|

시장보고서

상품코드

2064452

미주신경 자극 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vagus Nerve Stimulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

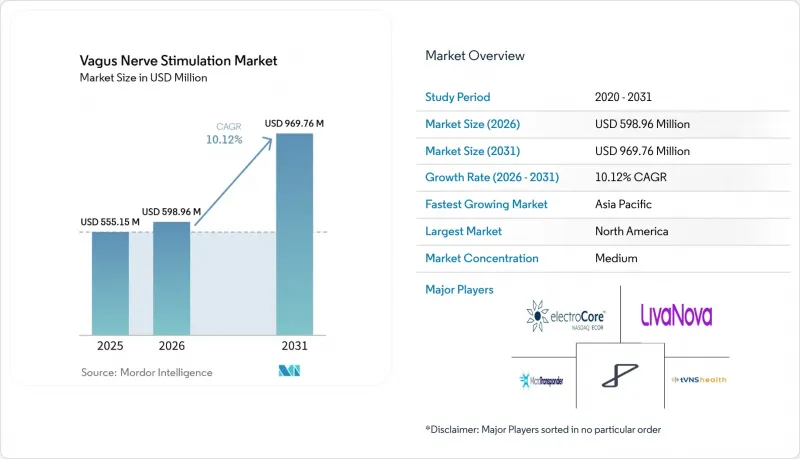

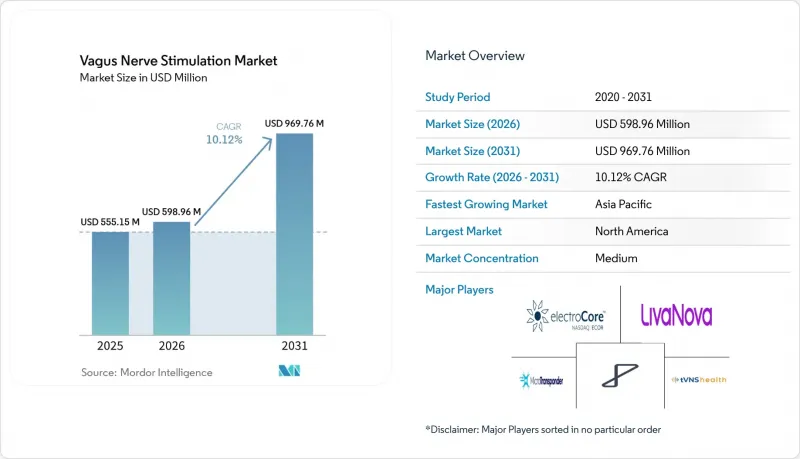

Mordor Intelligence에 의하면, 미주신경 자극 시장 규모는 2025년 5억 5,515만 달러로 평가되었습니다. 2026년에는 5억 9,896만 달러로 확대되어 2031년까지 9억 6,976만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 10.12%를 나타낼 전망입니다.

본 보고서는 제품별(이식형 VNS 기기 및 체외형 VNS 기기), 용도별(간질, 우울증, 기타 용도), 최종 사용자별(병원, 신경과 클리닉, 기타 최종 사용자), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 규모 및 전망은 상기 모든 부문에 대해 금액(달러) 기준으로 제시되어 있습니다.

세계의 미주신경 자극 시장 동향 및 인사이트

약물 내성 신경 질환의 유병률 증가

주요 의료 현장에서 약물 내성으로 분류되는 간질 환자의 비율은 여전히 높은 편이며, 전문 학회의 보고에 따르면 두 가지 적절한 항간질제로 지속적인 조절이 이루어지지 않는 경우, 그 비율은 20%에서 3분의 1 사이인 것으로 나타났습니다. 임상 지침은 약물 치료에 대한 반응이 예상될 확률이 낮은 경우, 기기를 이용한 신경 조절 요법을 조기에 고려하는 방향으로 지속적으로 발전하고 있으며, 이러한 변화는 프로그램 설정의 선택지 확대 및 실제 임상 코호트에서 확인된 장기적인 유익성 프로파일과 일치합니다. 치료 저항성 우울증의 경우, 증거 요약에 따르면 1차 선택 약물 요법에 대한 상당한 무반응이나 약물 변경을 반복함에 따라 효과가 감소하는 것으로 나타나고 있으며, 이로 인해 치료의 후반 단계에서 지속적인 증상 완화를 가져올 수 있는 기기 요법의 중요성이 부각되고 있습니다. 미국에서 우울증에 대한 보험 적용 재검토 절차는 현재 24개월간의 치료 결과를 기준으로 하고 있습니다. 여기에는 51.6%의 반응률과 조기 반응을 보인 환자에서 나타난 높은 지속성이 포함되어 있으며, 이러한 요소들이 결합되어 다음 주기에서 보험사가 접근성과 증거 요건 간의 균형을 어떻게 잡을지 시사하고 있습니다. 이러한 추세가 안정화되는 가운데, 신경학 및 정신의학 분야에서 치료법에 대한 인지도가 높아짐에 따라, 미주신경 자극 요법 시장에서 이식형 및 비침습형 시스템 모두에 대한 더 광범위한 적용 가능성이 입증되고 있습니다.

만성 약물 치료에서 신경 조절 치료로의 전환

임상의들은 전신성 부작용, 복약 순응도 문제, 다제 병용 요법으로 인한 삶의 질 저하와 같은 단점, 그리고 시간이 지남에 따라 프로그램이나 용량을 조정할 수 있는 기기 기반 신경 조절 요법을 지속적으로 비교 검토하고 있습니다. 종단적 데이터에 따르면, 부분 발작 유형에서 이식형 시스템의 유효성이 점진적으로 높아지는 것으로 나타나며, 해당 수술이 금기이거나 환자가 수술을 거부하는 경우, 치료의 최종 단계에서 이러한 시스템의 위상이 더욱 확고해지고 있습니다. 우울증의 경우, 수년에 걸친 관찰 연구 결과, 기존의 치료법을 다수 시도해도 효과를 얻지 못했던 환자 집단에서 임상적으로 의미 있는 반응률 및 관해율이 나타났으며, 이는 기존의 약물 요법의 한계를 넘어선 지속적인 효과로 가는 길을 뒷받침하는 것입니다. 비침습적 뇌 자극 요법과 직접 비교했을 때 동등한 효과를 얻을 수 있다고 해서 이를 표준 치료라고 할 수는 없지만, 경두개 자기 자극 요법(TMS)의 표준 프로그램에서 반응률의 기준치는 많은 기관에서 50-60% 범위에 집중되어 있으며, 그 지속성은 유지 요법 전략에 따라 달라집니다. 미국에서는 2019년 이후 우울증 적응증에 대한 보험 적용을 제한해 온 ‘증거 개발과 연계된 보험 적용(Coverage-with-Evidence-Development)’ 체계가 현재 공식적으로 재검토되고 있습니다. 최종 결정 과정에서 증상 평가 척도 외에도 실제 임상에서 효과가 지속되는 것으로 확인된다면, 도입이 가속화될 가능성이 있습니다. 장기적으로 볼 때, 제약사가 제시한 의료경제 분석에 따르면 입원 및 응급실 이용 감소로 인해 2년 이내에 투자 회수가 가능하다는 점이 강조되고 있으며, 이러한 주장은 미주신경 자극 시장을 주시하는 이해관계자들 사이에서 계속해서 공감을 얻고 있습니다.

이식형 VNS 시스템의 높은 초기 비용

이식형 시스템은 전문적인 시술, 전용 수술 시설 및 지속적인 사후 관리 프로그램이 필요하기 때문에 총 도입 비용 및 수술 전후 관리 비용은 여전히 단기적인 장벽으로 남아 있습니다. 이러한 재정적 부담을 더욱 부각시키는 방식으로, 미국의 의료 청구 데이터베이스를 바탕으로 한 연구에 따르면, VNS 이식 전 2년 동안 1인당 평균 의료비가 약 12만 3,500달러였던 것으로 밝혀졌습니다. 미국에서 서비스 종료 시 조치에 대한 보상과 관련하여, 2026년에 지급 수준을 인상한다는 개정안이 제출되었으나, 최종 결정의 방향과 시기에 따라 병원 및 진료소의 현금 흐름이 어느 정도 개선될지가 결정될 것입니다. 미국에서는 현재의 전국적인 보험 적용 결정에 따라, 장기 추적 조사를 수반하는 ‘증거 기반 보험 적용(coverage-with-evidence-development)’ 연구에 대한 지급으로만 제한되어 있기 때문에 우울증 치료에 대한 접근 경로는 여전히 제약을 받고 있습니다. 민간 보험 플랜의 경우, 임플란트 치료법의 승인을 받을 때 여러 약물 치료의 실패나 심리 치료 시도를 요건으로 삼는 경우가 많아, 증상이 남아 있는 환자들의 경우 치료 시작까지의 기간이 길어지고 있습니다. 여러 보험사는 2026년 보험 약관에서 우울증에 대한 이식형 미주신경 자극 요법을 ‘임상시험 단계’ 또는 ‘미확립’으로 분류하고 있으며, 이는 장기간에 걸친 관찰 연구 결과와 증거 평가가 완전히 일치하지 않는 현 상황을 반영하고 있습니다. 새로운 자가면역 질환에 대한 적응증 확대는 비용 대비 효과에 대한 논의를 바꿀 가능성이 있습니다. 왜냐하면 2025년 미국에서 류마티스 관절염에 대한 신경면역조절요법이 승인되었을 때, 상업적 전개와 실제 임상 데이터 생성을 지원하기 위한 성장 자금 조달도 동시에 이루어졌기 때문입니다. 또한, 각 제조업체들은 입원 및 응급실 내원 건수의 감소로 인해 이식형 시스템의 손익분기점이 약 2년 이내에 달성될 것이라는 보험사 대상 분석 결과도 제시하고 있으며, 이는 미주신경 자극 시장에서 여전히 중요한 메시지로 남아 있습니다.

부문별 분석

2025년 기준, 미주신경 자극 장치 시장에서 이식형 기기의 점유율은 58.10%를 차지했으나, 2031년까지 연평균 성장률(CAGR) 10.64%로 성장하며 외부 착용형 시스템이 시장을 주도할 것으로 전망됩니다. 미국에서 사춘기 환자에 대한 적응증 승인 이후 비침습적 시스템의 접근성이 확대됨에 따라, 외래 진료의 편의성과 더불어 진료소 및 가정 환경에서의 사용량이 증가하고 있습니다. 재향군인부의 구매량은 2024년에 대폭 증가했으며, 2025년에도 성장을 이어가며, 많은 시설에서 기기 교육 및 표준화된 프로토콜을 도입할 수 있도록 지원함으로써 조달 주도의 규모 확대를 뒷받침하고 있습니다. 벨기에에서 유럽 정책이 구체화됨에 따라, 이는 또 하나의 접근 창구가 되었으며, 그 결과 영국 이외의 지역에서 유통 및 의료 교육의 경제성을 뒷받침하고 있습니다. 상환 경로가 다양해지고 임상 팀의 경험이 축적됨에 따라, 수술을 원하지 않는 환자나 외래 진료에서 신속한 치료 시작이 유익한 환자를 대상으로 하는 미주신경 자극 시장에서 비침습적 치료 옵션이 입지를 다져가고 있습니다.

이식형 플랫폼은 중증 또는 난치성 사례에서 알고리즘을 통해 최적화된 지속적인 자극을 장기적인 목표를 향해 프로그래밍할 수 있다는 구조적 이점을 계속해서 제공합니다. 제조업체의 보고에 따르면, 2025년 한 해 동안 신경 조절 요법의 매출은 꾸준히 증가했으며, 미국 및 유럽의 기여가 지속적인 포트폴리오 투자를 뒷받침하고 있습니다. 무작위 대조 시험을 통해 검증된 차세대 폐쇄 루프 개념과 소형화 및 배터리 없는 임플란트는 수술 시간 단축과 장기적인 발전기 교체 횟수 감소를 시사하며, 지금까지 비수술적 치료 옵션을 지지하는 요인이 되었던 장벽을 낮출 가능성이 있습니다. 환자의 선호도에 맞춘 제품 전략에 힘입어, 미주신경 자극 업계는 하이브리드 모델로 전환되고 있습니다. 이는 난치성 중증 환자에 대한 견고한 이식형 기기의 성능과, 유연성과 신속성이 가장 중요한 상황에서 비침습적인 편의성을 결합한 것입니다. 이러한 접근 방식이 성숙해짐에 따라, 다양한 제품 라인을 통해 병원, 신경과 클리닉, 재향군인 의료 시스템 등 미주신경 자극 시장에 대한 진출이 확대될 가능성이 있습니다.

지역별 분석

2025년, 북미는 미주신경 자극 시장의 58.22%를 차지했으며, 아시아태평양은 2031년까지 연평균 성장률(CAGR) 11.93%를 기록할 전망입니다. 미국에서는 우울증에 대한 전국적인 보험 적용 재검토 과정에 따라, 수년에 걸친 치료 성과가 정책 논의의 중심이 되고 있으며, 이는 이식형 및 비침습형 시스템 모두의 접근성과 이용 패턴에 영향을 미칠 가능성이 있습니다. 2024년 재무 공시에 따르면, 미국의 신경 조절 요법 매출이 꾸준히 증가하고 있으며, 일관된 프로그램 운영과 사후 관리에 의존하는 의료 제공업체 채널을 통해 수요가 안정적으로 유지되고 있음을 보여줍니다. 연방 정부의 구매는 비침습형 기기의 중요한 성장 요인으로 작용하고 있으며, 2024년 재향군인용 시스템 매출이 주요 성장 요인으로 꼽히고, 2025년 매출액은 기업 보고 기준 약 3,200만 달러에 달했습니다. 이러한 징후들은 병원 시스템, 학술 네트워크 및 전국적인 보험사를 통합한 미주신경 자극 시장에서의 성숙한 채널 전략과 일치합니다.

유럽은 2025년 수요의 상당 부분을 차지했으며, 벨기에에서는 비침습적 치료에 대한 보험 적용을 위한 정책적 움직임이 나타났는데, 이는 인근 지역의 보험사들 간에 더 광범위한 논의를 촉진할 가능성이 있습니다. 2025년 경부용 비침습적 시스템에 대한 보험 적용 결정은 두통 및 편두통에 대한 적응증이 신경 조절 요법 분야에서 다른 근거 기반 용도로의 발판이 될 수 있음을 보여주는 구체적인 사례입니다. 제조업체와 학술 파트너들이 지속적으로 제품 포트폴리오를 갱신하는 것은 이러한 정책 동향을 보완하는 것이며, 예측 기간 동안 유럽이 신경학 및 류마티스학 치료 경로에 의료기기의 근거를 통합할 수 있는 기반을 마련하고 있습니다.

아시아태평양의 장기적인 성장 추세는 임상 현장의 준비 상황, 환자 접근 프로그램, 그리고 새로운 기기 설계의 보급과 밀접한 관련이 있습니다. 중국과 일본 등에서는 최근 의료기기 승인 절차가 합리화되면서, 혁신적인 이식형 및 비침습형 VNS 시스템 시장 진출이 가속화되고 있습니다. 중국에서는 국가의약품감독관리국(NMPA)의 개혁에 따라 의료기기 심사 기간이 단축된 반면, 일본의 의약품 및 의료기기종합기구(PMDA)는 패스트트랙 제도 하에서 혁신적인 신경 치료법을 계속해서 우선적으로 심사하고 있습니다. 이러한 규제 측면의 개선에 힘입어 다국적 기업들은 해당 지역에서의 사업 확장을 가속화하고 있습니다. 또한, 보험 환급과 관련된 동향도 시장 확산을 뒷받침하고 있습니다. 일본에서는 몇년전부터 간질에 대한 VNS 요법이 국민건강보험 적용 대상이 되어, 환자들의 접근성이 크게 개선되었습니다. 마찬가지로, 호주에서는 약물 내성 간질에 대한 VNS 요법이 메디케어 급여 목록 및 민간 보험의 적용 범위에 포함되어 있습니다. 중국에서는 국가 보험 의약품 목록(NRDL) 및 각 성의 보험 급여 프로그램에 신경 질환 치료법이 순차적으로 추가되고 있어, 첨단 의료기기를 활용한 치료에 대한 비용 부담이 점차 줄어들고 있습니다. 폐루프형 소형 임플란트에 관한 최근의 무작위 대조 연구에서는 만성기 뇌졸중 환자 집단에서 재택 환경에서의 기능 개선이 확인되었으며, 이는 향후 아시아태평양의 선진국 시장에서 재활센터를 통한 치료 도입에 기여할 가능성이 있습니다. 신경계 질환 및 자가면역 질환을 대상으로 한 임상시험이 더욱 확대됨에 따라, 주요 도시의 의료 제공업체들은 국제적인 연구 성과를 활용하여 지역 보험사의 요건에 부합하는 다직종 협력 프로그램을 구축할 수 있게 될 것입니다. 이 기반은 예측 기간 동안 미주신경 자극 요법 시장의 도입이 지속적으로 확대되는 데 기여할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the vagus nerve stimulation market size is expected to increase from USD 555.15 million in 2025 to USD 598.96 million in 2026 and reach USD 969.76 million by 2031, growing at a CAGR of 10.12% over 2026-2031.

This report is Segmented by Product (Implantable VNS Devices and External VNS Devices), Application (Epilepsy, Depression, and Other Applications), End User (Hospitals, Neurology Clinics, and Other End Users), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Size and Forecasts are Provided in Terms of Value (USD) for all the Above Segments.

Global Vagus Nerve Stimulation Market Trends and Insights

Increasing Prevalence of Drug-Resistant Neurological Disorders

Across major care settings, the share of epilepsy patients classified as drug resistant remains high, with professional society communications describing a 20% to one-third range when two appropriate antiseizure medications fail to deliver sustained control. Clinical guidance continues to evolve toward earlier consideration of device-enabled neuromodulation when predicted probabilities of medication response are low, a shift that aligns with expanded programming options and longer-term benefit profiles in real-world cohorts. In treatment-resistant depression, evidence summaries describe sizable nonresponse to first-line pharmacotherapy and diminishing returns with successive switches, which raises the salience of device pathways that can deliver durable symptom relief in later lines of care. The most recent U.S. coverage reconsideration process for depression is now anchored in 24-month outcomes, including a 51.6% response rate and strong durability among earlier responders, which together inform how payers balance access and evidence requirements in the next cycle.As these dynamics converge, therapy awareness in neurology and psychiatry underscores broader applicability for both implantable and non-invasive systems in the vagus nerve stimulation market.

Shift Toward Neuromodulation Over Chronic Drug Therapy

Clinicians continue to weigh systemic side effects, adherence challenges, and quality-of-life trade-offs of multi-drug regimens against device-based neuromodulation that can be programmed and titrated over time. Longitudinal data show progressive efficacy with implantable systems in focal seizure types, reinforcing their positioning in later lines when respective surgery is contraindicated or declined. In depression, multi-year observational findings show clinically meaningful response and remission rates in cohorts that had exhausted numerous prior options, which supports a pathway to sustained benefit beyond typical pharmacologic ceilings. Head-to-head parity with non-invasive brain stimulation is not the standard of care, yet benchmark response rates for transcranial magnetic stimulation often cluster in the 50-60% range in standard programs, with durability dependent on maintenance strategies in many sites. Within the U.S., the coverage-with-evidence-development framework that constrained access to depression indications since 2019 is now under formal reconsideration, which could accelerate adoption if the final decision recognizes real-world durability in addition to symptom scales. Over the long run, health-economic analyses presented by manufacturers emphasize breakeven in a two-year window due to reductions in hospitalizations and emergency utilization, a narrative that continues to resonate with stakeholders watching the vagus nerve stimulation market.

High Upfront Cost of Implantable VNS System

Total acquisition and perioperative costs remain a near-term barrier, as implantable systems require specialist procedures, specialized surgical facilities, and ongoing follow-up programming. Further emphasizing the financial burden, a study based on a United States healthcare claims database found that the mean healthcare costs were approximately USD 123,500 per person in the 2 years prior to VNS implantation. U.S. reimbursement for end-of-service procedures has moved through proposed updates that would increase payment levels in 2026, although the direction and timing of final rulings will determine how much relief hospitals and clinics experience on cash flows. Access pathways for depression are still constrained in the United States because the current national coverage determination limits payment to coverage-with-evidence-development studies with extended follow-up. Commercial plans often require multiple medication failures and psychotherapy trials before approving implantable options, which elongates time-to-therapy for patients who remain symptomatic. Several payers classify implantable vagus nerve stimulation for depression as investigational or unproven in their 2026 policy manuals, reflecting an evidence posture that has not fully converged with multi-year observational findings. New autoimmune indications may alter the cost-benefit narrative, because the 2025 U.S. approval of neuroimmune modulation for rheumatoid arthritis arrived alongside a growth capital raise intended to support commercial rollout and real-world data generation. Manufacturers also present payer-facing analyses that place breakeven for implantable systems in a roughly two-year window due to fewer hospitalizations and emergency visits, which remains a key message in the vagus nerve stimulation market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Clinical Evidence and Label Expansion

- Advancement in Device Miniaturization and Closed-Loop Systems

- Surgical Risk and Patient Reluctance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Implantable devices held 58.10% of the vagus nerve stimulation market share in 2025, while external systems are projected to lead with a 10.64% CAGR to 2031. Expanded access for non-invasive systems after adolescent clearance in the United States, combined with outpatient usability, underpins volume gains in clinics and home settings. Department of Veterans Affairs purchasing increased meaningfully in 2024 and continued to grow in 2025, reinforcing procurement-led scale in which device training and standardized protocols can be rolled out across many centers. European policy follow-through in Belgium adds another access point, which in turn supports distribution and medical education economics outside the United Kingdom. As reimbursement channels diversify and clinical teams expand their experience sets, non-invasive options are gaining ground in the vagus nerve stimulation market for patients who do not want surgery or who benefit from rapid starts in outpatient care.

Implantable platforms continue to offer structural advantages in severe or refractory presentations, where continuous and algorithm-optimized stimulation can be programmed to long-term targets. Manufacturer reporting highlights steady neuromodulation revenue growth across 2025, with regional contributions from the United States and Europe supporting ongoing portfolio investment. Next-generation closed-loop concepts and miniaturized, battery-free implants tested in randomized trials point to shorter procedures and fewer generator exchanges over time, which could reduce barriers that have historically favored nonsurgical options. With product strategies that match patient preferences, the vagus nerve stimulation industry leans into a hybrid model, pairing robust implantable performance for highly refractory cases with non-invasive convenience where flexibility and speed matter most. As these approaches mature, diversified product lines can expand participation in the vagus nerve stimulation market across hospitals, neurology clinics, and veterans' health systems.

Geography Analysis

North America captured 58.22% of vagus nerve stimulation market share in 2025, and Asia-Pacific is poised to record an 11.93% CAGR through 2031. In the United States, the national coverage reconsideration process for depression has placed multi-year outcomes at the center of policy debate, which could affect access and utilization patterns across both implantable and non-invasive systems. 2024 financial disclosures showed steady gains in U.S. neuromodulation revenue, indicating stable demand through provider channels that rely on consistent programming and follow-up. Federal purchasing has become a meaningful driver for non-invasive devices, with 2024 veterans' system sales cited as a key growth component and 2025 revenues reaching near USD 32 million on a company-reported basis. These signals are consistent with a maturing channel strategy in the vagus nerve stimulation market that blends hospital systems, academic networks, and national payers.

Europe retained a significant portion of 2025 demand and displayed policy movement for non-invasive coverage in Belgium, which can catalyze broader discussions across neighbouring payers. The 2025 reimbursement decision for a cervical non-invasive system provides a concrete example of how headache and migraine indications can open a toehold for other evidence-based uses in neuromodulation. Ongoing portfolio updates from manufacturers and academic partners complement these policy developments, and they position Europe to integrate device evidence into neurology and rheumatology pathways over the forecast window.

Asia-Pacific's long-run growth trajectory ties to clinic readiness, patient access programs, and the diffusion of newer device designs. Countries such as China and Japan have streamlined medical device approval pathways in recent years, accelerating the entry of innovative implantable and non-invasive VNS systems. In China, reforms by the National Medical Products Administration (NMPA) have reduced device review timelines, while Japan's Pharmaceuticals and Medical Devices Agency (PMDA) continue to prioritize innovative neurological therapies under fast-track programs. These regulatory improvements are encouraging multinational manufacturers to expand their footprint across the region. Reimbursement developments are also strengthening market penetration. In Japan, VNS therapy for epilepsy has been covered under the national health insurance system for several years, significantly improving patient accessibility. Similarly, Australia includes VNS therapy for drug-resistant epilepsy under the Medicare Benefits Schedule and private insurance coverage frameworks. In China, inclusion of more neurological treatments under the National Reimbursement Drug List (NRDL) and provincial reimbursement programs is gradually improving affordability for advanced device-based therapies. Recent randomized research on closed-loop miniaturized implants has showcased at-home functional gains in chronic stroke cohorts, which may inform therapy adoption in rehabilitation hubs across developed APAC markets over time. As more trials launch across neurology and autoimmune conditions, providers in major cities can leverage international findings to build multidisciplinary programs that align with local payer requirements. This foundation supports a durable gradient for adoption in the vagus nerve stimulation market over the forecast horizon.

- Adriakaim, Inc.

- Beijing PINS Medical Co., Ltd

- Bionics Institute

- Brain Control Co. Ltd.

- electroCore, Inc.

- Evren Technologies, Inc.

- LivaNova

- MicroTransponder Inc.

- Neuropix

- Parasym

- Pulsetto

- SetPoint Medical

- Soterix Medical

- tVNS Health GmbH

- X Nerve

- ZENOWELL

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Drug-resistant Neurological Disorders

- 4.2.2 Shift Toward Neuromodulation Over Chronic Drug Therapy

- 4.2.3 Growing Clinical Evidence and Label Expansion

- 4.2.4 Advancement in Device Miniaturization and Closed-Loop Systems

- 4.2.5 Expansion of Non-Invasive VNS Applications

- 4.2.6 Home-Use and Remote Therapy Compatibility

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Implantable VNS System

- 4.3.2 Surgical Risk and Patient Reluctance

- 4.3.3 Limited Reimbursement for Non-Invasive VNS

- 4.3.4 Competition From Alternative Neuromodulation Therapies

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Implantable VNS Devices

- 5.1.2 External VNS Devices

- 5.2 By Application

- 5.2.1 Epilepsy

- 5.2.2 Depression

- 5.2.3 Other Applications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Neurology Clinics

- 5.3.3 Other End Users

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Adriakaim, Inc.

- 6.3.2 Beijing PINS Medical Co., Ltd

- 6.3.3 Bionics Institute

- 6.3.4 Brain Control Co. Ltd.

- 6.3.5 electroCore, Inc.

- 6.3.6 Evren Technologies, Inc.

- 6.3.7 LivaNova PLC

- 6.3.8 MicroTransponder Inc.

- 6.3.9 Neuropix

- 6.3.10 Parasym

- 6.3.11 Pulsetto

- 6.3.12 SetPoint Medical

- 6.3.13 Soterix Medical

- 6.3.14 tVNS Health GmbH

- 6.3.15 X Nerve

- 6.3.16 ZENOWELL

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment