|

시장보고서

상품코드

2064484

결합조직질환 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Connective Tissue Disease - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

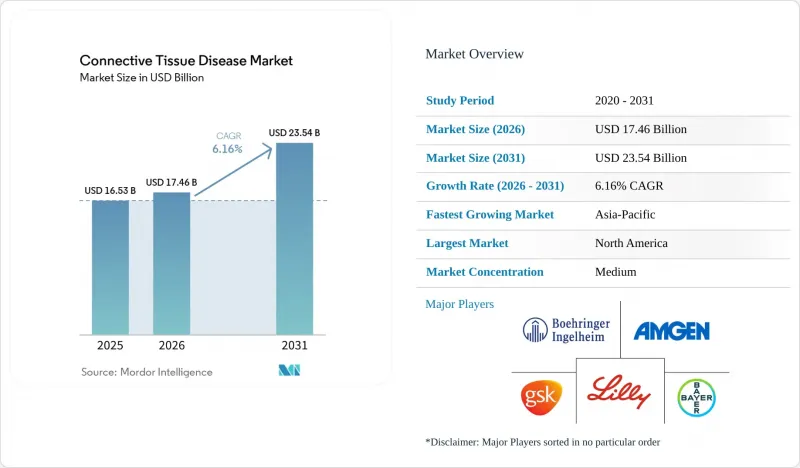

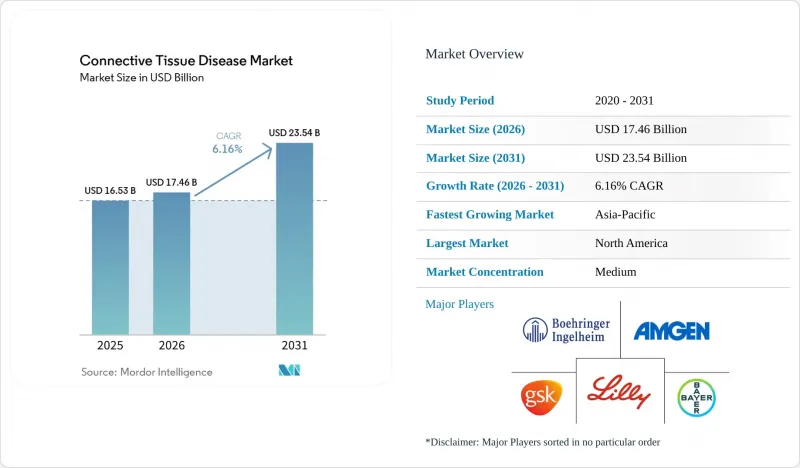

Mordor Intelligence에 의하면, 결합조직질환 시장 규모는 2025년 165억 3,000만 달러로 평가되었습니다. 2026년에는 174억 6,000만 달러로 확대되어 2031년까지 235억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 6.16%를 나타낼 전망입니다.

본 보고서는 질환별(RA, SLE, 경피증, 다발성 근염, 피부근염, 쇼그렌 증후군, MCTD, UCTD), 약물 분류별(바이오의약품, 의약품), 투여 경로(경구, 주사, 외용), 유통 채널(병원, 소매, 온라인 약국), 지역(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)별로 분류되어 있습니다.

세계의 결합조직질환 시장 동향 및 인사이트

루푸스 신염 및 SSc-ILD에 대한 새로운 치료 옵션

결합조직 질환 치료 시장에서 루푸스 신염은 경쟁이 더욱 치열한 단계로 접어들고 있습니다. 이는 2025년 하반기에 오비누츠주맙이 새로운 항-CD20 치료제로 추가되었기 때문입니다. 2025년 10월 FDA 승인과 2025년 12월 유럽집행위원회의 승인을 통해, 활동성 III 및 IV 등급 질환에 대해 제3상 임상시험 결과를 바탕으로 한 새로운 치료 옵션이 임상의들에게 제공되었습니다. REGENCY 임상시험에서는 환자의 46.4%가 완전한 신장 반응을 보인 반면, 표준 치료에서는 33.1%에 그쳤습니다. 이를 통해 처방 의사 및 보험사 입장에서는 보다 광범위한 도입을 위한 명확한 근거를 확보하게 되었습니다. SSc-ILD의 경우, SENSCIS-ON 임상시험의 3년 데이터가 닌테다닙의 지속적 사용을 뒷받침했으며, 2025년 네트워크 메타분석에서는 평가 대상 치료법 중 토실리주맙이 FVC 저하를 지연시키는 효과 측면에서 최상위 순위를 차지했습니다. 이러한 데이터가 축적됨에 따라, 결합조직 질환 치료 시장은 루푸스 신염이나 섬유화를 동반한 폐 병변의 경우, 제한적인 응급 치료에서 보다 명확한 치료 경로로 전환되고 있습니다.

ACR/CHEST를 통한 ILD 선별 검사 확대

또한, ACR과 CHEST가 RA, SSc, IIM, MCTD 및 쇼그렌 증후군에 대한 선별 검사 및 모니터링 권고안을 공동으로 마련함에 따라, 보다 체계적인 ILD 치료 경로가 확립되었으며, 이는 결합조직질환 치료 시장에도 긍정적인 영향을 미치고 있습니다. 이 지침에서는 고위험 환자에 대해 초진 시 흉부 고해상도 CT(HRCT) 및 폐기능 검사를 실시할 것을 권장하고 있으며, 이를 통해 폐 병변이 진행되기 전에 발견될 가능성이 높아집니다. 또한, IIM-ILD 및 SSc-ILD의 경우 첫 해에 면밀한 모니터링을 실시할 것을 권장하며, 이를 통해 류마티스과에서의 추적 관찰에서 호흡기과로의 의뢰까지 걸리는 시간을 단축할 수 있습니다. 부속된 치료 지침에서는 조건부 1차 치료제로 닌테다니브와 토시리주맙이 제시되어 있으므로, 진단 결과가 치료법 선택에 직접적으로 반영되도록 되어 있습니다. 유럽에서는 2025년 ERS 및 EULAR 지침에서 SLE를 포함함으로써 이 틀이 확대되었으며, 25개의 PICO에 기반한 권고 사항이 추가되었습니다. 이를 통해 지역 전체의 보험 급여 및 진료 관행의 통합이 촉진되고 있습니다.

생물학적 제제 및 전문 치료제의 높은 비용

치료 선택지가 확대되었다고는 하지만, 많은 환자에게 생물학적 제제는 여전히 고가이기 때문에 결합조직질환 치료 시장은 여전히 접근성 측면에서 장벽에 직면해 있습니다. 『The American Journal of Managed Care』지에 게재된 2025년 체계적 문헌고찰에 따르면, 미국 피부과 환자의 70% 이상이 면역매개성 질환에 대한 생물학적 제제 사용의 주요 장벽으로 높은 본인부담금을 꼽았습니다. 루푸스, 류마티스 관절염 및 관련 질환은 대개 장기간의 치료와 반복적인 모니터링이 필요하기 때문에 이와 유사한 비용 부담은 CTD(결합조직질환) 치료에서도 중요한 문제가 됩니다. 가격 협상이나 바이오시밀러 시장 진입을 통해 취득 비용은 절감할 수 있지만, 본인 부담금, 면책액, 진료 장소별 비용 등을 고려하면 경제적 부담의 격차를 완전히 해소할 수는 없습니다. 이는 특히 상환 관리가 엄격한 의료 제도 하에서 결합조직질환 치료 시장이 실제 치료 건수 증가 속도보다 임상적으로는 더 빠른 속도로 확대될 수 있음을 의미합니다.

부문별 분석

2025년 기준으로, 류마티스 관절염은 결합조직질환 치료 시장의 41.23%를 차지하며, 해당 시장에서 질환별 매출 기준 중 가장 큰 비중을 차지했습니다. 이러한 위상은 진단 건수의 많음, 성숙한 생물학적 제제를 통한 치료 경로, 그리고 DMARD(비생물학적 항류마티스제)와 생물학적 제제의 병용 요법에 대한 의사들의 오랜 경험을 반영하고 있습니다. 전신성 홍반성 루푸스는 2031년까지 연평균 성장률(CAGR) 8.23%로 확대될 것으로 예측되며, 결합조직질환 치료 시장에서 가장 빠르게 성장하는 질환 부문이 될 전망입니다. 2025년 하반기와 2026년에 승인된 오비누츠주맙, 피하 투여용 아니플로르맙, 그리고 소아용 베리무맙 자동 주사기는 루푸스 신염 및 더 광범위한 SLE 치료에 있어 치료 옵션을 확대했습니다. 또한, 중국에서 실시된 테리타시셉트의 3상 임상시험에서는 52주 시점에서 SRI-4 반응률이 67.1%(위약군은 32.7%)로 보고되었으며, 이는 SLE 치료제 파이프라인이 현재 시판 중인 약물을 뛰어넘어 더욱 확대되고 있음을 보여줍니다.

결합조직 질환 치료 시장에서는 피부경화증(전신성 피부경화증)에 대해 닌테다니브와 토시리주맙을 주축으로 한 2제 병용 요법을 통한 간질성 폐질환(ILD) 치료 방식이 지지를 얻고 있습니다. 쇼그렌 증후군의 경우, 생물학적 제제가 전 세계적으로 승인되지 않았기 때문에 여전히 명백한 미개척 분야이며, BAFF 경로 및 관련 자가면역 질환 연구 프로그램에 대한 관심은 여전히 높습니다. 다발성 근염 및 피부근염은 여전히 소규모 시장이지만, 2025년 조사에 따르면 피부근염 환자는 진단까지 평균 24.3주가 소요되었으며, 34%의 사례에서 초기 단계에 오진을 받은 것으로 나타났기 때문에 미충족 의료 수요가 심각한 수준입니다. 혼합성 결합조직 질환 및 미분화형 CTD는 여전히 인접 적응증에서 차용한 치료법에 크게 의존하고 있지만, 새로운 ILD 선별 검사 프로토콜 덕분에 이러한 환자들이 더 조기에 전문의의 진료를 받을 가능성이 높아지고 있습니다.

2025년 기준으로, 결합조직질환 치료 시장 규모의 63.12%를 바이오의약품이 차지했으며, 바이오의약품은 계속해서 해당 시장의 주요 가치 창출 요인으로 자리 잡고 있습니다. TNF-α 억제제, IL-6 수용체 길항제 및 BLyS 억제제는 더 광범위한 질환군과 확립된 치료 경로에서 사용되고 있기 때문에 이 범주의 핵심을 이루고 있습니다. 또한, 이 범주는 루푸스 신염 및 CTD-ILD에 대한 적응증 확대가 반복되고, 보다 명확한 적응증 범위가 확립됨에 따라 혜택을 보고 있습니다. 2025년부터 2026년에 걸친 일본의 PMDA 심사 주기 동안, SLE 치료용 피하 투여형 아니플로르맙과 신규 토시리주맙 바이오시밀러가 승인되었습니다. 이러한 요소들은 혁신과 저비용 생물학적 제제에 대한 접근성을 모두 뒷받침합니다. 이로 인해 성숙한 시장에서 가격 경쟁이 격화되더라도, 바이오의약품은 계속해서 중심적인 위치를 차지하게 될 것입니다.

의약품 시장은 2031년까지 연평균 성장률(CAGR) 7.93%를 나타낼 것으로 예측되며, 이는 결합조직질환 치료 시장에서 성장률이 가장 높은 의약품 분류가 될 것입니다. JAK 억제제 및 기타 면역억제제는 생물학적 제제의 보급이 여전히 고르지 않은 분야에서 확대 여지가 남아 있는 반면, NSAIDs, 코르티코스테로이드 및 기존 DMARDs는 여전히 상당한 처방량을 차지하고 있습니다. 또한 PMDA는 2025년부터 2026년까지의 승인 주기에서 거대세포동맥염 치료제인 우파다시티닙을 승인함으로써, 표적 지향형 경구용 면역학 약물에 대한 규제 당국의 지속적인 지지를 보여주고 있습니다. 동시에, 2025년 4월 RINVOQ의 첨부문서 및 2025년 10월 XELJANZ의 첨부문서에는 모니터링 의무가 명시되어 있으며, 이는 결합조직 질환 치료 시장의 해당 분야가 어느 정도의 속도로 확대될 수 있을지를 좌우하게 될 것입니다.

지역별 분석

2025년, 북미는 결합조직 질환 치료 시장 점유율의 43.62%를 차지하며, 이 지역은 전 세계 매출의 중심지로서의 위상을 유지했습니다. 그 기반의 상당 부분은 미국이 차지하고 있는데, 이는 전문의에 대한 접근성, 생물학적 제제의 이용 가능성, 그리고 보험 적용 범위가 다른 많은 지역보다 여전히 우수하기 때문입니다. 2026년에도 FDA의 제품 승인 확대는 치료 대상 환자층을 지속적으로 넓히고 있으며, 특히 피하 투여용 아니플로르맙 및 소아용 베리뮐맙 자동 주사기의 승인 이후에는 그 추세가 두드러집니다. 북미의 결합조직 질환 치료 시장은 CTD-ILD의 선별 검사 및 치료에 대한 명확한 지침의 뒷받침도 받고 있으며, 이를 통해 고위험군 환자에 대한 조기 개입이 촉진되고 있습니다. 이를 통해 확립된 류마티스 관절염 치료는 물론, 성장률이 높은 루푸스 및 간질성 폐질환(ILD)의 치료 사례에서도 해당 지역의 경쟁력이 유지되고 있습니다.

유럽은 광범위한 전문의 네트워크와 확립된 생물학적 제제 치료 기반을 바탕으로, 결합조직질환 치료 시장에서 여전히 2위를 차지하고 있습니다. 2025년 12월 유럽집행위원회가 루푸스 신염 치료제인 가지바로와 전신성 홍반성 루푸스(SLE) 치료제인 피하 투여형 사프네로를 승인한 것은 중증 루푸스 치료에 새로운 활력을 불어넣었습니다. 2025년 ERS 및 EULAR의 CTD-ILD 지침에서는 SLE에 대한 정책적 틀도 확대되어, 지역 전체에서 보다 표준화된 폐 검진 및 치료 결정이 촉진되고 있습니다. 서유럽이 계속해서 주요 수요 거점으로 자리매김하는 한편, 남유럽 및 동유럽 시장에서는 바이오시밀러 및 모니터링 경로가 성숙해짐에 따라 수요가 점차 증가할 것으로 전망됩니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 9.18%를 기록하며 성장할 것으로 예상되며, 결합조직질환 치료 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 일본은 이러한 성장 속도를 이끄는 요인 중 하나입니다. 이는 PMDA가 2025년부터 2026년까지의 승인 주기에서 SLE 치료용 피하 투여형 아니플로르마브, 거대세포동맥염 치료용 우파다시티닙, 그리고 신규 토시리주맙 바이오시밀러를 승인했기 때문입니다. 지역별 질환 발견률도 향상되고 있으며, 2025년 메타분석에 따르면 아시아·태평양 지역의 전신성 경피증 발생률은 10만 명년당 3.20명인 것으로 보고되었습니다. 또한, 2013년 이후의 진단 기준에 따르면, 기존의 정의보다 훨씬 더 많은 사례가 확인되고 있습니다. 중국, 한국, 인도, 호주는 생물학적 제제에 대한 접근성과 전문의의 진단이 지속적으로 확대되는 가운데, 결합조직질환 치료 시장에서 여전히 중요한 수요 기회를 제공합니다. 중동 및 아프리카와 남미는 여전히 시장 점유율이 낮은 편이지만, 공적 보험을 통한 보상이나 도시 지역의 전문의 체계가 고비용인 자가면역 질환 치료를 뒷받침할 수 있는 지역에서는 수요가 서서히 증가하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the connective tissue disease market size is expected to increase from USD 16.53 billion in 2025 to USD 17.46 billion in 2026 and reach USD 23.54 billion by 2031, growing at a CAGR of 6.16% over 2026-2031.

This report is Segmented by Disease (RA, SLE, Scleroderma, Polymyositis, Dermatomyositis, Sjogren's Syndrome, MCTD, UCTD), Drug Class (Biopharmaceuticals, Pharmaceuticals), Route of Administration (Oral, Injectable, Topical), Distribution Channel (Hospital, Retail, Online Pharmacies), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts in Value (USD).

Global Connective Tissue Disease Market Trends and Insights

New Options for Lupus Nephritis and SSc-ILD

Within the connective tissue disease treatment market, lupus nephritis is moving into a more competitive phase because obinutuzumab added a new anti-CD20 option in late 2025. FDA approval in October 2025 and European Commission approval in December 2025 gave clinicians a new option with phase 3 backing in active Class III and IV disease. In REGENCY, 46.4% of patients achieved complete renal response versus 33.1% on standard therapy, which gave prescribers and payers a clearer basis for wider uptake. In SSc-ILD, 3-year SENSCIS-ON data supported continued nintedanib use, and a 2025 network meta-analysis ranked tocilizumab highest for slowing FVC decline across evaluated options. As these data accumulate, the connective tissue disease treatment market is moving away from narrow rescue options and toward more defined treatment pathways in lupus nephritis and fibrosing lung involvement.

ACR/CHEST ILD Screening Expansion

The connective tissue disease treatment market is also benefiting from a more structured ILD care pathway after the ACR and CHEST jointly set screening and monitoring recommendations for RA, SSc, IIM, MCTD, and Sjogren disease. The guideline recommends HRCT chest and pulmonary function testing at presentation for high-risk patients, which increases the chance that lung involvement is identified before advanced progression. It also supports close monitoring in the first year for IIM-ILD and SSc-ILD, which reduces the time between rheumatology follow-up and pulmonary referral. The companion treatment guideline names nintedanib and tocilizumab among conditional first-line options, so diagnosis is translating more directly into therapy selection. In Europe, the 2025 ERS and EULAR guidance widened this framework by including SLE and adding 25 PICO-based recommendations, which support reimbursement and practice alignment across the region.

High Biologic and Specialty-Drug Costs

Even with broader treatment choice, the connective tissue disease treatment market still faces an access ceiling because biologics remain expensive for many patients. A 2025 systematic review in The American Journal of Managed Care found that more than 70% of U.S. dermatology patients cited high out-of-pocket costs as a main barrier to biologics for immune-mediated disease. The same cost pressure matters in CTD care because lupus, rheumatoid arthritis, and related disorders often require long treatment duration and repeated monitoring. Price negotiation and biosimilar entry can reduce acquisition cost, but they do not fully remove affordability gaps once co-pays, deductibles, and site-of-care charges are included. This means the connective tissue disease treatment market can expand clinically faster than it expands in real-world treated volume, especially in systems with tighter reimbursement controls.

Other drivers and restraints analyzed in the detailed report include:

- CAR-T Pipeline in Refractory Lupus

- Home-Administration Expansion in Lupus Biologics

- Safety Monitoring Burden for JAKs and Immunosuppressants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rheumatoid arthritis held 41.23% of the connective tissue disease treatment market share in 2025, which gave the connective tissue disease treatment market its largest disease revenue base. That position reflects higher diagnosed volume, a mature biologic treatment pathway, and long-standing physician familiarity with DMARD and biologic sequencing. Systemic lupus erythematosus is projected to expand at 8.23% CAGR through 2031, making it the fastest-growing disease segment in the connective tissue disease treatment market. Late 2025 and 2026 approvals of obinutuzumab, subcutaneous anifrolumab, and the pediatric belimumab autoinjector widened options across lupus nephritis and broader SLE care. A phase 3 telitacicept study in China also reported 67.1% SRI-4 response versus 32.7% on placebo at 52 weeks, which shows that the SLE pipeline is deepening beyond current marketed agents.

In the connective tissue disease treatment market, scleroderma or systemic sclerosis is gaining support from a two-drug ILD treatment pattern built around nintedanib and tocilizumab. Sjogren's syndrome remains a clear white space because no biologic has global approval, which keeps interest high in BAFF-pathway and adjacent autoimmune programs. Polymyositis and dermatomyositis remain smaller segments, but the unmet need is acute because dermatomyositis patients waited a mean 24.3 weeks to diagnosis and were initially misdiagnosed in 34% of cases in a 2025 survey. Mixed connective tissue disease and undifferentiated CTD still rely heavily on therapies borrowed from adjacent indications, while new ILD screening protocols are improving the odds that these patients reach specialist care sooner.

Biopharmaceuticals accounted for 63.12% share of the connective tissue disease treatment market size in 2025, and biologics remained the main value driver in the connective tissue disease treatment market. TNF-alpha inhibitors, IL-6 receptor antagonists, and BLyS inhibitors anchor this category because they are used across larger disease pools and established treatment pathways. The class also benefits from repeated label expansion and more defined use in lupus nephritis and CTD-ILD. Japan's 2025 to 2026 PMDA cycle approved subcutaneous anifrolumab for SLE and new tocilizumab biosimilars, which support both innovation and lower-cost biologic access. This keeps biopharmaceuticals central even when price competition increases in mature markets.

Pharmaceuticals are projected to grow at 7.93% CAGR through 2031, which makes them the fastest-growing drug class in the connective tissue disease treatment market. JAK inhibitors and other immunosuppressants still have room to expand in settings where biologic penetration remains uneven, while NSAIDs, corticosteroids, and conventional DMARDs continue to support large prescription volumes. The PMDA also approved upadacitinib for giant cell arteritis in the 2025 to 2026 cycle, showing continued regulatory support for targeted oral immunology agents. At the same time, the April 2025 RINVOQ label and the October 2025 XELJANZ label keep monitoring obligations visible, which shapes how fast this part of the connective tissue disease treatment market can scale.

Geography Analysis

North America held 43.62% of the connective tissue disease treatment market share in 2025, which kept the region at the center of global revenue. The United States accounts for most of that base because specialist access, biologic availability, and reimbursement depth remain stronger than in many other regions. In 2026, FDA-backed product expansion is still widening the treatable pool, especially after approvals for subcutaneous anifrolumab and the pediatric belimumab autoinjector. The connective tissue disease treatment market in North America also benefits from clear guideline support for CTD-ILD screening and treatment, which helps move high-risk patients toward earlier intervention. This keeps the region strong in both established rheumatoid arthritis care and higher-growth lupus and ILD use cases.

Europe remains the second-largest regional block in the connective tissue disease treatment market, supported by broad specialist networks and a well-established biologic treatment base. The December 2025 European Commission approvals for Gazyvaro in lupus nephritis and subcutaneous Saphnelo in SLE added fresh momentum in severe lupus care. The 2025 ERS and EULAR CTD-ILD guideline also extended the policy framework to SLE, which supports more standardized lung screening and treatment decisions across the region. Western Europe is likely to remain the main demand center, while Southern and Eastern markets add incremental volume as biosimilar and monitoring pathways mature.

Asia-Pacific is projected to grow at 9.18% CAGR through 2031, making it the fastest-growing region in the connective tissue disease treatment market size. Japan is helping drive that pace because the PMDA approved subcutaneous anifrolumab for SLE, upadacitinib for giant cell arteritis, and new tocilizumab biosimilars in the 2025 to 2026 cycle. Regional disease detection is also improving, and a 2025 meta-analysis reported pooled systemic sclerosis incidence in Asia-Pacific at 3.20 per 100,000 person-years, with post-2013 criteria identifying far more cases than older definitions. China, South Korea, India, and Australia remain important volume opportunities for the connective tissue disease treatment market as biologic access and specialist diagnosis continue to widen. The Middle East, Africa, and South America still hold smaller shares, but they add gradual demand where public reimbursement and urban specialist capacity can support higher-cost autoimmune care.

- Abbvie

- Amgen

- AstraZeneca

- Aurinia Pharmaceuticals Inc.

- Bayer

- Biogen

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Calliditas Therapeutics AB

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd. / Genentech, Inc.

- GlaxoSmithKline

- Johnson & Johnson Innovative Medicine

- Merck

- Novartis

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Teva Pharmaceutical Industries

- UCB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Diagnosed Autoimmune CTD Burden

- 4.2.2 Biologics and Targeted Therapy Penetration

- 4.2.3 New Options for Lupus Nephritis and SSC-ILD

- 4.2.4 ACR/CHEST ILD Screening Expansion

- 4.2.5 CAR-T Pipeline in Refractory Lupus

- 4.2.6 Home-Administration Expansion in Lupus Biologics

- 4.3 Market Restraints

- 4.3.1 High Biologic and Specialty-Drug Costs

- 4.3.2 Safety Monitoring Burden for JAKs and Immunosuppressants

- 4.3.3 Cell-Therapy Delivery and Long Follow-Up Constraints

- 4.3.4 Delayed Diagnosis in Overlap and Seronegative CTD Cases

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Disease

- 5.1.1 Rheumatoid Arthritis

- 5.1.2 Systemic Lupus Erythematosus

- 5.1.3 Scleroderma / Systemic Sclerosis

- 5.1.4 Polymyositis

- 5.1.5 Dermatomyositis

- 5.1.6 Sjogren's Syndrome

- 5.1.7 Mixed Connective Tissue Disease

- 5.1.8 Undifferentiated Connective Tissue Disease

- 5.2 By Drug Class

- 5.2.1 Biopharmaceuticals

- 5.2.1.1 Biologics

- 5.2.1.2 Biosimilars

- 5.2.2 Pharmaceuticals

- 5.2.2.1 NSAIDs

- 5.2.2.2 DMARDs

- 5.2.2.3 Corticosteroids

- 5.2.2.4 Immunosuppressants

- 5.2.2.5 Antimalarial Drugs

- 5.2.2.6 Other Pharmaceuticals

- 5.2.1 Biopharmaceuticals

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Injectable

- 5.3.2.1 Intravenous

- 5.3.2.2 Subcutaneous

- 5.3.3 Topical

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Amgen Inc.

- 6.3.3 AstraZeneca plc

- 6.3.4 Aurinia Pharmaceuticals Inc.

- 6.3.5 Bayer AG

- 6.3.6 Biogen Inc.

- 6.3.7 Boehringer Ingelheim International GmbH

- 6.3.8 Bristol Myers Squibb Company

- 6.3.9 Calliditas Therapeutics AB

- 6.3.10 Eli Lilly and Company

- 6.3.11 F. Hoffmann-La Roche Ltd. / Genentech, Inc.

- 6.3.12 GSK plc

- 6.3.13 Johnson & Johnson Innovative Medicine

- 6.3.14 Merck & Co., Inc.

- 6.3.15 Novartis AG

- 6.3.16 Pfizer Inc.

- 6.3.17 Regeneron Pharmaceuticals, Inc.

- 6.3.18 Sanofi

- 6.3.19 Teva Pharmaceutical Industries Ltd.

- 6.3.20 UCB S.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment