|

시장보고서

상품코드

2064471

미국의 의료용 테이프 및 붕대 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)U.S. Medical Tapes And Bandages - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

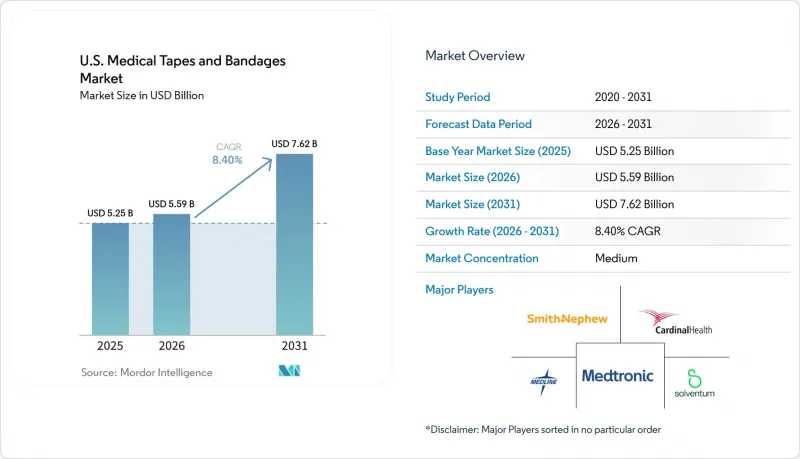

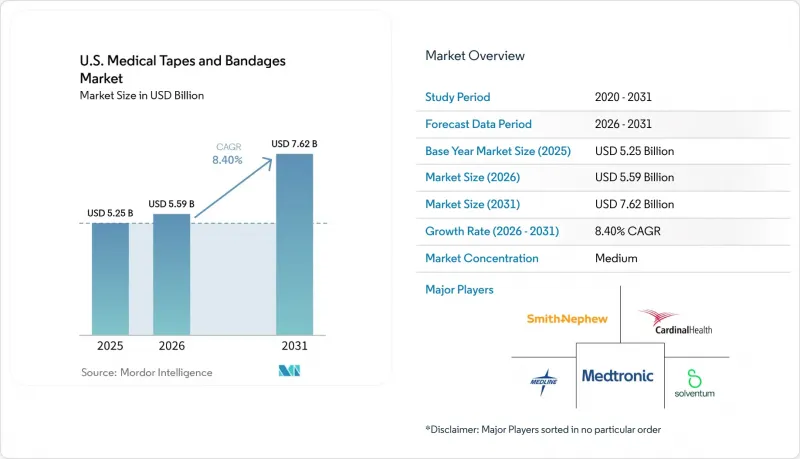

Mordor Intelligence에 의하면, 미국의 의료용 테이프 및 붕대 시장 규모는 2025년 52억 5,000만 달러로 평가되었고, 2026년에는 55억 9,000만 달러로 추정되고, 2026-2031년 CAGR 8.40%로 성장을 지속할 전망이며, 2031년까지 76억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품별(의료용 테이프, 드레싱, 붕대), 용도별(외과적 상처, 외상성 상처, 궤양, 스포츠 부상, 화상, 기타), 최종 사용자별(병원, 외래수술센터(ASC), 클리닉, 재택 헬스케어, 장기 요양 시설 및 전문 요양 시설, 소매, 군사), 유통 채널별(유통업체, 직접 판매, 기타)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 의료용 테이프 및 붕대 시장 동향과 인사이트

만성 상처와 당뇨병으로 인한 부담이 지속적인 수요를 창출하고 있습니다.

미국의 의료용 테이프 및 붕대 시장은 만성 상처와 당뇨병의 높은 유병률로 인해 안정적인 수요를 보이고 있습니다. 2025년에는 만성 상처가 1,050만 명의 메디케어 수급자에게 영향을 미치며, 연간 225억 달러의 의료비가 발생할 것으로 예상되며, 그중 상당 부분을 상처 드레싱이 차지하고 있습니다. 또한, 5,310만 명의 미국 당뇨병 환자는 평생 동안 15%-34%의 확률로 당뇨병성 족부 궤양을 발병할 위험에 직면해 있으며, 이로 인해 고정용 테이프, 테두리가 있는 드레싱, 붕대 시스템에 대한 지속적인 수요가 발생하고 있습니다. 이러한 제품들은 장기간에 걸친 치료 주기에 사용되기 때문에 보험 급여와 관련된 과제가 있음에도 불구하고 안정적인 수요가 확보되고 있습니다.

높은 외과 수술 건수와 ASC(외래수술센터(ASC))에서의 시술 건수가 테이프와 붕대 수요를 뒷받침하고 있습니다.

미국의 의료용 테이프 및 붕대 시장은 외래수술센터(ASC)로의 수술 전환이 진행되고 있는 데 힘입어 호조를 보이고 있습니다. 2024년에는 메디케어 인증을 받은 6,436곳의 외래수술센터(ASC)에서 640만 건의 메디케어 진료비 지급 대상 수술이 시행되었으며, 수혜자 1,000명당 수술 건수는 전년 대비 3.5% 증가했습니다. 인공 슬관절 치환술과 인공 고관절 치환술의 총 시술 건수 증가에 더해, 2026년 ASC 대상 시술 목록이 확대되어 560건의 시술이 추가됨에 따라, 외래 진료 현장에서의 상처 피복재 및 고정 제품에 대한 수요가 더욱 높아지고 있습니다.

2026년 CMS 지급 제도 개편이 클리닉의 상처 관리 경제 구조를 재편할 전망

미국의 의료용 테이프 및 붕대 시장에서는 클리닉에서의 상처 관리 분야에서 결제 방식에 있어 중대한 전환기를 맞이하고 있습니다. 2026 회계연도 의사 보수 일정에 관한 최종 규정에 따라, CMS는 일부 피부 대체재를 ‘부수적’ 소모품으로 재분류하고, 1제곱센티미터당 127.28달러의 전국 통일 지급률을 도입했습니다. 이로 인해, 1제곱센티미터당 2,000달러를 초과하는 상환을 가능하게 했던 기존의 ASP+6% 구조가 대체되었습니다. 이번 변경으로 인해 2026년에는 피부 대체재 서비스에 대한 메디케어의 종량제 지급 총액이 196억 달러 감소할 것으로 예상되며, 이는 중증 상처 치료의 경제성에 큰 변화를 가져올 것입니다. 클리닉에서는 기존 방식의 상처 관리 제품으로의 전환이 진행될 가능성이 있지만, 업무 흐름 조정에 따라 제품 선정이 지연될 우려가 있어 구매 행태에 단기적인 불확실성이 발생할 수 있습니다.

부문별 분석

2025년, 의료용 붕대는 매출의 38.45%를 차지하며 미국의 의료용 테이프 및 붕대 시장을 주도했습니다. 이러한 우위는 병원, 외래수술센터(ASC), 클리닉, 소매점, 가정 등에서 수술 후 관리, 압박 지지, 응급 처치, 일상적인 상처 덮개 용도로 널리 사용되고 있다는 점에 기인합니다. 의료기관과 일반 소비자의 양측 요구를 모두 충족시키는 붕대는 임상용 및 일반의약품(OTC) 유통 채널을 통해 안정적인 수요를 유지하고 있습니다.

가장 빠르게 성장하고 있는 부문인 의료용 테이프는 2026-2031년 연평균 성장률(CAGR) 8.25%를 달성할 것으로 전망됩니다. 이러한 성장은 CGM(연속 혈당 모니터링), 인슐린 펌프, 투명 필름 고정 테이프나 실리콘 테이프와 같은 첨단 테이프 형태의 채택 확대에 힘입어 이루어지고 있습니다. 접착력, 피부 친화성, 제거 시의 편안함에 대한 관심이 높아지면서 이 부문의 혁신이 촉진되고 있습니다.

2025년에는 외과적 상처가 매출의 35.66%를 차지했으며, 미국 의료용 테이프 및 붕대 시장에서 가장 큰 용도로 자리매김했습니다. 이는 수술 후 관리가 필요한 외래 및 당일 수술 건수가 많기 때문이며, 이로 인해 테이프, 드레싱, 붕대에 대한 안정적인 수요가 창출되고 있습니다.

가장 빠르게 성장하고 있는 용도인 ‘궤양 치료’는 2026-2031년 연평균 성장률(CAGR) 7.95%를 나타낼 것으로 예측됩니다. 이러한 성장은 당뇨병 환자 수 증가와 당뇨병성 궤양, 욕창, 정맥성 궤양 관리에 있어 기존 방식의 상처 치료에 대한 수요에 힘입어 이루어지고 있습니다. 2026년 CMS(미국 의료보험서비스센터)의 지급 제도 변경은 폼 드레싱 및 고정 테이프에 대한 수요를 더욱 부추기고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the u.S. medical tapes and bandages market size is expected to grow from USD 5.25 billion in 2025 to USD 5.59 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at 8.40% CAGR over 2026-2031.

This report is Segmented by Product (Medical Tapes, Dressings, Bandages), Application (Surgical Wounds, Traumatic Wounds, Ulcers, Sports Injuries, Burns, Others), End User (Hospitals, Ascs, Clinics, Home Healthcare, LTC/SNFs, Retail, Military), and Distribution Channel (Distributors, Direct Sales, and More). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Medical Tapes And Bandages Market Trends and Insights

Chronic Wound and Diabetes Burden Creating Persistent Volume Demand

The United States medical tapes and bandages market experiences steady demand due to the high prevalence of chronic wounds and diabetes. In 2025, chronic wounds impacted 10.5 million Medicare beneficiaries, generating USD 22.5 billion in annual care costs, with wound dressings comprising a significant share. Additionally, 53.1 million Americans with diabetes faced a 15%-34% lifetime risk of diabetic foot ulcers, driving recurring demand for securement tapes, bordered dressings, and bandage systems. These products are consumed over extended treatment cycles, ensuring consistent demand despite reimbursement challenges.

High Surgical and ASC Procedure Volumes Sustaining Core Tape and Bandage Demand

The United States medical tapes and bandages market benefits from the growing shift of procedures to ambulatory surgery centers (ASCs). In 2024, 6,436 Medicare-certified ASCs performed 6.4 million fee-for-service Medicare procedures, with a 3.5% year-over-year increase in procedure volume per 1,000 beneficiaries. Rising total knee and hip arthroplasty volumes, along with the 2026 ASC Covered Procedure List expansion adding 560 procedures, further boost demand for wound covering and securement products in outpatient settings.

2026 CMS Payment Reset Reshaping Office Wound Care Economics

The United States medical tapes and bandages market is experiencing a major payment shift in office-based wound care. Under the CY 2026 Physician Fee Schedule final rule, CMS reclassified several skin substitutes as "incident-to" supplies and introduced a flat national payment rate of USD 127.28 per square centimeter, replacing the previous ASP+6% structure that allowed reimbursements exceeding USD 2,000 per square centimeter. This change is expected to reduce gross Medicare fee-for-service spending on skin substitute services by USD 19.6 billion in 2026, significantly altering advanced wound treatment economics. While physician offices may shift toward conventional wound products, the disruption could delay product decisions as workflows adjust, creating short-term uncertainty in purchasing behavior.

Other drivers and restraints analyzed in the detailed report include:

- Wearable Medical Devices Redefining Adhesive Tape Specifications

- Payer-Driven Home Care Migration Expanding Alternate-Site Product Needs

- GPO Consolidation Compressing Institutional Tape and Bandage Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Medical Bandages accounted for 38.45% of revenue, leading the United States medical tapes and bandages market. Their dominance stems from extensive use in post-operative care, compression support, first-aid treatment, and routine wound covering across hospitals, ASCs, physician offices, retail stores, and homes. Serving both institutional and consumer needs, bandages maintain stable demand across clinical and over-the-counter channels.

Medical Tapes, the fastest-growing segment, is projected to achieve an 8.25% CAGR from 2026 to 2031. Growth is driven by increased adoption of CGMs, insulin pumps, and advanced tape formats like transparent film securement and silicone tapes. Enhanced focus on adhesion, skin tolerance, and removal comfort is driving innovation in this segment.

Surgical wounds contributed 35.66% of revenue in 2025, making them the largest application in the United States medical tapes and bandages market. This is linked to the high volume of outpatient and ambulatory procedures requiring post-treatment care, creating consistent demand for tapes, dressings, and bandages.

Ulcer Treatment, the fastest-growing application, is expected to post a 7.95% CAGR from 2026 to 2031. Growth is fueled by the diabetic population and demand for conventional wound care in managing diabetic, pressure, and venous ulcers. CMS payment changes in 2026 are further driving demand for foam dressings and securement tapes.

List of Companies Covered in this Report:

- AERO Healthcare

- B. Braun

- Cardinal Health

- Coloplast

- Convatec Group plc

- DeRoyal Industries

- Dukal

- Dynarex

- Essity Health & Medical

- HALYARD

- Hartmann Group

- Integra LifeSciences

- Kenvue Brands LLC

- Mckesson

- Medline Industries

- Medtronic

- Molnlycke Health Care

- Smiths Group

- Solventum Corporation

- Urgo Medical North America LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Chronic Wound and Diabetes Burden

- 4.2.2 High Surgical and ASC Procedure Volumes

- 4.2.3 Aging Patient Mix and Pressure Injury Risk

- 4.2.4 Shift Toward Home and Alternate-Site Wound Care

- 4.2.5 Adhesive Securement Demand from CGMs, Insulin Pumps, and Other Wearables

- 4.2.6 CMS Site-of-Care and Supply Reimbursement Mechanics Favor Efficient, Easy-Apply Products

- 4.3 Market Restraints

- 4.3.1 MARSI and Skin Irritation Risk

- 4.3.2 Pricing Pressure from GPOS and Distributor Consolidation

- 4.3.3 2026 Skin-Substitute Payment Reset Disrupting Office Wound-Care Purchasing

- 4.3.4 Routine-Vs-Nonroutine Supply Reimbursement Complexity in Home Care

- 4.4 Supply/Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Medical Tapes

- 5.1.1.1 Paper Tapes

- 5.1.1.2 Fabric Tapes

- 5.1.1.3 Plastic Tapes

- 5.1.1.4 Silicone / Acrylic / Rubber Tapes

- 5.1.1.5 Transparent Film / Dressing Retention Tapes

- 5.1.1.6 Elastic / Waterproof / Specialty Tapes

- 5.1.2 Dressings

- 5.1.2.1 Foam Dressings

- 5.1.2.2 Hydrocolloid Dressings

- 5.1.2.3 Film Dressings

- 5.1.2.4 Alginate Dressings

- 5.1.2.5 Hydrogel Dressings

- 5.1.2.6 Collagen Dressings

- 5.1.2.7 Superabsorbent Dressings

- 5.1.2.8 Antimicrobial Dressings

- 5.1.2.9 Other Advanced Dressings

- 5.1.3 Medical Bandages

- 5.1.3.1 Adhesive Bandages / First Aid Bandages

- 5.1.3.2 Gauze Bandage Rolls

- 5.1.3.3 Elastic Bandage Rolls

- 5.1.3.4 Cohesive / Self-Adherent Bandages

- 5.1.3.5 Conforming Bandages

- 5.1.3.6 Triangular Bandages

- 5.1.3.7 Orthopedic / Cast Bandages

- 5.1.3.8 Others

- 5.1.1 Medical Tapes

- 5.2 By Application

- 5.2.1 Surgical Wounds

- 5.2.2 Traumatic Wounds

- 5.2.3 Ulcers Treatment

- 5.2.4 Sports Injuries

- 5.2.5 Burn Injuries

- 5.2.6 Sport Injuries

- 5.2.7 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers

- 5.3.3 Clinics and Physician Offices

- 5.3.4 Home Healthcare

- 5.3.5 Long-Term Care and Skilled Nursing Facilities

- 5.3.6 Retail / Consumer Self-Care

- 5.3.7 Military and Emergency Care

- 5.4 By Distribution Channel

- 5.4.1 Distributors

- 5.4.2 Direct Sales / Enterprise Contracts

- 5.4.3 Retail Pharmacies

- 5.4.4 E-commerce / Online Medical Supply

- 5.4.5 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AERO Healthcare

- 6.3.2 B. Braun SE

- 6.3.3 Cardinal Health Inc.

- 6.3.4 Coloplast A/S

- 6.3.5 Convatec Group plc

- 6.3.6 DeRoyal Industries Inc.

- 6.3.7 Dukal

- 6.3.8 Dynarex

- 6.3.9 Essity Health & Medical

- 6.3.10 HALYARD

- 6.3.11 HARTMANN USA, Inc.

- 6.3.12 Integra LifeSciences Holdings Corporation

- 6.3.13 Kenvue Brands LLC

- 6.3.14 McKesson Corporation

- 6.3.15 Medline Industries Inc.

- 6.3.16 Medtronic plc

- 6.3.17 Molnlycke Health Care AB

- 6.3.18 Smith & Nephew plc

- 6.3.19 Solventum Corporation

- 6.3.20 Urgo Medical North America LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment