targets. Approximately 90% of pre-clinical programs that fail are not included in shared repositories. This gap forces sponsors to repeatedly encounter the same challenges. In May 2025, Recursion discontinued REC-994 after Phase 2 signals proved insufficient, emphasizing the risks of relying on biased datasets. Establishing consortia to consolidate negative results may be crucial for improving transferability in the AI-driven in-silico drug development market.

Other drivers and restraints analyzed in the detailed report include:

- Venture Capital and Corporations Rally Behind AI-Driven Biotechs

- Regulators Embrace Algorithmic Submissions

- Patent Law's Challenge with AI-Driven Molecular Design

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, lead optimization accounted for 33.33% of the AI-driven in-silico drug development market, highlighting the immediate advantages of AI-enhanced SAR and multiparameter optimization. For several oncology programs, fragment-based suites have significantly reduced synthesis iterations from over twenty to just a few. This segment's depth not only increases the market size but also drives higher investments in potency and selectivity by sponsors. Meanwhile, pre-clinical candidate selection is advancing rapidly, with a 33.30% CAGR, and is expected to narrow the gap by 2031. Integrated platforms are streamlining processes by combining design, ADME-Tox prediction, and manufacturability assessments into a continuous loop, accelerating IND filings.

In 2025, machine learning captured 46.45% of the revenue due to its mature supervised models, knowledge graphs, and gradient-boosting ensembles that seamlessly integrate into discovery workflows. Physics-augmented neural networks and graph embeddings exemplify the production readiness of this technology. The market's reliance on machine learning is further supported by proprietary historical SAR and crystallography data, which are challenging for new entrants to replicate.

Reinforcement learning is gaining traction with a 32.16% CAGR, as autonomous exploration bridges the gap between design and assay. Transformer engines have improved structure prediction coverage to 76% of the human proteome. Large language models have surpassed benchmarks in numerous therapeutic tasks. As closed-loop robotics becomes standard, reinforcement-learning agents are evolving from move-suggestion to real-time hypothesis generation and laboratory execution, enhancing the long-term market potential of this technology.

Geography Analysis

In 2025, North America accounted for 40.25% of the revenue, leveraging FDA guidance, Silicon Valley's hardware ecosystems, and discovery clusters in Boston and Salt Lake City. Venture funding remained concentrated, with significant follow-on rounds raised by key players. The region's policy clarity, including FDA's real-time trial monitoring and draft AI guidance, continues to attract global partnerships, reinforcing North America's central role in the AI in in-silico drug development market.

Europe maintained a mid-20% share, supported by stringent regulatory oversight and collaborative public-private federated-data initiatives. The EMA's AIM-NASH qualification and the anticipated EU AI Act provide clear yet demanding pathways for algorithmic submissions. Initiatives such as a safeguarded AI fund and GDPR-compliant hospital partnerships highlight efforts to integrate AI into healthcare while maintaining data privacy standards.

Asia-Pacific is expected to grow at the fastest rate, with a projected CAGR of 33.98% through 2031. China's Digital and Intelligent Transformation Plan, supported by state credits and provincial subsidies, aims to establish 100 digital drug factories and 10 large-model platforms by 2027. Japan's aging population drives a need for increased productivity, prompting investments from major companies. In India, the adoption of a cloud-native multiparameter-optimization platform is enabling a shift from generics to innovation, further expanding the regional AI in in-silico drug development market.

- Aria Intelligent Solutions

- Numerion Labs (Atomwise)

- Benevolent AI

- BioAge Labs

- Cloud Pharmaceuticals

- Cyclica

- Deep Genomics

- Evaxion Biotech

- Exscientia

- Healx

- Iktos

- Insilico Medicine

- Owkin

- Recursion Pharmaceuticals

- Relay Therapeutics

- Schrodinger

- Turbine

- Valo Health

- Verge Genomics

- XtalPi

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Cloud-Native High-Performance Computing Access

- 4.2.2 Pharma Shift to Fail-Fast AI-Assisted Screening Models

- 4.2.3 Growing Venture & Corporate Funding for AI-First Biotech

- 4.2.4 Regulatory Pilot Programs for Algorithmic Submissions (E.G., FDA's CDS Initiative)

- 4.2.5 Quantum-Inspired AI Accelerators Reaching Commercial Maturity

- 4.2.6 Data-Centric Foundation Models Enabling Zero-Shot Target Prediction

- 4.3 Market Restraints

- 4.3.1 Sparse Negative-Result Datasets Hindering Algorithm Generalization

- 4.3.2 Unresolved IP Ownership for AI-Generated Molecular Structures

- 4.3.3 High Switch-Out Costs from Incumbent Wet-Lab CRO Workflows

- 4.3.4 Regulatory Opacity on Explainability Thresholds for Generative Models

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application Stage

- 5.1.1 Target Identification

- 5.1.2 Hit Discovery

- 5.1.3 Lead Optimization

- 5.1.4 Pre-clinical Candidate Selection

- 5.2 By AI Technology

- 5.2.1 Machine Learning

- 5.2.2 Deep Learning

- 5.2.3 Natural Language Processing

- 5.2.4 Reinforcement Learning

- 5.2.5 Other AI Methods

- 5.3 By Drug Type

- 5.3.1 Small Molecule

- 5.3.2 Biologics

- 5.3.3 Other Types

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Neurology

- 5.4.3 Infectious Diseases

- 5.4.4 Cardiovascular

- 5.4.5 Metabolic Disorders

- 5.4.6 Other Therapeutic Areas

- 5.5 By End User

- 5.5.1 Pharmaceutical & Biotech Firms

- 5.5.2 Contract Research Organizations

- 5.5.3 Academic & Research Institutes

- 5.6 By Deployment Mode

- 5.6.1 Cloud-Based Platforms

- 5.6.2 On-Premise Solutions

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Australia

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Aria Intelligent Solutions

- 6.3.2 Numerion Labs (Atomwise)

- 6.3.3 BenevolentAI

- 6.3.4 BioAge Labs

- 6.3.5 Cloud Pharmaceuticals

- 6.3.6 Cyclica

- 6.3.7 Deep Genomics

- 6.3.8 Evaxion Biotech

- 6.3.9 Exscientia

- 6.3.10 Healx

- 6.3.11 Iktos

- 6.3.12 Insilico Medicine

- 6.3.13 Owkin

- 6.3.14 Recursion Pharmaceuticals

- 6.3.15 Relay Therapeutics

- 6.3.16 Schrodinger

- 6.3.17 Turbine

- 6.3.18 Valo Health

- 6.3.19 Verge Genomics

- 6.3.20 XtalPi

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment