|

시장보고서

상품코드

2065769

산업용 유통 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Industrial Distribution - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

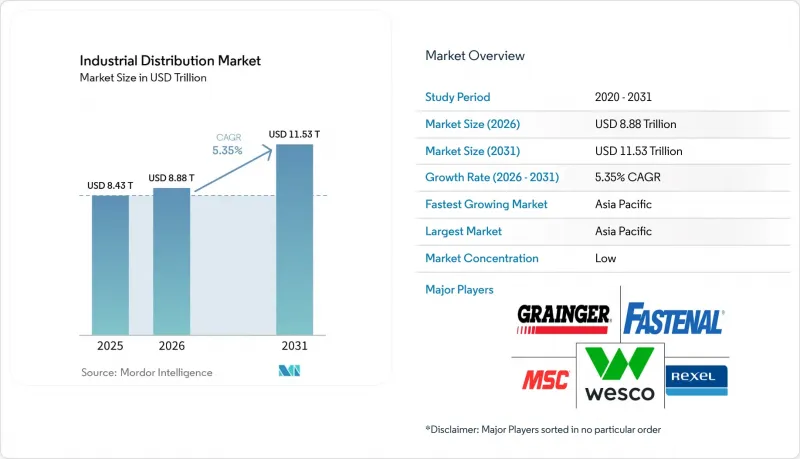

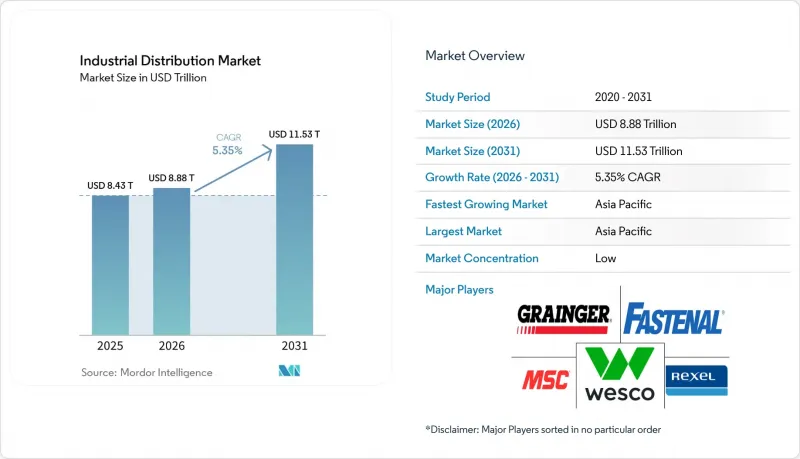

Mordor Intelligence에 의하면, 산업용 유통 시장 규모는 2025년에 8조 4,300억 달러로 평가되었고 2026년 8조 8,800억 달러에서 2031년까지 11조 5,300억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.35%를 나타낼 전망입니다.

본 보고서는 제품별(전기용품, 체결구, HVAC 기기 등), 유통 채널별(오프라인(지점/내근 영업) 등), 최종 사용 산업별(제조, 건설 및 인프라 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러) 단위로 제시되어 있습니다.

세계 산업용 유통 시장 동향과 인사이트

산업용 IoT(IIoT) 및 자동화 도입

실시간 자산 모니터링을 통해 유통업체는 사후 대응형 주문 처리에서 데이터 기반 재고 보충 서비스로 전환할 수 있게 됩니다. 엣지 컴퓨팅과 예측 분석을 결합함으로써, 예기치 못한 가동 중지 시간을 줄이고, 기계의 상태 신호에 맞추어 재고 수준을 조정할 수 있습니다. 지멘스의 산업용 기반 모델은 생성형 AI가 엔지니어링 주기를 단축함으로써, OEM 플랫폼과 공장 사용자를 연결하는 유통업체에게 서비스 수익 창출로 이어진다는 점을 보여주고 있습니다. 또한, 연결형 센서에 대한 투자는 고정밀 전기 부품 및 보안이 강화된 네트워크 장비에 대한 수요도 견인하고 있습니다.

대규모 인프라 프로젝트의 파이프라인

미국의 2조 달러 규모 프로젝트 계획과 중국이 스마트 인프라에 배정한 1조 5,000억 달러는 전력 케이블, 개폐 장치, 건설용 소모품에 대한 대량 발주로 이어지고 있습니다. 프로젝트 관리 지원과 적시 납품 능력을 갖춘 유통업체가 대규모 공급 계약을 수주하고 있습니다. 동남아시아에서도 각국 정부가 공항, 철도, 재생에너지 건설을 가속화하고 있어 성장세가 더욱 거세지고 있으며, 지역 재고와 기술 지원을 제공하는 유통업체에게는 유리한 상황이 되고 있습니다.

상품 가격 변동

철강 가격은 분기마다 15-20% 변동할 가능성이 있으므로, 재고 평가 손실을 방지하기 위해서는 유연한 가격 책정 및 헤지 전략이 필요합니다. 가격이 하락하면 고객들이 주문을 미루게 되어, 유통업체의 재고가 증가하고 자금이 묶이게 됩니다. 에너지 가격의 변동은 운송비 예산 수립과 수요 계획을 더욱 복잡하게 만들고 있습니다.

부문별 분석

전기 제품은 2025년 매출의 26.97%를 차지하며, 전력망 현대화 및 데이터센터 건설에서 그 중요성이 입증되었습니다. 재생에너지의 연계 및 공장 자동화로 인해 단위 수요가 증가함에 따라, 전기용품의 산업용 유통 시장 규모는 꾸준히 확대될 것으로 예측됩니다. 안전 용품 및 개인보호구(PPE) 시장은 연평균 성장률(CAGR) 9.38%를 기록하며 성장하고 있으며, 이는 전 세계적인 안전 규제와 기업의 위험 완화 조치의 혜택을 받고 있습니다. 한편, 산업용 패스너와 HVAC 장비는 꾸준한 건설 착공과 인프라 확충에 힘입어 성장하고 있습니다.

전자상거래 주문 처리의 발전으로 창고 자동화가 진전되는 가운데, 자재관리 시스템에 대한 투자가 활발해지고 있습니다. 베어링 및 동력 전달 부품의 경우, 예측 유지보수 일정에 연동된 견조한 MRO 수요가 나타나고 있습니다. 윤활유의 경우, 교환 주기가 긴 합성유로의 전환이 진행되고 있지만, 디지털을 통한 상태 모니터링을 통해 적절한 시기에 보충하는 것이 여전히 권장되고 있습니다. 커넥티드 툴과 계측 기기는 기계적 정밀도와 클라우드 분석을 결합하여 유통업체의 서비스 범위를 확대되고 있습니다.

지역별 분석

아시아태평양은 2025년에 매출의 36.21%를 차지해, 중국의 제조업 생산액 10조 달러와 인도의 화학 산업에서 두 자릿수 성장을 배경으로 2031년까지 연평균 성장률(CAGR) 8.55%로 성장할 전망입니다. 동남아시아를 향한 지역 공급망의 다각화가 진행됨에 따라, 국경을 초월한 유통 흐름이 강화되고 있습니다. 현지 유통업체는 다국어 지원 및 다양한 규제 기준에 대한 전문 지식이라는 강점을 활용하고 있습니다.

북미는 성숙 단계에 접어들고 있지만 여전히 혁신이 주도하는 시장입니다. 그레이저의 2024년 매출액 172억 달러는 규모의 경제성과 해당 지역에서 전자상거래를 활용한 조달에 대한 수요가 높음을 입증하고 있습니다. 제조업체의 85%가 AI 도입을 계획하고 있는 만큼, 커넥티드 컴포넌트에 대한 수요가 증가하고 있는 반면, 인프라 관련 법안에 따라 송전망 및 광대역 네트워크 업그레이드에 자본이 투입되고 있습니다. 상품 가격 변동과 운임 급등이 리쇼어링과 지역 내 창고 설치를 촉진하고 있습니다.

유럽은 변화를 촉진하는 정책적 압력에 직면해 있습니다. ‘탄소 국경 조정 메커니즘(CBAM)’에 따라 2026년까지 수입 철강의 비용이 톤당 약 16.19% 상승하게 되어, 이에 따라 유통업체들은 지역 내 재고 확보와 저탄소 자재 조달을 서둘러야 하는 상황에 놓여 있습니다. 소네파가 2024년에 단행한 20억 달러 규모의 인수 열풍은 규모 확대와 서비스 포트폴리오 확충을 목표로 한 진행 중인 업계 재편을 여실히 보여주고 있습니다. 지속가능성 목표는 에너지 효율이 높은 제품이나 순환형 경제와 관련된 제품에 대한 관심을 높이고 있습니다.

중동 및 아프리카에서는 산업 다각화 계획에 따라 점진적인 성장이 예상되는 반면, 라틴아메리카에서는 광업 인프라 및 자동차 제조업에 대한 투자가 확대되고 있습니다. 환율 변동이나 정치적 불안정은 여전히 주시해야 할 사항이지만, 장기적인 인프라 부족은 탄탄한 리스크 관리 능력을 갖춘 유통업체에게는 성장의 기회가 되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the industrial distribution market size was valued at USD 8.43 trillion in 2025 and estimated to grow from USD 8.88 trillion in 2026 to reach USD 11.53 trillion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031).

This report is Segmented by Product (Electrical Supplies, Fasteners, HVAC Equipment, and More), Distribution Channel (Offline (Branch / Inside Sales), and More), End-User Industry (Manufacturing, Construction and Infrastructure, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Distribution Market Trends and Insights

Industrial IoT and automation adoption

Real-time asset monitoring enables distributors to shift from reactive order fulfillment to data-driven replenishment services. Edge computing paired with predictive analytics cuts unplanned downtime and aligns stocking levels with machine health signals. Siemens' industrial foundation models illustrate how generative AI shortens engineering cycles and unlocks service revenue for distributors who bridge OEM platforms with factory users. Investments in connected sensors also pull through demand for high-precision electrical components and secure networking gear.

Infrastructure megaproject pipelines

A USD 2 trillion project slate in the United States and USD 1.5 trillion earmarked by China for smart infrastructure are translating into bulk orders for power cables, switchgear, and construction consumables. Distributors with project-management support and just-in-time delivery capabilities win large supply contracts. Southeast Asia adds momentum as governments accelerate airport, rail, and renewable energy builds, which favor distributors offering regional inventory and technical assistance.

Commodity-price volatility

Steel prices can fluctuate 15-20% within a quarter, forcing dynamic pricing and hedge strategies to avoid inventory write-downs. Customers delay orders when prices fall, inflating distributor stock and tying up cash. Energy price swings further complicate freight budgeting and demand planning.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce-led MRO fulfillment boom

- Stricter workplace-safety regulations

- Global logistics cost inflation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electrical supplies contributed 26.97% of 2025 revenue, confirming their importance in power grid upgrades and data-center builds. The industrial distribution market size for electrical supplies is expected to climb steadily as renewable energy connections and factory automation lift unit demand. Safety and PPE products, growing at 9.38% CAGR, benefit from global safety mandates and corporate risk mitigation, while industrial fasteners and HVAC equipment ride steady construction starts and infrastructure upgrades.

Material-handling systems are attracting investment as e-commerce fulfillment pushes warehouses toward automation. Bearings and power-transmission parts see resilient MRO demand tied to predictive maintenance schedules. Lubricants face substitution by synthetics with longer drain intervals, yet digital condition-monitoring still spurs timely replenishment. Connected tools and instruments blend mechanical precision with cloud analytics, widening distributor service scopes.

Geography Analysis

Asia-Pacific held 36.21% revenue in 2025 and is set to compound at 8.55% CAGR through 2031 on the back of USD 10 trillion in Chinese manufacturing output and India's double-digit chemicals expansion. Growing regional supply-chain diversification into Southeast Asia strengthens cross-border distribution flows. Local distributors gain advantage from multilingual support and familiarity with varying regulatory codes.

North America represents a mature yet innovation-driven arena. Grainger's USD 17.2 billion 2024 sales underscore scale efficiencies and the region's appetite for e-commerce-enabled procurement. Manufacturers' 85% AI adoption plans lift demand for connected components, while infrastructure legislation channels capital into grid and broadband upgrades. Commodity swings and freight inflation motivate reshoring and regional warehousing.

Europe faces transformational policy pressures. The Carbon Border Adjustment Mechanism will raise imported steel costs by about 16.19% per ton by 2026, prompting distributors to stock regionally and source lower-emission materials. Sonepar's USD 2 billion acquisition spree in 2024 highlights ongoing consolidation aimed at scale gains and broader service portfolios. Sustainability goals spur interest in energy-efficient products and circular-economy offerings.

The Middle East and Africa record incremental gains from industrial diversification plans, while Latin America draws spending into mining infrastructure and auto manufacturing. Currency volatility and political instability remain watchpoints, but long-term infrastructure gaps present growth headroom for distributors with robust risk-management capabilities.

- W.W. Grainger Inc.

- Fastenal Company

- WESCO International Inc.

- MSC Industrial Direct Co. Inc.

- Airgas Inc.

- Motion Industries Inc.

- Winsupply Inc.

- Applied Industrial Technologies Inc.

- MRC Global Inc.

- Sonepar USA

- Rexel Group

- Graybar Electric Co.

- HD Supply (HD Inc.)

- Anixter International

- Ferguson PLC

- Bisco Industries

- Kimball Midwest

- DistributionNOW

- Bunzl PLC

- Lawson Products Inc.

- Endries International

- Grainger MonotaRO (Japan)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industrial IoT and Automation adoption

- 4.2.2 Infrastructure megaproject pipelines

- 4.2.3 E-commerce-led MRO fulfillment boom

- 4.2.4 Stricter workplace-safety regulations

- 4.2.5 OEM-distributor API-based auto-replenishment

- 4.2.6 Carbon border adjustments push regional inventory hubs

- 4.3 Market Restraints

- 4.3.1 Commodity-price volatility

- 4.3.2 Global logistics cost inflation

- 4.3.3 OEM risk-sharing contracts squeeze margins

- 4.3.4 OEM direct e-commerce channel cannibalization

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Industry Value Chain Analysis

- 4.9 Macroeconomic Trend Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product

- 5.1.1 Electrical Supplies

- 5.1.2 Fasteners

- 5.1.3 HVAC Equipment

- 5.1.4 Safety and PPE Supplies

- 5.1.5 Material Handling and Packaging

- 5.1.6 Power Transmission and Bearings

- 5.1.7 Industrial Fluids and Lubricants

- 5.1.8 Tools and Instruments

- 5.1.9 Other Products

- 5.2 By Distribution Channel

- 5.2.1 Offline (Branch / Inside Sales)

- 5.2.2 Online / E-commerce Platforms

- 5.3 By End-user Industry

- 5.3.1 Manufacturing

- 5.3.2 Construction and Infrastructure

- 5.3.3 Energy and Utilities

- 5.3.4 Mining and Metals

- 5.3.5 Chemicals and Process

- 5.3.6 Transportation and Warehousing

- 5.3.7 Healthcare and Pharmaceuticals

- 5.3.8 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Southeast Asia

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Kenya

- 5.4.5.2.4 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 W.W. Grainger Inc.

- 6.4.2 Fastenal Company

- 6.4.3 WESCO International Inc.

- 6.4.4 MSC Industrial Direct Co. Inc.

- 6.4.5 Airgas Inc.

- 6.4.6 Motion Industries Inc.

- 6.4.7 Winsupply Inc.

- 6.4.8 Applied Industrial Technologies Inc.

- 6.4.9 MRC Global Inc.

- 6.4.10 Sonepar USA

- 6.4.11 Rexel Group

- 6.4.12 Graybar Electric Co.

- 6.4.13 HD Supply (HD Inc.)

- 6.4.14 Anixter International

- 6.4.15 Ferguson PLC

- 6.4.16 Bisco Industries

- 6.4.17 Kimball Midwest

- 6.4.18 DistributionNOW

- 6.4.19 Bunzl PLC

- 6.4.20 Lawson Products Inc.

- 6.4.21 Endries International

- 6.4.22 Grainger MonotaRO (Japan)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment