|

시장보고서

상품코드

2065792

해충 방제 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Insect Pest Control - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

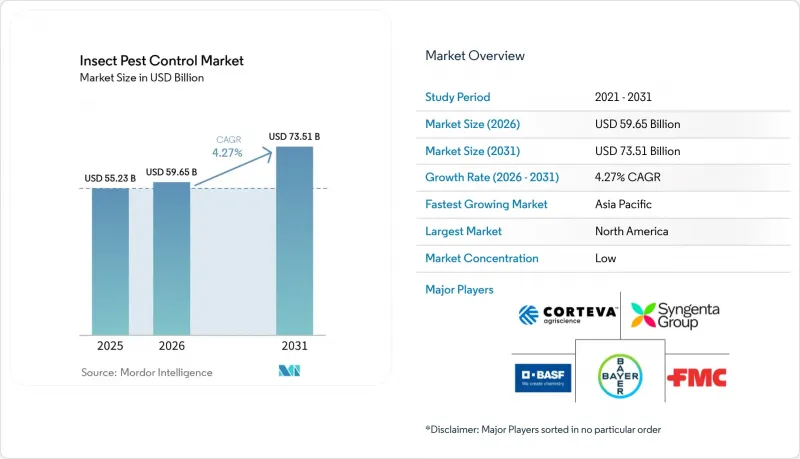

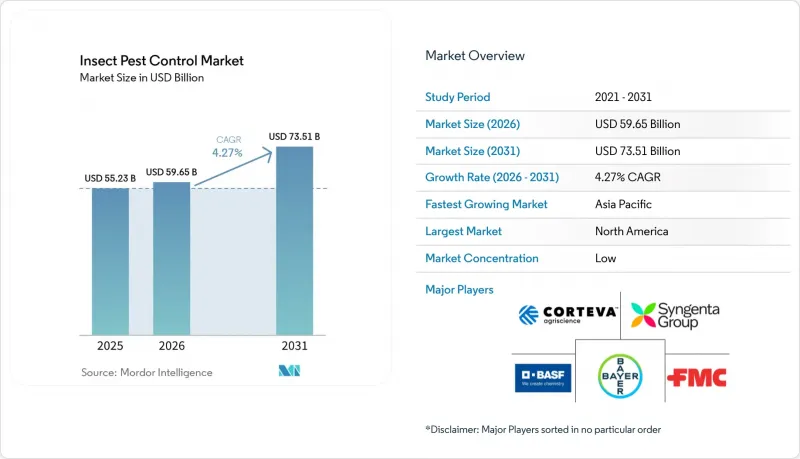

Mordor Intelligence에 의하면, 해충 방제 시장 규모는 2025년 552억 3,000만 달러에서 2026년에는 596억 5,000만 달러로 확대되어 2031년까지 735억 1,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.27%로 성장할 전망입니다.

본 보고서는 방제 방법(화학적, 생물학적, 물리적), 작물 유형(곡물, 과일 및 채소, 유지종자·콩류 등), 시용 방법(엽면 살포, 종자 처리, 토양 처리 등), 지역(북미, 유럽, 아시아태평양, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망(금액, 달러).

세계 해충 방제 시장 동향과 인사이트

심화되는 해충의 위협과 농작물 수확량 손실 위험

세계 농작물 생산은 해충으로 인한 수확량 손실이라는 심각한 압박에 계속해서 직면하고 있으며, 이는 농업의 수익성에 대한 가장 고질적인 위협 중 하나로 남아 있습니다. 2025년, 크롭 프로텍션 네트워크(Crop Protection Network)는 2024년 시즌에 무척추동물 해충이 미국 29개 주의 옥수수 수확량을 4.0% 감소시켜 6억 1,000만 부셸 이상의 손실을 초래했을 것으로 예측했습니다. 이는 현대 농업에서 해충 피해로 인한 경제적 부담이 여전히 지속되고 있음을 보여줍니다. 수확량 확보는 여전히 생산자의 수익성에서 핵심적인 요소이므로, 농장의 이익률이 어려운 상황이라 하더라도 해충 방제에 드는 비용을 미루기는 어렵습니다. 또한, 해충 방제 시장은 특히 해충의 발생 주기가 반복되는 작물의 경우, 동일 시즌 내에 여러 해충 종을 관리해야 할 필요성이 높아지고 있는 점에 힘입어 혜택을 보고 있습니다. 이러한 추세는 광범위한 해충 방제 프로그램에 대한 수요 증가를 뒷받침하고 있으며, 동일한 해충 방제 시장 내에서 여러 가지 작용기전을 제공할 수 있는 공급업체에게 유리하게 작용하고 있습니다.

규제 당국 및 소매업체의 저잔류 프로그램 추진

환경 규제의 강화와 소매업체 기준의 엄격화로 인해, 선택성이 더 높고 잔류량이 적은 해충 방제 프로그램으로의 전환이 가속화되고 있습니다. 미국 환경보호청(EPA)은 2025년 4월 29일, ‘살충제 전략’을 최종 확정했습니다. 이는 약 8,300만 에이커에 달하는 처리 대상 면적을 포괄하며, 살포 시 약제 비산을 방지하기 위한 완충 지대 및 유출수 관리 등의 완화 조치를 의무화하고 있습니다. 유럽에서는 농약 사용 및 기록 관리에 대한 감독이 강화되고 있으며, 농업 실무에서 디지털 기록 및 추적성으로의 광범위한 전환을 포함해 규정 준수 압박은 여전히 높은 수준을 유지하고 있습니다. 이로 인해 종합 해충 관리(IPM) 프로그램에 적합한 제품의 가치가 높아지면서, 바이오 농약, 페로몬 제제 및 선택성이 높은 화학농약의 활용 범위가 확대되고 있습니다. 따라서 해충 방제 시장에서는 규정 준수를 핵심으로 하는 프리미엄 프로그램과, 대체 압력이 더욱 강해지고 있는 범용 프로그램 사이에서 뚜렷한 양극화가 나타나고 있습니다.

기존 화학 농약에 대한 내성

해충 방제 시장은 몇몇 주요 해충 군에서 기존 화학 농약에 대한 내성이 높아지고 있어 명백한 한계에 직면해 있습니다. 바덴뷔르템베르크주가 발표한 2026년 공식 통합 해충 관리 지침에 따르면, 독일 라인 평야 및 크라이히가우 지역의 유채꽃노린재 개체군에서 ‘슈퍼 KDR 내성’이 확인되었다고 보고되었으며, 이러한 핫스팟에서는 대체 유효 성분을 사용할 것을 생산자들에게 권고하고 있습니다. 이로 인해 생산자는 저비용으로 반복적으로 살포하는 대신, 윤작이나 혼합 살포, 새로운 유효 성분의 사용이 필요하게 되므로 해충 방제 프로그램의 비용이 증가합니다. 또한, 기존 제품의 상업적 수명이 단축됨에 따라 신젠타 그룹의 IRAC 그룹 30에 속하는 살충제 등 새로운 작용기전을 가진 제품의 중요성이 커지고 있습니다. 그 결과, 해충 방제 시장은 성장을 이어가고 있지만, 그 중 기존 제품은 안정적인 판매량과 가격을 유지하기가 점점 더 어려워지고 있습니다.

부문별 분석

2025년, 화학적 해충 방제는 해충 방제 시장 점유율의 67.5%를 차지하며, 여전히 압도적인 차이로 최대 부문으로서의 지위를 유지했습니다. 이러한 위상은 광범위한 농지에서 쌓아온 오랜 실적, 강력한 유통망, 그리고 곡물, 면화, 유지종자, 플랜테이션 작물에 걸쳐 발생하는 다양한 복합 해충 문제를 해결할 수 있는 능력을 반영하고 있습니다. 또한, 해충 방제 업계에서 화학적 해충 방제는 새로운 합성 분자가 여전히 기존의 제네릭 계열보다 높은 가격을 유지하고 있기 때문에 상업적으로도 중요한 위치를 계속 차지하고 있습니다. 생물학적 방제는 가장 빠르게 성장하고 있는 부문으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.3%로 성장을 지속하고, 있습니다. 이는 성장의 축이 잔류물 관리와 내성 순환을 핵심으로 하는 프로그램으로 전환되고 있음을 보여줍니다. 중국의 2025년 및 2026년 기술 계획은 생물학적 순환 재배에 대한 추가적인 정책 지원을 제공함으로써, 세계 최대 규모의 작물 보호 시스템 중 하나에 대한 도입을 강화했습니다.

바이엘 AG는 Ginkgo Bioworks사와의 새로운 다년간 제휴를 통해 바이오 농약 플랫폼을 확대하고, 해충 방제 및 지속 가능한 농업 용도를 위한 미생물 제품 개발을 가속화했습니다. 그 결과, 많은 생산자들이 동일한 계절 계획 내에서 화학 농약과 생물 농약을 병용하게 되었기 때문에 해충 방제 시장에서는 더 이상 화학 농약과 생물 농약을 단순히 구분하지 않게 되었습니다. 이 혼합 모델을 통해 화학 농약 시장 규모를 유지하면서, 생물 농약이 해충 방제 시장에서 가장 빠르게 성장하고 있는 부문에서 더 큰 시장 점유율을 확보할 수 있게 될 것입니다.

지역별 분석

2025년, 북미는 해충 방제 시장 점유율의 37.6%를 차지하며 최대 지역 부문이 되었습니다. 이 지역은 확립된 통합 해충 관리(IPM) 시스템, 고품질 화학 농약의 높은 보급률, 그리고 생물 농약 및 종자 처리제의 탄탄한 개발 파이프라인이라는 강점을 활용하고 있습니다. 2025년 미국 환경보호청(EPA)이 최종 확정된 ‘농약 전략’은 약 8,300만 에이커에 달하는 처리 면적에 걸쳐 정밀 살포 및 잔류량 저감 프로그램의 도입을 촉진했습니다. 유럽은 여전히 중요한 고부가가치 지역이며, 규제 강화 및 문서화 기준의 강화로 인해 총 처리 면적의 확대 속도를 웃도는 속도로 제품 구성이 변화하고 있어, 선택적 화학 농약 및 생물학적 수단으로의 지속적인 대체가 진행되고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 5.6%를 나타낼 것으로 예측되는 가장 빠르게 성장하는 지역 부문이며, 해충 방제 시장의 향후 수요 증가에 있어 계속해서 핵심적인 역할을 담당하고 있습니다. 중국이 주요 견인 역할을 하고 있습니다. 해당 국가의 2025년 및 2026년 주요 작물 해충 방제 계획에 생물학적 방제 및 윤작 프로그램이 공식적으로 도입된 데다, 벼와 옥수수 재배 체계에서 매우 대규모의 해충 발생이 예상되기 때문입니다. 이에 따라 해당 지역에서는 수요 증가, 정책에 뒷받침된 생물학적 방제 도입, 그리고 재배 밀도 상승이 맞물려 강력한 성장 기반이 형성되고 있습니다. 남미는 브라질과 아르헨티나에서 대두와 옥수수의 재배 면적이 확대됨에 따라, 한 시즌당 해충 방제 주기 수가 증가하고 있어, 해충 방제 분야에서 계속해서 잠재적인 성장 지역으로 자리매김하고 있습니다. 브라질 국가공급공사(CONAB)는 2025/26년 시즌 대두 수확량이 사상 최고치인 1억 8,010만 메트르톤에 달할 것으로 전망하고 있으며, 대규모 줄 재배 시스템에서 발생하는 애벌레, 매미충, 흡즙성 해충에 대한 방제 프로그램 수요를 견인하고 있습니다. 또한, 해충의 내성이 점차 강해지고 있는 만큼, 생산자들은 살충제 순환 사용 프로그램, 종자 처리 및 생물학적 해충 방제 솔루션의 도입을 추진하고 있습니다.

중동 및 아프리카는 절대적인 규모로 보면 여전히 작지만, 두 지역 모두 해충 방제 시장에서 큰 성장 기회를 지니고 있습니다. 만안 국가들과 튀르키예에서 보호재배가 확대됨에 따라, 채소, 관상용 식물, 묘목 작물 분야에서 생물학적 방제 및 잔류물이 적은 해충 관리의 적용 범위가 넓어지고 있습니다. 아프리카에서는 특히 옥수수 및 기타 주곡 작물의 경우, 침입 해충으로 인한 압박이 여전히 크기 때문에 장기적인 수요가 견조합니다. 안델마트 아프리카는 동아프리카에서 차세대 해충 방제 솔루션을 개발 및 판매하기 위해 2025년에 프로비비와 제휴할 것이라고 발표했습니다. 이는 소규모 농가를 대상으로 한 페로몬 기반 시스템에 대한 상업적 관심이 높아지고 있음을 보여줍니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the insect pest control market size is anticipated to increase from USD 55.23 billion in 2025 to USD 59.65 billion in 2026 and reach USD 73.51 billion by 2031, growing at a CAGR of 4.27% over 2026-2031.

This report is Segmented by Control Method (Chemical, Biological, and Physical), by Crop Type (Grains and Cereals, Fruits and Vegetables, Oilseeds and Pulses, and More), by Mode of Application (Foliar Spray, Seed Treatment, Soil Treatment, and More), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). Market Forecasts in Value (USD).

Global Insect Pest Control Market Trends and Insights

Rising Insect Pressure and Crop-Loss Risk

Global crop production continues to face severe pressure from insect-driven yield losses, which remain one of the most persistent threats to farm profitability. In 2025, the Crop Protection Network anticipated that invertebrate pests reduced corn yields by 4.0% across 29 United States states during the 2024 season, resulting in losses exceeding 610 million bushels, demonstrating the continuing economic burden of insect infestations on modern agriculture. This keeps insect control spending hard to defer even when farm margins tighten, because yield protection remains central to grower economics. The insect pest control market also gains from the rising need to manage multiple pest species within the same season, especially in crops with repeated infestation cycles. That pattern supports a stronger demand for broad programs and favors suppliers that can offer several modes of action within the same insect pest control market.

Regulatory and Retailer Push for Lower-Residue Programs

Tighter environmental oversight and stricter retailer standards are accelerating the shift toward more selective and lower-residue insect control programs. The United States Environmental Protection Agency (EPA) finalized its Insecticide Strategy on April 29, 2025, covering nearly 83 million treated acres and requiring mitigation measures such as spray-drift buffers and runoff controls. In Europe, compliance pressure remains high as pesticide use and documentation receive closer scrutiny, including the broader shift toward digital recording and traceability in farm practices. This raises the value of products that fit integrated pest management (IPM) programs and creates more room for biologicals, pheromone tools, and selective chemistry. The insect pest control market, therefore, shows a clear split between premium programs built around compliance and commodity programs that face greater substitution pressure.

Resistance to Legacy Chemistries

The insect pest control market faces a clear limit due to rising resistance to older chemistries across several key pest complexes. The official 2026 integrated pest management guidance in Baden-Wurttemberg reported super-kdr resistance in oilseed rape flea beetle populations in the Rhine Plain and Kraichgau regions of Germany and advised growers to use alternative active ingredients in those hotspots. This raises program costs because growers need rotations, mixtures, and newer active ingredients instead of lower-cost repeat applications. It also shortens the commercially useful life of established products and increases the importance of novel modes of action, such as Syngenta Group's IRAC group 30 insecticides . The result is that the insect pest control market keeps growing, but legacy products within it face a harder path to stable volume and pricing.

Other drivers and restraints analyzed in the detailed report include:

- Fast Adoption of Biological Control and Bioinsecticides

- Precision Scouting, Drones, and AI Improve Treatment Timing

- Registration and MRL Pressure on Active Ingredients

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Chemical control accounted for 67.5% of the insect pest control market share in 2025, maintaining its position as the largest segment by a wide margin. This position reflects its long record in broad-acre crops, strong distribution coverage, and the ability to address many pest complexes across grains, cotton, oilseeds, and plantation crops. The chemical side of the insect pest control industry also remains commercially important because newer synthetic molecules still command higher pricing than older generic classes. Biological control is the fastest-growing segment, with a 6.3% CAGR during 2026-2031, indicating that growth is shifting toward programs built around residue management and resistance rotation. China's 2025 and 2026 technical plans provided additional policy support for biological rotations, thereby strengthening adoption in one of the world's largest crop protection systems.

Bayer AG expanded its biological crop protection platform through a new multi-year partnership with Ginkgo Bioworks to accelerate the development of microbial products for pest management and sustainable agriculture applications. The practical outcome is that the insect pest control market is no longer simply separating chemical and biological programs, because many growers now use both within the same seasonal plan. That mixed model should maintain the chemical scale while enabling biological products to capture a larger share of the fastest-growing segment of the insect pest control market.

Geography Analysis

North America accounted for 37.6% of the insect pest control market share in 2025, making it the largest regional segment. The region benefits from established integrated pest management systems, high adoption of premium chemistry, and a strong pipeline of biological and seed-applied products. The United States Environmental Protection Agency (EPA) final Insecticide Strategy in 2025 strengthened the case for precision-applied and lower-residue programs across nearly 83 million treated acres. Europe remains an important high-value region where regulatory attrition and more stringent documentation standards are changing the product mix faster than the total treated area, supporting continued substitution toward selective chemistry and biological tools.

Asia-Pacific is the fastest-growing regional segment, with a 5.6% CAGR during 2026-2031, and remains central to future demand expansion in the insect pest control market. China is a major driver because its 2025 and 2026 major crop pest plans formalized biological control plus rotation programs, and projected very large pest incidence across rice and corn systems. This gives the region a strong mix of volume demand, policy-backed biological adoption, and rising crop intensity. South America remains a potential growth region for insect pest control due to the expansion of soybean and corn acreage in Brazil and Argentina, which has increased the number of insect treatment cycles required per season. Brazil's National Supply Company (CONAB) has projected a record soybean harvest for the 2025/26 season of 180.1 million metric tons, driving demand for caterpillar, stink bug, and sucking-pest control programs in large-scale row-crop systems. Additionally, pest resistance is prompting growers to adopt rotational insecticide programs, seed treatments, and biological insect-control solutions.

The Middle East and Africa remain smaller in absolute terms, but both offer significant growth opportunities in the insect pest control market. Protected cultivation in Gulf countries and Turkey is widening the addressable base for biological and low-residue insect management in vegetables, ornamentals, and nursery crops. Africa has strong long-term demand because invasive pest pressure remains high, particularly in maize and other staple crops. Andermatt Africa announced a 2025 partnership with Provivi to develop and distribute next-generation pest control solutions in East Africa, which signals rising commercial interest in pheromone-based systems for smallholder agriculture.

- Syngenta Group Co., Ltd.

- Bayer AG

- BASF SE

- Corteva, Inc.

- FMC Corporation

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- Gowan Company, L.L.C.

- AMVAC Chemical Corporation (American Vanguard Corporation (AVD))

- Pro Farm Group Inc

- Certis USA L.L.C.

- Environmental Science U.S. LLC

- Koppert Biological Systems B.V.

- Biobest Group NV

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising insect pressure and crop-loss risk

- 4.2.2 Regulatory and retailer push for lower-residue programs

- 4.2.3 Fast adoption of biological control and bioinsecticides

- 4.2.4 Precision scouting, drones, and AI improve treatment timing

- 4.2.5 Protected-crop and nursery expansion lifts biocontrol demand

- 4.2.6 Seed-treatment and insect-protection trait stacking

- 4.3 Market Restraints

- 4.3.1 Resistance to legacy chemistries

- 4.3.2 Registration and MRL pressure on active ingredients

- 4.3.3 Generic erosion of blockbuster insecticides

- 4.3.4 Shelf-life and field-performance variability in biologicals

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of new entrants

- 4.6.2 Bargaining power of buyers

- 4.6.3 Bargaining power of suppliers

- 4.6.4 Threat of substitutes

- 4.6.5 Intensity of competitive rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Control Method

- 5.1.1 Chemical Control

- 5.1.2 Biological Control

- 5.1.3 Physical Control

- 5.2 By Crop Type

- 5.2.1 Grains and Cereals

- 5.2.2 Fruits and Vegetables

- 5.2.3 Oilseeds and Pulses

- 5.2.4 Plantation Crops

- 5.2.5 Turf and Ornamentals

- 5.3 By Mode of Application

- 5.3.1 Foliar Spray

- 5.3.2 Seed Treatment

- 5.3.3 Soil Treatment

- 5.3.4 Chemigation

- 5.3.5 Fumigation and Space Treatment

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Italy

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Turkey

- 5.4.5.4 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta Group Co., Ltd.

- 6.4.2 Bayer AG

- 6.4.3 BASF SE

- 6.4.4 Corteva, Inc.

- 6.4.5 FMC Corporation

- 6.4.6 UPL Limited

- 6.4.7 Sumitomo Chemical Co., Ltd.

- 6.4.8 Nufarm Limited

- 6.4.9 Gowan Company, L.L.C.

- 6.4.10 AMVAC Chemical Corporation (American Vanguard Corporation (AVD))

- 6.4.11 Pro Farm Group Inc

- 6.4.12 Certis USA L.L.C.

- 6.4.13 Environmental Science U.S. LLC

- 6.4.14 Koppert Biological Systems B.V.

- 6.4.15 Biobest Group NV