|

시장보고서

상품코드

2065575

GitOps 및 IaC 소프트웨어 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)GitOps And Infrastructure As-a-Code (IaC) Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

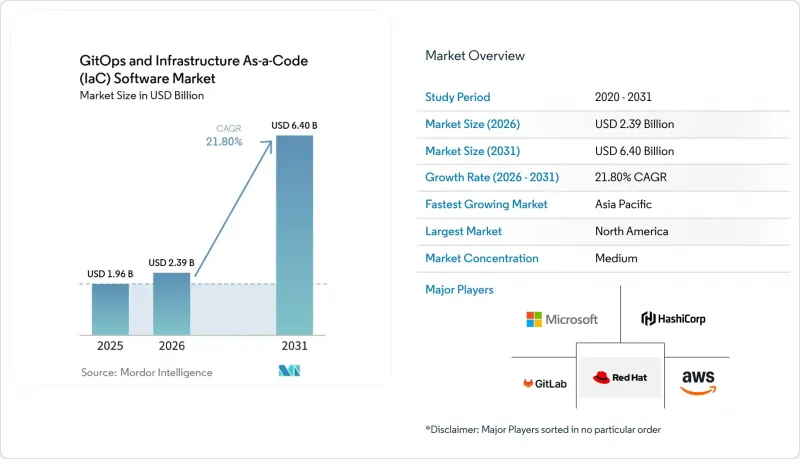

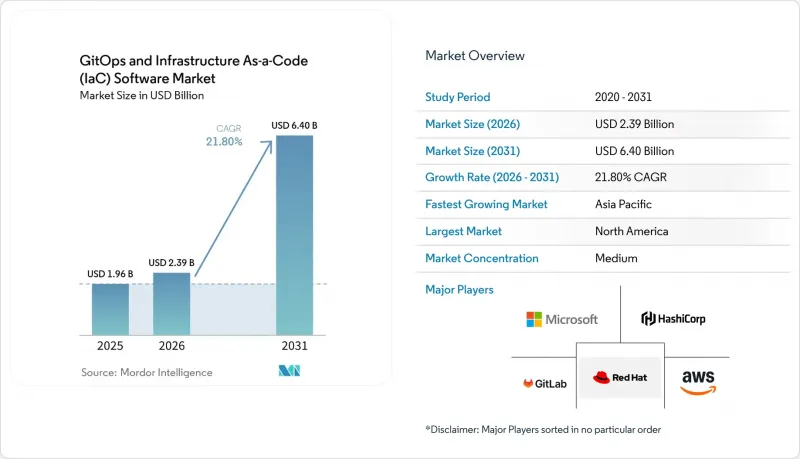

Mordor Intelligence에 의하면, GitOps 및 IaC 소프트웨어 시장 규모는 2025년 19억 6,000만 달러로 평가되었고, 2026년에는 23억 9,000만 달러로 추정되고, 2031년까지 64억 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 21.8%로 성장할 전망입니다.

본 보고서는 배포 모델별(SaaS, 자체 호스팅 등), 조직 규모별(중소기업, 대기업), 최종 사용자 산업별(IT 및 통신, 헬스케어 및 생명과학, 제조 등), 클라우드 환경별(퍼블릭 클라우드, 프라이빗 클라우드), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 GitOps 및 IaC 소프트웨어 시장 동향 및 인사이트

기업 내 클라우드 네이티브 도입

2025년까지 클라우드 네이티브 조직의 82%가 프로덕션 환경에서 쿠버네티스를 도입하게 되었으며, GitOps는 컨테이너화된 워크로드를 제공하는 사실상의 메커니즘으로서 입지를 확고히 했습니다. 금융기관은 이러한 변화를 상징하고 있습니다. 모건 스탠리는 500개 이상의 클러스터에서 Flux를 운영하며, GitOps를 핵심 거래 인프라에 직접 통합하고 있습니다. 통신 업계에서는 NTT 도코모가 AWS 상에서 GitOps와 AI 기반 자동화를 결합함으로써 5G 코어 구축 시간을 80% 단축했습니다. ArgoCD와 Flux가 CNCF에서 졸업함에 따라, 철저한 보안 감사와 확장성 테스트를 통해 엔터프라이즈급 신뢰성이 확립되었습니다. 그 결과, ArgoCD 사용자의 97%가 현재 이 도구를 프로덕션 환경에서 운영 중이며, 42%는 인스턴스당 500개 이상의 용도를 관리하고 있습니다.

DevSecOps 파이프라인으로의 전환

규제 대상 기업들은 보안 점검을 선언형 파이프라인에 통합하여 수동 검토 주기를 단축하고 있습니다. Pulumi의 2025년 12월 릴리스에서는 Terraform 및 OpenTofu용 통합 상태 관리 기능이 추가되어, ‘정책-as-코드’를 일원적으로 적용할 수 있게 되었습니다. GitLab 버전 18.7에서는 시크릿 유효성 검사 기능이 도입되어, 배포 전에 유효 기간이 만료된 인증 정보를 감지할 수 있게 되었습니다. 유럽의 은행들은 DORA 요건을 충족하기 위해 도입을 가속화하고 있으며, 인테사 산파올로는 시스코의 GitOps 지원 패브릭 컨트롤러를 활용해 감사 준비 시간을 70% 단축했다고 보고했습니다. PCI-DSS 자동화 청사진이 등장하면서, 결제 카드에 관한 통제 체계가 불변의 인프라로 체계화되었습니다. 많은 팀이 수동 방식의 키 로테이션에 의존하고 있기 때문에 시크릿 관리는 여전히 뒤처져 있으며, 통합된 저장소 솔루션의 필요성이 부각되고 있습니다.

Git을 중심으로 한 워크플로우에서의 기술 격차

2024년 영국 태스크포스가 실시한 조사에 따르면, 중소기업의 41%가 DevOps를 ‘너무 복잡하다’고 인식하고 있으며, 35%는 적절한 인력이 부족하다는 사실이 밝혀졌습니다. 이미 GitOps를 도입한 조직조차 어려움을 겪고 있습니다. 2025년 7월 CNCF 설문조사에 따르면, 환경 관리가 운영상의 가장 큰 과제로 대두되었으며, 많은 팀이 임시방편적인 워크플로를 스크립트로 작성하고 있습니다. 2025년 11월에 출시된 EKS 기반 관리형 ArgoCD는 설치 및 업그레이드에 드는 수고를 줄여주고, 중소기업의 기술 격차를 해소합니다. 플랫폼 엔지니어링 팀은 Git의 개념을 숨긴 셀프 서비스형 배포 포털을 제공함으로써 마찰을 더욱 줄이고 있지만, 이러한 접근 방식에는 전담 엔지니어와 초기 투자가 필요합니다. 현재 대학에서는 Kubernetes와 GitOps를 교육 과정에 도입하기 시작했으며, 향후 2-3년 내에 이러한 제약이 완화될 것으로 예측됩니다.

부문별 분석

하이브리드형 패턴은 SaaS의 민첩성과 온프레미스 환경에서의 제어라는 두 가지 요구 사항을 모두 충족합니다. 2025년 매출의 46.2%를 이 솔루션이 차지한 것으로 보아, GitOps 컨트롤러를 정책 엔진으로 통합한 통합 툴체인이 선호되고 있음을 알 수 있습니다. 규제 대상 조직들이 기밀 데이터를 보호하기 위해 에어갭이 적용된 가상 사설 클라우드 내에서 실행 에이전트를 가동하는 동시에 SaaS 제어 플레인을 도입하고 있기 때문에 하이브리드 부문은 연평균 성장률(CAGR) 24.2%를 기록하며 순수 SaaS를 능가할 것으로 예측됩니다. Spacelift의 FedRAMP 인증과 AWS의 관리형 ArgoCD 애드온은 벤더가 이 아키텍처를 제품화한 대표적인 사례입니다. 대형 은행들은 여전히 제로 트러스트 요건을 충족하기 위해 자체 호스팅 방식의 컨트롤 플레인을 선호하고 있지만, 운영 비용 증가로 인해 업그레이드나 패치 적용을 외부에 위탁하는 부분 호스팅 방식의 대시보드로 점차 전환하고 있습니다. 하이브리드 환경을 위한 GitOps 및 IaC 소프트웨어 시장 규모는 국내 처리를 의무화하면서도 중앙 집중식 관리를 허용하는 기밀 컴퓨팅의 동향과 연동되어 확대될 것으로 예측됩니다.

2세대 플랫폼에는 규정 준수 팩, 드리프트 감지, ‘정책-as-코드’ 템플릿이 번들로 제공되어 항공우주 및 방위 분야 계약업체들에게 매력적인 선택지가 되고 있습니다. 공공 부문에서는 조달 규정에 따라 SaaS 공급업체가 프라이빗 실행 모드를 지원한다는 증명을 요구하는 사례가 늘어나고 있으며, 이것이 하이브리드형에 대한 수요를 뒷받침하고 있습니다. 제조업 전반에 걸쳐, Flux를 실행하는 엣지 클러스터는 설치 공간이 작은 에이전트의 이점을 누리면서도 여전히 중앙 정책 허브에 연결되어 있어, 엔드포인트에 의존하지 않는 제어 플레인이 필수적임을 입증하고 있습니다. 그 결과, GitOps 및 Infrastructure as Code 소프트웨어 시장은 과거에 엄격했던 도입 범주 간의 경계를 점점 더 모호하게 만들고 있으며, 도입 장소가 아닌 유연성이 주요 구매 기준이 되고 있습니다.

2025년 매출에서 퍼블릭 클라우드 도입이 차지하는 비중은 71.8%를 나타낼 것으로 예측되며, 연평균 성장률(CAGR) 23.6%로 확대될 것으로 전망됩니다. 네이티브 통합이 그 기세를 뒷받침하고 있습니다. AWS는 원클릭으로 도입할 수 있는 ArgoCD 애드온을 제공하며, Azure는 Flux를 AKS에 번들로 제공하고, Google은 Anthos Config Management를 제공합니다. 프라이빗 클라우드는 금융 및 의료 분야에서 여전히 중요한 위치를 차지하고 있으며, 데이터 상주성 요건으로 인해 워크로드는 사내 호스팅형 OpenShift 클러스터로 이전되고 있습니다. 하이브리드 제어 플레인은 현재 두 환경을 연결하는 역할을 수행하고 있으며, Alibaba Cloud의 ACK One은 퍼블릭 클라우드 리소스와 동일한 GitOps 워크플로우 내에서 온프레미스 클러스터를 오케스트레이션하고 있습니다.

Flux의 마이크로컨트롤러 아키텍처는 리소스가 제한적인 엣지 노드에 적합하며, 온프레미스 배포 환경에서의 GitOps 및 IaC 소프트웨어 시장 점유율이 사라지는 것이 아니라 엣지·소버린 클라우드 프로젝트로 재편될 것임을 시사합니다. Cross-plane은 멀티 클라우드 환경을 사용자 정의 Kubernetes 리소스로 관리함으로써, 제공업체별 IaC 스크립트를 작성할 때 발생하는 오버헤드를 줄여줍니다. 퍼블릭 클라우드가 관리형 GitOps를 대중화함에 따라, 차별화의 초점은 규정 준수 기능, 지연 시간에 민감한 엣지 지원, AI를 활용한 롤아웃 전략으로 이동하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 매출의 33.6%를 차지했습니다. 이는 하이퍼스케일 클라우드의 보급과 은행 및 의료 업계의 엄격한 DevSecOps 요구 사항에 힘입은 결과입니다. Spacelift와 같은 FedRAMP 인증을 받은 SaaS 플랫폼이 연방 정부 기관에서의 도입을 확대함에 따라, Harness는 2025년 12월에 조달한 2억 4,000만 달러의 자금을 활용해 포춘 500대 기업을 대상으로 한 시장 진출을 가속화했습니다. Morgan Stanley나 Capital One과 같은 초기 도입 기업들은 현재 GitOps를 핵심 인프라로 자리매김하고 있으며, 엔터프라이즈 수준에서의 성숙도가 입증되었습니다. 캐나다에서는 미국과 유사한 추세가 나타나는 반면, 멕시코의 통신 사업자들은 5G 구축을 위해 GitOps를 시범 운영 중입니다.

아시아태평양은 가장 빠르게 성장하는 지역으로, 연평균 성장률(CAGR)은 25.8%로 전망됩니다. 일본의 도쿄가스는 하이브리드 워크로드를 위해 ArgoCD와 서비스 메시를 결합함으로써 30%의 비용 절감을 실현했습니다. 중국의 국영 기업들은 데이터 현지화법을 준수하기 위해 소버린 클라우드에 Flux를 도입하고 있으며, 알리바바 클라우드는 멀티 클러스터 환경을 관리하기 위해 ACK One에 GitOps를 통합하고 있습니다. 인도의 핀테크 업계는 멀티 클라우드 차익 거래를 활용하여 비용 효율성을 높이기 위해 AWS와 Azure 간에 워크로드를 이전하고 있습니다. 호주 및 뉴질랜드에서는 은행 업계와 정부의 디지털화 프로젝트에서 GitOps 도입이 빠르게 진행되고 있습니다.

유럽에서는 규제 준수를 원동력으로 삼아 견조한 성장세를 보이고 있습니다. 예를 들어, 인테사 산파올로는 ‘디지털 운영 복원력법(DORA)’을 준수하는 자동화 시스템을 도입함으로써 감사 시간을 70% 단축하는 데 성공했습니다. 이러한 성공 사례를 계기로 독일과 프랑스의 다른 금융기관들 사이에서도 유사한 전략을 채택하는 움직임이 확산되고 있습니다. 중동 및 아프리카·남미는 큰 잠재력을 지닌 신흥 시장입니다. 하이퍼스케일 클라우드 제공업체들이 현지 데이터센터를 설립함에 따라, 이러한 지역에 대한 관심이 높아지고 있습니다. 이러한 데이터센터의 존재는 지연 시간을 줄일 뿐만 아니라, 규정 준수 관련 과제도 해결하여 기업이 현지 규제 체계 내에서 보다 효과적으로 사업을 전개할 수 있도록 해줍니다. 이러한 추세는 첨단 기술의 추가 도입을 촉진하고, 해당 지역의 성장을 뒷받침할 것으로 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the gitOps and Infrastructure as Code software market size is expected to increase from USD 1.96 billion in 2025 to USD 2.39 billion in 2026 and reach USD 6.40 billion by 2031, growing at a CAGR of 21.8% over 2026-2031.

This report is Segmented by Deployment Model (SaaS, Self-Hosted, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecommunications, Healthcare and Life Sciences, Manufacturing, and More), Cloud Environment (Public Cloud, and Private Cloud), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GitOps And Infrastructure As-a-Code (IaC) Software Market Trends and Insights

Cloud-Native Adoption by Enterprises

Kubernetes reached production adoption in 82% of cloud-native organizations by 2025, anchoring GitOps as the de facto delivery mechanism for containerized workloads. Financial institutions exemplify this shift: Morgan Stanley runs Flux across more than 500 clusters, embedding GitOps directly into core trading infrastructure. In telecommunications, NTT DOCOMO cut 5G core build time by 80% by pairing GitOps with AI-driven automation on AWS. Graduation of ArgoCD and Flux from the CNCF imparted enterprise-grade trust through extensive security audits and scalability tests. Consequently, 97% of ArgoCD users now operate the tool in production, and 42% manage more than 500 applications per instance.

Shift Toward DevSecOps Pipelines

Regulated enterprises are moving security checks inside declarative pipelines, reducing manual review cycles. Pulumi's December 2025 release added unified state management for Terraform and OpenTofu, enabling consolidated policy-as-code enforcement. GitLab version 18.7 introduced secret validity scanning, detecting expired credentials before deployment. European banks accelerated adoption to satisfy DORA requirements, with Intesa Sanpaolo reporting a 70% cut in audit prep time using Cisco's GitOps-backed fabric controller. PCI-DSS automation blueprints have emerged, codifying payment-card controls as immutable infrastructure. Secrets management still lags because many teams rely on manual key rotation, highlighting the need for integrated vault solutions.

Skills Gap in Git-Centric Workflows

A 2024 U.K. task-force survey showed 41% of SMEs deem DevOps too complex and 35% lack adequate talent.Even organizations already using GitOps struggle: environment promotion emerged as the top operational headache in the July 2025 CNCF survey, with many teams scripting ad-hoc workflows. Managed ArgoCD on EKS, launched November 2025, cuts installation and upgrade toil, narrowing the skill gap for SMEs. Platform engineering teams further reduce friction by exposing self-service deployment portals that hide Git concepts, though this approach demands dedicated engineers and initial investment. Universities are now embedding Kubernetes and GitOps into curricula, suggesting the constraint will ease over the next two to three years.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Multi-Cloud and Hybrid-Cloud Strategies

- Growing Compliance Automation Needs in Regulated Industries

- Security Concerns Over Pipeline Secrets Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hybrid patterns address the dual need for SaaS agility and on-premises control. Solutions captured 46.2% of 2025 revenue, illustrating a preference for integrated toolchains that wrap GitOps controllers with policy engines. The hybrid segment is forecast to register a 24.2% CAGR, outpacing pure SaaS, as regulated entities deploy SaaS control planes while running execution agents inside air-gapped virtual private clouds to protect classified data. FedRAMP clearance for Spacelift and the managed ArgoCD add-on from AWS exemplify how vendors are productizing this architecture. Large banks still favor self-hosted control planes to meet zero-trust mandates, but rising operating costs steer them toward partially hosted dashboards that offload upgrades and patches. The GitOps and Infrastructure as Code software market size for hybrid deployments is projected to expand in tandem with confidential computing trends that mandate in-country processing while permitting centralized governance.

Second-generation platforms now bundle compliance packs, drift detection, and policy-as-code templates, making them appealing to aerospace and defense contractors. In the public sector, procurement rules increasingly require proof that SaaS providers support privatized execution modes, propelling hybrid demand. Across manufacturing, edge clusters running Flux benefit from thin-footprint agents but still connect to central policy hubs, confirming that an endpoint-agnostic control plane is crucial. As a result, the GitOps and Infrastructure as Code software market continues to blur the once-rigid lines between deployment categories, leaving flexibility, not location, as the prime buying criterion.

Public cloud deployments represented 71.8% of 2025 revenue and are forecast to progress at a 23.6% CAGR. Native integrations drive momentum: AWS offers a one-click ArgoCD add-on, Azure bundles Flux into AKS, and Google ships Anthos Config Management. Private clouds remain prominent in finance and healthcare, where data residency pushes workloads onto self-hosted OpenShift clusters. Hybrid control planes now straddle both worlds, with Alibaba Cloud's ACK One orchestrating on-premises clusters in the same GitOps workflow as public cloud resources.

Flux's microcontroller architecture suits resource-constrained edge nodes, signaling that the GitOps and Infrastructure as Code software market share for on-premises deployments will not evaporate but will reposition toward edge and sovereign-cloud projects. Cross-plane reconciles multi-cloud state as custom Kubernetes resources, trimming the overhead of writing provider-specific IaC scripts. As public clouds commoditize managed GitOps, differentiation shifts to compliance features, latency-sensitive edge support, and AI-assisted rollout strategies.

Geography Analysis

North America controlled 33.6% of global revenue in 2025, buoyed by hyperscale cloud penetration and stringent DevSecOps mandates across banking and healthcare. FedRAMP-cleared SaaS platforms such as Spacelift widened federal uptake, and Harness leveraged its December 2025 USD 240 million funding to accelerate go-to-market across Fortune 500 accounts. Early adopters like Morgan Stanley and Capital One now treat GitOps as core infrastructure, validating enterprise maturity. Canada mirrors U.S. trends, while Mexican telecoms pilot GitOps for 5G roll-outs.

Asia-Pacific is the fastest-growing region, projected at a 25.8% CAGR. Japan's Tokyo Gas achieved a 30% cost reduction by combining ArgoCD with service mesh for hybrid workloads. Chinese state-owned enterprises deploy Flux in sovereign clouds to honor data localization laws, and Alibaba Cloud embeds GitOps in ACK One to manage multi-cluster estates. India's fintech community capitalizes on multi-cloud arbitrage, shifting workloads between AWS and Azure for pricing efficiency. Australia and New Zealand exhibit strong uptake in banking and government digitization projects.

Europe demonstrates robust growth driven by regulatory compliance. For instance, Intesa Sanpaolo achieved a 70% reduction in audit times by implementing automation aligned with the Digital Operational Resilience Act (DORA). This success is motivating other financial institutions across Germany and France to adopt similar strategies. The Middle East and Africa, along with South America, are emerging markets showing significant potential. These regions are witnessing growing interest as hyperscale cloud providers establish local data centers. The presence of these data centers not only reduces latency but also addresses compliance challenges, enabling businesses to operate more effectively within local regulatory frameworks. This development is expected to drive further adoption of advanced technologies and foster growth in these regions.

- HashiCorp Inc

- GitLab Inc

- Weaveworks Limited

- Red Hat Inc

- Amazon Web Services Inc

- Microsoft Corporation

- Google LLC

- Perforce Software Inc Puppet

- Chef Software Inc

- CloudBees Inc

- Circle Internet Services Inc

- Atlassian Corporation Plc

- GitHub Inc

- SUSE LLC

- Mirantis Inc

- Pulumi Corporation

- Spacelift Inc

- Harness Inc

- Humanitec GmbH

- JFrog Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native adoption by enterprises

- 4.2.2 Shift toward DevSecOps pipelines

- 4.2.3 Rise of multi-cloud and hybrid-cloud strategies

- 4.2.4 Growing compliance automation needs in regulated industries

- 4.2.5 Open-source community acceleration around GitOps controllers

- 4.2.6 Demand for immutable infrastructure in edge computing

- 4.3 Market Restraints

- 4.3.1 Skills gap in Git-centric workflows

- 4.3.2 Security concerns over pipeline secrets management

- 4.3.3 Toolchain fragmentation and interoperability issues

- 4.3.4 Limited ROI visibility for large legacy environments

- 4.4 Industry Value Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porters Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 SaaS

- 5.1.2 Self Hosted

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises SMEs

- 5.2.2 Large Enterprises

- 5.3 By End User Industry

- 5.3.1 IT and Telecommunications

- 5.3.2 Banking Financial Services and Insurance BFSI

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Retail and E Commerce

- 5.3.5 Manufacturing

- 5.3.6 Government and Public Sector

- 5.3.7 Other End User Industries

- 5.4 By Cloud Environment

- 5.4.1 Public Cloud

- 5.4.2 Private Cloud

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Nigeria

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles includes Global Level Overview Market Level Overview Core Segments Financials as available Strategic Information Market Rank Share Products and Services Recent Developments

- 6.4.1 HashiCorp Inc

- 6.4.2 GitLab Inc

- 6.4.3 Weaveworks Limited

- 6.4.4 Red Hat Inc

- 6.4.5 Amazon Web Services Inc

- 6.4.6 Microsoft Corporation

- 6.4.7 Google LLC

- 6.4.8 Perforce Software Inc Puppet

- 6.4.9 Chef Software Inc

- 6.4.10 CloudBees Inc

- 6.4.11 Circle Internet Services Inc

- 6.4.12 Atlassian Corporation Plc

- 6.4.13 GitHub Inc

- 6.4.14 SUSE LLC

- 6.4.15 Mirantis Inc

- 6.4.16 Pulumi Corporation

- 6.4.17 Spacelift Inc

- 6.4.18 Harness Inc

- 6.4.19 Humanitec GmbH

- 6.4.20 JFrog Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White Space and Unmet Need Assessment