|

시장보고서

상품코드

2065608

미국의 혈압 측정 기기 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Blood Pressure Monitoring Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

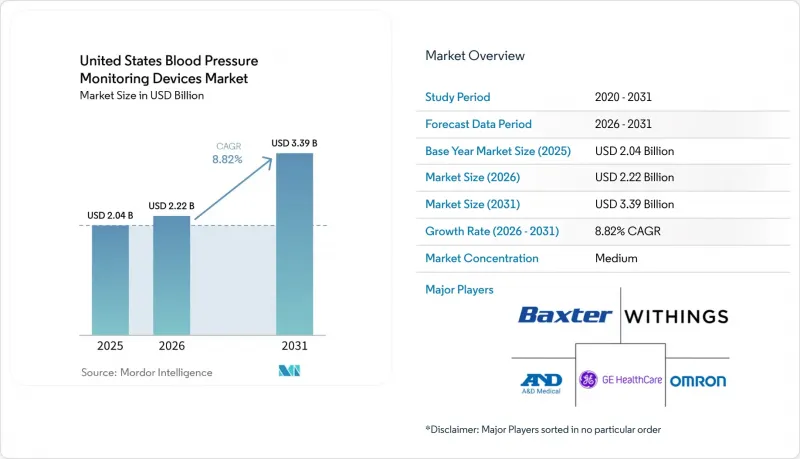

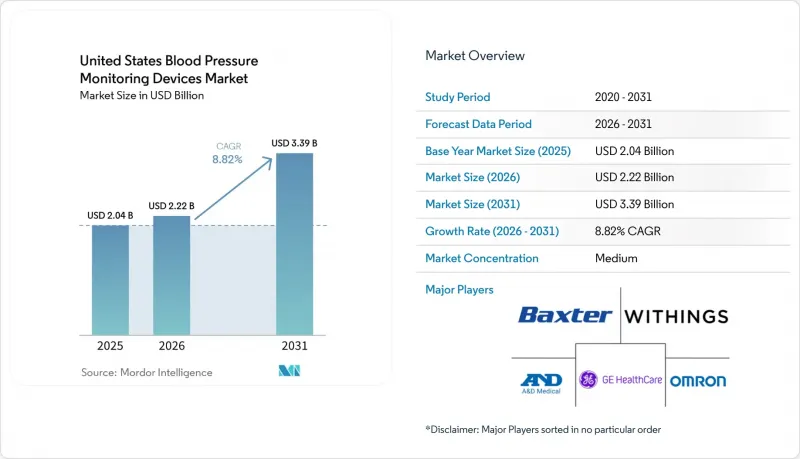

Mordor Intelligence에 의하면, 미국 혈압 측정 기기 시장 규모는 2025년에 20억 4,000만 달러로 평가되었고 2026년 22억 2,000만 달러에서 2031년까지 33억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 8.82%를 나타낼 전망입니다.

본 보고서는 제품 유형(아네로이드식, 디지털식, 휴대용, 커프 없는 웨어러블, 커프식), 기술(기존, 스마트 커넥티드, 커프리스), 최종 사용자(병원, 외래수술센터(ASC) 등), 유통 채널(의료기관용, 소매, 전자상거래, DTC RPM), 용도(고혈압, RPM, 예방 선별 검사, 임신)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 혈압 측정 기기 시장 동향 및 분석

관리가 제대로 이루어지지 않는 고혈압으로 인한 부담이 큽니다.

미국의 혈압 측정 기기 시장에서 가장 강력한 수요 기반이 되는 것은 유병률의 상승이 아니라 낮은 관리율에 있습니다. 이는 전국적인 유병률이 수년 동안 거의 비슷한 수준을 유지하고 있는 반면, 혈압 관리 상황은 여전히 미흡하기 때문입니다. 2021년 8월부터 2023년 8월 사이, 고혈압 성인 중 혈압이 130/80 mmHg 미만으로 관리되고 있던 비율은 고작 20.7%에 그쳤으며, 반복적인 측정이나 추적 관찰이 필요한 환자가 매우 많았습니다. 현재의 임상 지침에 따르면, 9,490만 명의 성인에게 생활 습관 개선과 약물 요법 지원이 권장되고 있어, 이러한 치료에 따른 부담을 가끔 병원을 방문하는 것만으로는 감당하기 어려운 상황입니다. 2025년 AHA 및 ACC 지침에서는 가정 혈압 측정을 고혈압 관리의 표준적인 부분으로 포함시키고, 치료 방침 결정을 진료소 밖에서 수집된 데이터와 더욱 밀접하게 연계함으로써 이러한 수요 패턴을 더욱 강화했습니다. 특히, 관리율이 여전히 낮은 청년층과 남성층에서는 수요 증가 여지가 더욱 크며, 이는 미국 혈압 측정 기기 시장에서 앱 연동형으로 사용하기 편리한 기기의 도입이 지속적으로 확대될 가능성을 시사합니다.

RPM 상환이 커넥티드 모니터링을 뒷받침

원격 모니터링이 점차 보급되고 있는 배경에는 환급 제도가 보다 폭넓은 원격 케어 업무 흐름을 지원하게 된 점이 꼽힙니다. 이로 인해 고혈압 환자를 지속적으로 관찰하는 것에 대한 의료 제공업체의 사업적 이점이 커지고 있습니다. 이러한 변화는 미국의 혈압 측정 기기 시장에서 중요한 의미를 지닙니다. 왜냐하면 도입 비용이 환자 개인의 부담에서 벗어나, 의료 시스템이나 의사 그룹이 관리하는 체계적인 치료 경로의 일부가 되기 때문입니다. 모니터링된 측정값이 만성 질환 관리 프로그램, 청구 워크플로우, 위험 관리 모델에 동시에 활용됨으로써, 의료 제공업체는 연결형 커프의 도입 대수를 확대할 타당한 근거를 확보할 수 있습니다. 이러한 환경에서는 데이터가 의료진에게 전달되기까지 환자가 수행해야 하는 작업의 횟수를 줄일 수 있으므로, 블루투스 전용 기기보다 셀룰러 통신이 지원되는 기기가 더 큰 이점을 제공합니다. 따라서, 특히 대규모 RPM 프로그램에 제품을 판매하는 공급업체의 경우, 미국의 혈압 측정 기기 시장에서는 정확도와 거의 맞먹을 정도로 보험 환급 제도의 설계가 제품 전략을 좌우하고 있습니다.

카프레스 기기의 정확도와 근거 간의 격차

카프리스형 기기는 상업적으로 큰 관심을 끌고 있지만, 근거가 부족하여 미국 혈압 측정 기기 시장 전체에서 진단이나 치료 방침 결정에 있어 그 활용은 여전히 제한되고 있습니다. 2025년 7월 Aktiia사가 시판용으로 FDA의 510(k) 승인을 획득한 이후에도, 보다 광범위한 임상 분야에서는 의료진이 진료 방식을 변경하기 전에 요구하는 수준의 비교 근거가 여전히 부족합니다. 미국심장협회(AHA)는 2025년 12월, 커프리스 기술에 대해서는 고혈압 진단이나 치료 방침을 확신하고 결정하기에 충분한 정확도가 아직 입증되지 않았다고 밝혔습니다. 따라서 이러한 기술들은 핵심적인 치료 경로라기보다는 웰니스 용도에 더 가까운 위치에 머물러 있습니다. 2026년 1월 FDA가 발표한 지침 초안은 향후 신청에 대한 임상 성능 시험 요건을 구체적으로 명시함으로써 기준을 한층 더 높였으며, 이에 따라 신규 진출기업에게는 더 많은 시간과 증거 자료가 요구될 것입니다. 직접 비교를 통한 검증이 보다 광범위하게 이루어지기 전까지는 미국 혈압 측정 기기 시장에서 고급 의료 기관용 및 RPM(원격 환자 모니터링) 채널은 커프식 기준에 의존하는 상태가 지속될 것으로 보입니다.

부문별 분석

2025년 기준으로 아날로그식 혈압계는 미국 혈압 측정 기기 시장 점유율의 36.31%를 차지했으나, 디지털식 혈압계는 2031년까지 연평균 성장률(CAGR) 11.38%를 나타낼 것으로 예측됩니다. 아날로그식 기기가 선두 자리를 유지하고 있는 이유는 병원 및 진료소가 여전히 저렴한 비용, 익숙한 작업 절차, 그리고 훈련된 환경 하에서 감독하에 이루어지는 청진 측정과의 지속적인 호환성을 중요하게 여기기 때문입니다. 이러한 도입 실적을 바탕으로, 특히 장비 교체를 단계적으로 진행하며 검증된 운영 절차를 선호하는 대규모 의료 제공 시스템에서 기존 부문은 여전히 견고한 입지를 유지하고 있습니다. 한편, 재택 간호, 연동 앱, 수은 대체재의 감소로 인해 자동 측정 기능이 신규 가정용 및 외래 환자 수요에서 기본적인 선택지로 자리 잡으면서, 디지털 혈압계의 발전은 여전히 빠른 속도로 진행되고 있습니다. 이러한 양극화는 미국의 혈압 측정 기기 시장이 한편으로는 의료 기관의 관성, 다른 한편으로는 가정 주도의 기기 교체라는 두 가지 서로 다른 속도로 움직이고 있음을 보여줍니다.

24시간 혈압 측정(ABPM) 모니터는 여전히 소규모 제품 카테고리이지만, 2025년 지침에서 ABPM이 ‘백의 고혈압’이나 ‘잠복성 고혈압’을 확인하기 위한 기준으로 계속해서 자리 잡고 있기 때문에 임상적으로 중요한 역할을 담당하고 있습니다. 이 권고 사항은 단일 진료소에서의 측정값보다 24시간 혈압 프로파일이 치료 조정에도 더 직접적인 영향을 미치는 신장내과 및 순환기내과 외래 진료 현장 수요를 뒷받침하고 있습니다. 팔목 밴드나 액세서리 역시 혈압 측정 기기 업계에서 여전히 중요한 위치를 차지하고 있습니다. 이는 교체 주기, 다양한 크기 옵션, 그리고 교정의 필요성 덕분에 장비의 초기 판매 이후에도 지속적인 수익이 발생하기 때문입니다. 커프리스형 웨어러블은 여전히 가장 규모가 작은 제품 부문이지만, Aktiia사의 2025년 7월 일반의약품(OTC) 승인 및 Nanowear사의 FDA 승인을 받은 연속 모니터링 경로와 같은 규제상의 이정표들은 혁신이 미래 카테고리 변혁의 한계를 넓혀가고 있음을 보여줍니다. 단기적인 전망으로는 기존 카테고리가 여전히 매출의 대부분을 차지하는 한편, 새로운 형태의 제품이 미국 혈압 측정 기기 시장 전체의 투자 우선순위에 영향을 미치는 제품 구성이 될 것으로 보입니다.

2025년 기준으로, 기존의 비스마트형 기기는 미국 혈압 측정 기기 시장 점유율의 63.24%를 차지했으나, 스마트 연결형 기기는 2031년까지 연평균 성장률(CAGR) 10.52%로 성장할 것으로 전망됩니다. 많은 병원 시스템이 이미 검증된 재고를 보유하고 있으며, 대규모 조달 팀이 여전히 의료 현장 간에 표준화하기 쉬운 제품을 선호하기 때문에 기존 의료기기가 지배적인 위치를 유지하고 있습니다. 비용 측면의 제약도 이 부문을 뒷받침하고 있습니다. 기존 혈압계는 연결형 생태계에 필요한 추가 소프트웨어 스택 없이도 일상적인 측정 요구를 충족시킬 수 있기 때문입니다. 스마트 연결형 기기의 성장이 가속화되고 있는 것은 혈압계의 가치가 단순한 측정값 표시에 그치지 않고 데이터 전송, 원격 관리, 임상 기록으로 확대되고 있기 때문입니다. 이러한 변화로 인해 미국의 혈압 측정 기기 시장은 순수한 하드웨어 경쟁에서 플랫폼 경쟁으로 전환되고 있습니다.

2024년 11월, 오므론이 표준 상완식 모니터를 통한 심방세동(AFib) 감지에 대해 FDA의 데 노보 승인을 획득한 것은 측정이라는 핵심적인 행위를 변경하지 않으면서도 알고리즘을 접목함으로써 제품의 포지셔닝을 어떻게 변화시킬 수 있는지를 보여주고 있습니다. 블루투스 연결 기기는 환자의 스마트폰이나 익숙한 앱의 조작과 자연스럽게 연동되므로, 여전히 폭넓은 소매 수요에 적합합니다. 한편, 셀룰러 연결 기기는 환자의 부담을 줄이고 측정값이 중단 없이 의료 제공업체의 시스템으로 전송될 가능성을 높이기 때문에 공식적인 원격 환자 모니터링(RPM) 프로그램에서 그 중요성이 점점 더 커지고 있습니다. 카프리스형 센서 기술의 매출 규모는 여전히 작지만, IEEE 1708이나 ISO 81060-2와 같은 규격은 이미 어떤 제품이 임상적 신뢰성이나 제3자 심사를 받을 수 있는지를 결정짓고 있습니다. 혈압 측정 기기 업계에서 검증 요건과 소프트웨어 통합 요건 모두를 조기에 준수하는 것이 의료 기관에 대한 우대적인 접근권을 확보하기 위한 주요 경로로 자리 잡고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the united states blood pressure monitoring devices market size was valued at USD 2.04 billion in 2025 and is estimated to grow from USD 2.22 billion in 2026 to reach USD 3.39 billion by 2031, at a CAGR of 8.82% during the forecast period (2026-2031).

This report is Segmented by Product Type (Aneroid, Digital, Ambulatory, Cuffless Wearables, Cuffs), Technology (Traditional, Smart Connected, Cuffless), End User (Hospitals, Ascs, and More), Distribution Channel (Institutional, Retail, E-Commerce, DTC RPM), and Application (Hypertension, RPM, Preventive Screening, Pregnancy). Market Forecasts are Provided in Terms of Value (USD).

United States Blood Pressure Monitoring Devices Market Trends and Insights

High Uncontrolled Hypertension Burden

The strongest demand base in the United States blood pressure monitoring devices market comes from low control rates rather than rising prevalence, because national prevalence has stayed near the same broad range for years while control remains weak. During August 2021 to August 2023, only 20.7% of hypertensive adults had blood pressure controlled below 130/80 mmHg, which left a very large pool of patients needing repeated measurement and follow-up. That care burden cannot be managed through occasional office visits alone, since 94.9 million adults are recommended for lifestyle modification and medication support under current clinical guidance. The 2025 AHA and ACC guideline reinforced this demand pattern by making home blood pressure monitoring a standard part of hypertension management and by linking treatment decisions more closely to out-of-office data. The demand runway is even broader among younger adults and men, where control rates remain lower, which points to sustained adoption potential for app-linked and easy-to-use devices in the United States blood pressure monitoring devices market.

RPM Reimbursement Supporting Connected Monitoring

Connected monitoring is gaining traction because reimbursement now supports a wider set of remote care workflows, which improves the provider business case for keeping hypertensive patients under continuous observation. This shift matters in the United States blood pressure monitoring devices market because the cost of adoption moves away from the patient alone and becomes part of an organized care pathway managed by health systems and physician groups. Providers can justify a larger installed base of connected cuffs when monitored readings feed chronic care programs, billing workflows, and risk-management models at the same time. Cellular-enabled devices benefit more than Bluetooth-only devices in these settings, because they reduce the number of patient actions required before data reaches the care team. Reimbursement design is therefore shaping product strategy in the United States blood pressure monitoring devices market almost as strongly as accuracy, especially for vendors selling into large RPM programs.

Cuffless Accuracy And Evidence Gaps

Cuffless devices are drawing high commercial interest, but the evidence gap is still limiting their use in diagnosis and treatment decisions across the United States blood pressure monitoring devices market. Even after Aktiia received FDA 510(k) clearance for over-the-counter use in July 2025, the broader clinical category still lacks the depth of comparative evidence that providers want before changing practice patterns. The American Heart Association stated in December 2025 that cuffless technologies had not yet shown enough accuracy to diagnose hypertension or guide treatment with confidence, which keeps them closer to wellness use than to core care pathways. The FDA's January 2026 draft guidance raises the bar further by specifying clinical performance testing expectations for future submissions, which increases time and evidence demands for new entrants. Until head-to-head validation becomes broader, premium institutional and RPM channels in the United States blood pressure monitoring devices market are likely to remain anchored in cuff-based standards.

Other drivers and restraints analyzed in the detailed report include:

- Home-Based Chronic-Care Management Adoption

- Validated-device Initiatives Improving Clinician Confidence

- Premium Pricing For Connected And Cuffless Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aneroid blood pressure monitors held 36.31% of the United States blood pressure monitoring devices market share in 2025, while digital blood pressure monitors are projected to grow at an 11.38% CAGR through 2031. Aneroid devices kept the lead because hospitals and clinics still value their low cost, familiar workflow, and continued fit with supervised auscultatory measurement in trained settings. That installed base gives the legacy segment resilience, especially in large provider systems that replace equipment gradually and prefer proven operating routines. Digital monitors are still advancing faster because home care, connected apps, and the decline of mercury alternatives are making automated measurement the default choice for new household and outpatient demand. This split shows that the United States blood pressure monitoring devices market is moving in two speeds, with institutional inertia on one side and home-led upgrading on the other.

Ambulatory blood pressure monitors remain a smaller product class, but they hold a strong clinical role because the 2025 guideline continues to treat ABPM as the reference standard for confirming white-coat and masked hypertension. That recommendation supports demand in nephrology and cardiology outpatient settings where 24-hour profiles shape treatment adjustments more directly than single office readings. Cuffs and accessories also remain important inside the blood pressure monitoring devices industry because replacement cycles, size variation, and calibration needs create recurring revenue after the initial device sale. Cuffless wearables are still the smallest product segment, but regulatory milestones such as Aktiia's July 2025 over-the-counter clearance and Nanowear's FDA-cleared continuous monitoring pathway show that innovation is pushing the edge of future category change. The near-term outcome is a product mix where conventional categories still carry most revenue, while newer formats influence investment priorities across the United States blood pressure monitoring devices market.

Traditional non-smart devices retained 63.24% of the United States blood pressure monitoring devices market share in 2025, while smart connected devices are set to grow at a 10.52% CAGR through 2031. Legacy devices remain dominant because many hospital systems already own validated inventories, and large procurement teams still favor products that are easy to standardize across care sites. Cost discipline also supports this segment, since traditional monitors can fill routine measurement needs without the extra software stack required by connected ecosystems. Smart connected devices are growing faster because the value of a monitor now extends beyond a reading and into data movement, remote management, and clinical documentation. This shift is pushing the United States blood pressure monitoring devices market toward platform competition rather than pure hardware competition.

Omron's FDA De Novo authorization in November 2024 for AFib detection inside a standard upper-arm monitor shows how algorithmic layering can change product positioning without changing the core act of measurement. Bluetooth-connected devices still suit broad retail demand because they work naturally with patient smartphones and familiar app behavior. Cellular devices are gaining strength in formal RPM programs because they lower patient friction and improve the chances that readings move into the provider system without interruption. Cuffless sensor-based technologies remain small in revenue terms, yet standards such as IEEE 1708 and ISO 81060-2 are already shaping which products can pursue clinical credibility and third-party review pathways. In the blood pressure monitoring devices industry, early compliance with both validation and software integration requirements is becoming the main route to premium institutional access.

List of Companies Covered in this Report:

- A&D Medical

- Aktiia

- American Diagnostic

- Baxter International (Welch Allyn)

- Beurer

- Braun Healthcare

- ForaCare AG

- GE Healthcare

- Greater Goods

- iHealth Labs

- Microlife

- Midmark

- Mindray

- OMRON

- Koninklijke Philips

- Rossmax

- Spacelabs Healthcare

- SunTech Medical

- Veridian Healthcare

- Withings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Uncontrolled Hypertension Burden

- 4.2.2 RPM Reimbursement Supporting Connected Monitoring

- 4.2.3 Home-Based Chronic-Care Management Adoption

- 4.2.4 Validated-Device Initiatives Improving Clinician Confidence

- 4.2.5 Maternal-Health Remote Monitoring Expansion

- 4.3 Market Restraints

- 4.3.1 Cuffless Accuracy and Evidence Gaps

- 4.3.2 Premium Pricing for Connected and Cuffless Devices

- 4.3.3 Lack of Reimbursement for Home BP Cuffs

- 4.3.4 Cuff-Size Mismatch Limiting Patient Eligibility

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Buyer Power

- 4.7.2 Supplier Power

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Aneroid Blood Pressure Monitors

- 5.1.2 Digital Blood Pressure Monitors

- 5.1.3 Ambulatory Blood Pressure Monitors

- 5.1.4 Cuffless Blood Pressure Wearables

- 5.1.5 Blood Pressure Cuffs and Accessories

- 5.2 By Technology

- 5.2.1 Traditional Non-smart Devices

- 5.2.2 Smart Connected Devices

- 5.2.3 Cuffless Sensor-based Devices

- 5.3 By End User

- 5.3.1 Hospitals and Clinics

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Home Healthcare Settings

- 5.3.4 Other End Users

- 5.4 By Distribution Channel

- 5.4.1 Institutional Direct Sales and Group Purchasing

- 5.4.2 Retail Pharmacies and Drug Stores

- 5.4.3 E-commerce

- 5.4.4 Direct-to-Consumer RPM Programs

- 5.5 By Application

- 5.5.1 Hypertension Diagnosis and Ongoing Management

- 5.5.2 Remote Patient Monitoring

- 5.5.3 Preventive Screening and Wellness Monitoring

- 5.5.4 Pregnancy and Preeclampsia Monitoring

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 A&D Medical

- 6.3.2 Aktiia

- 6.3.3 American Diagnostic Corporation

- 6.3.4 Baxter International (Welch Allyn)

- 6.3.5 Beurer GmbH

- 6.3.6 Braun Healthcare

- 6.3.7 ForaCare AG

- 6.3.8 GE HealthCare

- 6.3.9 Greater Goods

- 6.3.10 iHealth Labs

- 6.3.11 Microlife Corporation

- 6.3.12 Midmark Corporation

- 6.3.13 Mindray

- 6.3.14 Omron Healthcare

- 6.3.15 Philips

- 6.3.16 Rossmax International

- 6.3.17 Spacelabs Healthcare

- 6.3.18 SunTech Medical

- 6.3.19 Veridian Healthcare

- 6.3.20 Withings

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment