|

시장보고서

상품코드

2064496

임상시험용 포장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Clinical Trial Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

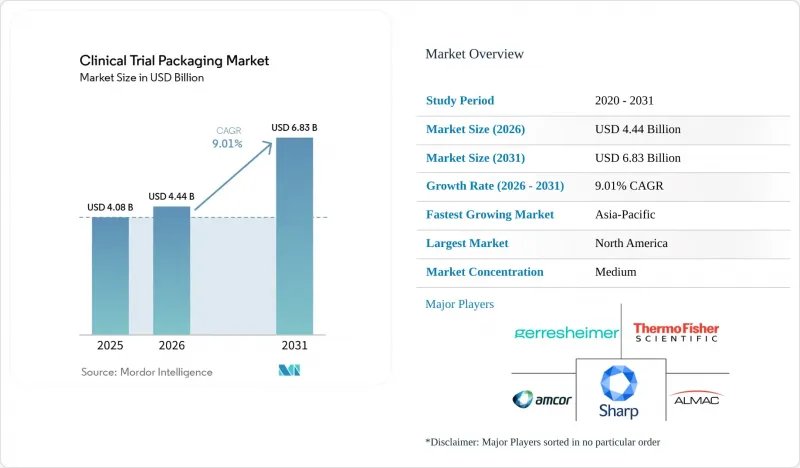

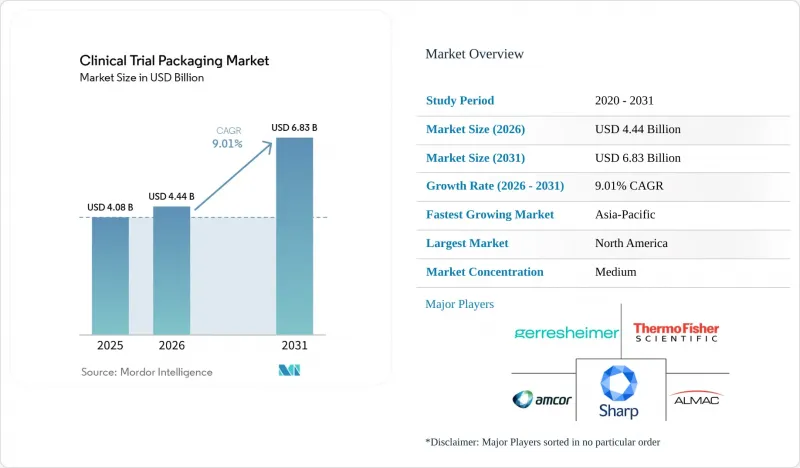

Mordor Intelligence에 의하면, 임상시험용 포장 시장 규모는 2025년에 40억 8,000만 달러로 평가되었습니다. 2026년에 44억 4,000만 달러에서 2031년까지 68억 3,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR은 9.01%를 나타낼 전망입니다.

본 보고서는 제품 유형(바이알 및 앰플, 주사기, 블리스터 팩, 병, 백 및 파우치, 튜브, 소포장 등), 소재 유형(플라스틱, 종이 및 골판지, 유리, 금속), 최종 사용자(연구 기관, 임상 연구 기관, 제약 회사) 및 지역(유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 임상시험용 포장 시장 동향 및 인사이트

임상시험 건수 증가와 연구개발(R&D)의 활성화

2023년부터 2025년에 걸쳐, 기업들이 파이프라인을 보강하고 바이오시밀러의 경쟁 압력에 대응하며 새로운 치료법에 대한 첫 인체 임상시험에 자금을 지원함에 따라, 후원사의 연구개발 예산은 높은 수준을 유지했습니다. 각 시험 단계에는 고유한 라벨링, 맹검화, 설명 책임 및 출하 절차가 필요하기 때문에 이러한 시험 활동 증가는 임상시험용 포장 시장에 직접적인 영향을 미칩니다. 시험의 수정은 수요를 더욱 증가시킬 것입니다. 왜냐하면 시험 도중에 프로토콜이 변경되면, 이미 제조된 재고에 대한 라벨 재부착이나 재포장이 필요해질 수 있기 때문입니다. 클리니젠사에 따르면, 이 회사의 주문형 포장 모델에 따라 미국 시설에서는 48시간 이내, EU 시설에서는 72시간 이내에 발송된다고 합니다. 이는 속도가 더 이상 틈새 시장을 겨냥한 프리미엄 서비스가 아니라, 표준적인 서비스로 기대받게 되었음을 보여줍니다. 또한, 영국에서는 2025년 ‘인체 첫 임상시험(First-in-Human)’ 신청 건수가 전년 대비 5% 증가했으며, 이는 보다 광범위한 조사 기반이 포장 워크플로우에 점차 통합되고 있음을 시사합니다.

증가하는 바이오의약품 및 주사제 개발

현재 제1상부터 제3상 임상시험의 절반 이상이 비경구 제제에 초점을 맞추고 있으며, 바이오의약품, 바이오시밀러 및 복잡한 항체 프로그램이 개발 파이프라인에서 차지하는 비중이 커짐에 따라 그 비율은 증가하는 추세입니다. 이러한 변화는 임상시험용 포장 시장에 호재가 되고 있습니다. 왜냐하면 주사제는 많은 경구용 약물에 비해 추출물·용출물, 습기 차단 및 투여 형태에 대한 관리를 더욱 엄격하게 수행해야 하기 때문입니다. VuRoyal사는 고pH 바이오의약품용으로 사이클로올레핀 폴리머 재질의 주사기 채택이 증가하고 있다는 점을 강조했습니다. 이러한 시스템은 유리의 박리나 실리콘 오일과의 상호작용 문제를 방지하는 데 도움이 되기 때문입니다. SCHOTT Pharma는 주사용 바이오의약품에 사용되는 프리필드 유리 주사기에 대한 수요에 힘입어, 2026년 상반기 약물 전달 시스템 부문의 매출이 2억 180만 유로(2억 2,800만 달러)에 달했다고 보고했습니다. 또한, 위약과 실제 약물은 맹검화된 바이오의약품 임상시험에서 외관을 동일하게 보이게 하기 위해 대부분의 경우 독자적인 마스킹이나 2차 포장이 필요하기 때문에 비교 대상의 관리가 더욱 복잡해지고 있습니다.

소량 맞춤 포장에 따른 높은 비용

소량 포장 프로젝트의 경우, 생산량에 비례하지 않는 고정된 품질 관리 및 출하 승인 비용이 발생하기 때문에 초기 단계의 후원사 입장에서는 단위당 경제성이 떨어집니다. Contract Pharma는 2025년 4월, 대규모 상업 생산을 전제로 한 규제가 소량 생산, 특히 모듈식 클린룸, 로봇 충전 또는 일회용 시스템을 보유하지 않은 기업들에게 불균형적인 부담이 되고 있다고 지적했습니다. 이 문제는 첨단 의료 분야에서 더욱 심각해질 것입니다. 왜냐하면 대상 환자가 수십 명에 불과한 경우라도, 유효성 검증, 안정성 포장 및 자격을 갖춘 담당자의 출하 승인이 캠페인 총 비용에서 큰 비중을 차지할 가능성이 있기 때문입니다. 이러한 압박은 시험 시작을 지연시킬 뿐만 아니라, 일부 후원사가 지원 범위를 축소하는 원인이 되어, 결과적으로 향후 프로토콜 위반의 위험을 높이는 결과로 이어집니다. 따라서 임상시험용 포장 시장은 계속 성장하고 있지만, 효율적인 소량 생산 시스템을 갖추지 못한 공급업체의 경우, 표면적인 수요 수치가 시사하는 것보다 더 어려운 이익률 환경에 직면하게 될 것입니다.

부문별 분석

2025년 기준으로, 주사기는 임상시험용 포장 시장의 26.34%를 차지했으며, 이는 비경구용 생물학적 제제의 강력한 입지와, 의료기관 및 가정에서 모두 투여 오류를 줄여주는 프리필드 제제의 보급을 반영한 것입니다. 임상시험용 포장 시장은 투여 준비 완료 상태의 유지, 투여량 관리, 그리고 맹검 시험에서 책임 소재를 명확히 할 수 있도록 하기 위해 여전히 주사기 제제에 크게 의존하고 있습니다. 바이알 및 앰플은 특히 동결건조 바이오의약품, 백신 및 종양학 연구 분야에서 투여 현장에서의 재구성 방식이 여전히 표준으로 자리 잡고 있어, 두 번째로 큰 제품군을 형성했습니다. 또한, 블리스터 팩은 일회 투여 구조 덕분에 의료진 팀의 변조 방지 대책 및 환자 수준의 추적 관리를 지원하기 때문에 경구용 항암제 및 중추신경계 프로그램에서 여전히 중요한 역할을 하고 있습니다.

키트 및 팩 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 9.73%로 가장 빠른 성장세를 보일 것으로 예상되며, 이는 임상시험용 포장 시장이 개별 1차 용기에서 시험 실시 준비가 완료된 완전한 조립품으로 전환되고 있음을 보여줍니다. 이러한 형태는 의약품, 투여 기기, 사용 설명서 및 반송용 자재를 하나의 환자용 세트로 통합한 것으로, 택배 배송 경로를 위한 검증된 운송 성능이 요구되는 경우가 점점 더 많아지고 있습니다. VuRoyal사는 분산형 공급 프로그램에서 이러한 운송 물품에 대한 ISTA 7D 또는 이에 상응하는 시험의 필요성이 점점 더 커지고 있다고 밝혔으며, 이로 인해 2차 포장 설계의 기술적 가치가 높아지고 있습니다. 써모피셔 사이언티피크(Thermo Fisher Scientific)는 펜실베이니아주 센터밸리에 위치한 자사의 임상시험 혁신 연구소에서 분산형 키트 형식을 위한 실시간 온도 및 GPS 모니터링 기능을 갖춘 스마트 패키지를 개발 중이라고 밝히며, 공급업체들이 포장 워크플로우에 데이터 수집 기능을 통합하고 있는 실태를 보여주었습니다.

지역별 분석

2025년 북미는 임상시험용 포장 시장 점유율의 38.56%를 차지했습니다. 이는 다수의 후원 기업, 확립된 cGMP 준수 임상용 포장 역량, 그리고 견고한 콜드체인 인프라에 힘입은 결과입니다. 해당 지역의 임상시험용 포장 시장은 환자에게 직접 제공되는 임상시험용 의약품 조제에 대한 미국의 규제 대응 방안이 명확해진 점도 호재로 작용하여, 택배 방식이 적용 가능한 이용 사례가 확대되었습니다. 알맥 그룹은 2025년 9월, 펜실베이니아주에서의 확장 계획 1단계를 완료하고, 3만 6,100제곱피트의 창고 공간과 -60°C에서 -80°C까지의 초저온 보관이 가능한 냉동고 76대를 증설했습니다. PCI 파마 서비스 역시 미국 내 무균 충전·최종 가공 및 의약품 및 의료기기 제조 역량에 대해 총액 10억 달러가 넘는 투자를 약속했습니다. 여기에는 2026년 5월에 가동을 시작한 뉴햄프셔주 베드포드의 GMP 기준에 부합하는 바이알 및 동결건조 라인이 포함됩니다.

2025년, 유럽은 임상시험용 포장 시장에서 2위의 점유율을 차지했으며, 독일, 프랑스, 영국이 포장, 라벨링 및 블라인드화 활동의 주요 거점이 되었습니다. 영국에서는 제1상 임상시험을 위한 14일간의 심사 절차를 포함하는 개정 임상시험 규정이 2026년 4월 28일에 발효된 반면, 유럽의약품청(EMA)은 2025년 7월 23일부터 ICH E6(R3)을 시행했습니다. EU GMP 부속서 13 및 EU 임상시험 규정은 후원사가 맹검 처리된 제품에 대한 오표기 위험을 제한해야 하므로, 전문적인 라벨링 및 맹검 처리 서비스에 대한 수요를 지속적으로 뒷받침하고 있습니다. SCHOTT Pharma는 2026년 1월, 빛에 민감한 동결건조 항체-약물 복합체(ADC)용으로 ‘EVERIC lyo’ 및 호박색 바이알을 출시했습니다. 이 제품은 EU, 미국 및 일본의 광투과율 요건을 충족하도록 설계되었습니다.

아시아태평양은 임상시험용 포장 시장에서 2031년까지 연평균 성장률(CAGR) 10.54%로 확대될 것으로 예상되며, 예측 기간 동안 가장 빠르게 성장하는 지역 클러스터가 될 전망입니다. 이러한 성장은 중국의 국내 CDMO 기반 확대, 인도의 CRO 사업 확장, 한국의 생물학적 제제 및 항체-약물 복합체(ADC) 제조에서의 역할, 그리고 일본의 자가주사용 및 재택 간호용 포장에 대한 수요에 힘입어 이루어지고 있습니다. TPC 마케팅 조사에 따르면, Chem-Station을 통해 일본 의약품 용기 및 포장 자재 시장이 2024년에 2,239억 엔(15억 달러)에 달했고, 2025년에는 2,276억 5,000만 엔(15억 3,000만 달러)에 이르렀으며, 프리필드 주사기와 오토인젝터가 가장 큰 성장세를 보이고 있다고 보고했습니다. 중국은 전 세계 세포 및 유전자 치료 임상시험의 30% 이상을 차지할 것으로 예상되며, 이에 따라 현지에서의 초저온 포장 및 검증 완료된 콜드체인 키트 조립에 대한 수요가 증가하고 있습니다. 삼성바이오로직스는 ‘Bio Japan 2025’를 통해 일본 제약 기업들과의 파트너십을 강화하고 있으며, 이는 아시아태평양의 제조 거점과 전 세계 임상 공급망 간의 연계가 더욱 공고해지고 있음을 시사합니다. 남미, 중동 및 아프리카는 여전히 규모가 가장 작은 지역 시장이며, 브라질과 남아프리카공화국이 주요 시험 실시 지역으로 꼽히지만, 수입 허가와 관련된 마찰과 콜드체인 인프라의 취약성으로 인해 더 광범위한 확장이 제한되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the clinical trial packaging market size is projected to be USD 4.08 billion in 2025, USD 4.44 billion in 2026, and reach USD 6.83 billion by 2031, growing at a CAGR of 9.01% from 2026 to 2031.

This report is Segmented by Product Type (Vials and Ampoules, Syringes, Blister Packs, Bottles, Bags and Pouches, Tubes, Sachets, and More), Material Type (Plastic, Paper and Corrugated Fiber, Glass, and Metal), End User (Research Laboratories, Clinical Research Organization, and Drug Manufacturing Companies), and Geography (Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Clinical Trial Packaging Market Trends and Insights

Growing Clinical Trial Volumes and R&D Intensity

Sponsor R&D budgets stayed elevated across 2023 to 2025 as companies refilled pipelines, responded to biosimilar pressure, and funded first-in-human work in newer modalities. That rise in trial activity directly affects the clinical trial packaging market, as each study phase requires its own labeling, blinding, accountability, and release process. Trial amendments add another layer of demand, since mid-study protocol changes can force relabeling or repackaging of inventory that has already been produced. Clinigen reported that its on-demand packaging model ships within 48 hours from U.S. facilities and within 72 hours from EU facilities, which shows how speed has become a standard service expectation rather than a niche premium offering. The UK also saw a 5% rise in first-in-human trial applications in 2025 compared with the prior year, suggesting a broader study base entering packaging workflows.

Rising Biologics and Injectable Drug Development

More than half of Phase I to Phase III clinical trials now focus on parenteral formulations, and that mix has been moving upward as biologics, biosimilars, and complex antibody programs take a larger share of development pipelines. The clinical trial packaging market benefits from that shift because injectable therapies need more control over extractables, leachables, moisture protection, and dose presentation than many oral drugs. VuRoyal highlighted the growing use of cyclic olefin polymer syringe formats for high-pH biologics, as these systems help avoid glass delamination and silicone-oil interaction issues. SCHOTT Pharma reported H1 2026 Drug Delivery Systems revenue of EUR 201.8 million (USD 228 million), supported by demand for prefillable glass syringes used in injectable biologics. Comparator management adds further complexity because placebo and active products often require custom masking and secondary packaging to appear identical during blinded biologic studies.

High Cost of Small-Batch Customized Packaging

Small-batch packaging campaigns incur fixed quality and release costs that do not scale with volume, making unit economics difficult for early-stage sponsors. Contract Pharma noted in April 2025 that regulations built around large commercial output create disproportionate burdens for small-batch operations, especially for companies that lack modular cleanrooms, robotic filling, or single-use systems. The challenge becomes sharper in advanced therapies because validation, stability packaging, and qualified person release can consume a large share of total campaign cost, even when only dozens of patients are being served. This pressure can delay study activation and also lead some sponsors to narrow the packaging scope, increasing the risk of protocol deviation later. The clinical trial packaging market, therefore, continues to grow, but providers without efficient small-batch systems face a tougher margin environment than headline demand numbers suggest.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Decentralized and Direct-To-Patient Trial Models

- Increasing Outsourcing to Integrated Clinical Supply Partners

- Fragmented Country-Level Labeling and Import Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Syringes held 26.34% of the clinical trial packaging market share in 2025, reflecting the strong presence of parenteral biologics and the wider use of prefilled formats that reduce dosing errors in both site-based and home-use settings. The clinical trials packaging market continues to rely heavily on syringe formats because they support ready-to-administer dosing, controlled presentation, and easier accountability in blinded studies. Vials and ampoules formed the second-largest product group, especially in lyophilized biologics, vaccines, and oncology studies, where reconstitution at the point of care remains standard. Blister packs also remained relevant for oral oncology and central nervous system programs because their unit-dose structure helps site teams manage tamper evidence and patient-level accountability.

Kits and packs are projected to record the fastest growth at a 9.73% CAGR from 2026 to 2031, indicating that the clinical trials packaging market is moving beyond individual primary containers toward complete study-ready assemblies. These formats combine the drug product, administration device, instructions for use, and return materials into a single patient-facing unit and often require validated transit performance for home delivery routes. VuRoyal stated that decentralized supply programs increasingly require ISTA 7D or equivalent testing for such shipments, which raises the technical value of secondary packaging design. Thermo Fisher Scientific said its clinical trials innovation lab in Center Valley, Pennsylvania has been developing smart packaging with real-time temperature and GPS monitoring for decentralized kit formats, which shows how providers are adding data capture into packaging workflows.

Geography Analysis

North America held 38.56% of the clinical trial packaging market share in 2025, supported by a dense sponsor base, established cGMP clinical packaging capacity, and strong cold-chain infrastructure. The clinical trials packaging market in the region also benefited from clearer U.S. regulatory treatment of direct-to-patient investigational product dispensing, which widened the addressable use cases for home-delivery formats. Almac Group completed phase one of its Pennsylvania expansion in September 2025, adding 36,100 sq. ft. of warehouse space and ultra-low temperature storage for 76 freezers at -60°C to -80°C. PCI Pharma Services also announced investment commitments totaling above USD 1 billion in U.S. sterile fill-finish and drug-device capabilities, including a GMP-ready vial and lyophilization line in Bedford, New Hampshire, commissioned in May 2026.

Europe held the second-largest share of the clinical trials packaging market in 2025, with Germany, France, and the UK as the main centers for packaging, labeling, and blinding activities. The UK introduced reformed clinical trial regulations effective April 28, 2026, including a 14-day assessment route for Phase I studies, while the European Medicines Agency implemented ICH E6(R3) from July 23, 2025. EU GMP Annex 13 and the EU Clinical Trial Regulation continue to support demand for specialized labeling and blinding services because sponsors must limit mislabeling risk in blinded products. SCHOTT Pharma launched EVERIC lyo and amber vials in January 2026 for light-sensitive lyophilized antibody-drug conjugates, and the product was designed to meet light transmission requirements in the EU, the U.S., and Japan.

Asia-Pacific is projected to expand at a 10.54% CAGR through 2031 in the clinical trials packaging market, making it the fastest-growing regional cluster in the forecast period. Growth is being driven by China's larger domestic CDMO base, India's expanding CRO footprint, South Korea's role in biologic and antibody-drug conjugate manufacturing, and Japan's demand for self-injection and home-care packaging. TPC Marketing Research reported through Chem-Station that Japan's pharmaceutical container and packaging material market reached JPY 223.9 billion (USD 1.5 billion) in 2024 and was projected to reach JPY 227.65 billion (USD 1.53 billion) in 2025, with prefilled syringes and autoinjectors posting the strongest gains. China is projected to account for more than 30% of global cell and gene therapy clinical trials, which is lifting demand for local cryogenic packaging and validated cold-chain kit assembly. Samsung Biologics used Bio Japan 2025 to deepen partnerships with Japanese pharmaceutical companies, which points to tighter links between Asia-Pacific manufacturing and global clinical supply chains. South America and the Middle East and Africa remained the smallest regional pool, with Brazil and South Africa acting as the main trial locations while import-license friction and weaker cold-chain infrastructure limited broader scale.

- Almac Group Limited

- Sharp Services, LLC

- Gerresheimer AG

- Amcor plc

- Thermo Fisher Scientific Inc.

- Clinigen Limited

- PCI Pharma Services

- Bilcare Limited

- Piramal Pharma Limited

- Myonex, Inc.

- BAP Pharma Ltd.

- Corden Pharma International GmbH

- West Pharmaceutical Services, Inc.

- SCHOTT Pharma AG & Co. KGaA

- Nipro Corporation

- Stevanato Group S.p.A.

- NextPharma Technologies Holding Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Clinical Trial Volumes and R&D Intensity

- 4.2.2 Rising Biologics and Injectable Drug Development

- 4.2.3 Expansion of Decentralized and Direct-to-Patient Trial Models

- 4.2.4 Increasing Outsourcing to Integrated Clinical Supply Partners

- 4.2.5 ICH E6(R3) Traceability and Blinding Requirements

- 4.2.6 Acceleration of Cell and Gene Therapy Trials

- 4.3 Market Restraints

- 4.3.1 High Cost of Small-Batch Customized Packaging

- 4.3.2 Fragmented Country-Level Labeling and Import Rules

- 4.3.3 Dangerous-Goods and Reverse-Logistics Constraints

- 4.3.4 EU Transport-Pack Compliance and Packaging Data Burden

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Vials and Ampoules

- 5.1.2 Syringes

- 5.1.3 Blister Packs

- 5.1.4 Bottles

- 5.1.5 Bags and Pouches

- 5.1.6 Tubes

- 5.1.7 Sachets

- 5.1.8 Other Product Types

- 5.2 By Material Type

- 5.2.1 Plastic

- 5.2.2 Glass

- 5.2.3 Metal

- 5.2.4 Paper and Corrugated Fiber

- 5.3 By End User

- 5.3.1 Research Laboratories

- 5.3.2 Clinical Research Organizations

- 5.3.3 Drug Manufacturing Companies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Almac Group Limited

- 6.4.2 Sharp Services, LLC

- 6.4.3 Gerresheimer AG

- 6.4.4 Amcor plc

- 6.4.5 Thermo Fisher Scientific Inc.

- 6.4.6 Clinigen Limited

- 6.4.7 PCI Pharma Services

- 6.4.8 Bilcare Limited

- 6.4.9 Piramal Pharma Limited

- 6.4.10 Myonex, Inc.

- 6.4.11 BAP Pharma Ltd.

- 6.4.12 Corden Pharma International GmbH

- 6.4.13 West Pharmaceutical Services, Inc.

- 6.4.14 SCHOTT Pharma AG & Co. KGaA

- 6.4.15 Nipro Corporation

- 6.4.16 Stevanato Group S.p.A.

- 6.4.17 NextPharma Technologies Holding Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment