|

시장보고서

상품코드

2065552

모빌리티 및 이전 관리 소프트웨어 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Mobility And Relocation Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

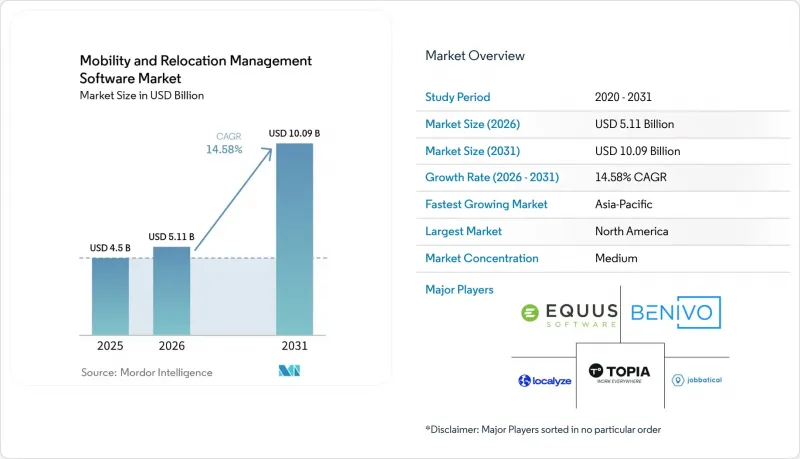

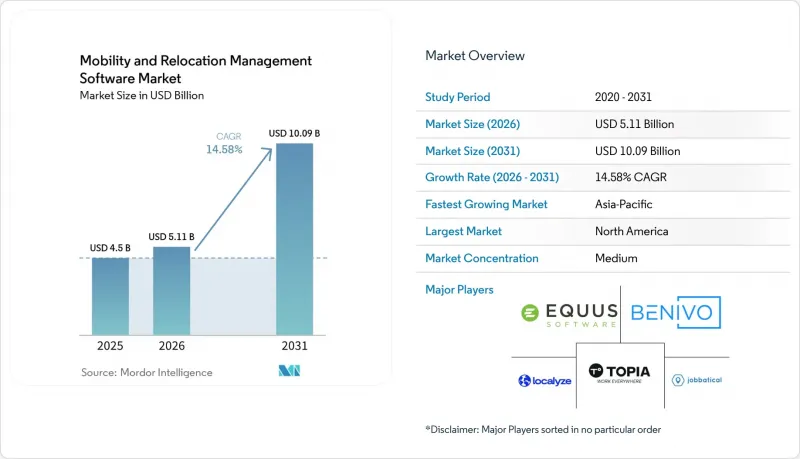

Mordor Intelligence에 의하면, 모빌리티 및 이전 관리 소프트웨어 시장 규모는 2025년 45억 달러로 평가되었습니다. 2026년 51억 1,000만 달러에서 2031년까지 100억 9,000만 달러에 이를 것으로 예상되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 14.58%를 나타낼 전망입니다.

본 보고서는 구성 요소(소프트웨어, 서비스), 배포 방식(클라우드 기반, On-Premise, 하이브리드), 기업 규모(대기업·중소기업), 용도(직원 전근 관리 등), 최종 사용자 산업(의료 및 생명과학 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 모빌리티 및 이전 관리 소프트웨어 시장 동향 및 인사이트

국경을 초월한 채용 및 분산 근무 방침의 확대

2020년부터 2025년에 걸쳐, 국경 간 채용은 선택적인 인재 확보 전술에서 핵심적인 인재 전략으로 전환되었으며, 이러한 변화가 모빌리티 및 이전 관리 소프트웨어의 잠재 시장을 직접적으로 확대시켰습니다. 국제변호사협회(IBA)의 보고서에 따르면, 2026년 3월에 도입된 가중치 적용 H-1B 비자 추첨 제도는 고임금 지원자를 우대하는 것으로, 중견 수준의 기술 인재 채용 흐름을 캐나다, 멕시코, 아일랜드로 밀어내어, 고용주가 동시에 관리해야 하는 인재 이동 경로(코리도)의 수를 증가시켰습니다. 프라고멘사의 보고서에 따르면, 2025년에는 전 세계 고용주의 74%가 필요한 인재 확보에 어려움을 겪었으며, 2030년까지 노동력 부족 규모는 8,500만 명에 달할 것이라는 예측도 제시되고 있습니다. 이는 국제적인 채용을 단순한 차선책이 아닌, 인재 계획의 핵심으로 계속해서 자리매김해야 할 필요성을 여실히 보여주고 있습니다. 더 많은 기업이 더욱 다양한 파견처에서 채용을 진행함에 따라, 모빌리티 담당 팀은 기존의 운영 모델로 관리하던 것보다 더 많은 활동 지역, 더 다양한 파견 형태, 그리고 더 많은 현지 규정 준수 요건을 추적해야 합니다. 이러한 운영상의 변화로 인해 스프레드시트나 이메일 교환을 통한 관리가 어려워지고 있으며, 더 대규모이고 다양한 인재 이동을 관리하기 위해 기업 전체 차원의 소프트웨어 도입이 촉진되고 있습니다. 또한, 인력 재배치가 더 이상 제한된 파견 대상국에 집중되지 않기 때문에 비전통적인 경로를 지원할 수 있는 플랫폼에 대한 수요도 증가하고 있습니다.

이민·세무·급여 계산 관련 규정 준수를 일원화하여 관리해야 할 필요성이 커지고 있습니다.

이주·전근 관리 소프트웨어 시장은 서로 연계되지 않은 팀이나 여러 파일에 걸쳐 관리하는 방식이 아닌, 단일 시스템을 통해 이민, 세무, 급여 관련 규정 준수를 관리해야 할 필요성이 더욱 절실해지고 있는 점도 성장에 힘을 실어주고 있습니다. EY의 조사에 따르면, 응답자의 95%가 규제 및 규정 준수의 복잡성이 모빌리티 도입을 지연시키고 있다고 답했으며, 이는 2026년 이 문제가 프로그램 실행에 얼마나 광범위한 영향을 미치고 있는지를 보여줍니다. EU의 입국·출국 관리 시스템에서는 수작업으로 이루어지던 여권 도장 확인이 생체 인식 등록 및 체류 기간 자동 추적으로 점차 대체되고 있습니다. 이는 기업의 프로그램에서 사후 요약이 아닌, 최신 규정 준수 대시보드를 유지할 수 있는 시스템에 대한 수요가 높아지고 있음을 의미합니다. 또한, 유럽 데이터 보호 위원회는 2026년 4월, GDPR(EU 개인정보보호규정) 제42조 및 제46조에 근거한 국제적 개인 데이터 이전 인증 메커니즘으로서 ‘Europrivacy’를 승인했습니다. 이는 국경을 초월한 데이터 거버넌스가 얼마나 빠르게 소프트웨어 인증 요건의 일부로 자리 잡고 있는지를 반영하고 있습니다. 디지털 국경 관리 시스템과 데이터 이전 규정이 더욱 공식화됨에 따라, 구매자들은 급여 계산 및 입국 관리 워크플로우를 실시간으로 실행할 수 있는 플랫폼을 더욱 높이 평가했습니다. 이에 따라, 감사에 대응할 수 있는 보고서 작성, 신속한 알림, 그리고 모빌리티, 세무, 급여 계산 기능 간의 원활한 통합을 지원할 수 있는 제품을 제공하는 벤더의 가격 결정력이 강화되고 있습니다.

판매 주기의 장기화와 복잡한 기업 통합

모빌리티 및 이전 관리 소프트웨어 시장에서는 구매자 수요가 분명히 존재하더라도, 장기적인 기업용 판매 주기로 인해 수익 창출이 계속 지연되고 있습니다. 이 분야의 조달 결정에는 일반적으로 법무, 세무, 인사, IT, 재무 각 팀이 관여하며, 각 그룹이 서로 다른 업무적 관점에서 제품을 평가하기 때문에 승인에 시간이 걸립니다. 또한, 조사 결과에 따르면 대규모 구매 기업들은 최종 선정에 앞서 3-5개의 HRIS 및 급여 계산 시스템과의 기존 양방향 연동을 기대하는 경우가 많으며, 이로 인해 프로세스 초기 단계에서 많은 소규모 공급업체들이 본격적인 검토 대상에서 제외되고 있습니다. 이 때문에 신규 진입 업체들은 도입 요건이 비교적 완만하고 의사결정 주기도 짧은 중견 시장으로 밀려나는 반면, 기존 업체들은 여전히 대기업과의 계약에서 강점을 발휘하고 있습니다. 그 결과, 시장 구조는 양극화되어 있으며, 구매 주기 전반에 걸쳐 통합의 깊이와 재무적 지속가능성이 중요시되기 때문에 제품의 기능성만으로는 수주율이 결정되지 않습니다. 이로 인해 자동화에 대한 근본적인 수요가 높아지고 있음에도 불구하고, 혁신이 수익으로 실현되기까지의 속도가 더디어지고 있습니다.

부문별 분석

이 소프트웨어는 2025년 시장에서 67.28%를 차지했으며, 구성 요소별로는 모빌리티 및 이전 관리 소프트웨어 시장에서 가장 큰 점유율을 확보함으로써, 부임 관리, 정책 관리, 입국 관리 및 보고서 작성 분야에서 핵심 시스템으로서의 입지를 확고히 다졌습니다. 2025년에는 모빌리티 관리 플랫폼이 소프트웨어 하위 유형 중 가장 큰 점유율(32.31%)을 차지했으며, 대규모 모빌리티 프로그램을 관리할 때 구매자들이 단일 기능 도구보다 통합형 플랫폼을 계속해서 선호하는 것으로 나타났습니다. 모빌리티 및 이전 관리 소프트웨어 시장에서 이러한 추세는 단일 프로세스 영역뿐만 아니라 부임 라이프사이클 전체를 아우를 수 있는 공급업체를 뒷받침하고 있습니다. 전근 워크플로우 소프트웨어, 입국 관리 및 규정 준수 관리 소프트웨어, 분석 플랫폼, 직원용 셀프 서비스 포털은 여전히 동일한 고객 계정 내의 서로 다른 사용자 그룹을 지원하며, 공급업체 입장에서는 번들형 구독이나 모듈 확장을 통해 계약을 확대할 여지가 되고 있습니다.

서비스 부문은 가장 빠르게 성장하고 있는 분야로, 2031년까지 연평균 성장률(CAGR)이 19.47%를 나타낼 것으로 전망됩니다. 이는 구매자가 공급업체나 파트너에게 단순히 소프트웨어에 대한 접근 권한을 제공하는 것뿐만 아니라, 운영 업무의 부담을 더 많이 관리해 줄 것을 요구하는 경향이 강해지고 있기 때문입니다. 이동 및 전근 관리 소프트웨어 업계에서 이는 더 많은 관할권에서 규정 준수 문제가 복잡해지는 가운데, 소프트웨어 플러스 서비스(SaaS) 모델로의 광범위한 전환을 반영하고 있습니다. 중견 기업의 구매 담당자들은 사내에 본격적인 모빌리티 팀을 구성하지 않은 채 예측 가능한 성과를 요구하는 경우가 많기 때문에 이들이 이러한 수요의 주요 원천이 되고 있습니다. 이러한 추세는 비용 관리의 책임이 소프트웨어 공급업체와 도입 파트너 간에 분담되고 있다는 사용자들의 의견과도 일치하며, 부가 기능보다는 서비스의 충실도가 보다 현실적인 구매 판단 기준이 되고 있음을 보여줍니다.

2025년 모빌리티 및 이전 관리 소프트웨어 시장에서 클라우드 기반 도입이 69.12%를 차지했으며, 이는 SaaS 방식의 제공이 신속한 도입과 벤더 관리를 통한 업데이트를 원하는 기업의 구매 성향과 얼마나 밀접하게 부합하는지를 여실히 보여주었습니다. 이러한 상황은 클라이언트 측에서 패치를 적용할 필요 없이 벤더 환경을 통해 이민법 및 규정 준수 규칙의 변경 사항을 수신할 수 있다는 실질적인 이점에 힘입어 가능했습니다. On-Premise 배포는 정부, 국방 및 금융 서비스 업계의 일부 등 규제가 엄격한 환경에서 여전히 중요합니다. 이러한 환경에서는 데이터 주권 요건과 레거시 인프라로 인해 완전한 클라우드 전환이 어려워지고 있습니다. 모빌리티 및 이전 관리 소프트웨어 시장에서 이러한 제약으로 인해, 도입 방식의 선택은 업종별 위험 프로파일 및 각국의 데이터 규제와 밀접하게 연관되어 있습니다.

하이브리드 방식은 가장 빠르게 성장하고 있는 형태로, 전 세계 고용주들이 프런트엔드의 유연성과 기밀성이 높은 인사·세무 데이터에 대한 엄격한 관리 사이의 균형을 모색함에 따라, 2031년까지 연평균 성장률(CAGR) 20.36%로 확대될 것으로 전망됩니다. 이 모델은 특정 범주의 직원 정보를 국내에 보관해야 하는 국가에서 특히 중요하며, 일부 다국적 프로그램의 경우 완전한 클라우드 도입이 현실적으로 어렵습니다. 또한, 이러한 구조를 통해 공급업체는 단일 고객 관계 내에서 전 세계 및 각 지역의 요구 사항을 충족할 수 있게 되며, 고객이 지역별로 병행되는 시스템을 유지해야 하는 상황을 피할 수 있습니다. 그 결과, 하이브리드 아키텍처는 기존 도입 모델과 최신 도입 모델 사이의 일시적인 타협안이 아니라, 전략적인 제품 특성으로 자리 잡고 있습니다.

지역별 분석

2025년 시장에서 북미는 41.77%를 차지하며, 모빌리티 및 이전 관리 소프트웨어 시장에서 가장 큰 점유율을 기록했습니다. 이는 다국적 기업의 본사가 집중되어 있다는 점, 성숙한 인사 기술 도입 관행, 그리고 확립된 전근 서비스 네트워크를 반영한 것입니다. 미국은 여전히 해당 지역에서 가장 큰 국가별 시장이었으나, 2026년 정책 환경의 변화로 인해 신규 H-1B 비자 신청에 대한 10만 달러의 수수료, 임금 가중치를 적용한 추첨, 그리고 취업 허가 조건의 강화 등을 통해 규정 준수 부담이 증가함에 따라, 고용주들은 보다 광범위한 리소스 관리의 필요성에 직면하게 되었습니다. 캐나다와 멕시코는 이러한 기술 인재 채용 동향의 변화로 인해 혜택을 보고 있으며, 기존 엔터프라이즈 플랫폼 도입 환경 내에서 다국간 프로젝트 처리에 대한 수요가 증가하고 있습니다. 아틀라스 반 라인즈(Atlas Van Lines)사의 보고서에 따르면, 2025년에는 기업의 54%가 전근 건수를 늘릴 것이며, 61%는 2026년에 예산을 증액할 것으로 전망되고 있는데, 이는 정책 설계가 더욱 유연해지고 직원 경험 문제가 중요시되는 상황 속에서도 해당 지역의 견고한 수요 기반이 뒷받침되고 있음을 보여줍니다. 또한, 니스쇼어 기술·제조 허브로서 멕시코의 위상이 높아지고 있는 점도, 이전의 소프트웨어 도입 주기에서는 그다지 중요하게 여겨지지 않았던 새로운 파견 경로를 만들어내고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 24.39%를 나타낼 것으로 예측되며, 모빌리티 및 이전 관리 소프트웨어 시장에서 가장 빠르게 성장하는 지역 부문이 될 전망입니다. 사용자들의 의견에 따르면, 이러한 성장은 인도, 중국, 일본, 한국, 호주에서의 제조업 확대, 지역 내 인력 배치 증가, 그리고 기업 인사 시스템의 디지털화 가속화와 관련이 있는 것으로 보입니다. 또한, 해당 지역에서는 기업 출장 활동의 활성화도 긍정적인 요인으로 작용하고 있어, 프로그램의 규모가 확대되고 자동화된 모빌리티 관리가 더욱 경제적으로 운영될 수 있는 거래량이 많은 환경이 조성되고 있습니다. 인도와 중국은 인바운드 이동성, 국내 배치, 현지 언어 지원, 데이터 상주 요건 등이 공급업체가 해당 시장을 겨냥한 제품을 구성하는 데 영향을 미치기 때문에 여전히 특히 중요한 시장으로 남아 있습니다.

유럽은 GDPR(EU 개인정보보호규정), EU 입출국 시스템, EU 임금 투명성 지침 등에 따라 이동 및 전근 관리 소프트웨어 시장에서 감사에 대응할 수 있는 문서화 및 보다 강력한 데이터 관리의 필요성이 높아지고 있어, 여전히 규모가 크고 규정 준수 요건이 엄격한 시장으로 남아 있습니다. ECA International은 2026년 4월, 유럽집행위원회가 ESSPASS에 관한 공개 협의를 시작했다고 보고했으며, 이는 가까운 시일 내에 EU 회원국 전체의 각국 사회보장 시스템과 연계되는 플랫폼이 필요해질 것임을 시사하고 있습니다. 독일, 영국, 프랑스는 대규모 다국적 노동력을 보유하고 있는 한편, 데이터 보호 및 규정 준수 대응과 관련하여 보다 엄격한 조달 요건을 갖추고 있어, 계속해서 지역 수요의 주축을 이루고 있습니다. 중동, 특히 아랍에미리트(UAE)와 사우디아라비아에서는 정부의 경제 다각화 프로그램에 따라 숙련된 외국인 노동자의 유입이 증가하고 있으며, 현지 후원 제도 및 할당 규정을 관리할 수 있는 소프트웨어에 대한 수요가 높아지면서 시장이 확대되고 있습니다. 남미에서는 브라질을 필두로 완만한 성장 기회가 예상됩니다. 브라질에서는 LGPD(개인정보보호법) 준수가 국경을 넘는 도입 과정에서 소프트웨어의 적격성 요건을 하나 더 추가하는 요인이 되고 있습니다. 한편, 아프리카는 여전히 초기 단계에 있지만, 기존과는 다른 경로를 통해 서비스 제공 범위를 확대함으로써 벤더들의 관심을 끌고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the mobility and relocation management software market size is projected to expand from USD 4.50 billion in 2025 and USD 5.11 billion in 2026 to USD 10.09 billion by 2031, registering a CAGR of 14.58% between 2026 and 2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, On-Premise, and Hybrid), Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Application (Employee Relocation Management and More), End-User Industry (Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Mobility And Relocation Management Software Market Trends and Insights

Expansion of Cross-Border Hiring And Distributed Work Policies

Cross-border hiring moved from a selective workforce tactic to a core talent strategy between 2020 and 2025, and that shift has directly widened the addressable market for mobility and relocation management software. The International Bar Association reported that the weighted H-1B lottery introduced in March 2026 favored higher-wage candidates and pushed mid-tier technical hiring flows toward Canada, Mexico, and Ireland, increasing the number of corridors employers must manage simultaneously. Fragomen reported that 74% of employers globally struggled to find the talent they needed in 2025, and the projected worker shortfall could reach 85 million by 2030, underscoring the need to keep international hiring central to workforce planning rather than a secondary option. As more companies hire across a wider mix of destinations, mobility teams must track more active jurisdictions, more assignment types, and more local compliance conditions than they managed in earlier operating models. That operating change makes spreadsheets and email chains harder to sustain, which supports software adoption across enterprises that now manage larger and more diverse mobility flows. It also increases demand for platforms that can support non-traditional corridors, because talent redeployment is no longer concentrated in a narrow group of destination countries.

Rising Need for Centralized Immigration, Tax, And Payroll Compliance

The mobility and relocation management software market is also being driven by a sharper need to manage immigration, tax, and payroll compliance from a single system rather than across disconnected teams and files. EY found that 95% of respondents said regulatory and compliance complexity was slowing mobility delivery, which shows how widely this issue is affecting program execution in 2026. The EU Entry/Exit System is replacing manual passport stamp checks with biometric registration and automated stay tracking, which means enterprise programs increasingly need systems that can maintain current compliance dashboards instead of retrospective summaries. The European Data Protection Board also approved Europrivacy in April 2026 as a certified mechanism for international personal data transfers under GDPR Articles 42 and 46, which reflects how quickly cross-border data governance is becoming part of software qualification requirements. As digital border systems and transfer rules become more formalized, buyers are placing higher value on platforms that can trigger payroll and immigration workflows in real time. That raises the pricing power of vendors whose products can support audit-ready reporting, faster alerts, and cleaner integration between mobility, tax, and payroll functions.

Long Sales Cycles and Complex Enterprise Integrations

Long enterprise sales cycles continue to slow revenue conversion in the mobility and relocation management software market, even when buyer demand is visible. Procurement decisions in this category usually involve legal, tax, HR, IT, and finance teams, and each group evaluates the product through a different operating lens, which extends approval time. The input also shows that large buyers often expect pre-built, bidirectional connections to 3-5 HRIS and payroll systems before final selection, which removes many smaller vendors from serious consideration early in the process. This pushes newer suppliers toward the mid-market, where deployment requirements are lighter, and decision cycles are shorter, while established vendors remain stronger in large-enterprise contracts. The result is a split market structure where product capability alone does not determine win rates, because integration depth and financial stamina matter throughout the buying cycle. That slows the recognition of innovation as revenue, even as the underlying need for automation grows.

Other drivers and restraints analyzed in the detailed report include:

- Shift From Spreadsheets to Integrated Mobility Automation

- Growth In Flexible Mobility Policies Such As Lump Sum And Core-Flex Programs

- Data Privacy, Cross-Border Transfer, And Security Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 67.28% of the 2025 market, giving it the largest mobility and relocation management software market share among components and confirming its role as the main system of record for assignment management, policy administration, immigration tracking, and reporting. Mobility management platforms held the largest software sub-type share at 32.31% in 2025, indicating that buyers continue to prefer consolidated platforms over single-function tools when managing large mobility programs. In the mobility and relocation management software market, that preference supports vendors that can cover the full assignment lifecycle rather than just one process area. Relocation workflow software, immigration and compliance management software, analytics platforms, and employee self-service portals still address different user groups within the same customer account, giving vendors room to extend contracts through bundled subscriptions and module expansion.

Services is the fastest-growing component, with a 19.47% CAGR through 2031, as buyers increasingly ask vendors and partners to manage more of the operating workload rather than just deliver software access. In the mobility and relocation management software industry, this reflects a broader move toward software-plus-services models as compliance complexity rises across more jurisdictions. Mid-market buyers are a key source of this demand because they often want predictable outcomes without building a full internal mobility team. That trend also aligns with user input that cost-control accountability is being split between software providers and implementation partners, making service depth a more practical buying factor than an add-on feature.

Cloud-based deployment accounted for 69.12% of the 2025 mobility and relocation management software market, underscoring how closely SaaS delivery aligns with enterprise buying preferences for faster implementation and vendor-managed updates. This position was supported by the practical benefit of receiving immigration and compliance rule changes through the vendor environment without client-side patching. On-premises deployment still matters in regulated settings such as government, defense, and parts of the financial services industry, where data sovereignty requirements or legacy infrastructure make full cloud migration difficult. In the mobility and relocation management software market, those constraints keep deployment choices closely tied to sector risk profiles and national data rules.

Hybrid deployment is the fastest-growing mode and is projected to expand at a 20.36% CAGR through 2031 as global employers try to balance front-end flexibility with tighter control over sensitive HR and tax data. This model is particularly relevant in countries where certain categories of employee information must remain within national borders, making full cloud deployment impractical for some multinational programs. The structure also helps vendors serve global and regional needs within a single customer relationship, rather than forcing clients to maintain parallel systems by geography. As a result, hybrid architecture is becoming a strategic product attribute rather than a temporary compromise between legacy and modern deployment models.

Geography Analysis

North America accounted for 41.77% of the 2025 market, giving the region the highest market share in mobility and relocation management software and reflecting its concentration of multinational headquarters, mature HR technology buying practices, and established relocation service networks. The United States remained the largest country market in the region, but the 2026 policy environment increased the compliance burden through a USD 100,000 fee for new H-1B petitions, a wage-weighted lottery, and tighter work authorization conditions, pushing employers toward broader corridor management needs. Canada and Mexico are benefiting from this redirection of technical hiring, which increases demand for multi-country case handling inside existing enterprise platform deployments. Atlas Van Lines reported that 54% of companies increased relocation volume in 2025 and that 61% expected to raise budgets in 2026, reinforcing the region's strong demand base even as policy design becomes more flexible and employee-experience issues gain weight. Mexico's rising position as a nearshore technology and manufacturing hub is also adding a newer assignment corridor that did not carry the same weight in earlier software adoption cycles.

Asia-Pacific is projected to grow at a 24.39% CAGR through 2031, making it the fastest-growing regional segment in the mobility and relocation management software market. The user input ties this growth to manufacturing expansion, greater intraregional deployment of talent, and faster digitization of enterprise HR systems across India, China, Japan, South Korea, and Australia. The region is also benefiting from stronger corporate travel activity, creating a higher-volume environment where automated mobility control becomes more economical for a wider range of program sizes. India and China remain especially important because inbound mobility, domestic deployment, local-language support, and data residency requirements all shape how vendors configure products for these markets.

Europe remains a large and compliance-intensive market because GDPR, the EU Entry/Exit System, and the EU Pay Transparency Directive all increase the need for audit-ready documentation and stronger data controls inside the mobility and relocation management software market. ECA International reported in April 2026 that the European Commission had launched a public consultation on ESSPASS, signaling a near-term need for platforms to connect with national social security systems across EU member states. Germany, the United Kingdom, and France continue to anchor regional demand because they combine large multinational workforces with stricter procurement expectations around data protection and compliance readiness. The Middle East, especially the UAE and Saudi Arabia, is growing as government diversification programs bring in more skilled international workers and require software that can manage local sponsorship and quota rules. South America presents a moderate growth opportunity led by Brazil, where LGPD compliance adds another layer of software qualification for cross-border deployments, while Africa remains earlier-stage but is drawing more vendor attention through expanding service coverage in non-traditional corridors.

- Equus Software, LLC

- Topia Mobility Inc.

- Localyze GmbH

- Jobbatical OU

- Benivo Limited

- Envoy Global, Inc.

- Mitratech, Inc.

- Ineo, LLC

- MoveAssist International Limited

- RelocationOnline Inc.

- Netensity Corporation

- UrbanBound, Inc.

- Updater Inc.

- ECA

- ReloTalent Pte Ltd.

- CadM USA Inc.

- CAD Management Ltd.

- WorkFlex

- Orion Mobility LLC

- mLINQS LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Expansion of Cross-Border Hiring and Distributed Work Policies

- 4.3.2 Rising Need for Centralized Immigration, Tax, and Payroll Compliance

- 4.3.3 Shift From Spreadsheets to Integrated Mobility Automation

- 4.3.4 Growth in Flexible Mobility Policies Such as Lump Sum and Core-Flex Programs

- 4.3.5 Need to Govern Short-Term Project Moves, Group Moves, and Internal Talent Deployments

- 4.3.6 Demand for Integrated Mobility Ecosystems Connecting Human Capital Systems, Payroll, Travel, and Vendors

- 4.4 Market Restraints

- 4.4.1 Long Sales Cycles and Complex Enterprise Integrations

- 4.4.2 Data Privacy, Cross-Border Transfer, and Security Requirements

- 4.4.3 Fragmented Destination-Service and Supplier Data Standards

- 4.4.4 Program Budget Volatility From Housing, Tax Gross-Up, and Exception Costs

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.1.1 Mobility Management Platforms

- 5.1.1.2 Relocation Workflow Software

- 5.1.1.3 Immigration and Compliance Management Software

- 5.1.1.4 Mobility Analytics Platforms

- 5.1.1.5 Employee Self-service Mobility Portals

- 5.1.2 Services

- 5.1.1 Software

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 Employee Relocation Management

- 5.4.2 Immigration and Visa Management

- 5.4.3 Assignment Management and Policy Administration

- 5.4.4 Expense and Compensation Management

- 5.4.5 Analytics and Compliance Reporting

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Equus Software, LLC

- 6.4.2 Topia Mobility Inc.

- 6.4.3 Localyze GmbH

- 6.4.4 Jobbatical OU

- 6.4.5 Benivo Limited

- 6.4.6 Envoy Global, Inc.

- 6.4.7 Mitratech, Inc.

- 6.4.8 Ineo, LLC

- 6.4.9 MoveAssist International Limited

- 6.4.10 RelocationOnline Inc.

- 6.4.11 Netensity Corporation

- 6.4.12 UrbanBound, Inc.

- 6.4.13 Updater Inc.

- 6.4.14 ECA

- 6.4.15 ReloTalent Pte Ltd.

- 6.4.16 CadM USA Inc.

- 6.4.17 CAD Management Ltd.

- 6.4.18 WorkFlex

- 6.4.19 Orion Mobility LLC

- 6.4.20 mLINQS LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment