|

시장보고서

상품코드

2064448

미국의 특수 의료용 의자 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Specialty Medical Chairs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

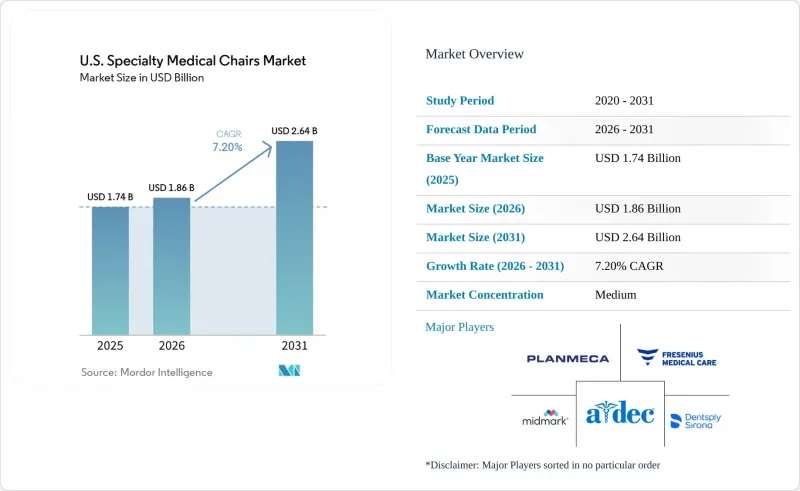

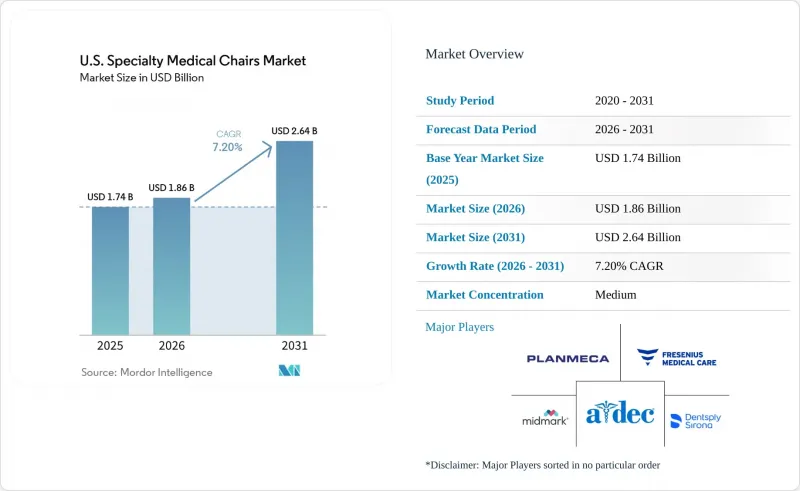

Mordor Intelligence에 의하면, 미국의 특수 의료용 의자 시장 규모는 2025년에 17억 4,000만 달러로 평가되었고, 2026년에 18억 6,000만 달러로 추정되고, 2031년까지 26억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 7.20%로 성장할 전망입니다.

본 보고서는 제품 유형별(검사용, 치료용, 재활용), 기술별(수동식, 유압식, 완전 전동식, 커넥티드 전동식), 최종 사용자별(병원, 치과 및 DSO, 외래수술센터(ASC), 투석 센터, 기타), 임상 용도별(치과, 안과, 이비인후과, 투석, 수액 요법, 산부인과, 기타)로 분류되어 있습니다. 예상치는 금액(달러)으로 표시되어 있습니다.

미국의 특수 의료용 의자 시장 동향 및 인사이트

외래 수술로의 전환이 치과용 의자 수요를 실시간으로 재편하고 있습니다.

CMS는 2026 회계연도(CY 2026)의 ‘입원 한정 목록’에서 285건의 근골격계 시술을 삭제하고, ASC 대상 시술 목록에 560건의 시술을 추가했습니다. 이로 인해 외래 시설로의 치료 건수 이전이 가속화되고 있습니다. 메디케어의 ASC에 대한 시설 지급액은 2026년에 92억 달러에 달할 것으로 예상되며, 메디케어 종량제 수급자 1인당 ASC 수술 건수는 2024년에 3.4% 증가할 전망입니다. 이러한 변화로 인해, 미국의 특수 의료용 의자 시장에서는 다양한 시술 워크플로우에 대응하고 외래 진료실의 레이아웃을 최적화할 수 있는 범용성이 높은 프로그래밍 가능한 전동 플랫폼에 대한 수요가 증가하고 있습니다.

고령화로 인한 다중 질환 병용에 대응하는 의료용 의자에 대한 수요

2060년까지 8,880만 명에 달할 것으로 예상되는 미국의 고령화에 따라, 이동의 어려움, 의자에서 다른 곳으로 옮겨 앉는 데 따르는 불편함, 낙상 방지에 대응할 수 있는 의료용 의자의 필요성이 높아지고 있습니다. 65세에서 74세 사이의 메디케어 수급자 중 53%가 3가지 이상의 만성 질환을 앓고 있는 만큼, 의료 기관에서는 기존의 고정 높이 의자를 보다 안전한 이동과 장시간 치료 지원을 제공하는 모델로 교체하고 있으며, 이로 인해 수요가 지리적으로 확대되고 교체 주기가 길어지고 있습니다.

높은 초기 비용이 자금 조달 격차를 초래합니다.

안과용 완전 전동식 특수 의료용 의자의 가격은 5,850달러에서 1만 1,650달러 사이이며, 치과용 의자는 6,300달러에서 1만 1,650달러 사이입니다. 한편, 고정식 채혈용 의자는 가격이 더 저렴하여 400달러에서 1,300달러 사이입니다. 17인치 낮은 승차 높이 기준을 충족하도록 제품을 재설계할 경우, 제조업체의 비용이 20%에서 30%까지 증가할 가능성이 있어, 대규모 의료 시스템과 예산이 제한된 소규모 클리닉 간에 재정적 격차가 발생하게 됩니다. 연방 정부의 자금 지원을 받는 의료 기관은 2026년 7월 8일까지 접근성 기준을 충족해야 하므로, 규정 준수 압박은 여전히 높은 상태입니다. 미국 특수 의료용 의자 시장 수요는 규정 준수 기준을 충족하는 범위 내에서는 견조한 편이지만, 보다 광범위한 업그레이드는 예산 제약으로 인해 제한되고 있습니다.

부문별 분석

치료용 의자는 화학요법, 수액 치료, 혈액 투석 등의 진료가 외래 센터로 이전되고 있는 상황을 배경으로, 2031년까지 연평균 성장률(CAGR) 8.20%를 기록하며 성장할 것으로 전망됩니다. 이 의자들은 장시간 사용 시의 편안함, 안정적인 자세 유지, 안전한 이동, 빈번한 사용에도 견딜 수 있는 내구성이 높이 평가받고 있으며, 미국 특수 의료용 의자 시장의 주요 성장 동력이 되고 있습니다. 등받이 기울기 조절 범위, 이동 편의성, 내구성이 균형 있게 조화를 이룬 모델이 선호되는 경향이 있습니다.

재활용 의자는 2025년에 75.69%의 시장 점유율을 차지했으며, 이는 요양 시설, 급성기 이후 회복기, 장기 요양 현장에서 수요를 반영한 것입니다. 장시간의 일상적인 사용에 따라 체압 분산, 비만 환자에 대한 대응 능력, 간병인의 안전성이 중요시되고 있습니다.

2025년, 전동 휠체어는 미국 의료용 특수 휠체어 시장의 65.55%를 차지했습니다. 이는 프로그래밍이 가능한 자세 조절 기능, 인체공학적 설계의 개선, 접근성 기준 준수가 주도한 결과입니다. 이러한 시스템은 간병인의 부담을 덜어주고 다양한 업무 흐름을 지원함으로써 병원, DSO(치과 클리닉 운영 조직), 외래 진료 시설에서 확고한 입지를 유지하고 있습니다.

유압식 및 반전동식 의자는 2031년까지 연평균 성장률(CAGR)이 7.99%를 나타낼 것으로 예측되며, 고도 연결 기능은 필요하지 않지만 높이 조절 기능이 필요한, 비용 효율성을 중시하는 환경에 부응하고 있습니다. 수동식 휠체어는 재택 간호 및 재택 투석 분야에서는 여전히 중요하지만, 시설에서의 사용은 감소할 것으로 예측됩니다. 유지보수의 가시성과 서비스의 편의성이 구매 시 중요한 판단 기준이 되어가고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the u.S. specialty medical chairs market size is projected to be USD 1.74 billion in 2025, USD 1.86 billion in 2026, and reach USD 2.64 billion by 2031, growing at a CAGR of 7.20% from 2026 to 2031.

This report is Segmented by Product Type (Examination, Treatment, Rehabilitation), Technology (Manual, Hydraulic, Fully Electric, Connected Electric), End User (Hospitals, Dental Practices and DSOs, Ascs, Dialysis Centers, and More), and Clinical Application (Dental, Ophthalmic, ENT, Dialysis, Infusion, OB/GYN, and More). Forecasts are in Value (USD).

U.S. Specialty Medical Chairs Market Trends and Insights

Outpatient Procedure Migration Restructuring Chair Demand in Real Time

CMS has removed 285 musculoskeletal procedures from its Inpatient-Only list for CY 2026 and added 560 procedures to the ASC Covered Procedures List, accelerating the shift of treatment volumes to ambulatory settings. Medicare facility payments to ASCs are projected to reach USD 9.2 billion in 2026, with ASC surgical procedures per fee-for-service Medicare beneficiary increasing by 3.4% in 2024. This shift is driving demand in the United States specialty medical chairs market for versatile, programmable electric platforms that support multi-procedure workflows and optimize outpatient room layouts.

Aging Demographics Driving Multi-Comorbidity Seating Requirements

The aging population in the United States, projected to reach 88.8 million by 2060, is increasing the need for medical chairs designed for mobility challenges, transfer difficulties, and fall prevention. With 53% of Medicare beneficiaries aged 65-74 managing three or more chronic conditions, facilities are replacing older fixed-height chairs with models offering safer transfers and longer treatment support, broadening demand geographically and extending replacement cycles.

High Upfront Chair Costs Creating Capital Access Disparities

Fully electric specialty exam chairs in ophthalmic applications are priced between USD 5,850 and USD 11,650, while dental chairs range from USD 6,300 to USD 11,650. Fixed phlebotomy seating is more affordable, priced between USD 400 and USD 1,300. Redesigning products to meet the 17-inch low transfer height standard could increase manufacturer costs by 20% to 30%, creating a financial gap between large health systems and smaller clinics with limited budgets. Compliance pressures remain high, as federally funded providers must meet accessibility standards by July 8, 2026. Demand in the United States specialty medical chairs market is steady at the compliance threshold, but broader upgrades are constrained by budget limitations.

Other drivers and restraints analyzed in the detailed report include:

- DSO Standardization Creating Fleet-Level Chair Procurement

- CKD and Infusion-Treatment Demand Sustained by Evolving Treatment Modalities

- Budget Pressure in Small and Independent Practices Dampening Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Treatment chairs are projected to grow at an 8.20% CAGR through 2031, driven by the shift of chemotherapy, infusion, and hemodialysis activities to outpatient centers. These chairs are valued for comfort during long sessions, stable positioning, safe transfers, and durability for high utilization, making them a key growth driver in the United States specialty medical chairs market. Models balancing recline range, transfer access, and durability are gaining preference.

Rehabilitation chairs held a 75.69% market share in 2025, reflecting their demand in skilled nursing, post-acute recovery, and long-term care settings. Extended daily use emphasizes pressure redistribution, bariatric capacity, and caregiver safety.

Fully electric chairs accounted for 65.55% of the United States specialty medical chairs market in 2025, driven by programmable positioning, enhanced ergonomics, and accessibility compliance. These systems reduce caregiver strain and support multiple workflows, maintaining their strong position across hospitals, DSOs, and outpatient sites.

Hydraulic and semi-electric chairs, with a projected 7.99% CAGR through 2031, cater to cost-sensitive settings requiring height adjustability without premium connectivity. Manual chairs remain relevant in home care and home dialysis but are expected to see reduced facility-based applications. Maintenance visibility and service simplicity are becoming critical purchase factors.

List of Companies Covered in this Report:

- ActiveAid, Inc.

- A-dec

- ATMOS MedizinTechnik

- Champion Manufacturing, Inc.

- DACOR Manufacturing, Inc.

- DENTALEZ, Inc.

- Dentsply Sirona

- Fresenius Medical Care AG

- Haag-Streit USA

- Hill Laboratories Company

- J. Morita Corp.

- Marco Ophthalmic, Inc.

- Medical Technology Industries, Inc.

- Midmark

- MP Seating

- OSSTEM IMPLANT Co., Ltd.

- Planmeca

- S4OPTIK LLC

- Takara Belmont

- The Brewer Company, LLC

- Topcon Healthcare, Inc.

- UMF Medical

- Winco Manufacturing, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Outpatient Procedure Migration

- 4.2.2 Aging and Mobility-Limited Patient Base

- 4.2.3 Dental Chair Replacement and DSO Standardization

- 4.2.4 Chronic Kidney Disease and Infusion-Treatment Demand

- 4.2.5 Accessible Exam-Chair Compliance After MDE Rule

- 4.2.6 Pressure-Injury Prevention Seating Protocols

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Powered Chairs

- 4.3.2 Budget Pressure in Small Clinics and Private Practices

- 4.3.3 Actuator and Upholstery Service Bottlenecks

- 4.3.4 Room Retrofit and Electrical-Load Constraints

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Examination Chairs

- 5.1.2 Treatment Chairs

- 5.1.3 Rehabilitation Chairs

- 5.2 By Technology / Actuation

- 5.2.1 Manual

- 5.2.2 Hydraulic / Semi-electric

- 5.2.3 Fully Electric

- 5.2.4 Connected / Programmable Electric

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Physician Offices and Specialty Clinics

- 5.3.3 Dental Practices and DSOs

- 5.3.4 Ambulatory Surgery Centers

- 5.3.5 Dialysis Centers

- 5.3.6 Blood Collection Centers

- 5.3.7 Rehabilitation Centers, Skilled Nursing Facilities, and Long-term Care Settings

- 5.3.8 Home Care and Home Dialysis Settings

- 5.3.9 Others

- 5.4 By Clinical Application

- 5.4.1 Dental

- 5.4.2 Ophthalmic

- 5.4.3 ENT

- 5.4.4 Dialysis

- 5.4.5 Infusion and Oncology

- 5.4.6 OB/GYN

- 5.4.7 Dermatology and Aesthetics

- 5.4.8 Podiatry

- 5.4.9 Rehabilitation and Physiotherapy

- 5.4.10 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 ActiveAid, Inc.

- 6.3.2 A-dec, Inc.

- 6.3.3 ATMOS MedizinTechnik GmbH & Co. KG

- 6.3.4 Champion Manufacturing, Inc.

- 6.3.5 DACOR Manufacturing, Inc.

- 6.3.6 DENTALEZ, Inc.

- 6.3.7 Dentsply Sirona Inc.

- 6.3.8 Fresenius Medical Care AG

- 6.3.9 Haag-Streit USA

- 6.3.10 Hill Laboratories Company

- 6.3.11 J. Morita Corp.

- 6.3.12 Marco Ophthalmic, Inc.

- 6.3.13 Medical Technology Industries, Inc.

- 6.3.14 Midmark Corporation

- 6.3.15 MP Seating

- 6.3.16 OSSTEM IMPLANT Co., Ltd.

- 6.3.17 Planmeca Oy

- 6.3.18 S4OPTIK LLC

- 6.3.19 Takara Belmont Corporation

- 6.3.20 The Brewer Company, LLC

- 6.3.21 Topcon Healthcare, Inc.

- 6.3.22 UMF Medical

- 6.3.23 Winco Manufacturing, LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment