|

시장보고서

상품코드

2066411

모바일 헬스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Mobile Health - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

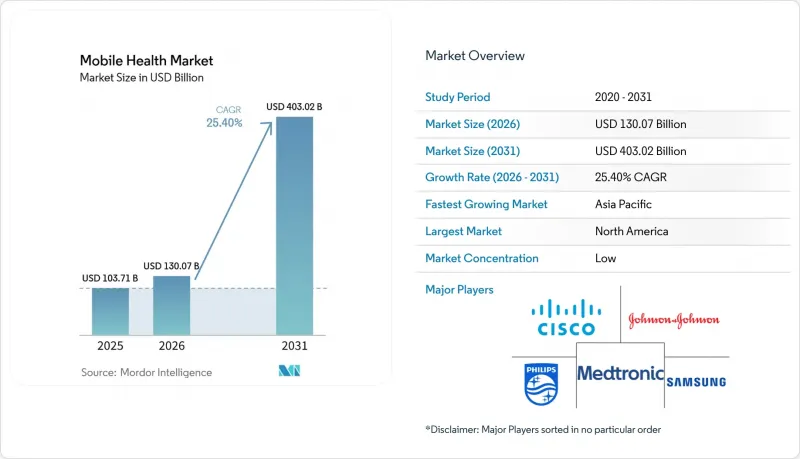

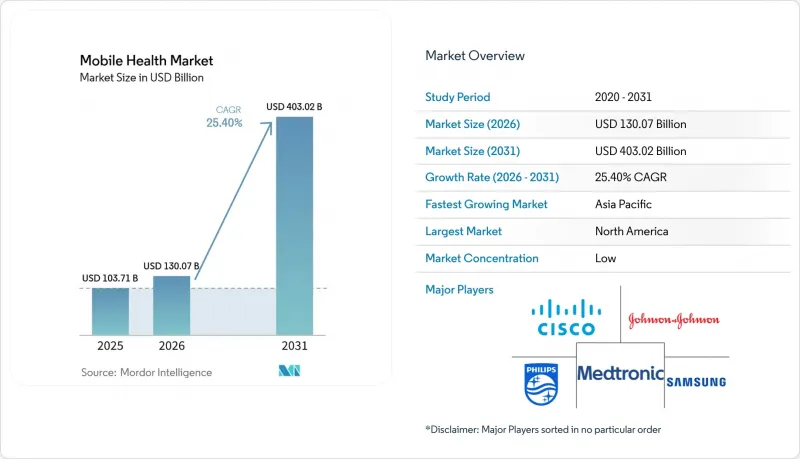

Mordor Intelligence에 의하면, 2026년 모바일 헬스 시장 규모는 1,300억 7,000만 달러로 추정되고 2025년 1,037억 1,000만 달러에서 확대해, 2031년에는 4,030억 2,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지의 연평균 성장률(CAGR)은 25.4%를 나타낼 것으로 전망됩니다.

본 보고서는 서비스 유형(치료 서비스, 진단 서비스, 모니터링 서비스(원격 환자 모니터링 기기 등) 등), 기기 유형(혈당 측정기 등), 용도(심혈관 질환 관리, 당뇨병 관리 등), 이해관계자(모바일 네트워크 사업자 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 모바일 헬스 시장 동향 및 인사이트

m헬스 플랫폼과 각국의 전자건강기록(EHR) 시스템 간의 통합이 임상 현장에서의 도입을 가속화하고 있습니다.

앱의 데이터가 전자건강기록(EHR)에 직접 연동되면 모바일 헬스 시장의 도입이 가속화될 것입니다. 이러한 변화는 현재 걸프협력회의(GCC) 회원국 병원들에서 나타나고 있으며, 공공 의료 기관의 4분의 3 이상이 모바일 인터페이스를 제공합니다. 임상팀에서는 중복 입력 감소가 보고되었으며, 상호운용성 덕분에 인지적 부담이 줄어들어 환자와의 소통에 할애할 시간을 확보할 수 있게 되었다는 점이 시사되고 있습니다. 간과되기 쉬운 결과 중 하나로, 견고한 애플리케이션 프로그래밍 인터페이스(API)를 제공하는 벤더가 환자의 시간 경과에 따른 정보에 대한 사실상 게이트키퍼 역할을 하고 있다는 점을 들 수 있습니다. 이러한 새로운 의존 관계로 인해 의료 시스템은 상호 운용성 분야의 선도 기업들과 장기 계약을 체결하게 되었으며, 구매 결정은 개별 솔루션보다는 플랫폼 쪽으로 기울고 있습니다. 따라서 모바일 헬스 업계에서는 통합 분야 인재 확보가 채용의 최우선 과제로 부상하고 있으며, 단기적으로는 인터페이스 엔지니어의 임금 상승이 예상됩니다. 데이터 공유 기준을 법제화하는 국가가 늘어남에 따라, 경쟁 우위는 기능의 수뿐만 아니라 규정 준수 대응 속도에 달려 있을 것입니다.

원격 환자 모니터링에 대한 보험 급여 코드 확대

미국 메디케어·메디케이드 서비스 센터(CMS)의 최신 규정에 따라 ‘원격 생리학적 모니터링’과 ‘원격 치료 모니터링’에 대해 각각 다른 지급 방식이 도입됨에 따라, 모바일 헬스 시장에 진출하는 기업들에게 보다 명확한 사업 모델이 구축되었습니다. 과거에는 연결형 기기 처방에 주저하던 의료 제공업체들도 현재는 예측 가능한 수익원을 확보하게 되었으며, 그 결과 병원 조달 팀은 시범 프로젝트가 아닌 전사적 플랫폼의 표준화를 추진하고 있습니다. 그 파급 효과로 인해 재무 책임자와 임상 리더 간의 협력이 더욱 강화되고 있습니다. 왜냐하면, 보상 최적화는 케어 경로의 재설계와 뗄 수 없는 관계에 있기 때문입니다. 이러한 연동을 통해 기술 공급업체들은 센서 하드웨어에 요금 분석 기능을 포함하도록 장려받고 있으며, 이에 따라 제공 내용은 단순한 기기 판매에서 수익성 향상으로 이어지는 서비스로 변화하고 있습니다. 여기서 도출되는 새로운 결론은 상환에 관한 지식이 제품 관리자의 핵심 역량이 되어가고 있다는 점이며, 이는 5년 전에는 존재하지 않았던 경력 경로를 시사합니다. 보험사들이 미국 이외의 지역에서도 이러한 코드를 채택함에 따라, 선행 기업들은 검증된 청구 템플릿을 새로운 시장에 적용하여 수익 창출까지 걸리는 기간을 단축할 수 있을 것입니다.

임상적 검증과 실제 임상 증거의 부족이 의사의 앱 처방을 저해하고 있습니다.

미국 식품의약국(FDA)은 500개 이상의 AI 도구를 승인했으나, 그중 상당수는 장기적인 예후 데이터가 부족하여 의사들은 검증되지 않은 앱의 처방에 소극적인 태도를 보이고 있습니다. 비교 연구에 따르면, 일반 소비자를 대상으로 한 웨어러블 기기는 이식형 모니터에 비해 심방세동의 발생을 감지하는 빈도가 낮은 것으로 나타나, 의사들의 회의적인 태도를 더욱 강화하고 있습니다. 이러한 신뢰성의 격차로 인해, 환자가 생성하는 데이터는 증가하고 있음에도 불구하고 임상적 판단에 거의 반영되지 않는 양극화가 발생하고 있으며, 이러한 비효율성은 양측 모두에게 불만의 원인이 되고 있습니다. 이에 대응하여 각 벤더사는 디지털 도구의 개발 주기에 맞춘 실용적인 임상시험을 실시하기 위해 학술 기관과 제휴하여 증거 생성 기간을 단축하고 있습니다. 그 결과, 모바일 헬스 업계에서는 소프트웨어의 반복 개발과 무작위 대조군 연구 기법을 융합한 하이브리드 비즈니스 모델이 채택되기 시작했습니다. 이는 과거에는 양립할 수 없는 것으로 여겨졌던 운영상의 융합입니다. 새로운 인사이트로, 제품이 보험 적용 목록에 등재되기 위해서는 그 주장이 동료 심사를 통과해야 하므로, 시장 출시 팀에게 통계적 소양이 필수적이라는 점을 들 수 있습니다.

부문별 분석

모니터링 서비스는 2025년에 모바일 헬스 시장의 45.30% 점유율을 차지했습니다. 이는 의료 제공업체에게 예측 가능한 현금 흐름을 보장하는 견고한 상환 코드에 의해 뒷받침되고 있습니다. 이러한 시장 규모상의 우위는 매일 수집되는 생리학적 데이터를 바탕으로 적시에 개입하는 만성 질환 프로그램에서 비롯된 것으로, 이러한 노력을 통해 재입원으로 인한 불이익이 완화됩니다. 진단 분야는 현재 규모가 작지만, AI를 활용한 도구가 초기 연구 단계에서 전문의 수준의 정확도를 보여주고 있는 만큼, 2031년까지 연평균 성장률(CAGR) 26.3%로 확대될 것으로 예측됩니다. 이러한 추세는 분야 간의 융합을 시사하고 있으며, 플랫폼에서는 모니터링 기능과 진단 기능을 모두 통합하는 경향이 강해지고 있어, 카테고리 간의 경계가 모호해지고 있습니다. 이로부터 즉시 도출되는 결론은 단일 기기가 이중 역할을 수행할 경우, 서비스의 이중 계산을 방지하기 위해 상환 체계를 재검토해야 할 수도 있다는 점입니다. 이 분야의 융합을 예견하는 이해관계자들은 선제적으로 청구 코드를 조정함으로써 선구자로서의 우위를 확보할 수 있을 것입니다.

혈당 측정기는 디바이스 부문 내 모바일 헬스 시장 규모의 27.60%를 차지하고 있으며, 이러한 압도적인 점유율은 전 세계 당뇨병 유병률과 엄격한 혈당 관리에 대한 임상적 필요성으로 설명될 수 있습니다. 쌀알만 한 크기로 최장 1년간 지속되는 이식형 센서 등의 지속적인 혁신을 통해 교체 주기가 연장될 것으로 기대되며, 그 결과 수익 모델이 구독형 분석으로 재편될 전망입니다. 호흡 모니터 시장은 2031년까지 연평균 성장률(CAGR) 27.2%를 나타낼 것으로 전망되며, 팬데믹 이후 폐 건강에 대한 관심이 높아진 흐름을 타고, 주관적인 증상이 나타나기 전에 상태 악화를 감지하는 머신러닝 알고리즘을 활용하고 있습니다. 이러한 동향을 통해 추측할 수 있는 것은 혈당, 호흡, 심박수 데이터를 통합하는 멀티센서 기기가 단일 매개변수 하드웨어 시장을 잠식할 가능성이 있다는 점입니다. 따라서 공급업체는 틈새 시장에서 리더십을 유지할지, 아니면 플랫폼 전략으로 전환할지 평가해야 합니다.

지역별 분석

연평균 성장률(CAGR) 28.7%의 성장이 예상되는 아시아태평양은 의료 서비스가 충분히 제공되지 않는 대규모 인구층이 존재한다는 점과, 병원 내 5G 회랑에 대한 정부의 투자 혜택을 받고 있습니다. 인도의 헬스테크 스타트업들은 전 세계의 자본을 유치하고 있는 반면, 중국의 민간 독립형 5G 네트워크 시범 프로그램은 현지 혁신을 두드러지게 하고 있습니다. 이 지역에서는 전통 의학을 디지털 플랫폼에 통합하려는 움직임이 보이며, 문화에 부합하는 참여 모델이 제공되고 있는데, 이는 전 세계적으로 제품을 현지화하는 데 참고가 될 수 있습니다. 새로운 시사점으로, 컨텐츠 현지화가 불가능한 다국적 기업은 기술적으로 뛰어나더라도 정체될 위험에 직면할 가능성이 있습니다.

유럽은 혁신과 환자 보호의 균형을 도모하는 ‘일반 데이터 보호 규정(GDPR(EU 개인정보보호규정))’ 등의 규제 체계를 통해 확고한 입지를 유지하고 있습니다. 중동의 ‘비전 2030’ 이니셔티브는 민관 협력을 촉진하여 원격 진료 건수를 늘리는 한편, 걸프 지역을 AI 분류 도구의 실증 거점으로 자리매김하고 있습니다. 남미의 도입 곡선을 보면, 합리적인 가격이 보급을 주도하고 있음을 알 수 있습니다. 저가형 스마트폰과 선불 데이터 요금제의 조합 덕분에 브라질 내륙 지역의 인터넷 접속이 확대되고 있습니다. 이러한 지역들의 공통점은 규제 차이가 존재하기 때문에 공급업체들이 효율적으로 규모를 확대하기 위해 규정 준수 기능을 모듈화해야 한다는 점입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, mobile health market size in 2026 is estimated at USD 130.07 billion, growing from 2025 value of USD 103.71 billion with 2031 projections showing USD 403.02 billion, growing at 25.4% CAGR over 2026-2031.

This report is Segmented by Service Type (Treatment Services, Diagnostic Services, Monitoring Services [Remote Patient Monitoring Devices, and More], and More), Device Type (Blood Glucose Monitors, and More), Application (Cardiovascular Disease Management, Diabetes Management, and More), Stakeholder (Mobile Network Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Mobile Health Market Trends and Insights

Integration of mHealth Platforms with National EHR Systems Accelerating Clinical Adoption

Mobile Health market adoption accelerates when data from apps flows directly into Electronic Health Records, a shift now visible in Gulf Cooperation Council hospitals where more than three-quarters of public facilities expose mobile interfaces. Clinical teams report fewer duplicate entries, suggesting that interoperability reduces cognitive load and frees time for patient engagement. An overlooked consequence is that vendors supplying robust application programming interfaces become de-facto gatekeepers of longitudinal patient information. This new dependency encourages health systems to negotiate long-term contracts with interoperability leaders, tilting purchasing decisions toward platforms over point solutions. The Mobile Health industry therefore sees integration talent emerge as a top hiring priority, an inference that suggests wage inflation for interface engineers in the short term. As more countries legislate data-sharing standards, competitive advantage will hinge on speed of compliance rather than on feature count alone.

Expansion of Remote Patient-Monitoring Reimbursement Codes

The latest Centers for Medicare & Medicaid Services rules introduce distinct payment pathways for Remote Physiologic Monitoring and Remote Therapeutic Monitoring, creating a clearer business case for Mobile Health market participants. Providers that once hesitated to prescribe connected devices now receive predictable revenue streams, which in turn drives hospital procurement teams to standardize on enterprise-wide platforms instead of pilot projects. A knock-on effect is a deeper partnership between financial officers and clinical leaders, because reimbursement optimization becomes inseparable from care-path redesign. This linkage is nudging technology suppliers to bundle billing analytics with sensor hardware, transforming their offering from device sales to margin-enhancement services. The fresh inference is that reimbursement literacy becomes a core competency for product managers, signaling a career pathway that did not exist five years ago. As payers replicate these codes outside the United States, first movers will likely transplant proven billing templates into new territories and shorten time to profitability.

Limited Clinical Validation & Real-World Evidence Undermining Physician Prescription of Apps

Although the Food and Drug Administration has cleared more than 500 artificial-intelligence tools, many lack longitudinal outcome data, and physicians hesitate to prescribe unvalidated apps. Comparative studies show consumer wearables detecting fewer atrial-fibrillation events than implantable monitors, reinforcing physician skepticism. This credibility gap leads to a dichotomy where patient-generated data proliferates but seldom informs clinical decisions, an inefficiency that frustrates both parties. Vendors respond by partnering with academic centers for pragmatic clinical trials that align with digital-tool development cycles, shortening evidence generation timelines. The Mobile Health industry consequently adopts hybrid business models that blend software iteration with randomized-controlled methodologies, an operational convergence once considered incompatible. The new inference is that statistical literacy becomes essential for go-to-market teams, as product claims must withstand peer review to win formulary placement.

Other drivers and restraints analyzed in the detailed report include:

- Sensor Miniaturization & Battery Advances Enabling Medical-Grade Wearables

- Consumer Shift Toward On-Demand Virtual Care via App-Store Ecosystems

- Interoperability Challenges with Legacy Hospital IT Slowing Enterprise Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring services captured 45.30 % Mobile Health market share in 2025, anchored by robust reimbursement codes that secure predictable cash flows for providers. Their market size advantage stems from chronic-disease programs that rely on daily physiologic data to trigger timely interventions, a practice that lowers readmission penalties. Diagnostics, though smaller today, are forecast to expand at a 26.3 % CAGR to 2031 as AI-enhanced tools demonstrate specialist-level accuracy in early studies. This momentum suggests convergence: platforms increasingly bundle both monitoring and diagnostic functionality, blurring categorical boundaries. An immediate inference is that reimbursement frameworks may need revision to avoid double-counting services when a single device performs dual roles. Stakeholders that anticipate this merger of categories could pre-emptively align billing codes and secure first-mover advantage.

Blood-glucose monitors account for 27.60 % of the Mobile Health market size in the device category, a dominance explained by global diabetes prevalence and the clinical imperative for tight glycemic control. Continuous innovation, such as rice-sized implantable sensors lasting up to a year, promises to extend replacement cycles and thus reshape revenue models toward subscription analytics. Respiratory monitors, projected at 27.2 % CAGR to 2031, ride a wave of post-pandemic awareness of pulmonary health and leverage machine-learning algorithms that flag deterioration before subjective symptoms emerge. An inference from these trajectories is that multi-sensor devices integrating glucose, respiratory, and cardiac data could cannibalize single-parameter hardware. Suppliers must therefore evaluate whether to protect niche leadership or pivot to platform strategies.

Geography Analysis

Asia-Pacific, projected to grow at 28.7% CAGR, benefits from large underserved populations and government investments in 5G hospital corridors. Indian health-tech start-ups draw global capital, while Chinese pilot programs for private standalone 5G networks showcase local innovation. The region's willingness to integrate traditional medicine within digital platforms offers culturally tuned engagement models that could inspire global product adaptations. A new inference is that multinationals unable to localize content risk stagnation despite technical excellence.

Europe maintains a strong position owing to regulatory frameworks like the General Data Protection Regulation that balance innovation with patient safeguarding. The Middle East's Vision 2030 initiatives foster public-private partnerships, propelling teleconsultation volumes and positioning the Gulf as a proving ground for AI triage tools. South America's adoption curve reveals that affordability drives uptake: low-cost smartphones paired with prepaid data bundles broaden access in Brazil's interior. An inference across these regions is that regulatory heterogeneity will compel vendors to modularize compliance features to scale efficiently.

- Apple

- Alphabet Inc. (Google)

- Samsung Group

- Medtronic

- Koninklijke Philips

- OMRON

- Johnson & Johnson (Verily)

- Teladoc Health

- Dexcom

- Cisco Systems

- Oracle

- Veradigm Inc.

- Athenahealth

- AliveCor

- AirStrip Technologies Inc.

- Babylon Holdings Limited

- Qualcomm Life Inc.

- Wellmo Mobile Wellness Solutions MWS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of mHealth Platforms with National EHR Systems Accelerating Clinical Adoption

- 4.2.2 Expansion of Remote Patient-Monitoring Reimbursement Codes

- 4.2.3 Sensor Miniaturization & Battery Advances Enabling Medical-Grade Wearables

- 4.2.4 Consumer Shift Toward On-Demand Virtual Care via App-Store Ecosystems

- 4.2.5 Corporate Wellness Programs Scaling App Subscriptions Through Bundled Health Insurance

- 4.3 Market Restraints

- 4.3.1 Limited Clinical Validation & Real-World Evidence Undermining Physician Prescription of Apps

- 4.3.2 Interoperability Challenges with Legacy Hospital IT Slowing Enterprise Deployments

- 4.3.3 Heightened Data-Privacy Concerns Reducing Patient Consent Rates in High-Income Markets

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Treatment Services

- 5.1.1.1 Independent Aging Solutions

- 5.1.1.2 Chronic Disease Management

- 5.1.2 Diagnostic Services

- 5.1.3 Monitoring Services

- 5.1.3.1 Remote Patient Monitoring Devices

- 5.1.3.2 Medical Call Centers Manned by Healthcare Professionals

- 5.1.3.3 Tele-consultation

- 5.1.3.4 Post-Acute Care Services

- 5.1.4 Wellness & Fitness Solutions

- 5.1.5 Other Services

- 5.1.1 Treatment Services

- 5.2 By Device Type

- 5.2.1 Blood Glucose Monitors

- 5.2.2 Cardiac Monitors

- 5.2.3 Hemodynamic Monitors

- 5.2.4 Neurological Monitors

- 5.2.5 Respiratory Monitors

- 5.2.6 Body & Temperature Monitors

- 5.2.7 Remote Patient Monitoring Devices

- 5.2.8 Other Device Types

- 5.3 By Application

- 5.3.1 Cardiovascular Disease Management

- 5.3.2 Diabetes Management

- 5.3.3 Mental Health & Behavioral Disorders

- 5.3.4 Women's Health & Fertility Tracking

- 5.3.5 Fitness & Lifestyle Tracking

- 5.4 By Stakeholder

- 5.4.1 Mobile Network Operators

- 5.4.2 Healthcare Providers

- 5.4.3 Application / Content Players

- 5.4.4 Payers & Employers

- 5.4.5 Other Stakeholders

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Apple Inc.

- 6.3.2 Alphabet Inc. (Google)

- 6.3.3 Samsung Electronics Co. Ltd.

- 6.3.4 Medtronic PLC

- 6.3.5 Koninklijke Philips N.V.

- 6.3.6 Omron Corporation

- 6.3.7 Johnson & Johnson (Verily)

- 6.3.8 Teladoc Health Inc.

- 6.3.9 Dexcom Inc.

- 6.3.10 Cisco Systems Inc.

- 6.3.11 Oracle Corporation (Cerner)

- 6.3.12 Veradigm Inc.

- 6.3.13 athenahealth Inc.

- 6.3.14 AliveCor Inc.

- 6.3.15 AirStrip Technologies Inc.

- 6.3.16 Babylon Holdings Limited

- 6.3.17 Qualcomm Life Inc.

- 6.3.18 Wellmo Mobile Wellness Solutions MWS Oy

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment