|

시장보고서

상품코드

2064449

미국의 재처리 의료기기 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Reprocessed Medical Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

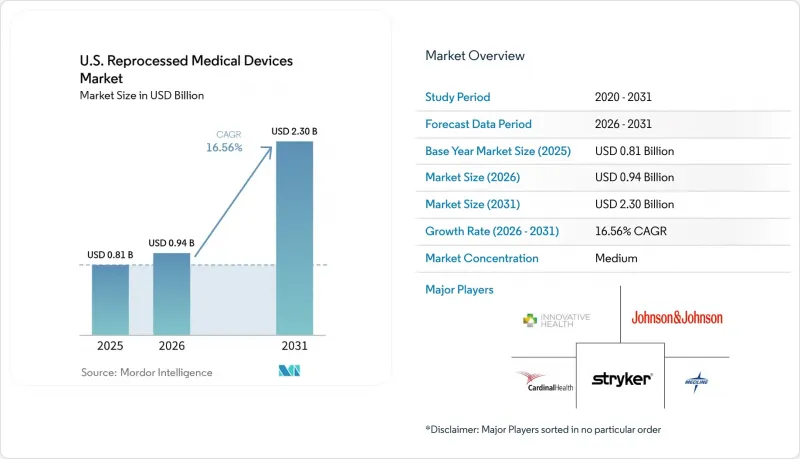

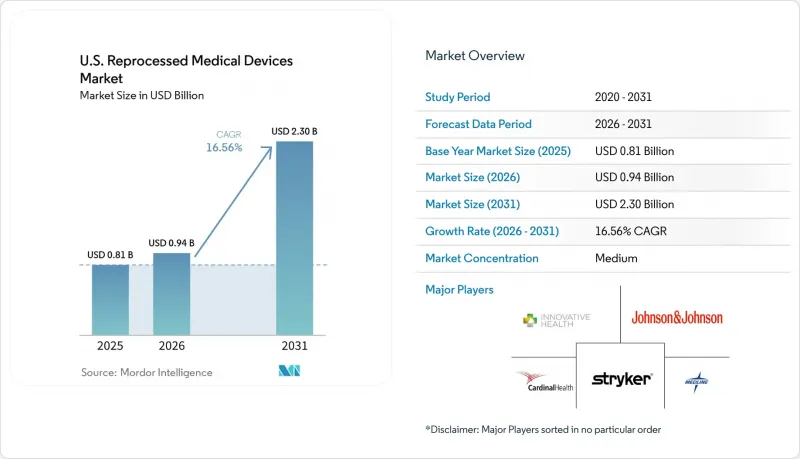

Mordor Intelligence에 의하면, 미국의 재처리 의료기기 시장 규모는 2025년에 8억 1,000만 달러로 평가되었습니다. 2026년 9억 4,000만 달러에서 2031년까지 23억 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 16.56%를 나타낼 전망입니다.

본 보고서는 제품 유형(심혈관, 복강경, 기타), 재처리 모델(타사/상업용, 기타), 의료기기 위험 등급(크리티컬, 세미크리티컬, 논크리티컬), 임상 용도(심장학 및 전기생리학, 소화기학, 기타), 최종 사용자(급성기 병원, ASC, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 재처리 의료기기 시장 동향 및 인사이트

병원공급 비용 억제 및 각 처치별 지속적인 비용 절감

미국의 재처리 의료기기 시장에서는 병원의 비용 압박이 여전히 주요 촉진요인으로 작용하고 있습니다. 이는 구매 담당 팀이 예산에 미치는 영향을 연례 검토 시점이 아닌, 사례별로 평가할 수 있기 때문입니다. 2025년, AMDR은 가맹 재처리 업체들이 병원에 4억 9,550만 달러의 비용 절감을 가져다주었다고 보고했으며, 이익률 압박에 직면한 재무팀에게 재처리는 매우 중요한 전략이 되고 있습니다. 승인된 재사용 주기를 통해 동일한 회계연도 내에서 반복적으로 비용을 절감할 수 있으므로, 이러한 절감 효과는 지속적입니다. 2024년, Innovative Health는 재처리를 통해 연간 100만 미 달러 이상을 절감하고 있는 전기생리학 검사실이 50% 증가했다고 밝혔습니다. 또한, FDA의 새로운 승인으로 인해 제휴 검사실의 평균 절감액이 17% 증가했습니다. 이러한 변화에 따라 병원들은 재처리를 단순한 선택적 활동이 아닌 핵심 조달 전략으로 자리매김하기 시작했습니다.

심혈관 및 전기생리학적 수술 건수 증가

심혈관 및 전기생리학 수술 건수 증가가 미국의 재처리 의료기기 시장을 견인하고 있습니다. 이러한 전문 분야는 고가의 일회용 제품에 크게 의존하고 있기 때문입니다. 심방세동 수술 건수는 연간 약 17%의 속도로 증가하고 있으며, 의료기기 비용은 연간 25억 달러에 달할 전망입니다. 증례 수가 많을수록 비용 절감 효과는 커집니다. 예를 들어, 시술 건수가 많은 프로그램의 경우, 심초음파 카테터 1개를 재처리함으로써 단가를 3,500달러에서 1,400-1,750달러로 낮출 수 있기 때문입니다. 49개 병원으로 구성된 한 의료 시스템에서는 4년 동안 490만 달러의 비용 절감을 달성하는 동시에 1만 9,000파운드 이상의 폐기물을 감축함으로써, 처리 능력이 뛰어난 실험실에서의 재처리가 가져다주는 재정적·운영적 이점을 입증했습니다.

OEM을 통한 재처리 대책 설계 및 계약상 전략

미국의 재처리 의료기기 시장에서 OEM(원천 장비 제조업체)은 비용 대비 효과가 높은 솔루션에 대한 수요가 있음에도 불구하고, 그 규모와 계약상의 영향력을 이용해 재처리 장비의 도입을 방해하고 있습니다. 번들링(묶음 판매), 소프트웨어를 통한 제어, 선택적 지원과 같은 전략은 재처리 제품 도입을 검토하는 병원들에게 걸림돌이 되고 있습니다. 2026년에 메드트로닉(Medtronic) 및 바이오센스 웹스터(BioSense Webster)에 내려진 법원 판결은 반경쟁적 행위에 대처하는 데 있어 전환점이 되었으나, 상업적 과제와 OEM 전략의 진화로 인해 고부가가치 의료기기 부문에서 시장 침투는 여전히 더딘 상태입니다.

부문별 분석

2025년, 미국의 재처리 의료기기 시장 점유율의 56.50%를 심혈관용 기기가 차지했습니다. 이는 전기생리학용 카테터의 높은 단가와 심장 카테터실에서 오랜 기간 이어져 온 재처리 관행에 기인한 것입니다. 재처리를 통해 시술 비용이 30% 가까이 절감됨에 따라, 병원 관리자들은 전기생리학 분야에서 상당한 비용 절감 효과를 누리고 있으며, 병원이 재사용 프로그램을 확대함에 따라 심혈관 기기는 주요 수익원으로 자리 잡고 있습니다.

정형외과 및 관절경용 의료기기는 일반외과용 제품과 함께, 설계의 재현성과 효율적인 회수 워크플로우 덕분에 중간 수준으로 평가되었습니다. 복강경용 의료기기는 비용 효율성이 극히 중요한 외래 진료로의 전환에 힘입어, 수술 워크플로우를 방해하지 않으면서도 합리적인 가격의 솔루션을 원하는 수요와 부합함에 따라, 2026년부터 2031년까지 연평균 성장률(CAGR) 16.20%를 나타낼 것으로 전망됩니다.

2025년 미국의 재처리 의료기기 시장에서 제3자 및 상업용 재처리 업체들이 84.12%의 점유율을 차지하며 시장을 독점했습니다. 이는 규모, 물류, 규제에 관한 전문 지식이 중요시되고 있음을 반영하고 있습니다. 대형 사업자는 회수, 검증, 규정 준수를 효율적으로 관리함으로써, 소규모 프로그램에서는 실현할 수 없는 비용 측면의 우위와 업무상의 노하우를 제공합니다.

이 모델은 대량 처리의 장점을 활용하여, 데이터에 기반한 품질 및 사이클 관리의 개선을 가능하게 합니다. 2026년부터 2031년까지 연평균 성장률(CAGR) 16.99%가 예상되는 가운데, 병원들이 재처리 의료기기 도입은 물론 위험 감소와 관리 간소화를 우선시함에 따라 아웃소싱은 계속해서 선호되는 접근 방식이 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the u.S. reprocessed medical devices market size was valued at USD 0.81 billion in 2025 and is estimated to grow from USD 0.94 billion in 2026 to reach USD 2.30 billion by 2031, at a CAGR of 16.56% during the forecast period (2026-2031).

This report is Segmented by Product Type (Cardiovascular, Laparoscopic, and Others), Reprocessing Model (Third-Party/Commercial and Others), Device Risk Class (Critical, Semi-Critical, Non-Critical), Clinical Application (Cardiology and EP, Gastroenterology, and Others), and End User (Acute Care Hospitals, Ascs, and Others). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Reprocessed Medical Devices Market Trends and Insights

Hospital Supply Cost Containment and Recurring Per-Procedure Savings

Hospital cost pressures remain a key driver in the United States reprocessed medical devices market, as purchasing teams can assess budget impacts on a case-by-case basis rather than during annual reviews. In 2025, AMDR reported that member reprocessors saved hospitals USD 495.5 million, making reprocessing a critical strategy for finance teams under margin pressure. These savings are recurring, as cleared reuse cycles allow repeated cost reductions within the same fiscal period. In 2024, Innovative Health noted a 50% increase in electrophysiology labs saving over USD 1 million annually through reprocessing, with average partner lab savings rising 17% due to new FDA clearances. This shift is prompting hospitals to treat reprocessing as a core procurement strategy rather than an optional initiative.

Rising Cardiovascular and Electrophysiology Procedure Volumes

Increasing cardiovascular and electrophysiology procedure volumes are driving the United States reprocessed medical devices market, as these specialties rely heavily on expensive single-use products. Atrial fibrillation procedures have been growing at nearly 17% annually, with device costs reaching USD 2.5 billion annually. High case volumes amplify savings, as reprocessing a single intracardiac echo catheter can reduce unit costs from USD 3,500 to USD 1,400-1,750 in high-volume programs. A 49-hospital health system achieved USD 4.9 million in savings over four years while diverting over 19,000 pounds of waste, reinforcing the financial and operational benefits of reprocessing in high-throughput labs.

OEM Anti-Reprocessing Design and Contracting Tactics

In the United States reprocessed medical devices market, original equipment manufacturers (OEMs) leverage their scale and contractual power to hinder the adoption of reprocessed devices, despite the demand for cost-effective solutions. Tactics such as bundling practices, software controls, and selective support create barriers for hospitals seeking reprocessed options. Although legal verdicts against Medtronic and Biosense Webster in 2026 marked a shift in addressing anti-competitive practices, commercial challenges and evolving OEM strategies continue to slow market penetration in high-value device categories.

Other drivers and restraints analyzed in the detailed report include:

- Waste Reduction and Health-System Decarbonization Goals

- FDA-Cleared Category Expansion Lifting Buyer Confidence

- FDA Validation and Quality-System Burden

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, cardiovascular devices accounted for 56.50% of the United States reprocessed medical devices market share, driven by the high unit value of electrophysiology catheters and a long history of reprocessing in cardiac labs. Administrators benefit from significant savings in electrophysiology, with reprocessing reducing procedure costs by nearly 30%, making cardiovascular devices a key revenue driver as hospitals expand reuse programs.

Orthopedic and arthroscopy devices, along with general surgery products, held mid-tier positions due to repeatable designs and efficient collection workflows. Laparoscopic devices are projected to grow at a 16.20% CAGR from 2026 to 2031, supported by the shift to outpatient settings where cost efficiency is critical, aligning with the need for affordable solutions without disrupting surgical workflows.

Third-party and commercial reprocessing dominated the United States reprocessed medical devices market in 2025, with an 84.12% share, reflecting the preference for scale, logistics, and regulatory expertise. Large operators manage collection, validation, and compliance efficiently, offering cost advantages and operational insights that smaller programs cannot match.

This model benefits from processing large volumes, enabling data-driven improvements in quality and cycle management. With a projected 16.99% CAGR from 2026 to 2031, outsourcing remains the preferred approach as hospitals prioritize risk reduction and administrative simplicity alongside reprocessed devices.

List of Companies Covered in this Report:

- Abbott Laboratories

- Alliance Medical Corporation

- Arjo, Inc.

- Avante Health Solutions

- Cardinal Health

- Case Medical, Inc.

- Centurion Medical Products Corp.

- EP Sustain

- GE HealthCare Technologies Inc.

- Innovative Health LLC

- Johnson & Johnson MedTech

- Medline Industries

- Midwest Reprocessing Center LLC

- NEScientific

- Sterilmed, Inc.

- STERIS

- Stryker

- SureTek Medical

- Vanguard

- Vein360 LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hospital Supply Cost Containment and Recurring Per-Procedure Savings

- 4.2.2 Waste Reduction and Health-System Decarbonization Goals

- 4.2.3 Rising Cardiovascular and Electrophysiology Procedure Volumes

- 4.2.4 FDA-Cleared Category Expansion Lifting Buyer Confidence

- 4.2.5 ASC Migration Increasing Demand for Lower-Cost Invasive Devices

- 4.2.6 Digital Traceability Strengthening Reprocessor Selection

- 4.3 Market Restraints

- 4.3.1 FDA Validation and Quality-System Burden

- 4.3.2 Clinician Perception and Value-Analysis Committee Friction

- 4.3.3 OEM Anti-Reprocessing Design and Contracting Tactics

- 4.3.4 Low Return Yield and Turnaround Complexity for Advanced Catheters

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Cardiovascular Devices

- 5.1.2 Laparoscopic Devices

- 5.1.3 General Surgery Devices

- 5.1.4 Gastroenterology Devices

- 5.1.5 Orthopedic and Arthroscopy Devices

- 5.1.6 ENT Devices

- 5.1.7 Non-invasive Patient Care Devices

- 5.2 By Reprocessing Model

- 5.2.1 Third-Party / Commercial Reprocessing

- 5.2.2 In-House Hospital Reprocessing

- 5.2.3 Blended OEM-Reprocessor Programs

- 5.3 By Device Risk Class

- 5.3.1 Critical Devices

- 5.3.2 Semi-Critical Devices

- 5.3.3 Non-Critical Devices

- 5.4 By Clinical Application

- 5.4.1 Cardiology and Electrophysiology

- 5.4.2 Gastroenterology

- 5.4.3 General Surgery

- 5.4.4 Orthopedic and Arthroscopy

- 5.4.5 ENT

- 5.4.6 Vascular Surgery

- 5.4.7 Urology and Gynecology

- 5.5 By End User

- 5.5.1 Acute Care Hospitals

- 5.5.2 Ambulatory Surgery Centers

- 5.5.3 Specialty Clinics and Cath Labs

- 5.5.4 Government and Federal Facilities

- 5.5.5 Academic and Research Hospitals

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Alliance Medical Corporation

- 6.3.3 Arjo, Inc.

- 6.3.4 Avante Health Solutions

- 6.3.5 Cardinal Health, Inc.

- 6.3.6 Case Medical, Inc.

- 6.3.7 Centurion Medical Products Corp.

- 6.3.8 EP Sustain

- 6.3.9 GE HealthCare Technologies Inc.

- 6.3.10 Innovative Health LLC

- 6.3.11 Johnson & Johnson MedTech

- 6.3.12 Medline Industries, LP

- 6.3.13 Midwest Reprocessing Center LLC

- 6.3.14 NEScientific, Inc.

- 6.3.15 Sterilmed, Inc.

- 6.3.16 STERIS plc

- 6.3.17 Stryker Corporation

- 6.3.18 SureTek Medical

- 6.3.19 Vanguard AG

- 6.3.20 Vein360 LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment