|

시장보고서

상품코드

2065597

미국의 피부과용 의약품 시장 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Dermatological Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

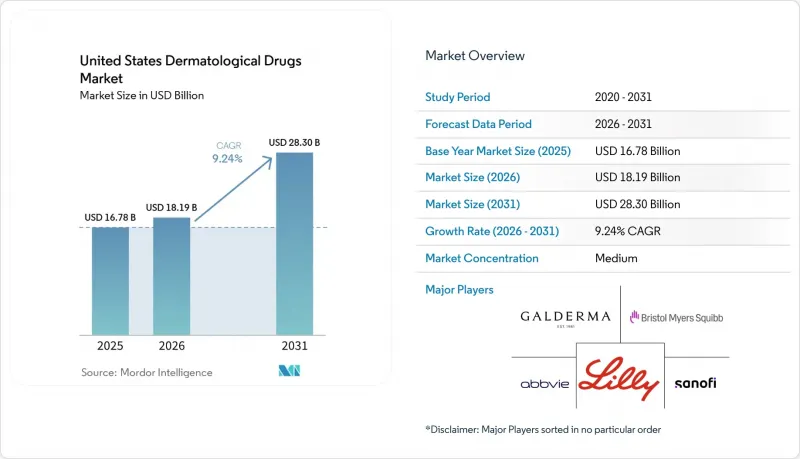

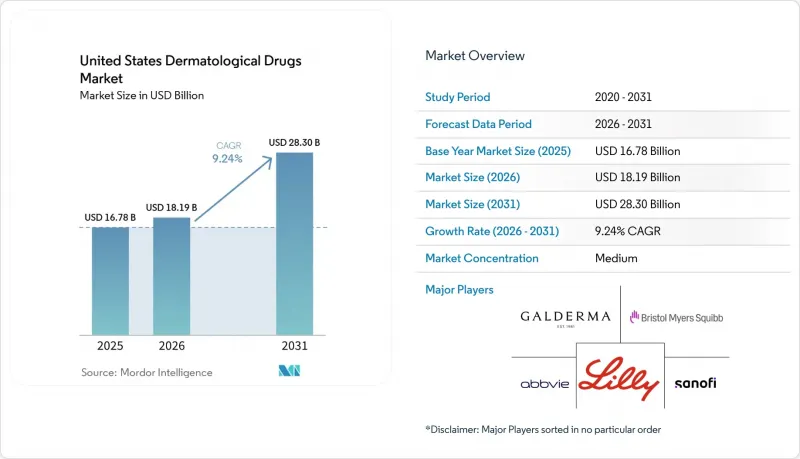

Mordor Intelligence에 의하면, 미국 피부과용 의약품 시장 규모는 2025년 167억 8,000만 달러에서 2026년에는 181억 9,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 9.24%로 성장을 지속하여, 2031년에는 283억 달러에 이를 것으로 예측됩니다.

본 보고서는 적응증(여드름, 건선, 아토피 피부염, 주사, 원형 탈모증, HS, 기타), 처방 현황(처방약, 일반의약품), 투여 경로(외용, 경구, 비경구), 약제 분류(코르티코스테로이드, 레티노이드, 항생제, PDE-4 억제제, JAK 억제제, 생물학적 제제, 기타), 유통 채널(병원, 소매, 온라인 약국)별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

미국 피부과용 의약품 시장 동향과 인사이트

건선 치료에서 생물학적 제제의 사용 확대

생물학적 제제를 이용한 치료로 인해 치료에 대한 기대가 ‘부분적인 질환 관리’에서 ‘피부 증상의 현저한 개선’으로 전환됨에 따라, 건선은 여전히 미국 피부과 의약품 시장의 주요 수익원으로 자리 잡고 있습니다. 애비(AbbVie)사는 2025년 ‘스카이리지(Skyrizi)’의 전 세계 매출이 176억 달러에 달할 것이라고 보고했는데, 이는 주요 면역요법 제제들에게 있어 건선 시장이 얼마나 큰 상업적 잠재력을 갖게 되었는지를 보여줍니다. 또한, 존슨앤드존슨은 2026년 3월, 성인 및 청소년의 일반성 건선에 대한 최초의 경구용 IL-23R 길항제로 알려진 ‘Icotyde’에 대해 FDA의 승인을 획득했습니다. 이로써, 그동안 피하 투여형 바이오의약품이 주도해 온 이 치료 분야에 중요한 비주사제 치료 옵션이 추가되게 됩니다. 이러한 변화가 중요한 이유는 처방 경쟁이 기본적인 효능의 차이에 의존하는 정도가 줄어들고, 투여의 편의성, 환자의 선호도, 그리고 브랜드가 약물 전환 주기를 통해 환자를 유지할 수 있는지 여부에 더 중점을 두기 시작했기 때문입니다. 시장 침투가 진행됨에 따라, 미국의 피부과용 의약품 시장에서는 초진에 따른 수요뿐만 아니라 브랜드 전환 및 제품 라인 확충을 통해 추가적인 가치 이동이 예상됩니다.

중등도에서 중증의 아토피 피부염 치료 옵션 확대

아토피 피부염은 치료법이 바이오의약품, 경구용 면역조절제, 그리고 새로운 비스테로이드계 외용약까지 확대됨에 따라, 미국 피부과 의약품 시장에서 가장 중요한 전문 분야 중 하나가 되었습니다. 듀피센트는 2025년에 전 세계적으로 178억 달러의 순매출을 기록했으며, 리제네론사는 전 세계적으로 140만 명 이상의 환자가 이 약물로 치료를 받고 있다고 보고했습니다. 2026년 1분기 매출액은 49억 달러에 달했으며, 이는 이 치료 기반이 얼마나 대규모이며 지속 가능한지를 보여주고 있습니다. 또한, 사노피는 2026년 3월, COAST 1, COAST 2 및 SHORE 임상시험에서 아무리테리맙의 3상 임상시험에 대한 긍정적인 결과를 보고했습니다. 이로써 중등도에서 중증 질환을 대상으로 하는 후기 단계의 생물학적 제제 후보가 하나 더 추가되게 됩니다. 따라서 이 범주는 양극단으로 확대되고 있으며, 중증 사례에서는 고부가가치의 전문 생물학적 제제가 도입되고, 경증 사례에서는 지속성이 더 높은 비스테로이드계 외용 요법으로 전환되고 있습니다. 이러한 폭넓은 치료 단계 구조 덕분에, 단일 작용기전이나 특정 중증도 범위에 의존하지 않고도 미국의 피부과용 의약품 시장이 확대되고 있습니다.

생물학적 제제의 높은 가격과 사전 승인 절차의 장벽

임상적 수요가 활발함에도 불구하고, 접근성 문제는 여전히 미국 피부과용 의약품 시장에 큰 걸림돌이 되고 있습니다. PMC를 통해 공개된 『JAMA Dermatology』의 분석에 따르면, 생물학적 제제 처방전의 87%가 사전 승인을 필요로 하며, 일반 피부과 진료소에서는 이 절차로 인해 월평균 3,454달러의 행정 비용이 발생하는 것으로 밝혀졌습니다. 이러한 부담으로 인해 치료 지연은 의사의 소극적인 태도나 환자 수요 부족 때문이 아니라, 행정 절차나 보험사의 심사에 의해 발생하는 경우가 많아지고 있습니다. 또한 이로 인해 진료소는 본래라면 치료의 조기 시작이나 사후 관리에 할애해야 할 시간을 접근 관리에 쏟을 수밖에 없는 상황에 처해 있습니다. 상환 제도 개혁이 긍정적인 방향으로 진행되고 있음에도 불구하고, 사전 승인은 여전히 미국 피부과용 의약품 시장의 실질적인 전환을 지연시키고 있습니다.

부문별 분석

2025년, 건선은 미국 피부과용 의약품 시장 점유율의 33.87%를 차지하며, 본 보고서에서 가장 큰 치료 분야로서의 위상을 유지했습니다. 이러한 우위는 생물학적 제제의 높은 보급률과 중등도에서 중증 질환의 높은 연간 치료비를 반영한 것입니다. 애비(AbbVie)사의 ‘스카이리지(Skyrizi)’는 2025년에 전 세계 매출 176억 달러를 기록했습니다. 이는 건선을 대상으로 한 바이오의약품이 전문의의 진료에 정착된다면, 어느 정도의 규모에 이를 수 있는지를 보여주고 있습니다. 또한, 2026년 3월에는 일반 건선에 대한 최초의 경구용 IL-23R 길항제인 ‘Icotyde’가 FDA의 승인을 획득했습니다. 이를 통해 주사 요법을 꺼리는 환자층에 대한 접근성을 확대할 가능성이 있는 비주사형 전신 요법 옵션이 추가되었습니다. 아토피 피부염은 듀피센트의 지속적인 시장 확대와 미국 피부과 의약품 업계에서 치료 옵션을 넓혀주고 있는 폭넓은 파이프라인에 힘입어 여전히 2위 적응증을 유지하고 있습니다.

화농성 땀샘염은 성장세가 가장 두드러지는 적응증으로, 2031년까지의 성장률은 9.97%로 예측됩니다. 또한, 이 적응증은 상업적 기반이 비교적 작은 상태에서 적응증 확장이 시작되었습니다는 점에서 두드러집니다. UCB는 2024년 11월, 중등도에서 중증의 화농성 땀샘염을 앓고 있는 성인 환자를 대상으로 한 ‘비므젤룩스’에 대해 FDA의 승인을 획득하고, 이 질환에 대한 최초의 IL-17A 및 IL-17F 이중 억제제를 시장에 출시했습니다. UCB사는 해당 제품의 2025년 순매출이 22억 유로(24억 달러 상당)에 달할 것이라고 보고했습니다. 그 후, 노바티스는 2026년 3월, 중등도에서 중증의 화농성 땀샘염을 앓고 있는 12세 이상의 소아 환자를 대상으로 한 ‘코센틱스’의 FDA 승인을 획득하여 치료 옵션을 더욱 확대했습니다. 로사 및 진균성 피부 감염증의 경우, 여전히 합리적인 가격의 국소 치료제와 안정적인 판매량에 의존하고 있지만, 원형 탈모증의 경우 FDA 승인을 받은 JAK 억제제가 등장함에 따라 그 존재감이 더욱 커지고 있습니다. 또한, 2025년에 ‘듀피센트’가 만성 자발성 두드러기 및 수포성 유사천포창에 대해 피부과 관련 적응증 확대 승인을 획득함에 따라, 보다 광범위한 ‘기타’ 그룹의 중요성도 커지고 있습니다.

2025년 매출액 중 처방약이 73.42%를 차지하고 있으며, 이는 여전히 브랜드 전문 치료제나 처방용 외용제에 얼마나 큰 가치가 집중되어 있는지를 보여줍니다. 미국 피부과용 의약품 시장에서 이 분야는 전문의의 평가, 보험사의 심사 또는 지속적인 임상 모니터링이 필요한 건선, 아토피 피부염, 화농성 땀샘염 치료제가 주도하고 있습니다. 또한, 중등도에서 중증의 질환의 경우, 주사용 바이오의약품이나 모니터링이 필요한 경구약은 자가 관리로 대체할 수 없기 때문에 투여 경로의 복잡성도 처방약 수요를 뒷받침하고 있습니다. 그렇긴 하지만, 2031년까지 OTC 제품의 연평균 성장률(CAGR)은 10.06%로 예측되고 있으며, 이는 처방약 부문을 웃도는 속도인 만큼 매출 구성비에 변화가 나타나기 시작하고 있습니다. 이러한 급속한 성장은 미국의 피부과용 의약품 시장이 고가의 처방약으로의 전환에만 의존하는 것이 아니라, 소비자 주도형 관리를 통해 확대되고 있음을 시사합니다.

OTC 시장은 소비자들의 피부 관리에 대한 인식 제고, 디지털 상담의 편의성 향상, 소매점 및 온라인을 통한 구매 용이성 증대 등 동시에 진행되고 있는 여러 요인의 혜택을 받고 있습니다. 이러한 요인들은 여드름이나 경미한 습진, 그 밖의 복잡성이 낮은 질환과 같이 환자가 전문의의 진료를 받기 전에 치료를 시작하는 경우가 많은 경우에 가장 중요합니다. 원격의료와 디지털 약국 도구도 이러한 변화를 뒷받침하고 있습니다. 환자는 기존의 진료소 주도의 절차보다 더 신속하게 증상 확인부터 제품 추천, 구매에 이르기까지의 과정을 진행할 수 있기 때문입니다. 지급자의 관점에서 볼 때, OTC로의 전환은 치료 성과가 반드시 보험 적용 대상인 처방약이 필요하지 않은 분야에서 보험 지급 부담을 줄일 수 있습니다. 그 결과, 미국의 피부과용 의약품 업계는 더욱 다층적인 구조를 띠게 되었으며, 처방약이 매출을 주도하는 한편, 일반의약품(OTC)은 편의성과 접근성을 무기로 시장 점유율을 지속적으로 확대되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the united states dermatological drugs market size is expected to grow from USD 16.78 billion in 2025 to USD 18.19 billion in 2026 and is forecast to reach USD 28.30 billion by 2031 at 9.24% CAGR over 2026-2031.

This report is Segmented by Indication (Acne, Psoriasis, Atopic Dermatitis, Rosacea, Alopecia Areata, HS, Other), Prescription Status (Prescription, OTC), Route (Topical, Oral, Parenteral), Drug Class (Corticosteroids, Retinoids, Antibiotics, PDE-4 Inhibitors, JAK Inhibitors, Biologics, Other), and Distribution (Hospital, Retail, Online Pharmacies). Market Forecasts are in Value (USD).

United States Dermatological Drugs Market Trends and Insights

Rising Biologic Uptake in Psoriasis

Psoriasis remains the main specialty revenue engine in the United States dermatological drugs market because biologic therapy has moved treatment expectations closer to high skin-clearance outcomes rather than partial disease control. AbbVie reported Skyrizi global revenue of USD 17.6 billion in 2025, which shows how large the commercial psoriasis pool has become for leading immune therapies. Johnson & Johnson also received FDA approval in March 2026 for Icotyde, described as the first oral IL-23R antagonist for plaque psoriasis in adults and adolescents, which adds a meaningful non-injectable option to a class that had been led by subcutaneous biologics. That shift matters because prescribing competition is starting to depend less on basic efficacy differences and more on dosing convenience, patient preference, and whether a brand can hold patients through switching cycles. As penetration matures, the United States dermatological drugs market is likely to see more value migrate through brand switching and line extension rather than through first-time diagnosis alone.

Expanding Moderate-To-Severe Atopic Dermatitis Treatment Pool

Atopic dermatitis has become one of the most important specialty segments in the United States dermatological drugs market because treatment now spans biologics, oral immunomodulators, and newer non-steroidal topicals. Dupixent generated USD 17.8 billion in global net sales in 2025, and Regeneron reported more than 1.4 million patients on treatment globally with first-quarter 2026 sales of USD 4.9 billion, which shows how large and durable this treatment base has become. Sanofi also reported positive Phase 3 data in March 2026 for amlitelimab across the COAST 1, COAST 2, and SHORE trials, which adds another late-stage biologic candidate for moderate-to-severe disease. The category is therefore widening at both ends, with severe disease pulling in high-value specialty biologics and milder disease moving toward more durable non-steroidal topical management. This broader treatment ladder is helping the United States dermatological drugs market expand without depending on a single mechanism or one patient severity band.

High Biologic Prices and Prior-Authorization Friction

Access barriers remain a major brake on the United States dermatological drugs market, even when clinical demand is strong. A JAMA Dermatology analysis available through PMC found that 87% of biologic prescriptions required prior authorization and that a typical dermatology practice faced an average monthly administrative cost of USD 3,454 from this process. That burden means treatment delays are often driven by paperwork and payer review rather than by physician reluctance or lack of patient need. It also pushes practices to spend time on access management that could otherwise support faster initiation or follow-up care. Even with reimbursement reform moving in a favorable direction, prior authorization keeps slowing real conversion in the United States dermatological drugs market.

Other drivers and restraints analyzed in the detailed report include:

- Strong FDA Approval Cadence in Medical Dermatology

- Persistent Acne Burden Sustaining Rx and OTC Demand

- Biosimilar Interchangeability and PBM Switching Friction

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Psoriasis held 33.87% of United States dermatological drugs market share in 2025, which kept it as the largest therapeutic revenue pool in this report. That lead reflects strong biologic penetration and high annual treatment value in moderate-to-severe disease. AbbVie's Skyrizi posted USD 17.6 billion in global revenue in 2025, which shows how much scale psoriasis-targeted biologics can reach once they become embedded in specialist practice. March 2026 also brought FDA approval for Icotyde as the first oral IL-23R antagonist for plaque psoriasis, adding a non-injectable systemic option that may widen reach among patients reluctant to use injectable therapy. Atopic dermatitis remained the second-largest indication, supported by the continued scale of Dupixent and by a broader pipeline that is widening treatment choice in the United States dermatological drugs industry.

Hidradenitis suppurativa is the fastest-growing indication, with projected growth of 9.97% through 2031, and it stands out because class expansion is starting from a lower commercial base. UCB received FDA approval in November 2024 for Bimzelx in adults with moderate-to-severe hidradenitis suppurativa, introducing the first dual IL-17A and IL-17F inhibitor for the condition, and UCB reported 2025 net sales of EUR 2.2 billion, equivalent to USD 2.4 billion, for the product. Novartis then expanded the treatment pool further in March 2026 with FDA approval of Cosentyx for pediatric patients aged 12 and older with moderate-to-severe hidradenitis suppurativa. Rosacea and fungal skin infections continue to rely more on affordable topical therapy and stable volume, while alopecia areata has become more visible after the arrival of FDA-approved JAK options. The broader "other" group is also gaining relevance, because Dupixent added dermatology-adjacent approvals in chronic spontaneous urticaria and bullous pemphigoid during 2025.

Prescription products accounted for 73.42% of 2025 revenue, which shows how much value is still concentrated in branded specialty therapies and prescription topicals. This part of the United States dermatological drugs market is led by psoriasis, atopic dermatitis, and hidradenitis suppurativa treatments that require specialist evaluation, payer review, or continued clinical monitoring. Prescription demand is also sustained by route complexity, since injectable biologics and monitored oral agents cannot be replaced by self-care in moderate-to-severe disease. Even so, the revenue mix is beginning to shift because OTC products are forecast to grow at 10.06% CAGR through 2031, which is faster than the prescription tier. That faster pace suggests the United States dermatological drugs market is widening through consumer-directed management rather than relying only on high-cost prescription escalation.

The OTC side benefits from several forces moving at the same time, including stronger consumer skincare awareness, easier digital consultation, and better retail and online availability. These factors matter most in acne, mild eczema, and other lower-complexity conditions where patients often start treatment before entering specialist care. Telehealth and digital pharmacy tools also support this shift, because patients can move from symptom review to product recommendation and purchase more quickly than in a traditional office-led pathway. From a payer perspective, OTC migration can reduce reimbursement pressure in categories where outcomes do not always require a covered prescription. The result is a more layered United States dermatological drugs industry, where prescription products keep revenue leadership, but OTC products continue to pull share through convenience and access.

List of Companies Covered in this Report:

- Abbvie

- Almirall

- Amgen

- Arcutis Biotherapeutics

- Bausch Health

- Bristol-Myers Squibb

- Eli Lilly and Company

- Galderma

- GlaxoSmithKline

- Incyte

- Johnson & Johnson Innovative Medicine

- Leo Pharma

- Novartis

- Organon

- Pfizer

- Regeneron Pharmaceuticals

- Sanofi

- Sun Pharmaceuticals Industries

- Teva Pharmaceutical Industries

- UCB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Biologic Uptake in Psoriasis

- 4.2.2 Expanding Moderate-To-Severe Atopic Dermatitis Treatment Pool

- 4.2.3 Persistent Acne Burden Sustaining Rx and OTC Demand

- 4.2.4 Strong FDA Approval Cadence in Medical Dermatology

- 4.2.5 Medicare Part D Redesign Improving Specialty-Drug Affordability

- 4.2.6 Teledermatology and Digital Pharmacy Integration Accelerating Conversion

- 4.3 Market Restraints

- 4.3.1 High Biologic Prices and Prior-Authorization Friction

- 4.3.2 JAK Safety Monitoring and Label-Related Caution

- 4.3.3 Dermatologist Workforce Maldistribution

- 4.3.4 Biosimilar Interchangeability and PBM Switching Friction

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Indication

- 5.1.1 Acne

- 5.1.2 Psoriasis

- 5.1.3 Atopic Dermatitis

- 5.1.4 Rosacea

- 5.1.5 Alopecia Areata

- 5.1.6 Hidradenitis Suppurativa

- 5.1.7 Fungal Skin Infections

- 5.1.8 Other Dermatological Indications

- 5.2 By Prescription Status

- 5.2.1 Prescription

- 5.2.2 Over-the-Counter

- 5.3 By Route of Administration

- 5.3.1 Topical

- 5.3.2 Oral

- 5.3.3 Parenteral

- 5.4 By Drug Class

- 5.4.1 Corticosteroids

- 5.4.2 Retinoids

- 5.4.3 Antibiotics

- 5.4.4 Antifungals

- 5.4.5 Calcineurin Inhibitors

- 5.4.6 PDE-4 Inhibitors

- 5.4.7 JAK Inhibitors

- 5.4.8 Biologics

- 5.4.9 Other Drug Classes

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies & Drugstores

- 5.5.3 Online Pharmacies

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AbbVie Inc.

- 6.3.2 Almirall

- 6.3.3 Amgen

- 6.3.4 Arcutis Biotherapeutics

- 6.3.5 Bausch Health Companies

- 6.3.6 Bristol Myers Squibb

- 6.3.7 Eli Lilly and Company

- 6.3.8 Galderma

- 6.3.9 GSK

- 6.3.10 Incyte

- 6.3.11 Johnson & Johnson Innovative Medicine

- 6.3.12 LEO Pharma

- 6.3.13 Novartis

- 6.3.14 Organon

- 6.3.15 Pfizer

- 6.3.16 Regeneron Pharmaceuticals

- 6.3.17 Sanofi SA

- 6.3.18 Sun Pharmaceutical Industries

- 6.3.19 Teva Pharmaceuticals USA

- 6.3.20 UCB

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment