|

시장보고서

상품코드

2064506

미국의 병원 및 헬스케어용 여과 장비 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)U.S. Hospital & Healthcare Spending For Filtration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

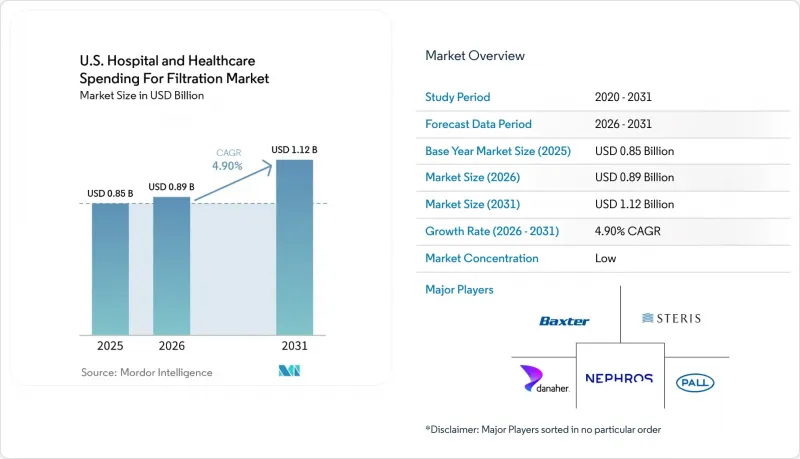

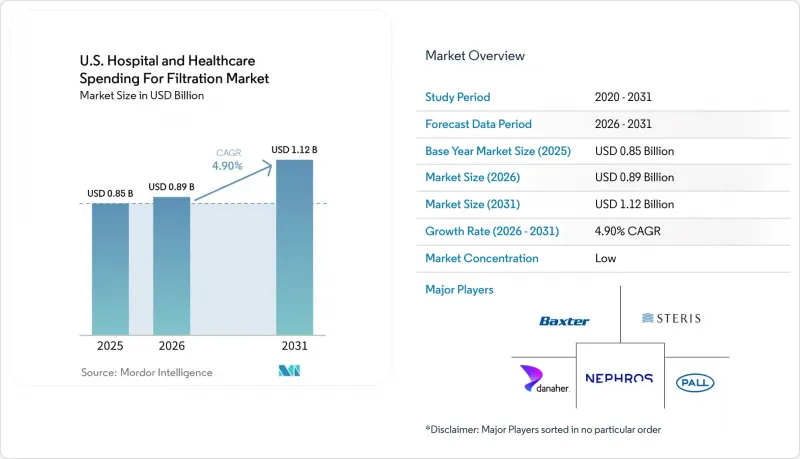

Mordor Intelligence에 의하면, 미국의 병원 및 헬스케어용 여과 장비 시장 규모는 2025년에 8억 5,000만 달러로 평가되었고, 2026년 8억 9,000만 달러로 추정되고, 2031년까지 11억 2,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.90%를 나타낼 전망입니다.

본 보고서는 제품별(공기 여과, 액체 여과 등), 여과 공정별(HEPA, ULPA, 활성탄·기상 여과 등), 최종 용도별(병원 등), 용도별(환자 관리용 공기질 등), 지역별(미국 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 병원 및 헬스케어용 여과 장비 시장 동향과 인사이트

CDC·ASHRAE의 기류 기준이 중환자실용 여과 장비 수요를 재편하고 있습니다.

ANSI/ASHRAE/ASHE 표준 170의 2025년판에서는 의료시설에 대한 환기 요건이 개정되었으며, 행동 의학 및 영상 진단 구역 등 현대 의료 패턴에 부합하는 공간 유형이 추가되었습니다. 이로 인해 기존 병원들은 기존 공조 시스템이 규정 준수 기준을 충족하는지 평가해야 할 필요가 생겨, 미국의 병원용 여과기 시장에 영향을 미치고 있습니다. 신축과 달리, 이러한 프로젝트에서는 대부분의 경우 기존의 덕트나 기계 설비를 그대로 활용하게 됩니다. CDC가 권장하는 휴대용 산업용 HEPA 장치는 고정식 HVAC 시스템만으로는 충분하지 않은 구역에서 오염 물질 제거 효과를 높여줍니다. 이로 인해, 특히 수술실이나 격리 구역과 같은 중요한 공간에서 설비 교체 주기와 보조적인 여과를 통해 수요가 발생하고 있습니다.

CMS와 조인트 커미션의 철저한 수질 관리가 액체 여과에 대한 지속적인 투자를 촉진

CMS는 메디케어 및 메디케이드 인증 병원, 크리티컬 액세스 병원, 장기 요양 시설에 대해 레지오넬라균 등의 병원체로 인한 위험을 줄이기 위한 물 관리 방침을 시행할 것을 의무화하고 있습니다. 이러한 방침에 따라 지속적인 위험 평가, 관리 조치 및 모니터링이 요구되며, 물의 안전은 지속적인 운영상의 최우선 과제로 자리 잡고 있습니다. 조인트 커미션은 인증 과정에서 감염 관리와 환경 관리를 중시함으로써 이러한 노력을 더욱 강화하고 있습니다. 이로 인해 사용 현장용 필터, 모니터링 도구, 교체용 매체에 대한 수요가 꾸준히 발생하고 있어, 건설 예산이 부족한 상황에서도 액체 여과는 여전히 견조한 성장세를 보이고 있습니다.

병원의 설비 투자 억제로 인해 여과 장비 교체 주기가 연장됨

규제 준수 압박이 커지고 있음에도 불구하고, 자금 조달의 불균형은 미국 병원용 여과 시장의 일부 부문에 있어 여전히 과제로 남아 있습니다. 2025년, HFMA는 10억 달러를 초과하는 병원 프로젝트가 15건 있다고 보고했으며, 이는 주요 의료 시스템의 막대한 투자를 반영하고 있습니다. 그러나 소규모 시설들은 자금 부족에 직면해 있으며, 2024년 ASHE 조사에 따르면 79%가 미뤄졌던 유지보수 자금의 절반 이하만 확보한 상태였고, 43%는 고작 10%만 확보한 것으로 나타났습니다. 예산 제약으로 인해 여과 시스템의 교체가 지연되고 교체 주기가 길어지면서, 프로젝트 진행이 더뎌지고 있습니다. 각 벤더사는 현재 이러한 과제를 해결하기 위해 수명 주기 비용 절감, 에너지 효율 향상, 그리고 업무에 미치는 영향 최소화에 주력하고 있습니다.

부문별 분석

2025년, 공기 여과는 53.14%의 점유율을 차지했으며, 입원 환자 관리, 수술실, 고위험 구역에 이르는 병원의 환기 시스템에서 중요한 역할을 수행함에 따라 1위 자리를 유지했습니다. 병원은 엄격한 공기 처리 기준을 충족해야 하며, 2025년 표준 170의 개정에 따라 공간 수준에 대한 요건이 확대되었습니다. 이에 이어 액체 여과가 이어졌으며, 음용수의 안전성, 투석수 처리 및 사용 현장의 관리가 주요 동력이 되었습니다.

의료기기용 여과 시장은 2031년까지 연평균 성장률(CAGR) 6.10%를 기록하며 성장할 것으로 예상되며, 미국 병원용 여과 시장에서 가장 빠르게 성장하는 부문이 될 전망입니다. 이러한 성장은 ST108 규격에 대한 대응 및 진료 거점 간 시술 건수의 이동에 따른 의료 기구 재처리량 증가와 관련이 있습니다. 현재, 복잡한 의료기기의 경우 재처리 시 수질 및 생물학적 부하에 대한 보다 엄격한 관리가 요구되고 있습니다. 외래 시술의 고도화에 따라 워크플로우 내 여과 공정이 증가하고 있으며, 멸균 처리 프로토콜을 준수하는 검증된 시스템에 대한 수요가 높아지고 있습니다.

HEPA 여과는 2025년에 44.45%의 시장 점유율을 차지한 것으로 평가되었으며, 고위험 및 응급 치료 구역의 병원 환기 시스템에서 확고히 자리 잡은 역할 덕분에 여전히 가장 큰 공정 범주로 남아 있습니다. ULPA 여과는 보다 엄격한 격리가 필요한 틈새 용도에 대응하는 한편, 활성탄 및 기상 시스템은 전문 분야에서 발생하는 악취, 화학 물질 및 공기질 제어에 대응했습니다.

역삼투(RO)는 2031년까지 연평균 성장률(CAGR) 7.40%를 기록할 전망이며, 미국 병원용 여과 시장에서 가장 빠르게 성장하는 공정 부문이 될 것으로 예측됩니다. 이러한 성장은 투석 치료의 확대, 수질 안전에 대한 집중, 그리고 신뢰성이 높은 멸균 처리용수 경로에 대한 수요에 힘입어 이루어지고 있습니다. 역삼투 기술이 주목을 받고 있는 한편, 이는 HEPA를 대체하는 것이 아니라 보완하는 역할을 하며, 물 관련 규정 준수 및 예산 배분에 대한 관심이 높아지고 있음을 반영하고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the u.S. hospital & healthcare spending for filtration market size was valued at USD 0.85 billion in 2025 and is estimated to grow from USD 0.89 billion in 2026 to reach USD 1.12 billion by 2031, at a CAGR of 4.90% during the forecast period (2026-2031).

This report is Segmented by Product (Air Filtration, Liquid Filtration, and More), Filtration Process (HEPA, ULPA, Activated Carbon, and Gas-Phase, and More), End Use (Hospitals, and More), Application Area (Patient-Care Air Quality, and More), and Geography (United States and More). The Market Forecasts are Provided in Terms of Value (USD).

U.S. Hospital & Healthcare Spending For Filtration Market Trends and Insights

CDC and ASHRAE Airflow Compliance Reshape Critical-Care Filtration Demand

The 2025 edition of ANSI/ASHRAE/ASHE Standard 170 revised ventilation requirements for healthcare facilities, adding space types aligned with modern care patterns, such as behavioral health and imaging areas. This impacts the United States hospital filtration market as older hospitals must assess if existing air-handling systems meet compliance standards. Unlike new constructions, these projects often adapt legacy ductwork and mechanical systems. Portable industrial-grade HEPA units, recommended by the CDC, enhance contaminant removal in areas where fixed HVAC systems are insufficient. This creates demand driven by both replacement cycles and supplemental filtration, especially in critical spaces like operating rooms and isolation areas.

CMS and Joint Commission Water-Management Enforcement Drives Sustained Liquid Filtration Investment

CMS mandates that Medicare and Medicaid-certified hospitals, critical access hospitals, and long-term care facilities implement water management policies to mitigate risks from pathogens like Legionella. These policies require ongoing risk assessments, control measures, and monitoring, making water safety a continuous operational priority. The Joint Commission reinforces this focus by emphasizing infection control and environmental care in accreditation processes. This drives consistent demand for point-of-use filters, monitoring tools, and replacement media, ensuring liquid filtration remains a resilient segment even during tighter construction budgets.

Hospital Capital Rationing Extends Filtration Replacement Cycles

Uneven capital access continues to challenge segments of the United States hospital filtration market, despite rising compliance pressures. In 2025, HFMA reported 15 hospital projects exceeding USD 1 billion, reflecting significant investments by major systems. However, smaller facilities face funding shortfalls, with a 2024 ASHE survey showing 79% received less than half of their deferred maintenance funding, and 43% secured only 10%. Budget constraints delay filtration upgrades and extend replacement cycles, slowing project conversions. Vendors now focus on lifecycle savings, energy efficiency, and reduced disruptions to address these challenges.

Other drivers and restraints analyzed in the detailed report include:

- Outpatient Migration Multiplies Filtration Nodes Across ASCs and Clinics

- AAMI ST108 Triggers Capital Cycles in Sterile-Processing Water Infrastructure

- Maintenance Complexity Across Multi-Modal Filtration Strains Operational Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, air filtration held a 53.14% share, maintaining its lead due to its critical role in hospital ventilation systems across inpatient care, surgeries, and high-risk areas. Hospitals are required to meet stringent air handling standards, with the 2025 Standard 170 update broadening space-level requirements. Liquid filtration followed, driven by potable water safety, dialysis water treatment, and point-of-use controls.

Medical device filtration is projected to grow at a 6.10% CAGR through 2031, making it the fastest-growing segment in the United States hospital filtration market. Growth is linked to ST108 upgrades and increased reprocessing of instruments as procedural volumes shift across care sites. Complex devices now require stricter control over water quality and bioburden during reprocessing. Rising outpatient procedure acuity has increased filtration stages in workflows, pushing demand for validated systems aligned with sterile-processing protocols.

HEPA filtration accounted for 44.45% share in 2025, remaining the largest process category due to its established role in hospital ventilation for high-risk and critical treatment areas. ULPA filtration catered to niche applications requiring tighter containment, while activated carbon and gas-phase systems addressed odor, chemical, and air quality control in specialized areas.

Reverse osmosis is expected to grow at a 7.40% CAGR through 2031, becoming the fastest-growing process segment in the United States hospital filtration market. This growth is driven by dialysis expansion, water safety focus, and the need for reliable sterile-processing water pathways. While reverse osmosis gains attention, it complements rather than replaces HEPA, reflecting increased focus on water-side compliance and budget allocation.

List of Companies Covered in this Report:

- AAF International

- Absolute Water Technologies

- Baxter

- Camfil USA

- Consolidated Sterilizer Systems

- Danaher

- Envirogen Group

- Evoqua Water Technologies

- Freudenberg Filtration Technologies

- ITW Medical

- MANN+HUMMEL

- Mentor Water Technologies

- Nephros, Inc.

- NuStream Filtration

- Pall Medical

- Parker Hannifin

- Pentair

- STERIS

- Veolia Water Technologies

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CDC and ASHRAE Airflow Compliance in Critical-Care Spaces

- 4.2.2 CMS and Joint Commission Water-Management Enforcement

- 4.2.3 Outpatient Migration Expands Filtration Points Across ASCs and Clinics

- 4.2.4 AAMI ST108 Upgrades Sterile-Processing Water Loops

- 4.2.5 Low-Pressure-Drop Retrofit Filters Gain Priority in Margin-Stressed Hospitals

- 4.3 Market Restraints

- 4.3.1 Hospital Capital Rationing and Deferred Facilities Projects

- 4.3.2 Maintenance Complexity Across Air, Water, Steam, and Device Filters

- 4.3.3 Specialized Media and Membrane Sourcing Volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Air Filtration

- 5.1.2 Liquid Filtration

- 5.1.3 Medical Device Filtration

- 5.1.4 Environmental and Utility Filtration

- 5.2 By Filtration Process

- 5.2.1 HEPA Filtration

- 5.2.2 ULPA Filtration

- 5.2.3 Activated Carbon and Gas-Phase Filtration

- 5.2.4 Reverse Osmosis

- 5.2.5 Ultrafiltration

- 5.2.6 Microfiltration

- 5.2.7 Endotoxin and Final-Barrier Filtration

- 5.3 By End Use

- 5.3.1 Hospitals

- 5.3.2 Outpatient and Ambulatory Care

- 5.3.3 Post-Acute and Long-Term Care

- 5.3.4 Dialysis and Renal Care Sites

- 5.3.5 Diagnostic and Laboratory Sites

- 5.4 By Application Area

- 5.4.1 Patient-Care Air Quality

- 5.4.2 Sterile Processing and Reprocessing Water

- 5.4.3 Facility Water Safety

- 5.4.4 Clinical and Diagnostic Utilities

- 5.4.5 Respiratory and Infusion Protection

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AAF International

- 6.3.2 Absolute Water Technologies

- 6.3.3 Baxter International Inc.

- 6.3.4 Camfil USA

- 6.3.5 Consolidated Sterilizer Systems

- 6.3.6 Danaher Corporation

- 6.3.7 Envirogen Group

- 6.3.8 Evoqua Water Technologies

- 6.3.9 Freudenberg Filtration Technologies

- 6.3.10 ITW Medical

- 6.3.11 MANN+HUMMEL

- 6.3.12 Mentor Water Technologies

- 6.3.13 Nephros, Inc.

- 6.3.14 NuStream Filtration

- 6.3.15 Pall Medical

- 6.3.16 Parker-Hannifin Corporation

- 6.3.17 Pentair

- 6.3.18 STERIS plc

- 6.3.19 Veolia Water Technologies

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment