|

시장보고서

상품코드

2065571

통신 전사적 자원 계획(ERP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Telecom Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

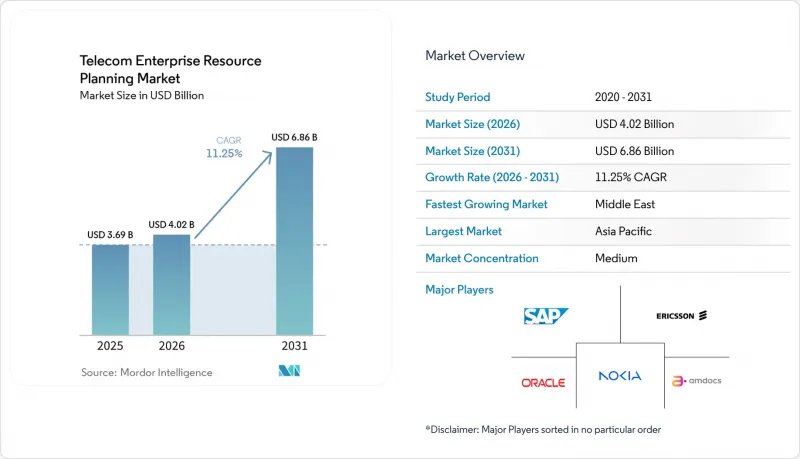

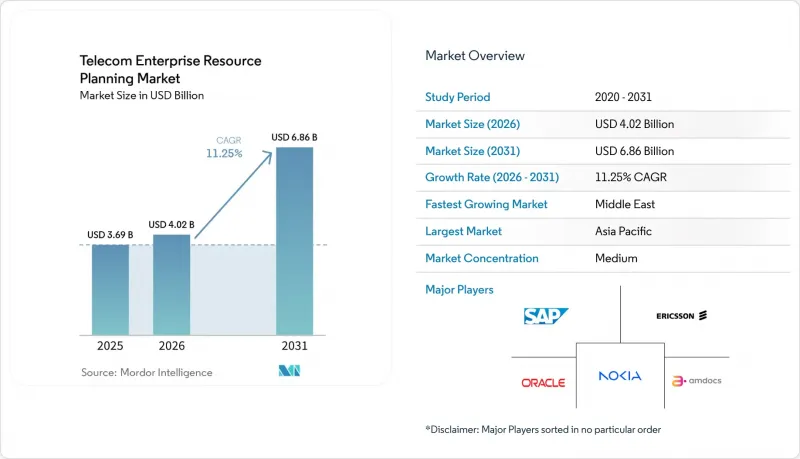

Mordor Intelligence에 의하면, 통신 전사적 자원 계획(ERP) 시장 규모는 2025년 36억 9,000만 달러로 평가되었습니다. 2026년에는 40억 2,000만 달러로 확대되어 2031년까지 68억 6,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 11.25%로 성장할 전망입니다.

본 보고서는 배포 모델(On-Premise, 클라우드, 하이브리드), 구성 요소(소프트웨어 및 서비스), 조직 규모(중소규모 통신 사업자·대규모 통신 사업자), 기능(재무 및 회계, 인사, 공급망·조달, 고객 관계 관리, 네트워크 관리 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 통신 전사적 자원 계획(ERP) 시장 동향 및 인사이트

통신 서비스 제공업체(CSP)에서의 5G 네트워크 보급

독립형 5G 코어 네트워크에는 실시간 과금, 동적 비용 배분, 파트너 클라우드 간의 오케스트레이션이 필요하지만, 이러한 기능들은 기존의 ERP 시스템으로는 지원할 수 없습니다. MTN 남아프리카의 2025년 사업 계획에서 이러한 과제가 부각됨에 따라, 이 회사는 재무, 재고, 네트워크 분석을 통합한 클라우드 네이티브 제품군을 도입하기로 했습니다. 오만과 인도네시아의 통신 사업자들도 이러한 변화에 발맞추어 API 기반 ERP 워크플로를 통해 서비스 개시까지 걸리는 기간을 몇 주에서 몇 시간으로 단축했습니다. 또한, 5G의 저지연성과 슬라이싱 기능을 통해 세분화된 SLA 가격 책정이 필요한 수직 통합형 엔터프라이즈 서비스가 가능해지면서, 카탈로그 기능과 수익 보장 엔진을 탑재한 모듈형 ERP로의 전환이 가속화되고 있습니다. 하이브리드 방식은 On-Premise 환경의 과금 거버넌스를 유지하면서 슬라이스의 수익화를 최적화하는 분석 기능을 클라우드화할 수 있기 때문에 현재 시장 성장률을 웃도는 속도로 확대되고 있습니다.

자동화를 통한 운영 비용 절감 노력

ARPU 성장 둔화와 통신탑 임대료 급등으로 인해, 통신 사업자들이 수작업에 의존하는 프로세스를 유지할 여지는 거의 남아 있지 않습니다. 릴라이언스 지오는 통합된 ERP 플랫폼 내에서 조달, 재고 대조, 공급업체 대금 지급을 자동화함으로써 2024년에 운영 비용을 30% 절감했습니다. 에릭슨은 SAP S/4HANA로 전환한 후 프로젝트 예산을 30% 절감함으로써, 클라우드 ERP가 도입 기간과 컨설팅 비용을 모두 단축할 수 있음을 입증했습니다. GDPR(EU 개인정보보호규정)과 같은 규제 체계는 감사 추적 기록의 자동화를 더욱 요구하고 있으며, 규정 준수는 비용 센터에서 이사회 차원의 성장 동력으로 변모하고 있습니다. 한때 자본 제약으로 어려움을 겪었던 중소 통신사들은 그로 인해 시장 전체의 연평균 성장률(CAGR)보다 약 1.5배 빠른 속도로 SaaS형 ERP를 도입하고 있습니다.

Tier 3 통신 사업자에게 있어 높은 초기 라이선스 비용

중규모 통신 사업자의 경우, 엔터프라이즈급 ERP 라이선스 비용이 500만 달러를 초과하기도 하며, 그 금액은 통신탑 건설비나 주파수 대역 갱신 비용에 필적합니다. SaaS의 가격 책정은 이러한 부담을 줄여주지만, 벤더 종속이나 환율 변동에 대한 우려를 불러일으키고 있습니다. 이러한 재무적 장벽으로 인해 예상 연평균 성장률(CAGR)은 약 1.4% 하락했으며, 공급업체의 파이프라인은 대형 기존 사업자로 편중되어 있습니다.

부문별 분석

하이브리드형 도입은 2025년에 통신 전사적 자원 계획(ERP) 시장에서 상당한 점유율을 확보했으며, 2031년까지 연평균 성장률(CAGR) 15.2%로 성장할 전망입니다. 통신 사업자는 가입자 데이터와 중요한 과금 처리를 On-Premise에서 유지하면서, 분석, 조달, 인사 관리에는 클라우드의 확장성을 활용하고 있습니다. 이러한 접근 방식은 데이터 주권과 관련된 장벽을 우회할 수도 있습니다. 클라우드 모델은 여전히 매력적이며, 2025년에는 통신 전사적 자원 계획(ERP) 시장의 46%를 차지했지만, 미션 크리티컬한 워크로드에는 여전히 로컬에서의 제어가 요구되기 때문에 순수 클라우드 모델의 성장세는 하이브리드 모델에 뒤처지고 있습니다. 지연 시간에 민감한 엣지 용도이 보급됨에 따라, 통신 전사적 자원 계획(ERP) 시장 규모는 더욱 확대될 것으로 예측됩니다.

Freedom Mobile의 클라우드 전환 사례는 하이브리드 설계를 통해 99.99%의 가용성과 IT 운영 비용(OPEX) 35% 절감을 실현할 수 있음을 입증했습니다. 현재 Vodafone와 Orange, 그리고 걸프 지역 통신사들에서도 유사한 모델이 도입되고 있습니다. 중국과 러시아에서는 엄격한 데이터 거주 요건이 퍼블릭 클라우드 도입을 저해하고 있지만, 규제 당국은 향후 규제를 완화할 의향을 밝히고 있어, 이에 따라 예측 기간 동안 누적된 수요가 하이브리드 솔루션으로 전환될 것으로 전망됩니다.

2025년에는 소프트웨어 라이선싱이 매출의 55%를 차지했지만, 컨설팅에서 관리형 운영에 이르는 서비스는 연평균 성장률(CAGR) 17.8%라는 더 빠른 속도로 확대되고 있습니다. 통신 사업자들이 데이터 마이그레이션, AI 모델 튜닝, API 거버넌스 등 희소성이 높은 기술을 외부에 위탁함에 따라, 통신 업계의 서비스용 전사적 자원 계획(ERP) 시장이 확대되고 있습니다. 에릭슨의 SAP 프로그램은 라이선스 비용이 아닌 자동화된 전환을 통해 30%의 비용 절감을 실현함으로써, 가치가 어디에서 창출되는지를 명확히 보여주었습니다.

IBM, 액센츄어, 암독스 등의 시스템 통합 업체들은 전환 일정을 보장하는 고정 가격의 번들 패키지를 제공하고 있으며, 이러한 제안은 기한이 정해지지 않은 IT 예산에 지친 CFO들의 공감을 얻고 있습니다. AI 모듈이 네트워크 관리 분야에 점차 확산됨에 따라 ‘서비스형 데이터 사이언스자(Data Scientist as a Service)’에 대한 수요가 증가하고 있으며, 해당 서비스에 대한 지출 비중이 더욱 확대되고 있습니다. 그 결과, 소프트웨어가 기반으로서의 역할을 유지하는 한편, 통신 전사적 자원 계획(ERP) 시장에서 서비스 점유율은 꾸준히 확대될 것으로 예측됩니다.

지역별 분석

아시아태평양은 2025년에 매출의 34%를 차지했으며, 인도의 5G 사업 수익화가 급속히 진행되고 중국에서 수십억 달러 규모의 가상화 프로그램이 이를 주도했습니다. 릴라이언스 지오가 ERP를 활용해 운영 비용(OpEx)을 30% 절감한 데 이어, 바티 에어텔과 보다폰 아이디어도 유사한 프로젝트를 시작했습니다. 4G 주기에서 현대화를 이룬 일본과 한국은 현재 주파수 대역을 최적화하는 AI 오버레이 모듈에 주력하고 있으며, 시장 점유율이 핵심 재무 지표에서 네트워크 분석으로 미묘하게 이동하고 있습니다. 현지 규제 당국이 국경을 넘는 데이터 유통에 대한 장벽을 완화함에 따라, 하이브리드 ERP 도입은 증가하는 엣지 컴퓨팅 트래픽에 발맞추어 나갈 것입니다.

중동은 연평균 성장률(CAGR) 13.6%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 사우디아라비아의 ‘비전 2030’ 요건과 아랍에미리트(UAE)의 스마트시티 구상에서는 실시간 과금, IoT 통합, 유연한 프로비저닝이 요구되고 있습니다. STC와 에티살라트는 이러한 기능을 확보하기 위해 클라우드 네이티브 ERP로의 전환을 추진하고 있으며, 걸프협력회의(GCC)의 데이터법 조화를 위한 노력이 이러한 추세를 더욱 가속화하고 있습니다. 튀르키예와 이스라엘도 이에 발맞추어, 경쟁이 치열한 모바일 시장에서 ERP 현대화를 활용해 기업용 서비스 포트폴리오의 차별화를 꾀하고 있습니다.

북미와 유럽은 여전히 규모가 크지만, 시장은 성숙기에 접어들었습니다. AT&T의 140억 달러 규모의 네트워크 계획과 Verizon의 주파수 대역 투자에서는 조달 및 재고 관리 자동화를 위한 ERP에 막대한 자금이 배정되고 있습니다. 유럽에서는 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)에 따라 실시간 수익 보장이 의무화되어 있어, 통신 사업자들은 규정 준수 워크플로가 통합된 ERP 제품군을 도입하도록 장려받고 있습니다. 따라서 성장 전략은 그린필드 방식의 시스템 교체보다는 모듈 수준의 업그레이드에 중점을 두고 있습니다. 남미와 아프리카에서는 진전이 더딘 편이지만, ‘성장에 따른 과금’ 방식을 제공하는 SaaS 모델이 자금 사정에 어려움을 겪고 있는 통신 사업자들의 잠재적 수요를 발굴하기 시작하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the telecom ERP market size is expected to increase from USD 3.69 billion in 2025 to USD 4.02 billion in 2026 and reach USD 6.86 billion by 2031, growing at a CAGR of 11.25% over 2026-2031.

This report is Segmented by Deployment Model (On-Premise, Cloud, and Hybrid), Component (Software and Services), Organization Size (Small and Medium Telecom Operators and Large Telecom Operators), Function (Finance and Accounting, Human Resources, Supply Chain and Procurement, Customer Relationship Management, Network Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Telecom Enterprise Resource Planning Market Trends and Insights

Proliferation Of 5G Networks Among CSPs

Standalone 5G cores require real-time billing, dynamic cost allocation, and orchestration across partner clouds, functions that legacy ERP stacks cannot handle. MTN South Africa's 2025 rollout exposed these gaps, prompting the carrier to adopt a cloud-native suite that integrates finance, inventory, and network analytics. Operators in Oman and Indonesia echoed this pivot, reducing activation windows from weeks to hours through API-based ERP workflows. 5G's latency and slicing capabilities also unlock vertical enterprise services that demand granular SLA pricing, intensifying the shift toward modular ERP with embedded catalog and revenue-assurance engines. Hybrid deployments now outpace market growth because they retain on-premise billing governance while cloudifying analytics that optimize slice monetization.

Push Toward Operational Expenditure Reduction Via Automation

Stagnant ARPU and tower-lease inflation leave operators little room for manual processes. Reliance Jio cut operating costs by 30% in 2024 by automating procurement, inventory reconciliation, and vendor payments within a unified ERP fabric. Ericsson shaved 30% off project budgets after moving to SAP S/4HANA, confirming that cloud ERP compresses both implementation time and consultant fees. Regulatory frameworks like GDPR further demand automated audit trails, turning compliance from a cost center into a board-level driver. Small and medium carriers, once hampered by capital constraints, are therefore adopting SaaS ERP at almost 1.5 times the overall market CAGR.

High Upfront Licensing Costs For Tier-3 Operators

For a mid-size carrier, enterprise-grade ERP licenses can exceed USD 5 million, a figure that rivals tower builds and spectrum renewals. ARPU below USD 2 restricts credit headroom, delaying modernization projects in Africa and parts of Southeast Asia. SaaS pricing eases the pain but triggers concerns about vendor lock-in and exchange-rate volatility. This financial barrier reduces the projected CAGR by roughly 1.4 percentage points and skews vendor pipelines toward larger incumbents.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption Of Cloud-Native BSS/OSS Stacks In Tier-1 Operators

- Integration Of AI-Driven Predictive Analytics Within ERP Suites

- Data Migration Complexities From Legacy OSS/BSS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid deployments captured a meaningful share of the telecom ERP market in 2025 and are poised to grow at a 15.2% CAGR through 2031. Operators keep subscriber data and critical billing on-premise while leveraging cloud elasticity for analytics, procurement, and HR. The approach also sidesteps sovereign data hurdles. Cloud models remain attractive, holding 46% telecom ERP market share in 2025, but pure-play cloud growth trails hybrid because mission-critical workloads still demand local control. The telecom ERP market size for hybrid solutions is expected to widen further as latency-sensitive edge applications proliferate.

Freedom Mobile's cloud migration proved that a hybrid design can deliver 99.99% availability and 35% IT Opex savings. Similar blueprints are now deployed by Vodafone, Orange, and operators across the Gulf states. In China and Russia, strict data-residency clauses hold back public-cloud adoption, yet regulators signal eventual relaxation, which will funnel pent-up demand toward hybrid over the forecast window.

Software licenses generated 55% revenue in 2025, but services, from consulting to managed operations, are scaling faster at 17.8% CAGR. The telecom ERP market for services is expanding as carriers outsource scarce skills in data migration, AI model tuning, and API governance. Ericsson's SAP program saved 30% not on licensing but on automated migration, underscoring where value accrues.

System integrators such as IBM, Accenture, and Amdocs are packaging fixed-price bundles that guarantee cut-over timelines, a proposition resonating with CFOs fatigued by open-ended IT budgets. As AI modules permeate network management, demand for data-scientist-as-a-service further tilts wallet share toward services. Consequently, the telecom ERP market share of services is projected to expand steadily, even as software retains its foundational role.

Geography Analysis

Asia-Pacific held 34% revenue in 2025, fueled by India's rapid 5G monetization and China's multi-billion-dollar virtualization programs. Reliance Jio's ERP-driven 30% OpEx drop spurred Bharti Airtel and Vodafone Idea to initiate similar projects. Japan and South Korea, having modernized during 4G cycles, now focus on AI overlay modules that optimize spectrum, subtly shifting wallet share from core finance to network analytics. As local regulators ease cross-border data hurdles, hybrid ERP adoption will keep pace with rising edge-compute traffic.

The Middle East is the fastest-growing region, with a 13.6% CAGR. Saudi Arabia's Vision 2030 mandates and the United Arab Emirates' smart-city agendas require real-time billing, IoT integration, and elastic provisioning. STC and Etisalat pivoted to cloud-native ERP to secure those capabilities, and the Gulf Cooperation Council's efforts to harmonize data laws further accelerate momentum. Turkey and Israel follow suit, leveraging ERP modernization to differentiate enterprise service portfolios in a crowded mobile landscape.

North America and Europe remain sizable but mature. AT&T's USD 14 billion network plan and Verizon's spectrum investments allocate meaningful funds to ERP for procurement and inventory automation. In Europe, GDPR compels real-time revenue assurance, nudging operators toward ERP suites with embedded compliance workflows. Growth therefore tilts toward module-level upgrades rather than greenfield replacements. South America and Africa progress more slowly, yet SaaS models that offer pay-as-you-grow pricing begin to unlock latent demand among cash-strapped carriers.

- SAP SE

- Oracle Corporation

- Microsoft Corporation

- International Business Machines Corporation

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- TEOCO Corporation

- Amdocs Limited

- CSG Systems International Inc.

- The Sage Group plc

- Infor Inc.

- Comarch S.A.

- Tecnotree Corporation

- Oracle NetSuite LLC

- SYSPRO (Pty) Ltd.

- Epicor Software Corporation

- IFS AB

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- FPT Software Company Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition * Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Networks Among CSPs

- 4.2.2 Push Toward Operational Expenditure Reduction Via Automation

- 4.2.3 Rising Adoption of Cloud-Native BSS/OSS Stacks in Tier-1 Operators

- 4.2.4 Integration of AI-Driven Predictive Analytics Within ERP Suites

- 4.2.5 Regulatory Mandates for Real-Time Revenue Assurance and Auditability

- 4.2.6 Growing Demand for End-to-End Network Visibility Across Multi-Vendor Environments

- 4.3 Market Restraints

- 4.3.1 High Upfront Licensing Costs for Tier-3 Operators

- 4.3.2 Data Migration Complexities From Legacy OSS/BSS

- 4.3.3 Scarcity of Telecom-Specific ERP Implementation Talent

- 4.3.4 Concerns Over Data Sovereignty in Cross-Border Cloud Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Threat of Substitutes

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Bargaining Power of Suppliers

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Small and Medium Telecom Operators

- 5.3.2 Large Telecom Operators

- 5.4 By Function

- 5.4.1 Finance and Accounting

- 5.4.2 Human Resources

- 5.4.3 Supply Chain and Procurement

- 5.4.4 Customer Relationship Management

- 5.4.5 Network Management

- 5.4.6 Inventory Management

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 Microsoft Corporation

- 6.4.4 International Business Machines Corporation

- 6.4.5 Telefonaktiebolaget LM Ericsson

- 6.4.6 Nokia Corporation

- 6.4.7 TEOCO Corporation

- 6.4.8 Amdocs Limited

- 6.4.9 CSG Systems International Inc.

- 6.4.10 The Sage Group plc

- 6.4.11 Infor Inc.

- 6.4.12 Comarch S.A.

- 6.4.13 Tecnotree Corporation

- 6.4.14 Oracle NetSuite LLC

- 6.4.15 SYSPRO (Pty) Ltd.

- 6.4.16 Epicor Software Corporation

- 6.4.17 IFS AB

- 6.4.18 Huawei Technologies Co., Ltd.

- 6.4.19 ZTE Corporation

- 6.4.20 FPT Software Company Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

(주말 및 공휴일 제외)