|

시장보고서

상품코드

2066450

암 바이오마커 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cancer Biomarkers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

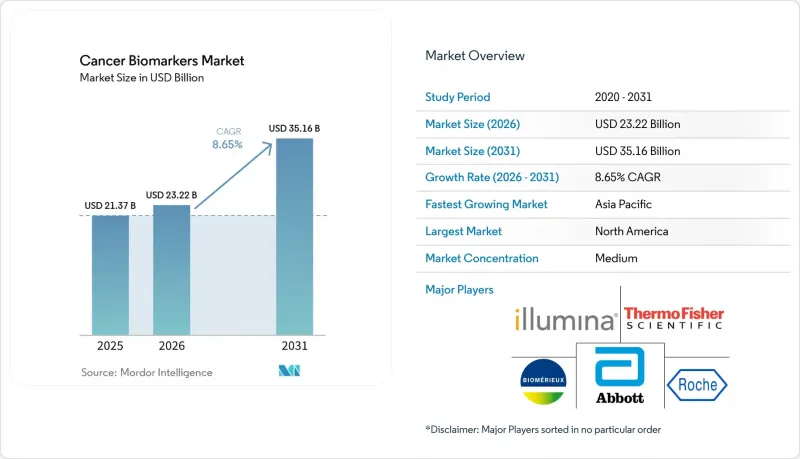

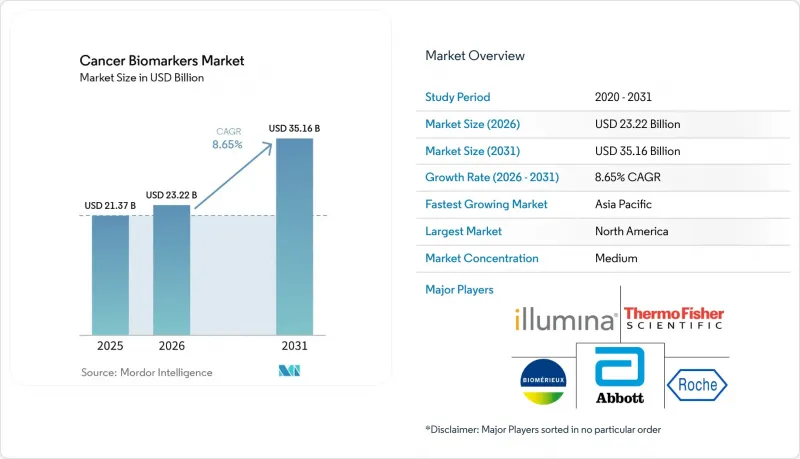

Mordor Intelligence에 의하면, 암 바이오마커 시장 규모는 2025년에 213억 7,000만 달러로 평가되었습니다. 2026년 232억 2,000만 달러에서 2031년까지 351억 6,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 8.65%를 나타낼 전망입니다.

본 보고서는 질환별(유방암, 폐암, 전립선암 등), 생체분자 유형별(단백질 바이오마커 등), 프로파일링 기술별(오믹스 기술, 영상 진단 기술 등), 최종 사용자별(병원 및 진료소 등), 지역별(북미, 유럽, 아시아태평양 등)으로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 암 바이오마커 시장 동향 및 인사이트

암 유병률의 급증

암 발병률이 증가함에 따라, 모든 주요 의료 시장에서 분자 스크리닝에 대한 장기적인 수요가 지속되고 있습니다. 미국에서만 2024년에 180만 건 이상의 신규 환자가 기록되었으며, 이러한 부담으로 인해 보험사들은 무증상 단계에서 종양을 발견할 수 있는 검사를 우선적으로 실시했습니다. 전 세계의 의료 시스템은 바이오마커를 통한 조기 발견이 사망률을 낮추고 치료비를 절감한다는 점을 인식하고 있으며, 검사 비용에 대한 광범위한 보험 적용에 대한 사업적 근거를 강화하고 있습니다.

예방적 위험 평가와 조기 발견으로의 전환

임상 전략은 확정된 질환의 진단에서 개별 위험 예측으로 전환되고 있습니다. 옥스퍼드 인구 건강(Oxford Population Health)은 최대 7년 전의 여러 가지 암을 예측할 수 있는 371개의 혈장 단백질 신호를 보고했으며, 이는 예측적 분자 의학의 실현 가능성을 보여줍니다. 현재 대규모 혈액 검사를 통한 선별 검사는 민감도 75%, 특이도 98.6%를 달성하고 있으며, 단일 암 검사가 현실적으로 어려운 상황에서 환자의 순응도를 높이는 다목적 선별 검사 도구를 제공함으로써 암 바이오마커 시장의 혁신을 가속화하고 있습니다.

바이오마커를 기반으로 한 진단의 높은 비용

액체 생검의 평균 비용은 2,800달러인 반면, 조직 생검은 700달러로, 비용에 민감한 의료 시스템에서는 도입이 제한되고 있습니다. 메디케어는 검사에 대한 광범위한 보험 적용을 승인하기 전에 여전히 광범위한 임상적 유용성에 대한 증거를 요구하고 있으며, 이로 인해 검사 이용이 지연되고 공급업체의 이익률이 압박받고 있습니다. 현장 진단(PoC) 기기는 시술 비용을 절감할 수 있지만, 실질적인 비용 절감은 생산 규모와 자동화 수준에 달려 있습니다.

부문별 분석

2025년 기준으로 유방암은 암 바이오마커 시장의 33.96%를 차지했으며, 그 기반이 되는 것은 현재 입원 및 외래 진료 환경 모두에서 일상적인 치료 결정의 지침으로 활용되고 있는 성숙한 HER2, ER 및 PR 검사 프로토콜입니다. 이러한 선도적 지위는 보험 급여의 근거가 되며, 의사들 사이에서도 널리 인정받고 있는 수십 년에 걸친 임상적 근거에 뒷받침되고 있습니다. 순환 종양 DNA(ctDNA) 검사의 활용 확대는 미세 잔류 병변을 모니터링하기 위한 비침습적 대안을 제공함으로써 유방암 시장의 입지를 더욱 공고히 하고 있습니다.

전립선암은 가장 빠르게 성장하고 있는 부문으로, 기존 검진에 대한 문화적 거부감이 여전히 높은 아시아 지역에서 비침습적 바이오마커 패널이 지지를 얻음에 따라 2031년까지 연평균 성장률(CAGR) 9.21%로 확대될 것으로 전망됩니다. EpiSwitch와 같은 후성유전학적 검사는 PSA 단독 검사보다 높은 특이도를 보이며, 불편한 검사 절차를 피할 수 있기 때문에 역사적으로 조기 진단이 뒤처져 있던 지역에서 이러한 검사의 보급을 촉진하고 있습니다. 이러한 동향을 종합해 보면, 암 바이오마커 시장에서는 유방암이 계속해서 지배적인 위치를 차지할 것이지만, 전립선암의 매출 점유율은 크게 확대될 것으로 보입니다.

면역측정법의 보급과 단백질 기반 진단법을 뒷받침하는 광범위한 임상적 근거 덕분에, 2025년 매출의 51.78%를 단백질 분석 항목이 차지했습니다. 병원에서는 몇 시간 이내에 결과를 확인할 수 있는 ELISA나 화학발광법 플랫폼이 활용되고 있으며, 긴급한 의사결정 시 단백질 마커가 우선적으로 채택되는 경향이 강해지고 있습니다.

전체 유전체 시퀀싱이 주류로 자리 잡음에 따라, 유전자 마커 시장은 2031년까지 연평균 성장률(CAGR) 9.63%를 나타낼 것으로 예측됩니다. 시퀀싱 비용의 급격한 하락과 AI를 활용한 변이 감지 파이프라인 덕분에 임상의들은 수백 개의 암 유전자를 동시에 분석할 수 있게 되었으며, 유전자 검사가 일선 의료 현장에 도입됨에 따라 정밀 유전체학 관련 제품을 활용한 암 바이오마커 시장 규모가 확대되고 있습니다. 다유전자 동반 진단과 관련된 업계 간 협력은 유전자 검사 매출 확대를 더욱 가속화하고 있습니다.

지역별 분석

북미는 안정적인 보험 환급, 확립된 바이오뱅크 네트워크, 그리고 신속한 검사 승인을 촉진하는 명확한 FDA 승인 절차에 힘입어 2025년 매출의 42.08%를 차지했습니다. 연방 정부의 정책은 계속해서 혁신을 지원하고 있지만, 실험실 개발 검사(LDT)에 관한 새로운 규정에 따라 향후 4년간 12억 9,000만 달러의 규정 준수 비용이 발생할 것으로 예측됩니다. 로슈가 미국에 500억 달러를 투자하는 등 자본을 투입한 것은 암 바이오마커 시장에서 해당 지역의 향후 성장 궤도에 대한 신뢰를 뒷받침하고 있습니다.

유럽은 2위를 차지했으며, GDPR(EU 개인정보보호규정)의 보호 조치 하에 유전체 데이터 공유를 조화롭게 하는 ‘유럽 헬스 데이터 스페이스’에 힘입고 있습니다. 독일의 ‘건강 데이터 이용법’과 유럽 전역에 걸친 액체 생검 표준화 이니셔티브에 힘입어, 집단 검진에서 바이오마커의 유용성이 확대되고 있습니다. 그렇긴 하지만, 엄격한 개인정보 보호 의무로 인해 데이터 교환 협상이 장기화되면서, 때때로 범유럽 차원의 임상시험이 지연되기도 합니다.

아시아태평양은 2027년까지 각국 정부가 의료 인프라 구축에 1,380억 달러 이상을 투자함에 따라 9.76%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 중국의 국가 주도의 AI 시스템에 대한 투자와 일본의 전국적 규모의 유전체 이니셔티브가 각 지역의 혁신 파이프라인을 뒷받침하고 있습니다. 전립선암과 위암을 대상으로 한 비침습적 검사가 점차 보급되면서, 조기 발견에 있어 기존에 존재하던 격차가 줄어들고 있습니다. 다양한 규제 체계가 여전히 존재하지만, 지역 간 조화를 위한 노력이 진행되고 있어, 향후 승인 절차의 효율화와 신흥 경제국 전반에 걸친 암 바이오마커 시장의 확대가 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the cancer biomarkers market size was valued at USD 21.37 billion in 2025 and estimated to grow from USD 23.22 billion in 2026 to reach USD 35.16 billion by 2031, at a CAGR of 8.65% during the forecast period (2026-2031).

This report is Segmented by Disease (Breast Cancer, Lung Cancer, Prostate Cancer, and More), Biomolecule Type (Protein Biomarkers and More), Profiling Technology (Omics Technologies, Imaging Technologies, and More), End User (Hospitals & Clinics, and More) and Geography (North America, Europe, Asia-Pacific and More). The Market and Forecasts are Provided in Terms of Value (USD).

Global Cancer Biomarkers Market Trends and Insights

Surge in Cancer Prevalence

Escalating cancer incidence sustains long-term demand for molecular screening in every major healthcare market. The United States alone recorded more than 1.8 million new cases in 2024, a burden prompting payers to favor tests that can flag tumors at asymptomatic stages. Health systems worldwide recognize that earlier detection through biomarkers lowers mortality and reduces treatment expenditures, strengthening the business case for broad test reimbursement.

Shift to Proactive Risk Assessment & Early Detection

Clinical strategies are pivoting from diagnosing established disease toward predicting individual risk. Oxford Population Health reported 371 plasma-protein signals that forecast multiple cancers up to seven years in advance, illustrating the feasibility of predictive molecular medicine. Large-scale blood-based screens now achieve 75% sensitivity with 98.6% specificity, providing multipurpose screening tools that improve patient compliance in settings where single-tumor tests are impractical, thereby accelerating innovation in the cancer biomarkers market.

High Cost of Biomarker-Based Diagnostics

Liquid biopsies average USD 2,800 versus USD 700 for tissue biopsies, limiting adoption in cost-sensitive systems. Medicare still requires extensive clinical-utility evidence before granting broad test coverage, delaying access and compressing vendor margins. While point-of-care devices can reduce procedural outlays, meaningful cost decline hinges on manufacturing scale and automation.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Multi-Omics & NGS Platforms

- AI-Enabled Biomarker Discovery Pipelines

- Uncertain & Region-Specific Reimbursement Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Breast malignancies represented 33.96% of the cancer biomarkers market in 2025, anchored by mature HER2, ER, and PR testing protocols that now guide routine therapeutic decisions in both inpatient and outpatient settings. This leadership rests on decades of clinical evidence that underpins reimbursement and physician familiarity. Expanded use of circulating-tumor-DNA assays further entrenches breast cancer's market position by providing minimally invasive options for monitoring minimal residual disease.

Prostate cancer is the fastest-rising segment, advancing at a 9.21% CAGR to 2031 as non-invasive biomarker panels gain favor in Asia where cultural hesitancy toward traditional screening remains high. Epigenetic assays such as EpiSwitch deliver higher specificity than PSA alone and avoid uncomfortable procedures, a combination that propels uptake in regions where early-stage diagnosis has historically lagged. Together, these trends indicate that prostate cancer will significantly escalate its revenue share despite breast cancer's continuing dominance in the cancer biomarkers market.

Protein analytes accounted for 51.78% of 2025 revenue thanks to the ubiquity of immunoassays and the extensive clinical evidence supporting protein-based diagnostics. Hospitals rely on ELISA and chemiluminescence platforms that deliver results within hours, reinforcing their preference for protein markers in acute decision-making.

Genetic indicators are anticipated to post a 9.63% CAGR through 2031 as whole-genome sequencing becomes mainstream. Plummeting sequencing costs and AI-driven variant-calling pipelines let clinicians interrogate hundreds of oncogenes simultaneously, propelling genetic tests into frontline care and enlarging the cancer biomarkers market size for precision-genomics offerings. Industry collaboration on multi-gene companion diagnostics further accelerates the revenue expansion of genetic assays.

Geography Analysis

North America captured 42.08% of 2025 revenue, bolstered by robust reimbursement, an established biobank network, and clear FDA pathways that facilitate rapid test approvals. Federal policy continues to support innovation, even as new rules for laboratory-developed tests impose USD 1.29 billion in compliance costs over four years. Capital commitments such as Roche's USD 50 billion US investment affirm confidence in the region's future growth trajectory for the cancer biomarkers market. .

Europe ranks second, supported by the European Health Data Space, which harmonizes genomic data sharing under GDPR safeguards. Germany's Health Data Use Act and European-wide liquid-biopsy standardization initiatives expand the utility of biomarkers in population screening. Still, stringent privacy obligations prolong data-exchange negotiations, occasionally delaying pan-European trials.

Asia-Pacific is set to record the swiftest 9.76% CAGR as governments allocate more than USD 138 billion to upgrade medical infrastructure by 2027. China's investment in sovereign AI systems and Japan's nationwide genome initiatives underpin local innovation pipelines. Non-invasive tests addressing prostate and gastric cancers are gaining acceptance, narrowing historical disparities in early detection. Diverse regulatory frameworks persist, yet regional harmonization efforts are underway, pointing to streamlined future approvals and an expanding cancer biomarkers market across emerging economies.

- Roche

- Abbott Laboratories

- Thermo Fisher Scientific

- QIAGEN

- Illumina

- Agilent Technologies

- Merck

- bioMerieux

- Quest Diagnostics

- Hologic

- Becton Dickinson & Co.

- Bio-Rad Laboratories

- PerkinElmer

- Myriad Genetics

- NeoGenomics Inc.

- Guardant Health

- Foundation Medicine Inc.

- Exact Sciences Corp.

- NanoString Technologies Inc.

- Bio-Techne

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in prevalence of cancer worldwide

- 4.2.2 Shift from diagnosis to proactive risk assessment & early detection

- 4.2.3 Rapid adoption of multi-omics & NGS platforms

- 4.2.4 AI-enabled biomarker discovery pipelines

- 4.2.5 Expansion of decentralized liquid-biopsy devices in emerging markets

- 4.2.6 Regulators fast-track approvals for companion diagnostics

- 4.3 Market Restraints

- 4.3.1 High cost of biomarker-based diagnostics

- 4.3.2 Uncertain & region-specific reimbursement pathways

- 4.3.3 Stringent data-privacy rules curbing genomic data sharing

- 4.3.4 Limited availability of longitudinal biobank samples

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Disease

- 5.1.1 Breast Cancer

- 5.1.2 Lung Cancer

- 5.1.3 Prostate Cancer

- 5.1.4 Colorectal Cancer

- 5.1.5 Cervical Cancer

- 5.1.6 Other Cancers

- 5.2 By Biomolecule Type

- 5.2.1 Protein Biomarkers

- 5.2.2 Genetic Biomarkers

- 5.2.3 Others

- 5.3 By Profiling Technology

- 5.3.1 Omics Technologies

- 5.3.2 Imaging Technologies

- 5.3.3 Immunoassays

- 5.3.4 Others

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Clinical & Reference Laboratories

- 5.4.3 Pharma & Biotech Companies

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche Ltd

- 6.3.2 Abbott Laboratories Inc.

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 QIAGEN N.V.

- 6.3.5 Illumina Inc.

- 6.3.6 Agilent Technologies

- 6.3.7 Merck KGaA (Millipore Sigma)

- 6.3.8 bioMerieux SA

- 6.3.9 Quest Diagnostics

- 6.3.10 Hologic Inc.

- 6.3.11 Becton Dickinson & Co.

- 6.3.12 Bio-Rad Laboratories Inc.

- 6.3.13 PerkinElmer Inc.

- 6.3.14 Myriad Genetics Inc.

- 6.3.15 NeoGenomics Inc.

- 6.3.16 Guardant Health

- 6.3.17 Foundation Medicine Inc.

- 6.3.18 Exact Sciences Corp.

- 6.3.19 NanoString Technologies Inc.

- 6.3.20 Bio-Techne Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment