|

시장보고서

상품코드

2065535

미국의 화상 치료 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)United States Burn Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

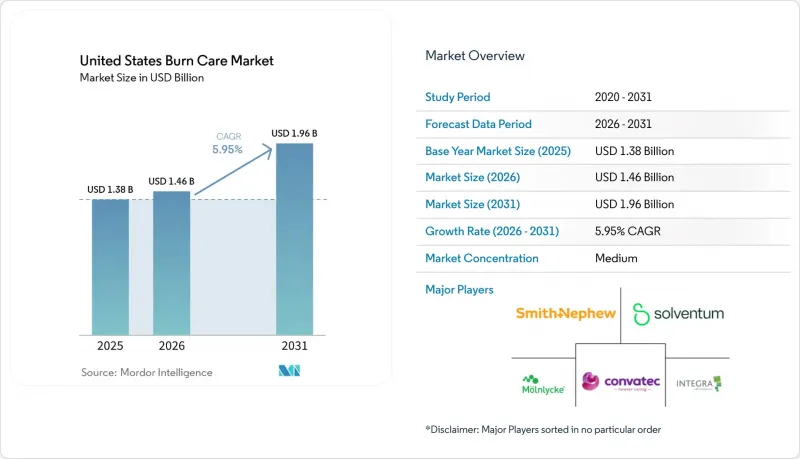

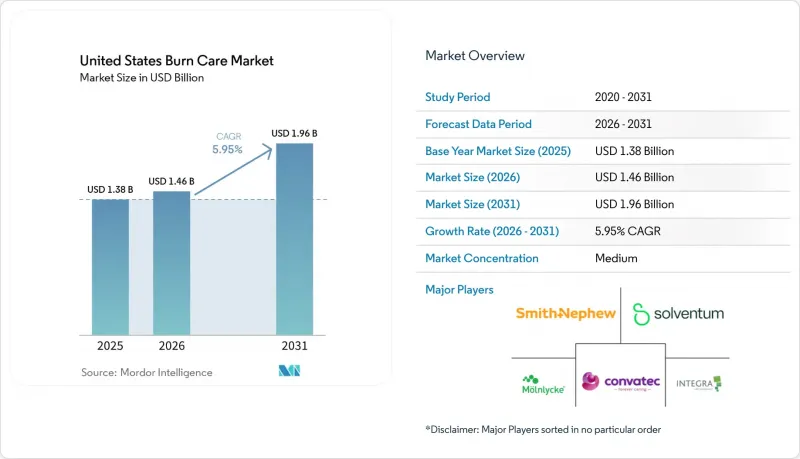

Mordor Intelligence에 의하면, 미국의 화상 치료 시장 규모는 2025년에 13억 8,000만 달러로 평가되었습니다. 2026년 14억 6,000만 달러에서 2031년까지 19억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 5.95%를 나타낼 전망입니다.

본 보고서는 제품 유형(고도 피복재(폼 피복재 등), 생물학적 제제·피부 대체재 등), 화상의 깊이(표재성, 부분층, 전층 화상), 치료 환경(병원, 전문 화상 센터·상처 클리닉 등), 화상 원인(화기 화상, 전기 화상 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 화상 치료 시장 동향 및 인사이트

미국 내 높은 화상 환자 수와 집중된 의뢰 환자 유입

미국의 화상 치료 시장은 대규모이며 안정적인 치료 인프라의 혜택을 지속적으로 누리고 있습니다. 이는 CDC(미국 질병통제예방센터)의 자료에 따르면 화재 및 화상과 관련된 부상자 수가 연간 약 39만 8,000건에 달하는 반면, 미국 화상 협회(American Burn Association)의 보고에 따르면 2만 9,165건이 입원을 필요로 했기 때문입니다. 연간 100건 이상의 화상 환자를 수용하는 94개 병원이 전체 화상 입원 환자의 81%를 차지하고 있기 때문에 수요가 전국에 고르게 분산되어 있는 것은 아닙니다. 이러한 집중 현상으로 인해, 광범위하지만 얕은 유통망보다는 처방약 목록에 등재되는 것이 더 중요시되는 신뢰할 수 있는 구매 거점이 형성되고 있습니다. 남대서양 지역만으로도 화상으로 인한 입원 환자의 26%를 차지하고 있어, 이 지역은 인프라 계획 및 공급업체 선정 시 우선순위 결정에 있어 더 큰 역할을 담당하고 있습니다. 따라서 미국의 화상 치료 시장에서 제품의 도입은 ABA 인증 센터나 환자 수가 많은 병원을 통한 소개 속도와 밀접한 관련이 있습니다. 이러한 환자 수가 많은 의료기관에 직접 접근할 수 있는 제조업체는 첨단 피복재, 이식편 및 보조 요법 분야에서 지속적인 사용을 확보하는 데 유리한 입장에 있습니다.

고도 피복재, 이식편 및 생물학적 제제의 도입

미국의 화상 치료 시장은 첨단 피복재와 생물학적 제제를 별개의 선택지로 취급하기보다는 이 둘을 결합한 치료 방식으로 전환되고 있습니다. 화상 외과 의사들은 전층 화상 및 심부 부분층 화상에 대해 단계적 치료 프로토콜을 더욱 빈번하게 채택하고 있으며, 이로 인해 진피 템플릿, 이식편 지지 제품 및 보조적인 상처 피복재에 대한 수요가 증가하고 있습니다. 인테그라 라이프사이언시스(Integra LifeSciences)는 2026년 4월에 개최된 3개의 학회에서 985건의 사례 및 23명의 환자를 대상으로 한 화상 사례 시리즈에서 도출된 실세계 데이터(REW)를 발표했습니다. 이에 따르면, 진피 재생 템플릿이 의료기관의 표준 치료 알고리즘에 점차 도입되고 있는 것으로 나타났습니다. 한편, 의약품 도입 담당 팀은 많은 부분층 화상의 경우, 고비용의 생물학적 제제로 전환하기 전에 여전히 ‘비수술 우선’ 접근 방식을 선호하고 있기 때문에 피복재 수요는 견조한 추세를 보이고 있습니다. 규제 당국의 움직임도 이러한 추세를 뒷받침하고 있습니다. FDA는 AVITA Medical사의 콜라겐 기반 진피 매트릭스 ‘Cohealyx’와 생합성 상처 매트릭스 ‘PermeaDerm’을 승인한 데 이어, 2025년 4월에는 Abeona Therapeutics사의 ‘ZEVASKYN’을 승인했습니다. 이는 증거 수준이 높은 제품이라면 여전히 시장에 출시할 수 있음을 시사합니다. 이러한 임상 현장에서의 폭넓은 수용과 더 높은 근거 기준이 결합됨에 따라, 미국의 화상 치료 시장에서 첨단 피복재와 생물학적 제제 모두 여전히 견조한 성장세를 유지하고 있습니다.

바이오의약품의 높은 비용과 NPWT를 많이 활용하는 치료 경로

미국의 화상 치료 시장에서는 치료 경로가 바이오의약품이나 NPWT에 크게 의존하는 경우, 도입에 명백한 한계가 존재합니다. 미국의 화상 협회(American Burn Association)의 보고에 따르면, 화상 환자의 29.1%가 메디케이드 수혜자이며, 10.2%는 무보험자이거나 본인 부담금을 지불해야 하기 때문에 많은 의료 기관이 고액의 첨단 치료 비용을 감당할 수 있는 능력이 제한되어 있습니다. NPWT를 이용한 이식편 준비는 입원 치료 시 드레싱 교체 1회당 1,000-3,000달러의 추가 비용이 발생할 가능성이 있어, 확실한 치료 성과 데이터가 없는 지역 병원에서는 비용 대비 효과의 정당성을 입증하기 어렵습니다. 또한, 화상 센터 환자의 15.9%가 메디케어(Medicare) 가입자이며, 많은 피부 대체재에 대한 보험 급여 조건이 엄격해짐에 따라 지불 주체의 구성은 더욱 제한적입니다. 이에 따라 각 제조업체들은 경제적 가치에 대한 논의를 뒷받침하기 위해, 인테그라(Integra)사의 ‘PriMatrix’에 관한 논문이나 케레시스(Kerecis)사의 입원 기간 단축 관련 데이터 등 실세계 데이터(REW)를 더욱 적극적으로 활용하고 있습니다. 이러한 비용 측면의 압박으로 인해, 신제품이 미국 전역의 화상 치료 시장 전체에 보급되는 속도가 둔화되고 있습니다.

부문별 분석

미국의 화상 치료 시장에서는 첨단 피복재가 주도적인 위치를 차지하고 있으며, 2025년에는 매출의 42.31%를 차지했습니다. 이러한 장점은 병원, 외래 진료, 재택 회복 프로그램에서 표재성, 부분층 및 특정 수술 후 상처에 폭넓게 사용되고 있음을 반영합니다. 항균성 은 코팅재 및 폼 코팅재는 폭넓은 환자층의 감염 관리 및 삼출액 관리에 대응할 수 있기 때문에 여전히 가장 널리 사용되는 형태입니다. 스미스 앤 네퓨(Smith & Nephew)가 2026년 3월에 출시한 ‘ALLEVYN COMPLETE CARE’는 경쟁 제품보다 뛰어난 삼출액 관리 성능을 내세우고 있으며, 이는 해당 부문에서 혁신이 여전히 프리미엄 가격 책정을 뒷받침하고 있음을 보여줍니다.

생물학적 제제 및 피부 대체재는 미국의 화상 치료 시장에서 가장 빠르게 성장하고 있는 제품 부문으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 8.38%를 나타낼 것으로 전망됩니다. 이러한 성장은 전층 화상 및 복잡한 심부 부분층 화상에 대한 임상적 적용 확대와 더불어, 현재 BLA(생물학적 제제 승인 신청) 절차를 거치는 제품을 우선시하는 규제상의 변화를 반영한 것입니다. Vericel사의 보고에 따르면, NexoBrid는 2026년 1분기에 화상 치료 분야에서 1,200만 달러의 매출을 기록했으며, 이는 전년 동기 대비 91% 증가한 수치입니다. 이 회사는 2026년 연간 실적 전망치를 4,400만-4,800만 달러로 상향 조정했습니다. 음압상처치료법은 이식편 준비 및 상처 관리에 있어 여전히 중요한 보조 수단으로 자리 잡고 있지만, 한편으로는 생물학적 제제에 대한 지출 증가를 감당할 수 없는 의료 기관에서는 기존의 피복재가 여전히 비용 면에서 우위를 점하고 있습니다. 따라서 미국의 화상 치료 시장은 첨단 피복재가 시장 규모를 유지하고, 생물학적 제제가 가장 빠른 매출 성장을 기록하는 등 양극화된 제품 구조를 보이고 있습니다.

2025년에는 부분층 화상이 63.24%를 차지했으며, 화상 깊이에 따른 분류에서는 미국의 화상 치료 시장에서 가장 큰 비중을 차지했습니다. 이 비율은 미국의 화상 협회(American Burn Association)가 보고한 임상 양상과 일치하는데, 수술이 필요하지만 장기적인 인공호흡이 필요하지 않은 심부 부분층 화상이 입원 환자의 32%를 차지한 반면, 수술과 인공호흡이 모두 필요한 가장 중증의 화상은 불과 4.4%에 그쳤습니다. 폼, 하이드로콜로이드, 알긴산염 및 기타 첨단 피복재는 치유를 촉진하는 동시에 불필요한 치료 범위를 최소화하기 위해, 이러한 상처 관리에서 여전히 핵심적인 역할을 수행하고 있습니다. 또한, NexoBrid와 같은 효소 데브리드먼트 제품도 생존 조직을 손상시키지 않으면서 딱지를 선택적으로 제거할 수 있기 때문에 심부 부분층 화상 치료에서 주목받고 있으며, 이러한 치료 접근법은 최근의 임상 지침에도 반영되어 있습니다.

전층 화상은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.52%로 확대될 것으로 예측되며, 미국의 화상 치료 시장에서 화상 깊이별 카테고리 중 가장 빠르게 성장할 분야가 될 전망입니다. 이러한 화상은 표재성 화상에 비해 치료가 복잡하고, 외과적 처치가 빈번하며, 1건당 수익도 크기 때문에 이 분야의 성장은 중요한 의미를 지닙니다. PolyNovo사의 ‘NovoSorb BTM’은 Valleywise Health 및 LAC+USC를 포함한 미국의 화상 치료 센터에서 다기관 공동 주요 임상시험이 현재 진행 중이며, 2026년 12월에 완료될 전망입니다. 이 시험 결과는 절제·이식 프로토콜에서 합성 매트릭스의 더 광범위한 사용을 촉진할 가능성이 있습니다. 표재성 화상은 여전히 전체 사례의 대부분을 차지하고 있지만, 치료 강도가 낮기 때문에 가치에 대한 기여도는 제한적입니다. 이러한 추세에 따라, 미국의 화상 치료 시장은 부분층 화상의 유병률에 힘입으면서도, 전층 화상 사례가 제품의 고도화와 프리미엄화를 주도하는 구조를 띠고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the united states burn care market size was valued at USD 1.38 billion in 2025 and is estimated to grow from USD 1.46 billion in 2026 to reach USD 1.96 billion by 2031, at a CAGR of 5.95% during the forecast period (2026-2031).

This report is Segmented by Product Type (Advanced Dressings [Foam Dressings, and More], Biologics and Skin Substitutes, and More), Burn Depth (Superficial, Partial-Thickness, Full-Thickness Burns), Care Setting (Hospitals, Specialised Burn Centres and Wound Clinics, and More), and Burn Etiology (Thermal, Electrical, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Burn Care Market Trends and Insights

High U.S. Burn Case Burden and Concentrated Referral Flows

The United States burn care market continues to benefit from a large and steady treatment base because the CDC-linked burn burden stands near 398,000 fire or burn-related injuries annually, while the American Burn Association reported that 29,165 cases required inpatient admission. Demand is not spread evenly across the country because 94 hospitals that each admit at least 100 burn encounters per year account for 81% of all inpatient burn admissions. This concentration creates dependable purchasing nodes where formulary access matters more than broad but shallow distribution coverage. The South Atlantic alone contributes 26% of inpatient burn admissions, which gives that region a larger role in infrastructure planning and supplier prioritization. In the United States burn care market, product adoption is therefore tied closely to referral velocity through ABA-verified centers and high-volume hospitals. Manufacturers with direct access to these high-throughput institutions are better placed to secure repeat use across advanced dressings, grafts, and support therapies.

Advanced Dressings, Grafts, and Biologics Adoption

The United States burn care market is shifting toward care pathways that combine advanced dressings with biologics rather than treating the two categories as separate choices. Burn surgeons are using staged treatment protocols more often for full-thickness and deep partial-thickness injuries, which raises demand for dermal templates, graft-support products, and adjunct wound coverage. Integra LifeSciences presented real-world evidence from 985 cases and a 23-patient burn series across three conferences in April 2026, which shows that dermal regeneration templates are moving into routine institutional algorithms. At the same time, dressing volumes remain firm because formulary teams still favor a dressing-first approach for many partial-thickness wounds before escalating to higher-cost biologic products. Regulatory activity is reinforcing this trend because the FDA cleared AVITA Medical's Cohealyx collagen-based dermal matrix and PermeaDerm biosynthetic wound matrix, while the FDA approved Abeona Therapeutics' ZEVASKYN in April 2025, which signals that high-evidence products can still move forward. This combination of broader clinical acceptance and a higher evidence threshold keeps both advanced dressings and biologics in positive growth territory within the United States burn care market.

High Cost of Biologics and NPWT-Intensive Care Pathways

The United States burn care market faces a clear adoption ceiling when treatment pathways depend heavily on biologics and NPWT. The American Burn Association reported that 29.1% of burn patients were covered by Medicaid and 10.2% were uninsured or self-paying, which limits the ability of many facilities to absorb expensive advanced therapies. NPWT-assisted graft preparation can add USD 1,000-3,000 per dressing change episode in inpatient care, which makes cost justification difficult in community hospitals without strong outcomes data. The payer mix becomes even more restrictive because 15.9% of burn-center patients are on Medicare and facilities now face tighter reimbursement for many skin substitutes. In response, manufacturers are leaning more heavily on real-world evidence such as Integra's PriMatrix publications and Kerecis data on reduced hospital length of stay to support economic value discussions. These cost pressures slow the pace at which newer products can scale across the full United States burn care market.

Other drivers and restraints analyzed in the detailed report include:

- Burn-Centre Expansion and Outpatient Pathway Optimization

- Teleburn Networks Closing Rural Access Gaps

- CMS 2026 Skin-Substitute Payment Reset

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Advanced dressings held the leading position in the United States burn care market, accounting for 42.31% of revenue in 2025. Their lead reflects broad use across superficial, partial-thickness, and selected post-surgical wounds in hospitals, ambulatory settings, and home recovery programs. Antimicrobial silver dressings and foam dressings remain the most widely used formats because they address infection control and exudate management across a large patient pool. Smith+Nephew's March 2026 launch of ALLEVYN COMPLETE CARE, which cited stronger exudate management performance than competing products, shows that innovation continues to support premium pricing in this tier.

Biologics and skin substitutes are the fastest-growing product segment in the United States burn care market, with an 8.38% CAGR expected from 2026 to 2031. This growth reflects stronger clinical use in full-thickness and complex deep partial-thickness injuries, along with a regulatory shift that now favors BLA-pathway products. Vericel reported that NexoBrid generated USD 12.0 million in burn care revenue in Q1 2026, up 91% year on year, and the company raised its full-year 2026 guidance to USD 44-48 million. Negative pressure wound therapy remains an important support layer in graft preparation and wound management, while traditional dressings still hold a cost-led role in facilities that cannot absorb higher biologic spending. The United States burn care market therefore shows a two-track product structure where advanced dressings preserve scale and biologics capture the fastest revenue growth.

Partial-thickness burns represented 63.24% in 2025, giving them the largest role in the United States burn care market by burn depth. This share follows the clinical pattern reported by the American Burn Association, where deep partial-thickness injuries requiring surgery but not prolonged ventilation made up 32% of hospital admissions, while the most extensive injuries requiring both surgery and ventilation accounted for only 4.4%. Foam, hydrocolloid, alginate, and other advanced dressings remain the backbone for these wounds because they support healing while limiting unnecessary escalation. Enzymatic debridement products such as NexoBrid are also gaining traction in deep partial-thickness care because they can remove eschar selectively without sacrificing viable tissue, a treatment approach reflected in recent clinical guidance.

Full-thickness burns are forecast to expand at a 7.52% CAGR from 2026 to 2031, making them the fastest-growing burn-depth category in the United States burn care market. Their growth matters because these injuries carry higher product complexity, heavier surgical use, and greater revenue per episode than superficial burns. PolyNovo's NovoSorb BTM remains in a multicenter pivotal study at U.S. burn centers including Valleywise Health and LAC+USC, with estimated completion in December 2026, which could support wider use of synthetic matrices in excision-and-graft protocols. Superficial burns still contribute large case volume, but their lower treatment intensity limits their value contribution. This pattern keeps the United States burn care market anchored by partial-thickness prevalence while allowing full-thickness cases to drive product sophistication and premiumization.

List of Companies Covered in this Report:

- AROA Biosurgery

- Avita Medical

- Coloplast

- Convatec

- DeRoyal Industries

- Human BioSciences

- Integra LifeSciences

- Kerecis

- Mallinckrodt Pharmaceuticals

- MediWound

- Medline Industries

- MIMEDX Group

- Molnlycke Health Care

- MTF Biologics

- Organogenesis

- PolyNovo

- Smiths Group

- Solventum

- Vericel

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High U.S. Burn Case Burden and Concentrated Referral Flows

- 4.2.2 Advanced Dressings, Grafts, and Biologics Adoption

- 4.2.3 Burn-Center Expansion and Outpatient Pathway Optimization

- 4.2.4 Teleburn Networks Closing Rural Access Gaps

- 4.2.5 Lithium-Ion Battery Fires Increasing High-Acuity Cases

- 4.2.6 BARDA-Backed Severe-Burn Preparedness and Domestic Capacity

- 4.3 Market Restraints

- 4.3.1 High Cost of Biologics and NPWT-Intensive Care Pathways

- 4.3.2 CMS 2026 Skin-Substitute Payment Reset

- 4.3.3 Rural Burn-Center Access and Specialist Staffing Gaps

- 4.3.4 Higher Evidence and Regulatory Bar for Advanced Biologics

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Advanced Dressings

- 5.1.1.1 Foam Dressings

- 5.1.1.2 Hydrocolloid Dressings

- 5.1.1.3 Hydrogel Dressings

- 5.1.1.4 Alginate Dressings

- 5.1.1.5 Antimicrobial Silver Dressings

- 5.1.1.6 Collagen Dressings

- 5.1.1.7 Silicone Contact Layers

- 5.1.2 Biologics and Skin Substitutes

- 5.1.3 Negative Pressure Wound Therapy

- 5.1.4 Traditional Dressings

- 5.1.5 Other Product Types

- 5.1.1 Advanced Dressings

- 5.2 By Burn Depth

- 5.2.1 Superficial Burns

- 5.2.2 Partial-Thickness Burns

- 5.2.3 Full-Thickness Burns

- 5.3 By Care Setting

- 5.3.1 Hospitals

- 5.3.2 Specialised Burn Centres and Wound Clinics

- 5.3.3 Ambulatory Surgery Centers

- 5.3.4 Home Health and Virtual Follow-up

- 5.3.5 Other Care Settings

- 5.4 By Burn Etiology

- 5.4.1 Thermal Burns

- 5.4.2 Electrical Burns

- 5.4.3 Chemical Burns

- 5.4.4 Radiation and Friction Burns

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 AROA Biosurgery

- 6.3.2 AVITA Medical

- 6.3.3 Coloplast

- 6.3.4 ConvaTec Group

- 6.3.5 DeRoyal Industries

- 6.3.6 Human BioSciences

- 6.3.7 Integra LifeSciences

- 6.3.8 Kerecis

- 6.3.9 Mallinckrodt

- 6.3.10 MediWound

- 6.3.11 Medline Industries

- 6.3.12 MIMEDX Group

- 6.3.13 Molnlycke Health Care

- 6.3.14 MTF Biologics

- 6.3.15 Organogenesis

- 6.3.16 PolyNovo

- 6.3.17 Smith+Nephew

- 6.3.18 Solventum

- 6.3.19 Vericel Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment