|

시장보고서

상품코드

2066389

특수 화학제품 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Specialty Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

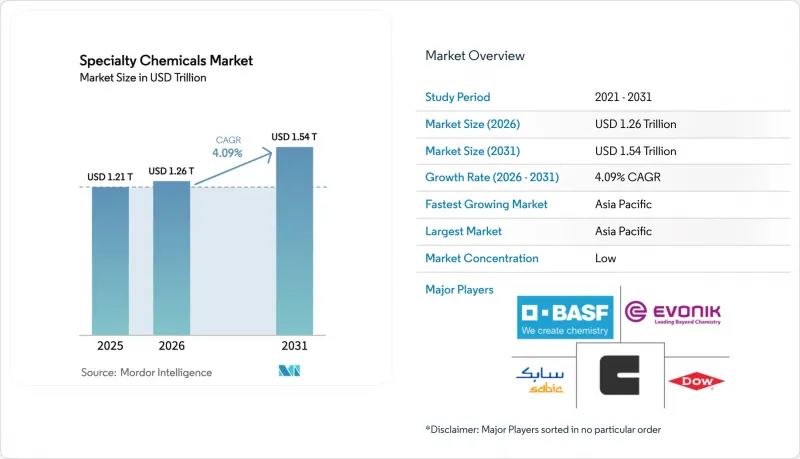

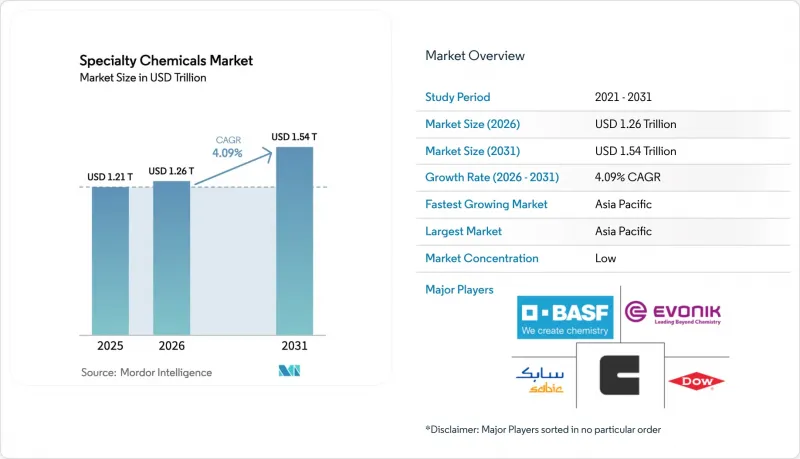

Mordor Intelligence에 의하면, 특수 화학제품 시장 규모는 2025년 1조 2,100억 달러에서 2026년에는 1조 2,600억 달러로 확대되어 2031년까지 1조 5,400억 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 4.09%로 성장할 전망입니다.

본 보고서는 최종 사용 산업별(페인트 및 코팅, 촉매, 건설용 화학제품, 화장품용 화학제품, 염료, 잉크·안료, 전자 화학제품, 수처리용 화학제품, 식품 첨가물, 농약 등) 및 지역별(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 특수 화학제품 시장 동향과 인사이트

아시아태평양 및 GCC 국가들에서 인프라 투자가 급증하면서 건설용 화학제품 수요가 증가하고 있습니다.

사우디아라비아의 NEOM 프로젝트에 더해, UAE의 파이프라인 계획, 싱가포르의 2025년 예상 건설 수요, 그리고 호주의 인프라 계획이 맞물려 폴리카르복실산 에테르계 고성능 감수제, 방수막 및 부식 방지제에 대한 안정적인 수요를 뒷받침하고 있습니다. 그린빌딩 인증 요건을 충족하기 위해, 특히 싱가포르의 ‘슈퍼 로 에너지(Super Low Energy)’ 프로그램에 참여하는 건설업체들은 저VOC 실란트와 속경화형 보수 모르타르의 사용을 점점 더 늘리고 있습니다. 높은 염분 농도의 사막 환경에 대응하고 납기를 단축하기 위해 Sika, Fosroc, Saint-Gobain 등 다국적 공급업체들은 해당 지역 내 혼화제 공장의 생산 능력을 확대되고 있습니다. 만안 지역의 메가 프로젝트에서는 콘크리트 혼합물에 100년의 내구 수명이 요구됨에 따라, 수축 보상제나 결정성 방수재의 사용이 현저히 증가하고 있습니다. 또한, EPC 도급업체는 디지털 트윈 모델을 도입하여 배합 비율을 미세 조정하고 있으며, 그 결과 콘크리트 1입방미터당 고범위 감수제의 소비량이 증가하고 있습니다.

반도체 생산 능력 경쟁이 전자용 화학제품 수요를 견인하고 있습니다.

엔테그리스, 헴록 세미컨덕터, 스미카 일렉트로닉 머티리얼즈는 미국의 ‘CHIPS and Science Act(CHIPS·과학법)’에 따라 자금을 지원받았습니다. 초고순도 용매와 폴리실리콘에 투입되는 이러한 자금은 공급 거점이 아시아에서 미국으로 현저하게 이동하고 있음을 여실히 보여주고 있습니다. SEMI는 300mm 팹 설비에 대한 지출이 증가할 것으로 전망하고 있습니다. 이러한 증가 추세에 따라 과산화수소, 황산, CMP 슬러리 시장이 확대되고 있습니다. 일본의 JSR 인수는 포토레지스트 생산 능력을 국가 이익에 부합하도록 조정하기 위한 전략적 조치입니다. 동시에, 도쿄오카 공업은 파운드리에서의 도입 속도에 맞추어 EUV 등급 제품의 생산을 확대되고 있습니다. 수익을 안정화하기 위해 클린룸용 화학약품 제조업체는 팹과 10년간의 테이크-오어-페이 계약을 체결하고 있습니다. 이는 기존에 웨이퍼 생산량에 연동되던 수익 변동을 완화하기 위한 전략입니다. 첨단 패키징 노드가 발전함에 따라, 칩렛 아키텍처에 필수적인 혁신적인 유전체 페이스트와 저-k 스핀온 소재에 대한 수요가 증가하고 있습니다.

원유 파생상품의 가격 변동이 원자재 비용을 끌어올립니다.

2026년, 브렌트 원유 가격이 하락함에 따라 나프타 크래커의 스프레드는 축소될 것입니다. 이러한 변화는 프로파일렌 및 에틸렌 공급망과 관련된 특수 화학제품 제조업체들에게 이러한 비용을 가격에 반영해야 하는 과제를 안겨줍니다. 2024년, 아시아의 나프타 가격은 등락을 거듭했으나, 2025년에는 하락할 것으로 전망됩니다. 한편, 프로파일렌과 에틸렌의 현물 가격은 여전히 큰 변동을 보이고 있으며, 정유시설의 가동 중단이나 지정학적 사건의 영향을 받고 있습니다. 업계 선두 기업인 BASF나 다우와 달리, 중소규모의 특수 화학제품 제조업체들은 대규모 헤지를 할 여력이 없습니다. 그들은 종종 3개월에 달하는 견적 지연에 직면하고 있으며, 입찰부터 출하까지의 기간 동안 원자재 가격이 급등할 경우 계약상 위약금을 물어야 할 위험에 처해 있습니다. 에보닉사의 숙신산이나 BASF사의 재생 가능 나프타 제조 공정과 같은 바이오 유래 대체품은 어느 정도 도움이 되지만, 가격은 상대적으로 비싼 임베디드니다. 이러한 가격 책정은 특히 이익률이 낮은 용도의 경우, 하류 구매자들에게 과제가 되고 있습니다.

부문별 분석

2025년, 가격의 급등락에도 불구하고 비료 출하량이 견조한 추세를 보였기 때문에 농약은 특수 화학제품 시장 전체 매출의 19.98%를 차지했습니다. 뉴트리엔사는 칼륨 및 질소 비료의 상당한 출하량을 보고했으며, 야라사는 다양한 작물용 영양소를 운송했습니다. 건설용 화학제품 중 특수 화학제품 시장 규모는 GCC(걸프협력회의) 및 아시아태평양의 메가 프로젝트 파이프라인을 배경으로, 2026년부터 2031년까지 연평균 성장률(CAGR) 6.33%로 확대될 것으로 예상되며, 혼화제, 방수재, 보수용 모르타르가 가장 빠르게 부가가치를 창출하는 분야가 될 전망입니다. 신흥 경제국에서는 건축물의 도장 재시공과 폴리머를 많이 사용하는 자동차 부문의 경량화 추세가 뒷받침되면서, 도료 및 코팅재 수요가 견인되고 있습니다. 이러한 추세를 뒷받침하는 사례로, BASF가 2024년에 전기차용으로 최적화된 수성 클리어코트를 출시한 점을 들 수 있습니다. 이는 OEM의 주력 제품에 대한 중요한 기술적 전환을 의미합니다. 전자 화학제품 분야에서는 미국의 보조금 제도와 아시아 지역의 웨이퍼 생산이 지속적으로 확대되는 데 따른 혜택을 누리고 있습니다. 이로 인해 고순도 산, CMP 슬러리, 포토레지스트 수요가 급증하고 있습니다. 한편, 수처리용 화학제품은 PFAS 규제가 호재로 작용하고 있으며, 접착제 및 실런트 수요 증가는 EC용 포장 및 배터리 팩의 개스킷용 내열성 PUR 핫멜트에 대한 수요에 힘입어 견인되고 있습니다.

지역별 분석

아시아태평양은 2025년에 특수 화학제품 매출의 46.94%를 차지해, 2031년까지 연평균 성장률(CAGR) 4.58%를 기록할 전망입니다. 이러한 성장은 주로 중국의 화학 부문이 고부가가치 중간체로 사업 중심을 옮기고 있는 데 힘입은 것이며, 국내 농약 및 폴리머 산업을 장려하는 인도의 지원 정책에 의해 뒷받침되고 있습니다. 구자라트주와 마하라슈트라주에 위치한 인도의 산업 클러스터에서는 수익성이 높은 수출 기회를 염두에 두고 염료 및 안료의 생산 능력을 확대되고 있습니다. 일본과 한국은 2019년 수출 규제 이후 정부의 지원을 받아 설비 투자를 확대한 덕분에 포토레지스트 및 과산화수소 분야에서 높은 점유율을 차지하며 시장을 독점하고 있습니다. 특히, JSR이 재팬 인더스트리얼 파트너스에 인수됨에 따라, 해당 권리가 국내 관리 하에 남게 될 것이 확실해졌습니다. 아세안 지역에서는 베트남에서 급증하고 있는 산업단지 건설 계획과 태국의 EEC 회랑을 통해 혼화제 및 수처리 생산 능력이 강화되고 있습니다. 한편, 싱가포르는 친환경 인증의 최고 기준을 마련하고, 저VOC 배합을 장려하기 위해 노력하고 있습니다.

북미 시장 점유율은 작지만, 그 혁신의 기세는 주목할 만합니다. 이 대륙에서는 1980년대 이후 가장 중요한 원자재의 국내 복귀(리쇼어링) 움직임이 나타나고 있으며, 업스트림 화학제품에 대한 자금 투입과 수요 예측이 그 대표적인 사례입니다. 미국의 자동차 경량화 관련 규제로 인해 탄소섬유 프리프레그와 PEEK에 대한 수요가 증가하고 있습니다. 동시에, PFAS 규제 시행이 임박함에 따라 대체 응집제에 대한 투자가 촉진되고 있습니다. 유럽에서는 개정된 ‘산업 배출 지침’이나 엄격한 폐수 규제에 드러나듯이, 이러한 적극적인 자세가 환경 분야에서의 리더십을 화학제품 수요 증가와 연결시키고 있습니다. 여기에는 막 생물 반응기, PFAS가 포함되지 않은 계면활성제, 바이오 분산제 등이 포함됩니다. 중동의 특수 화학 부문은 사우디 아람코의 야심 찬 하류 부문 투자와 NEOM 메가시티 프로젝트의 혜택을 받고 있습니다. 이 모든 요인들은 부식 방지제, 유전용 살균제, 그리고 고성능 콘크리트 혼화제에 대한 활발한 수요를 창출하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the specialty chemicals market size is expected to increase from USD 1.21 trillion in 2025 to USD 1.26 trillion in 2026 and reach USD 1.54 trillion by 2031, growing at a CAGR of 4.09% over 2026-2031.

This report is Segmented by End-User Industry (Paints and Coatings, Catalysts, Construction Chemicals, Cosmetic Chemicals, Dyes, Inks and Pigments, Electronic Chemicals, Water Treatment Chemicals, Food Additives, Agrochemicals, and More) and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Specialty Chemicals Market Trends and Insights

Infrastructure Spending Boom in Asia-Pacific and GCC Countries Boosts Construction Chemicals

Saudi Arabia's NEOM project, alongside the UAE's pipeline, Singapore's projected construction demand for 2025, and Australia's infrastructure program, are collectively fueling a consistent demand for polycarboxylate ether super-plasticizers, waterproofing membranes, and corrosion inhibitors. In a bid to align with green-building certifications, contractors, particularly in Singapore's Super Low Energy program, are increasingly opting for low-VOC sealants and rapid-cure repair mortars. To cater to the high-salinity desert environments and reduce delivery lead times, multinational suppliers like Sika, Fosroc, and Saint-Gobain are ramping up their regional admixture plants. Given the 100-year service life requirement for concrete blends in Gulf megaprojects, there's a notable surge in the use of shrinkage-compensating agents and crystalline waterproofing. Furthermore, EPC contractors are integrating digital-twin models to fine-tune dosage rates, leading to an uptick in the consumption of high-range water reducers for every cubic meter of concrete.

Semiconductor Capacity Race Spurs Electronic-Grade Chemical Demand

Entegris, Hemlock Semiconductor, and Sumika Electronic Materials received funding under the U.S. CHIPS and Science Act. These funds, directed toward ultra-high-purity solvents and polysilicon, underscore a notable shift in supply hubs from Asia to the U.S. SEMI forecasts higher spending on 300 mm fab equipment. This uptick broadens the market for hydrogen peroxide, sulfuric acid, and CMP slurries. Japan's acquisition of JSR is a strategic move, aligning photoresist capacity with national interests. Concurrently, Tokyo Ohka Kogyo is boosting production of EUV-grade products, adapting to the pace of foundry adoptions. To stabilize revenues, cleanroom chemical manufacturers are entering into 10-year take-or-pay contracts with fabs, a strategy aimed at mitigating the revenue fluctuations historically tied to wafer starts. As advanced packaging nodes evolve, there's a heightened demand for innovative dielectric pastes and low-k spin-on materials, essential for chiplet architectures.

Crude-Derivative Price Volatility Inflates Feedstock Costs

In 2026, as Brent crude prices retreat, naphtha-cracker spreads tighten. This shift creates challenges for specialty formulators linked to propylene and ethylene chains, as they grapple with passing on these costs. In 2024, Asian naphtha prices fluctuated, with forecasts predicting a dip in 2025. Meanwhile, spot prices for propylene and ethylene remain volatile, swaying with refinery downtimes and geopolitical events. Unlike industry giants BASF or Dow, smaller specialty producers operate without the luxury of hedging at scale. They often contend with three-month quotation delays, making them vulnerable to contract penalties if feedstock prices surge between tender and shipment. While bio-alternatives like succinic acid from Evonik and renewable-naphtha routes from BASF offer some respite, they come at a premium. This pricing poses challenges for downstream buyers, especially in applications with tight margins.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Industrial-Water Discharge Norms Fuel Water-Treatment Additives

- Auto Lightweighting Rules Escalate Need for High-Performance Polymers

- VOC Regulations Restrict Solvent-Borne Chemistries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Agrochemicals contributed 19.98% of the overall specialty chemicals market revenue in 2025 as fertilizer volumes held firm despite price turbulence. Nutrien reported notable shipments of potash and nitrogen, while Yara transported various crop nutrients. The specialty chemicals market size for construction chemicals is forecast to expand at a 6.33% CAGR between 2026 and 2031 on the back of GCC and Asia-Pacific megaproject pipelines, positioning admixtures, waterproofing, and repair mortars as the fastest incremental value creators. Emerging economies are driving demand for paints and coatings, bolstered by architectural repainting and lightweighting in the polymer-rich automotive sector. A testament to this trend is BASF's 2024 introduction of waterborne clearcoats tailored for electric vehicles, marking a significant technological shift into mainstream OEM offerings. Electronic chemicals are reaping the benefits of subsidy pools in the U.S. and ongoing expansions in Asia's wafer fabrication. This has led to a surge in demand for high-purity acids, CMP slurries, and photoresists. Meanwhile, water treatment chemicals are capitalizing on PFAS regulations, and the rising demand for adhesives and sealants is driven by e-commerce packaging and the need for heat-resistant PUR hot melts in battery-pack gasketing.

Geography Analysis

Asia-Pacific owned 46.94% of specialty chemicals revenue in 2025 and is tracking a 4.58% CAGR through 2031. This growth is largely driven by China's chemical sector pivoting towards high-end intermediates and bolstered by India's incentive scheme, which champions domestic agrochemicals and polymers. Indian clusters in Gujarat and Maharashtra are ramping up dye and pigment capacities, eyeing lucrative export opportunities. Japan and South Korea, benefiting from government-backed capital expansions post-2019 export restrictions, dominate the market with premium stakes in photoresists and hydrogen peroxide. Notably, JSR's acquisition by Japan Industrial Partners ensures that rights remain under domestic stewardship. In the ASEAN region, Vietnam's burgeoning industrial-park pipeline and Thailand's EEC corridor are enhancing capacity for admixtures and water treatment. Meanwhile, Singapore is setting the gold standard for green certifications, promoting low-VOC formulations.

While North America holds a smaller market share, its intensity of innovation is noteworthy. The continent is witnessing its most significant materials reshoring initiative since the 1980s, highlighted by funding and projected needs for upstream chemicals. U.S. mandates for vehicle lightweighting are driving up demand for carbon-fiber prepregs and PEEK. At the same time, impending PFAS regulations are catalyzing investments in alternative coagulants. Europe's proactive stance, evident in its revamped Industrial Emissions Directive and stringent wastewater mandates, is translating environmental leadership into heightened chemical demand. This includes membrane bioreactors, PFAS-free surfactants, and biobased dispersants. The Middle East's specialty chemicals sector is reaping rewards from Saudi Aramco's ambitious downstream investment and the NEOM megacity project, both of which have a voracious appetite for corrosion inhibitors, oilfield biocides, and high-performance concrete admixtures.

- 3M

- AECI

- Afton Chemical

- Akzo Nobel NV

- Albemarle Corporation

- ALTANA

- Archroma

- Arkema Group

- Ashland

- Asian Paints

- Axalta Coating Systems

- Baker Hughes Company

- BASF SE

- Berger Paints India Limited

- Buckman

- Chevron Corporation

- Clariant

- Corteva

- Covestro AG

- DIC Corporation

- Dow

- DSM

- DuPont

- Eastman Chemical Company

- Ecolab

- Evonik Industries AG

- Exxon Mobil Corporation

- Ferro Corporation

- Flint Group

- FMC Corporation

- GCP Applied Technologies Inc.

- H.B. Fuller Company

- Halliburton

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Holcim

- Huntsman International LLC

- Infineum International Limited

- Kemira

- KRONOS Worldwide Inc.

- Kurita Water Industries Ltd

- LANXESS

- Lonza

- MAPEI SpA

- Merck KGaA

- NIPSEA GROUP

- Nouryon

- Nutrien Ltd

- Pidilite Industries Ltd

- PPG Industries Inc.

- Procter & Gamble

- RPM International Inc.

- SABIC

- Saint-Gobain

- Schlumberger Limited

- Sika AG

- Solenis

- Solvay

- Syngenta

- The Chemours Company

- The Lubrizol Corporation

- The Sherwin-Williams Company

- Venator Materials PLC

- Veolia

- W. R. Grace & Co.

- Wacker Chemie AG

- Yara

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure spending boom in Asia-Pacific and GCC Countries boosts construction chemicals

- 4.2.2 Semiconductor capacity race spurs electronic-grade chemical demand

- 4.2.3 Tightening industrial-water discharge norms fuel water-treatment additives

- 4.2.4 Auto lightweighting rules escalate need for high-performance polymers

- 4.2.5 Perovskite PV scale-up creates niche for specialty conductive inks

- 4.3 Market Restraints

- 4.3.1 Crude-derivative price volatility inflates feedstock costs

- 4.3.2 VOC regulations restrict solvent-borne chemistries

- 4.3.3 Urban-farming DIY bio-inputs erode small-lot agrochemical sales

- 4.4 Value Chain Analysis

- 4.5 Raw-Material Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By End-User Industry

- 5.1.1 Paints and Coatings

- 5.1.1.1 Market Dynamics

- 5.1.1.2 Application

- 5.1.1.2.1 Architectural

- 5.1.1.2.2 Automotive

- 5.1.1.2.3 Industrial

- 5.1.1.2.4 Wood

- 5.1.1.2.5 Other Applications

- 5.1.2 Catalysts

- 5.1.2.1 Market Dynamics

- 5.1.2.2 Function

- 5.1.2.2.1 Chemical Synthesis Catalysts

- 5.1.2.2.2 Petroleum Refining Catalysts

- 5.1.2.2.3 Polymerization Catalysts

- 5.1.3 Construction Chemicals

- 5.1.3.1 Market Dynamics

- 5.1.3.2 Application

- 5.1.3.2.1 Commercial

- 5.1.3.2.2 Industrial

- 5.1.3.2.3 Infrastructure

- 5.1.3.2.4 Residential

- 5.1.3.2.5 Public Space

- 5.1.4 Cosmetic Chemicals

- 5.1.4.1 Market Dynamics

- 5.1.4.2 Application

- 5.1.4.2.1 Hair Care

- 5.1.4.2.2 Skin Care

- 5.1.4.2.3 Oral Care

- 5.1.4.2.4 Personal Hygiene

- 5.1.4.2.5 Other Applications

- 5.1.5 Dyes, Inks, and Pigments

- 5.1.5.1 Market Dynamics

- 5.1.5.2 Type

- 5.1.5.2.1 Inks

- 5.1.5.2.2 Dyes

- 5.1.5.2.3 Organic Pigments

- 5.1.5.2.4 Inorganic Pigments

- 5.1.6 Electronic Chemicals

- 5.1.6.1 Market Dynamics

- 5.1.6.2 Application

- 5.1.6.2.1 Semiconductors and Integrated Circuits

- 5.1.6.2.2 Printed Circuit Boards

- 5.1.7 Water Treatment Chemicals

- 5.1.7.1 Market Dynamics

- 5.1.7.2 Function

- 5.1.7.2.1 Flocculants

- 5.1.7.2.2 Coagulants

- 5.1.7.2.3 Biocides and Disinfectants

- 5.1.7.2.4 Defoamers and Defoaming Agents

- 5.1.7.2.5 pH Adjusters and Softeners

- 5.1.7.2.6 Other Functions

- 5.1.8 Food Additives

- 5.1.8.1 Market Dynamics

- 5.1.8.2 Type

- 5.1.8.2.1 Natural Additives

- 5.1.8.2.2 Synthetic Additives

- 5.1.9 Agrochemicals

- 5.1.9.1 Market Dynamics

- 5.1.9.2 Type

- 5.1.9.2.1 Fertilizers

- 5.1.9.2.2 Herbicide

- 5.1.9.2.3 Fungicide

- 5.1.9.2.4 Insecticide

- 5.1.9.2.5 Nematicide

- 5.1.9.2.6 Molluscicide

- 5.1.9.2.7 Other Crop Protection Chemicals

- 5.1.10 Industrial and Institutional Cleaners

- 5.1.10.1 Market Dynamics

- 5.1.10.2 Application

- 5.1.10.2.1 General Purpose Cleaners

- 5.1.10.2.2 Disinfectants and Sanitizers

- 5.1.10.2.3 Laundry Care Products

- 5.1.10.2.4 Vehicle Wash Products

- 5.1.11 Lubricant Additives

- 5.1.11.1 Market Dynamics

- 5.1.11.2 Product Type

- 5.1.11.2.1 Dispersants and Emulsifiers

- 5.1.11.2.2 Detergents

- 5.1.11.2.3 Oxidation Inhibitors

- 5.1.11.2.4 Extreme-pressure Additives and Anti-wear Additives

- 5.1.11.2.5 Viscosity Index Modifiers

- 5.1.11.2.6 Friction Modifiers

- 5.1.11.2.7 Corrosion Inhibitors

- 5.1.11.2.8 Other Product Types

- 5.1.12 Mining Chemicals

- 5.1.12.1 Market Dynamics

- 5.1.12.2 Function

- 5.1.12.2.1 Flotation Chemicals

- 5.1.12.2.2 Extraction Chemicals

- 5.1.12.2.3 Grinding Aids

- 5.1.13 Oilfield Chemicals

- 5.1.13.1 Market Dynamics

- 5.1.13.2 Application

- 5.1.13.2.1 Biocide

- 5.1.13.2.2 Corrosion and Scale Inhibitor

- 5.1.13.2.3 Demulsifier

- 5.1.13.2.4 Polymer

- 5.1.13.2.5 Surfactant

- 5.1.13.2.6 Other Chemical Types

- 5.1.14 Adhesives and Sealants

- 5.1.14.1 Market Dynamics

- 5.1.14.2 Technology

- 5.1.14.2.1 Water-borne Adhesives

- 5.1.14.2.2 Solvent-borne Adhesives

- 5.1.14.2.3 Hot-melt Adhesives

- 5.1.14.2.4 Reactive Adhesives

- 5.1.14.2.5 Other Adhesives

- 5.1.14.2.6 Sealants

- 5.1.15 Plastic Additives

- 5.1.15.1 Market Dynamics

- 5.1.15.2 Plastic Type

- 5.1.15.2.1 Polyethylene (PE)

- 5.1.15.2.2 Polystyrene (PS)

- 5.1.15.2.3 Polypropylene (PP)

- 5.1.15.2.4 Polyamide (PA)

- 5.1.15.2.5 Polyethylene Terephthalate (PET)

- 5.1.15.2.6 Polyvinyl Chloride (PVC)

- 5.1.15.2.7 Polycarbonate (PC)

- 5.1.15.2.8 Other Plastic Types

- 5.1.16 Rubber Processing Chemicals

- 5.1.16.1 Market Dynamics

- 5.1.16.2 Application

- 5.1.16.2.1 Tire

- 5.1.16.2.2 Non-tire

- 5.1.17 Specialty Polymers

- 5.1.17.1 Market Dynamics

- 5.1.18 Textile Chemicals

- 5.1.18.1 Market Dynamics

- 5.1.18.2 Application

- 5.1.18.2.1 Coating and Sizing Chemicals

- 5.1.18.2.2 Colorants and Auxiliaries

- 5.1.18.2.3 Finishing Agents

- 5.1.18.2.4 Desizing Agents

- 5.1.18.2.5 Other Application

- 5.1.1 Paints and Coatings

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 ASEAN Countries

- 5.2.1.6 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.3.1 Adhesives and Sealants

- 6.3.2 Agrochemicals

- 6.3.3 Construction Chemicals

- 6.3.4 Lubricants and Oil Additives

- 6.3.5 Mining Chemicals

- 6.3.6 Oilfield Chemicals

- 6.3.7 Paints and Coatings

- 6.3.8 Specialty Polymers

- 6.3.9 Water Treatment Chemicals

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 AECI

- 6.4.3 Afton Chemical

- 6.4.4 Akzo Nobel NV

- 6.4.5 Albemarle Corporation

- 6.4.6 ALTANA

- 6.4.7 Archroma

- 6.4.8 Arkema Group

- 6.4.9 Ashland

- 6.4.10 Asian Paints

- 6.4.11 Axalta Coating Systems

- 6.4.12 Baker Hughes Company

- 6.4.13 BASF SE

- 6.4.14 Berger Paints India Limited

- 6.4.15 Buckman

- 6.4.16 Chevron Corporation

- 6.4.17 Clariant

- 6.4.18 Corteva

- 6.4.19 Covestro AG

- 6.4.20 DIC Corporation

- 6.4.21 Dow

- 6.4.22 DSM

- 6.4.23 DuPont

- 6.4.24 Eastman Chemical Company

- 6.4.25 Ecolab

- 6.4.26 Evonik Industries AG

- 6.4.27 Exxon Mobil Corporation

- 6.4.28 Ferro Corporation

- 6.4.29 Flint Group

- 6.4.30 FMC Corporation

- 6.4.31 GCP Applied Technologies Inc.

- 6.4.32 H.B. Fuller Company

- 6.4.33 Halliburton

- 6.4.34 Henkel AG & Co. KGaA

- 6.4.35 Hexcel Corporation

- 6.4.36 Holcim

- 6.4.37 Huntsman International LLC

- 6.4.38 Infineum International Limited

- 6.4.39 Kemira

- 6.4.40 KRONOS Worldwide Inc.

- 6.4.41 Kurita Water Industries Ltd

- 6.4.42 LANXESS

- 6.4.43 Lonza

- 6.4.44 MAPEI SpA

- 6.4.45 Merck KGaA

- 6.4.46 NIPSEA GROUP

- 6.4.47 Nouryon

- 6.4.48 Nutrien Ltd

- 6.4.49 Pidilite Industries Ltd

- 6.4.50 PPG Industries Inc.

- 6.4.51 Procter & Gamble

- 6.4.52 RPM International Inc.

- 6.4.53 SABIC

- 6.4.54 Saint-Gobain

- 6.4.55 Schlumberger Limited

- 6.4.56 Sika AG

- 6.4.57 Solenis

- 6.4.58 Solvay

- 6.4.59 Syngenta

- 6.4.60 The Chemours Company

- 6.4.61 The Lubrizol Corporation

- 6.4.62 The Sherwin-Williams Company

- 6.4.63 Venator Materials PLC

- 6.4.64 Veolia

- 6.4.65 W. R. Grace & Co.

- 6.4.66 Wacker Chemie AG

- 6.4.67 Yara

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment