|

시장보고서

상품코드

2065578

미국의 욕창 예방 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Pressure Ulcer Prevention - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

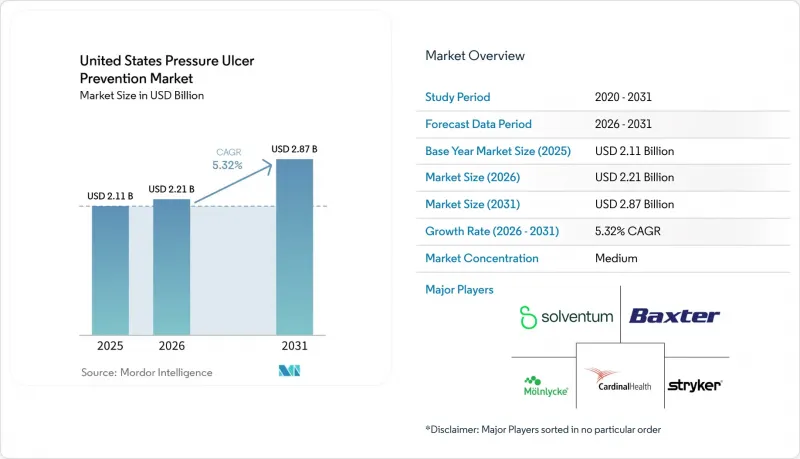

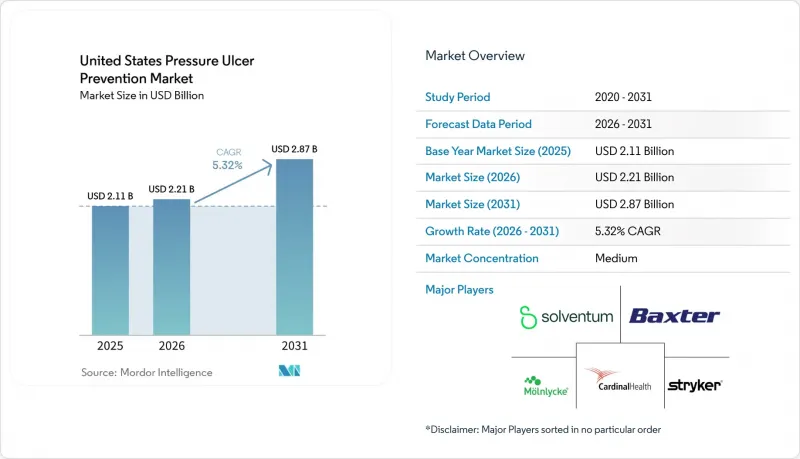

Mordor Intelligence에 의하면, 미국의 욕창 예방 시장 규모는 2025년 21억 1,000만 달러로 평가되었고, 2026년에는 22억 1,000만 달러로 추정되고, 2031년까지 28억 7,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 5.32%로 성장할 전망입니다.

본 보고서는 제품 유형별(지지대, 예방용 드레싱, 체위 유지 및 보호구, 피부 보호 제품, 감지 및 모니터링 기술) 및 최종 사용자별(병원·외래수술센터(ASC), 진료소, 장기 요양 및 응급 치료 센터, 재택 요양 시설)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 욕창 예방 시장 동향 및 인사이트

고령화, 운동에 제한이 있는 환자, 중증 환자군

고령화는 욕창 예방 시장에 있어 여전히 가장 지속적인 수요 기반입니다. 이는 고령자가 움직이지 못하는 상태나 허약한 상태에 빠지기 쉬우며, 입원 기간이 길어지는 경향이 있기 때문입니다. 2025년 시점에서 베이비붐 세대는 61세에서 79세 사이의 연령대에 해당합니다. 즉, 미국에서는 병원, 장기 요양 시설, 재택 환경을 불문하고 욕창 위험에 노출되기 쉬운 대규모 환자 집단이 계속해서 존재하게 될 것입니다. 이러한 인구 동향의 변화가 중요한 이유는 예방에 드는 비용이 환자 수뿐만 아니라 고위험 입원 환자 1인당 필요한 치료의 중증도나 기간에 따라서도 증가하기 때문입니다. 또한 고령 환자 중 비만, 심혈관 질환 및 기타 동반 질환을 함께 앓는 사례가 증가하고 있으며, 비만 환자에게 적합한 침구와 더욱 우수한 습기 관리가 요구됨에 따라 제품의 가격대도 상승하고 있습니다. 이러한 추세로 인해, 욕창 예방 시장의 수익 기반은 단순한 병상 이용률 증가가 시사하는 것보다 훨씬 광범위해지고 있습니다.

HAPI(의료 품질 평가 프로그램)에 따른 비용 및 의료 품질 관련 제재

병원 내 욕창은 비용 관리, 간호 품질, 그리고 평판 위험에 동시에 영향을 미치기 때문에 현재 경영진의 의사결정 과정에서 더욱 중요한 위치를 차지하고 있습니다. 의료 기관들이 표준화가 가능하고 추적 가능하며, 품질 심사 시 정당성을 설명할 수 있는 예방 프로토콜을 더욱 중시하게 되면서, 욕창 예방 시장은 이러한 변화의 혜택을 누리고 있습니다. 클리블랜드 클리닉은 체계적인 다직종 협력을 통한 예방 프로토콜을 도입한 후, 2024-2025년 병원 내 욕창 발생률이 36% 감소했다고 보고했습니다. 이는 운영상의 이점이 명확하다면, 병원이 체계적인 예방 조치를 확대하려는 의지가 있음을 보여줍니다. 또한, 의료기관 측에서는 보다 상세한 입원 기록과 환자의 입원 기간 동안 이루어진 예방 활동에 대한 명확한 증거가 요구되고 있기 때문에 문서화 기준도 점점 더 중요해지고 있습니다. 이에 따라 조기 평가, 일관된 간호 서비스 제공, 간호팀 전체에 걸친 감사 가능한 기록 관리를 지원하는 제품과 워크플로우의 매력이 높아지고 있습니다.

고급 욕창 예방용 매트리스의 높은 도입 및 교체 비용

높은 도입 비용과 교체 비용으로 인해, 욕창 예방 시장이 소규모 병원이나 요양 시설에 더욱 깊이 확산되는 속도가 여전히 제한되고 있습니다. 고도의 교대 가압 시스템이나 공기 누출을 최소화하는 시스템은 더 뛰어난 임상 성능을 제공하지만, 유지보수, 교체용 커버, 펌프, 그리고 직원의 숙련도 향상에 따른 지속적인 비용도 수반됩니다. 렌탈 모델은 초기 구매 장벽을 낮추지만, 한편으로는 제3자에 대한 의존성을 야기하여 케어 네트워크 전체의 표준화를 지연시킬 가능성도 있습니다. 이러한 격차는 예방 예산이 인건비나 기타 필수 경비와 직접적으로 경쟁하는 지방 병원이나 소규모 요양 시설에서 가장 두드러집니다. 그 결과, 대규모 의료 시스템은 장비를 신속하게 교체하는 반면, 소규모 시설은 구형이거나 사양이 낮은 욕창 예방용 매트리스를 계속 사용하는 등, 양극화된 욕창 예방 시장이 형성되고 있습니다.

부문별 분석

2025년, 지지용 제품은 매출의 62.87%를 차지했으며, 욕창 예방 시장에서 가장 큰 점유율을 기록했습니다. 이는 중환자 치료나 수술 전후 관리 현장에서 여전히 능동적인 체중 재분배가 핵심적인 예방책으로 활용되고 있기 때문입니다. 이러한 높은 점유율은 중환자실(ICU)이나 스텝다운 병동, 중증도가 높은 환자들이 기본적인 지원 측면에서는 일관되게 제공받기 어려운 지속적인 지원이 필요한 경우가 많다는 사실을 반영하고 있습니다. 교대 송풍식, 저공기손실식, 횡방향 회전식 플랫폼 등의 동적 시스템은 위험이 가장 높고 최고 수준의 모니터링이 필요한 환자에게 사용되기 때문에 여전히 시장 가치의 상당 부분을 차지하고 있습니다. Arjo사는 급성기 의료의 모든 상황에서 표준 치료와 비만 환자 치료의 요구를 모두 충족시키는 ‘AtmosAir Velaris’ 및 ‘Auralis’와 같은 플랫폼을 통해, 욕창 예방 시장의 이 분야에서 계속해서 확고한 입지를 다지고 있습니다. 정적 폼, 젤 오버레이, 하이브리드형 반응성 제품은 예산 제약이 심하고, 완전한 동적 기능보다 제품의 간편성이 중시되는 장기 요양 및 재택 간호 현장에서 여전히 중요한 역할을 하고 있습니다.

피부 보호 제품은 2031년까지 연평균 성장률(CAGR) 6.36%를 나타낼 것으로 예측되며, 욕창 예방 시장에서 가장 빠르게 성장하는 제품 카테고리로 자리매김하고 있습니다. 이러한 성장은 수술 전·후 관리, 외래 진료, 퇴원 계획 과정에서 장벽 필름, 자극이 없는 보호제, 예방적 피부 관리가 더욱 널리 활용되고 있음을 반영합니다. 피부 보호 제품의 욕창 예방 시장 규모가 확대되고 있는 이유는 이러한 제품들이 표준화되기 쉽고, 급성기 이외의 유통 채널로 유통하기 쉬우며, 간병인이 임상 시설 밖에서도 사용하기 편리하기 때문입니다. 또한, 마찰 및 전단력 감소와 관련된 더욱 강력한 근거가 프로토콜의 광범위한 채택을 뒷받침하고 있기 때문에 예방용 드레싱의 기술 혁신도 이 부문을 지탱하고 있습니다. 감지 및 모니터링 기술은 현재로서는 여전히 가장 규모가 작은 분야이지만, 의료 제공업체들이 위험을 조기에 파악하고 업무 흐름 기록을 개선하기를 원함에 따라 의료 기관들의 관심이 높아지고 있습니다. 또한 Bruin Biometrics사는 자사의 ‘Provizio SEM 스캐너’가 상용화 이후 100만 건 이상의 환자 스캔을 달성했으며, 보고 대상인 욕창을 약 5만 건 예방한 것으로 추정된다고 밝혔습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the united states pressure ulcer prevention market size is expected to increase from USD 2.11 billion in 2025 to USD 2.21 billion in 2026 and reach USD 2.87 billion by 2031, growing at a CAGR of 5.32% over 2026-2031.

This report is Segmented by Product Type (Support Surfaces, Prophylactic Dressings, Positioners & Protectors, Skin Protection Products, Detection & Monitoring Technologies), and End User (Hospitals & ASCs, Clinics, Long Term Care & Urgent Care Centers, Homecare Settings). The Market Forecasts are Provided in Terms of Value (USD).

United States Pressure Ulcer Prevention Market Trends and Insights

Aging, Immobile, and Critically Ill Patient Base

The aging population remains the most durable demand base for the pressure ulcer prevention market because older adults are more likely to experience immobility, frailty, and longer inpatient stays. Baby boomers were in the 61 to 79 age range in 2025, which means the United States continues to carry a large cohort of patients who are more exposed to pressure injury risk across hospitals, long-term care sites, and home settings. That demographic shift matters because prevention spending rises not only with patient numbers, but also with the severity and duration of care required for each high-risk admission. The product mix is also moving upward in value because older patients increasingly present with obesity, cardiovascular conditions, and other comorbidities that require bariatric-rated surfaces and better moisture control. This pattern gives the pressure ulcer prevention market a broader revenue base than simple bed occupancy growth would suggest.

HAPI Cost and Quality-Of-Care Penalties

Hospital-acquired pressure injuries now sit much closer to executive decision making because they affect cost control, care quality, and reputational risk at the same time. The pressure ulcer prevention market benefits from this shift because provider systems are putting more weight on prevention pathways that can be standardized, tracked, and defended during quality review. Cleveland Clinic reported a 36% reduction in hospital-acquired pressure injuries between 2024 and 2025 after implementing a systematic interprofessional prevention protocol, which shows that hospitals are willing to scale structured prevention when the operational case is clear. Documentation standards are also becoming more important because facilities need stronger admission records and clearer proof of prevention activity throughout the patient's stay. That increases the appeal of products and workflows that support early assessment, consistent care delivery, and auditable records across nursing teams.

High Capital and Replacement Cost of Advanced Surfaces

High acquisition and replacement costs continue to limit how quickly the pressure ulcer prevention market can move deeper into smaller hospitals and nursing facilities. Advanced alternating-pressure and low-air-loss systems offer better clinical capability, but they also bring ongoing costs tied to maintenance, replacement covers, pumps, and staff familiarization. Rental models reduce the first purchase hurdle, yet they can also create dependence on third parties and slow standardization across a care network. This gap is most visible in rural hospitals and smaller skilled nursing facilities where prevention budgets compete directly with labor needs and other essential expenses. The result is a two-speed pressure ulcer prevention market in which large health systems upgrade faster while smaller sites stay on older or lower-specification surfaces.

Other drivers and restraints analyzed in the detailed report include:

- Homecare and Post-Discharge Prevention Demand

- Better Support Surfaces and Prophylactic Dressings

- Variable Adherence to Turning and Skin-Assessment Protocols

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Support surfaces captured 62.87% of revenue in 2025, which gave them the largest share within the pressure ulcer prevention market because critical care and perioperative settings still rely on active redistribution as a core prevention measure. This high share reflects the fact that ICU, step-down, and higher-acuity patients often need continuous support that basic surfaces cannot provide consistently. Dynamic systems such as alternating-air, low-air-loss, and lateral rotation platforms continue to command a larger portion of value because they are used for patients with the greatest risk exposure and the highest level of monitoring. Arjo remains well placed in this part of the pressure ulcer prevention market through platforms such as AtmosAir Velaris and Auralis, which support both standard and bariatric care needs across acute settings. Static foam, gel overlays, and hybrid reactive formats remain important in long-term care and home settings where budget discipline is tighter, and product simplicity matters more than full dynamic capability.

Skin protection products are projected to grow at 6.36% CAGR through 2031, which makes them the fastest-growing product category within the pressure ulcer prevention market. That growth reflects wider use of barrier films, no-sting protectants, and preventive skin management in perioperative pathways, ambulatory care, and discharge planning. The pressure ulcer prevention market size for Skin Protection Products is rising because these items are easier to standardize, easier to distribute into non-acute channels, and easier for caregivers to use outside clinical facilities. Prophylactic dressing innovation also supports the category because stronger evidence around friction and shear reduction encourages broader protocol adoption. Detection and Monitoring Technologies remain the smallest segment today, but institutional interest is increasing as providers seek earlier risk visibility and better workflow documentation, and Bruin Biometrics reported that its Provizio SEM Scanner had exceeded 1 million patient scans since commercialization, with an estimated 50,000 reportable pressure injuries prevented.

List of Companies Covered in this Report:

- Agiliti Health, Inc.

- AliMed, Inc.

- Arjo AB

- Baxter

- Bruin Biometrics, LLC

- Cardinal Health

- Coloplast

- ConvaTec Group plc

- DeRoyal Industries

- EHOB, Inc.

- Invacare

- Joerns Healthcare

- LINET Group

- Medline Industries

- Molnlycke Health Care

- Smith+Nephew plc

- Solventum Corporation

- Stryker

- Talley Group

- Wellell

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Immobile, and Critically Ill Patient Base

- 4.2.2 HAPI Cost and Quality-Of-Care Penalties

- 4.2.3 Homecare and Post-Discharge Prevention Demand

- 4.2.4 Better Support Surfaces and Prophylactic Dressings

- 4.2.5 HH-PI eCQM and POA Documentation Pressure

- 4.2.6 Early Detection Workflows Using SEM and Thermal Imaging

- 4.3 Market Restraints

- 4.3.1 High Capital and Replacement Cost of Advanced Surfaces

- 4.3.2 Variable Adherence to Turning and Skin-Assessment Protocols

- 4.3.3 Device-Related Pressure Injury Complexity

- 4.3.4 Diagnostic Ambiguity Between POA Injury, Skin Failure, and HAPI

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Support Surfaces

- 5.1.1.1 Dynamic Support Surfaces

- 5.1.1.1.1 Alternating-air Mattresses

- 5.1.1.1.2 Low-air-loss Mattresses

- 5.1.1.1.3 Air-fluidized and High-air-loss Mattresses

- 5.1.1.1.4 Lateral Rotation and Microclimate-enabled Surfaces

- 5.1.1.2 Static Support Surfaces

- 5.1.1.2.1 Foam Mattresses

- 5.1.1.2.2 Gel Overlays

- 5.1.1.2.3 Static Air and Hybrid Reactive Overlays

- 5.1.1.1 Dynamic Support Surfaces

- 5.1.2 Prophylactic Dressings

- 5.1.2.1 Sacral Dressings

- 5.1.2.2 Heel Dressings

- 5.1.2.3 Anatomical Multi-site Dressings

- 5.1.3 Positioners & Protectors

- 5.1.3.1 Heel Off-loading Boots

- 5.1.3.2 Turn and Repositioning Aids

- 5.1.3.3 Wheelchair Cushions and Seat Positioners

- 5.1.4 Skin Protection Products

- 5.1.4.1 Barrier Creams

- 5.1.4.2 No-sting Barrier Films and Skin Protectants

- 5.1.5 Detection & Monitoring Technologies

- 5.1.5.1 SEM Scanners

- 5.1.5.2 Wearable Turn-compliance Sensors

- 5.1.5.3 Thermal and Imaging-based Assessment Tools

- 5.1.1 Support Surfaces

- 5.2 By End User

- 5.2.1 Hospitals & Ambulatory Surgery Centers

- 5.2.1.1 Intensive Care Units

- 5.2.1.2 Medical-Surgical and Step-down Units

- 5.2.1.3 Perioperative and PACU Settings

- 5.2.2 Clinics

- 5.2.2.1 Wound Care Centers

- 5.2.2.2 Outpatient Specialty Clinics

- 5.2.3 Long Term Care & Urgent Care Centers

- 5.2.3.1 Skilled Nursing Facilities

- 5.2.3.2 Nursing Homes and Assisted Living Facilities

- 5.2.3.3 Urgent Care Centers

- 5.2.4 Homecare Settings

- 5.2.4.1 Home Health Agencies

- 5.2.4.2 Hospice and Palliative Home Care

- 5.2.4.3 Caregiver-managed Home Use

- 5.2.1 Hospitals & Ambulatory Surgery Centers

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Agiliti Health, Inc.

- 6.3.2 AliMed, Inc.

- 6.3.3 Arjo AB

- 6.3.4 Baxter International Inc.

- 6.3.5 Bruin Biometrics, LLC

- 6.3.6 Cardinal Health, Inc.

- 6.3.7 Coloplast Corp.

- 6.3.8 ConvaTec Group plc

- 6.3.9 DeRoyal Industries, Inc.

- 6.3.10 EHOB, Inc.

- 6.3.11 Invacare Corporation

- 6.3.12 Joerns Healthcare LLC

- 6.3.13 LINET Group SE

- 6.3.14 Medline Industries, LP

- 6.3.15 Molnlycke Health Care AB

- 6.3.16 Smith+Nephew plc

- 6.3.17 Solventum Corporation

- 6.3.18 Stryker Corporation

- 6.3.19 Talley Group Limited

- 6.3.20 Wellell Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment