|

시장보고서

상품코드

2066476

사기 탐지 및 방지 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Fraud Detection and Prevention (FDP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

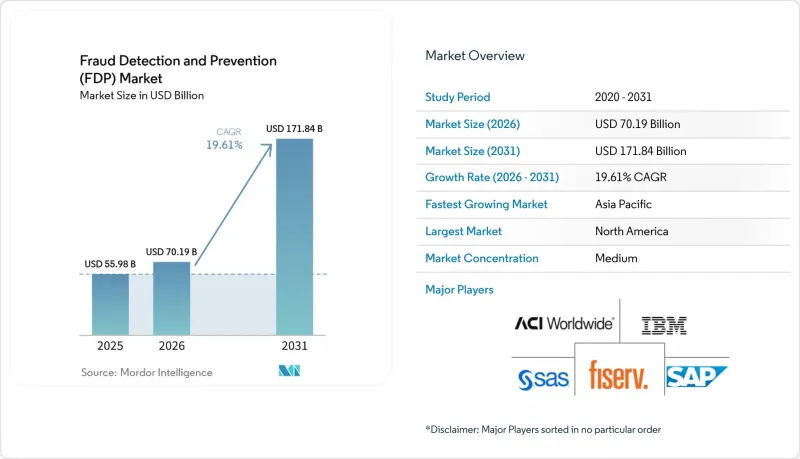

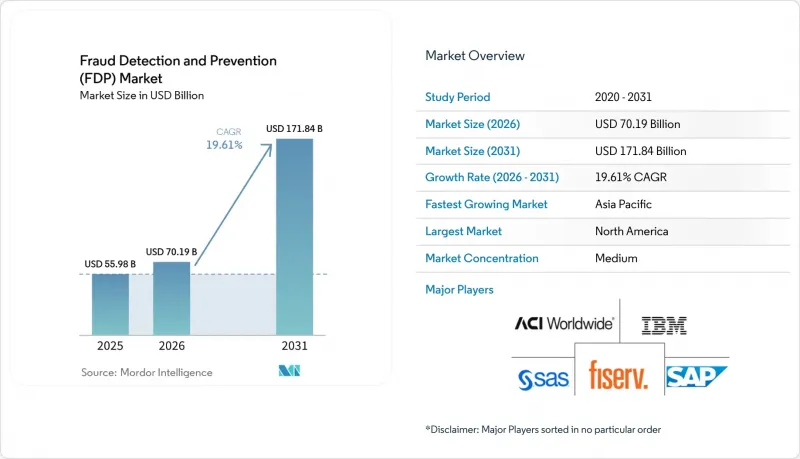

Mordor Intelligence에 의하면, 사기 탐지 및 방지 시장 규모는 2025년 559억 8,000만 달러로 평가되었습니다. 2026년에는 701억 9,000만 달러로 확대되어 2031년까지 1,718억 4,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 19.61%로 성장할 전망입니다.

본 보고서는 구성 요소(솔루션 및 서비스), 배포 방식(클라우드 및 On-Premise), 조직 규모(중소기업 및 대기업), 최종 사용자 산업(은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 헬스케어 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 사기 탐지 및 방지 시장 동향 및 인사이트

디지털 결제 및 전자상거래 거래량 증가

소비자들이 물리적 보안 기능이 부족한 온라인 채널로 이동함에 따라, 비대면 카드 거래가 전 세계 부정 사용 손실의 대부분을 차지하게 되었습니다. 유럽중앙은행의 보고서에 따르면, 2024년 전체 카드 부정 사용 건수의 79%를 비대면 카드 부정 사용이 차지했습니다. 인도의 통합 결제 인터페이스(UPI)에서는 2025년 12월 한 달 동안만 167억 3,000만 건의 거래가 처리되어 전년 대비 45% 증가했으며, 이로 인해 일괄 처리 방식의 레거시 시스템에 부하가 가해졌습니다. 국경을 넘는 전자상거래에서는 해당 지역 고유의 위험 패턴이 다른 지역에 일반화되는 경우가 드물기 때문에 감지가 복잡해지고 있으며, 공급업체는 해당 지역에 특화된 모델을 유지할 수밖에 없습니다. 가맹점은 부정 방지 및 고객 경험 간의 균형을 맞추기 위해 수동형 생체 인증을 도입하고 있으며, 결제 중개업체는 네트워크 인텔리전스를 집약함으로써 소규모 판매자라도 컨소시엄 전체의 신호를 활용할 수 있게 되었습니다.

AML 및 PSD2 SCA에 관한 엄격한 규정 준수

잇따른 규제 개정에 따라 다단계 인증, 지속적인 모니터링 및 감사 가능한 워크플로가 의무화되었습니다. 유럽은행감독청(EBA)이 2024년에 강화한 ‘강화된 고객 인증(SCA)’의 적용 예외 요건으로 인해, 마찰 없는 결제의 기준치가 낮아졌으며, 발행 기관들은 위험 기반 시스템을 도입해야 하는 상황에 직면해 있습니다. 2025년에 심의를 거친 ‘결제 서비스 지침 3(PSD3)’ 초안에서는 승인된 푸시 결제 사기에 대한 책임이 송금 은행으로도 확대되며, 감지 책임이 거래 개시 단계로 이전하게 됩니다. 미국에서는 FinCEN(금융범죄단속국)의 실질 소유자 규정에 따라 지배 구조에 대한 검증이 의무화되어 있어, 그래프 데이터베이스 분석에 대한 관심이 높아지고 있습니다. 다국적 금융기관은 국가별로 상이한 데이터 보관 의무를 조율해야 하므로, 그 결과 모델 가중치를 공유하면서도 학습 데이터를 국경 내에 유지하는 페더레이티드 러닝 기법이 채택되고 있습니다.

높은 오감지율이 고객 경험을 저해하고 있습니다.

기존 규칙을 적용할 경우, 여전히 정당한 주문 중 두 자릿수 비율이 잘못 분류되고 있으며, 그 결과 운영 비용 증가와 고객 생애 가치(LTV) 하락이 발생하고 있으며, 그 규모는 직접적인 부정 손실을 초과하는 경우도 있습니다. 수동 심사에서는 플래그가 지정된 거래 1건당 10-15달러의 비용이 발생하기 때문에 이익률이 낮은 가맹점에게는 큰 부담이 되고 있습니다. 키 입력 리듬이나 기기의 기울기 각도를 포착하는 행동 생체 인식 기술은 오감지율을 3% 미만으로 낮출 수 있을 것으로 기대되지만, 많은 동의 획득 체계에서 지속적인 행동 포착이 민감한 개인 데이터로 취급되고 있어 도입이 지연되고 있습니다. 특히 국경 간 주문의 영향은 막대합니다. 익숙하지 않은 IP의 지역 정보가 속도 점검을 유발하여 장바구니 포기나 평판 저하를 초래하고 있기 때문입니다.

부문별 분석

사기 탐지 및 방지 솔루션 시장 규모는 2025년 최고치를 기록하며, 플랫폼, 인증 게이트웨이, 리포팅 대시보드가 전체의 66.26%를 차지하며 신속한 투자 수익률(ROI)을 가져왔습니다. 그러나 관리형 감지, 모델 검증, 규제 자문 등의 서비스는 패키지 소프트웨어보다 더 빠르게 확대되고 있습니다. 금융 기관들은 적응형 부정방지가 매주 모델을 업데이트하고 끊임없이 진화하는 규정 준수 매핑을 필요로 하는 지속적인 과정이라는 점을 인식하고 있습니다. 전문 컨설팅 기업들은 현재 데이터 사이언스 전문 인력과 SaaS 대시보드를 결합한 서비스를 제공하고 있으며, 은행은 전략적 통제권을 양도파관 않고도 특징량 엔지니어링을 외부에 위탁할 수 있게 되었습니다. 한때는 조연에 불과했던 보고서 및 시각화 모듈이 이사회 차원에서 주목을 받기 시작하고 있습니다. 이는 실시간 노출 지표가 자본 배분 결정에 영향을 미치기 때문입니다. 부정 행위 감지와 신원 확인을 통합함으로써 구성 요소 간의 경계가 모호해지며, 고객 라이프사이클 전반에 걸친 통합적인 리스크 스코어링이 가능해집니다.

장기적으로는 상품화 압력으로 인해 벤더들은 독자적인 데이터 네트워크나 저지연 추론을 통해 차별화를 꾀할 수밖에 없게 되었습니다. IBM이 2025년에 출시된, 사용량에 따라 요금이 부과되는 ‘사기 감지 서비스(Fraud Detection as a Service)’는 종량제 모델이 비용을 실제 거래 위험과 연동시키는 구조를 여실히 보여주고 있습니다. 재무 위험 및 규제상의 중요도에 따라 경보의 우선순위를 결정하는 워크플로우의 조정은 이제 필수 요건이 되어가고 있습니다. 금융기관들은 현재 부정 방지 예산의 30-40%를 외부 서비스에 할당하고 있으며, 이는 자본 지출(Capex)을 통한 기술 구매에서 측정 가능한 손실 감소 성과에 초점을 맞춘 운영 비용(OpEx) 기반의 파트너십으로의 전환을 촉진하고 있습니다.

클라우드는 2025년 매출의 63.82%를 차지했으며, 2031년까지 약 19.95%의 성장이 예상됩니다. 이는 탄력적인 컴퓨팅을 통해 사기 방지 팀이 필요에 따라 GPU 클러스터를 구축하여 그래프 신경망 훈련을 수행할 수 있게 되었기 때문입니다. 실시간 확장성을 통해 다운타임 없이 매주 모델 재배포가 완료되며, 주요 하이퍼스케일러가 부여한 보안 인증은 규제 당국의 기대 사항 대부분을 충족하고 있습니다. 데이터 주권에 관한 법령에 따라 국경을 넘는 전송이 금지된 경우나, 데이터센터에 대한 최근 투자가 아직 감가상각 기간 중인 경우에는 On-Premise 도입이 계속됩니다. 하이브리드 아키텍처에서는 고위험 거래를 로컬에서 평가하는 동시에, 익명화된 집계 데이터를 클라우드 데이터 레이크에 집약함으로써 데이터 상주 규칙과 머신러닝의 효율성을 모두 충족시키고 있습니다. 유럽은행감독청(EBA)은 2024년, 클라우드로의 아웃소싱이 책임 소재를 이전하는 것은 아니라는 점을 분명히 했으며, 이를 통해 리스크 위원회는 중요한 업무 부하를 이전할 수 있다는 확신을 얻었습니다.

단일 공급업체에 대한 종속성을 피하고 내결함성을 높이기 위해 지역 간에 컴퓨팅 리소스를 분산시키려는 전 세계 은행들 사이에서 멀티클라우드 전략이 탄력을 받고 있습니다. 그렇긴 하지만, 툴체인의 차이로 인해 데이터 동기화가 복잡해지고 있으며, 모델 버전의 편차로 인해 채널 간에 일관성 없는 의사결정이 발생할 가능성이 있습니다. 2025년 하반기 미국 중견 은행 여러 곳이 도입한 Google Cloud의 가상 사설 클라우드(VPC) 도입 사례는 고객이 암호화 키에 대한 관리 권한을 보유하는 경우 규제 당국을 설득할 수 있음을 보여줍니다.

지역별 분석

2025년, 북미는 전 세계 매출의 31.87%를 차지했습니다. 이는 디지털 결제 보급률이 높고 견고한 규정 준수 체제가 구축되어 지출이 견조한 추세를 보였기 때문입니다. 미국 연방거래위원회(FTC)는 2023년 소비자 사기로 인한 손실액이 100억 달러에 달했다고 보고했으며, 이를 통해 경영진 차원에서 관리 체계를 개선하는 것이 시급하다는 점이 재인식되었습니다. 캐나다의 ‘Real-Time Rail’이나 미국의 ‘FedNow’와 같은 실시간 결제 시스템 덕분에 결제 처리 시간이 단축되면서, 은행들은 모델 스코어링 지연을 1초 미만으로 줄여야만 하는 상황에 처해 있습니다. 제3자 서비스 제공업체에 대한 규제 당국의 감독이 강화됨에 따라, 금융기관은 공급업체의 모델에 대해 설명 가능성과 편향성에 관한 감사를 실시해야 합니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 인도, 중국, 호주, 일본이 결제 인프라 현대화를 추진함에 따라 연평균 성장률(CAGR) 20.43%를 나타낼 것으로 전망됩니다. 인도의 UPI는 2025년 12월에 167억 3,000만 건의 거래를 처리했으며, 이는 인도 중앙은행(RBI)이 고액 송금에 대한 추가 인증을 의무화하는 계기가 되었습니다(RBI.ORG.IN). 중국에서 진행 중인 디지털 위안화 시범 사업은 현금 없는 결제 생태계를 지방의 군 단위까지 확대하고 있으며, 오프라인 지갑을 통한 신원 도용 등 새로운 부정 행위 경로를 낳고 있습니다. 일본의 개정된 자금세탁방지(AML) 지침은 규칙 기반 점검보다 지속적인 모니터링을 중시하고 있어, AI 플랫폼 등에 대한 수요를 촉진하고 있습니다. 호주의 ‘뉴 페이먼트 플랫폼(NPP)’은 2024년에 12억 건의 실시간 송금을 처리하면서, 일괄 처리용 ACH 파일을 위해 구축된 사기 분석 시스템의 결함을 드러냈습니다.

유럽은 PSD2의 ‘강력한 고객 인증’ 요건을 배경으로 여전히 큰 시장 점유율을 유지하고 있지만, 2024년 카드 비대면 거래로 인한 손실액은 42억 유로(45억 달러)에 달했습니다. 27개 회원국 간에 해석 차이가 있는 점이 다국적 사업 전개를 복잡하게 만들고 있어, 은행들은 지역별로 설정을 변경할 수 있는 정책 엔진 도입을 추진하고 있습니다. 남미에서는 브라질의 ‘Pix’가 2024년에 420억 건의 거래를 기록한 것을 계기로 성장세가 가속화되고 있으며, 이에 따라 중앙은행은 거래 한도와 야간 일시 중단 기간을 설정하기에 이르렀습니다. 중동 및 아프리카에서는 디지털 생태계에 참여하고 있지만 은행 계좌가 없는 사람들을 보호하기 위해 모바일 머니를 대상으로 한 사기 분석 시스템의 도입이 가속화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the fraud detection and prevention market size is expected to increase from USD 55.98 billion in 2025 to USD 70.19 billion in 2026 and reach USD 171.84 billion by 2031, growing at a CAGR of 19.61% over 2026-2031.

This report is Segmented by Component (Solutions, and Services), Deployment Mode (Cloud, and On-Premises), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (BFSI, Retail and E-Commerce, Healthcare, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Fraud Detection and Prevention (FDP) Market Trends and Insights

Rising Digital Payments And E-Commerce Transaction Volumes

Card-not-present transactions account for the majority of global fraud losses as consumers shift to online channels where physical security features are absent. The European Central Bank reported that card-not-present fraud accounted for 79% of total card fraud in 2024. India's Unified Payments Interface processed 16.73 billion transactions in December 2025 alone, a 45% year-over-year increase that strained batch-oriented legacy systems. Cross-border e-commerce complicates detection because region-specific risk patterns rarely generalize, compelling vendors to maintain localized models. Merchants are adopting passive biometrics to balance fraud control and customer friction, and payment facilitators aggregate network intelligence so even small sellers benefit from consortium-wide signals.

Stringent Regulatory Compliance For AML And PSD2 SCA

Successive rulemakings are mandating multi-factor authentication, continuous monitoring, and auditable workflows. The European Banking Authority's tightened Strong Customer Authentication exemptions in 2024 narrowed frictionless-payment thresholds, prompting issuers to deploy risk-based engines. Proposed Payment Services Directive 3, which is circulating in 2025, would extend liability for authorized push-payment fraud to sending banks, shifting detection to the initiation layer. In the United States, FinCEN's beneficial-ownership rule requires verification of control structures, driving interest in graph-database analytics. Multinational institutions must reconcile divergent data-residency obligations, leading to federated learning approaches that keep training data within national borders while sharing model weights.

High False-Positive Rates Undermining Customer Experience

Legacy rules still misclassify legitimate orders at double-digit rates, generating operational cost and lifetime-value erosion that sometimes exceed direct fraud losses. Manual reviews can cost USD 10-15 per flagged transaction, burdening merchants with thin margins. Behavioral biometrics that capture keystroke cadence and device-tilt angles promise to cut false positives below 3%, yet deployment lags because many consent frameworks treat continuous behavior capture as sensitive personal data. Cross-border orders suffer most, since unfamiliar IP geographies trip velocity checks, leading to cart abandonment and reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- AI And Machine Learning Models Increasing Real-Time Detection Accuracy

- Tokenization And EMV 3-D Secure 2.3 Adoption Reducing Card-Not-Present Fraud

- Integration Complexity With Fragmented Legacy Core Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The fraud detection and prevention market size for solutions reached its highest level in 2025, capturing 66.26% of platforms, authentication gateways, and reporting dashboards delivered rapid ROI. Yet services, including managed detection, model validation, and regulatory advisory, are expanding faster than packaged software. Institutions are learning that adaptive fraud defense is an ongoing process requiring weekly model refreshes and ever-evolving compliance mapping. Specialist consultancies now bundle data-science talent with SaaS dashboards so banks can outsource feature engineering without ceding strategic oversight. Reporting and visualization modules that once sat on the sidelines are gaining board-level attention because real-time exposure metrics influence capital-allocation decisions. Consolidation of fraud detection with identity verification blurs component boundaries, enabling unified risk scoring across the customer lifecycle.

Longer term, commoditization pressures solutions vendors to differentiate through proprietary data networks and low-latency inference. IBM's 2025 expansion of consumption-priced fraud detection as a service illustrates how pay-as-you-go models align costs with actual transaction risk. Workflow orchestration that prioritizes alerts based on financial risk and regulatory severity is becoming table stakes. Institutions now allocate 30-40% of their fraud-prevention budget to external services, reinforcing the shift from capex technology purchases to opex partnerships focused on measurable loss-reduction outcomes.

Cloud captured 63.82% of 2025 revenue, growing around 19.95% through 2031, as elastic compute lets fraud teams spin up GPU clusters for graph neural network training on demand. Real-time scaling means weekly model redeployments are complete without downtime, and security certifications from major hyperscalers satisfy most supervisory expectations. On-premises installations persist where data-sovereignty statutes prohibit cross-border transfer or where recent datacenter investments remain on depreciation schedules. Hybrid architectures, which score high-risk transactions locally while pooling de-identified aggregates in cloud data lakes, reconcile residency rules with machine-learning efficiency. The European Banking Authority clarified in 2024 that cloud outsourcing does not transfer accountability, giving risk committees confidence to migrate critical workloads.

Multi-cloud strategies gain traction among global banks keen to avoid single-vendor lock-in and to distribute compute across regions for resilience. Still, divergent toolchains complicate data synchronization, and model version drift can lead to inconsistent decisions across channels. Google Cloud's virtual-private-cloud deployment pattern, adopted by several mid-tier U.S. banks in late 2025, shows regulators can be convinced when customers retain encryption-key control.

Geography Analysis

North America generated 31.87% of global revenue in 2025 as high digital-payment penetration and robust compliance frameworks kept spending elevated. The U.S. Federal Trade Commission logged USD 10 billion in consumer fraud losses in 2023, reinforcing board-level urgency for improved controls. Real-time rails such as the Real-Time Rail in Canada and FedNow in the United States are shortening settlement windows, forcing banks to reduce model-scoring latency to sub-second levels. Regulatory scrutiny intensifies around third-party service providers, compelling financial institutions to audit vendor models for explainability and bias.

Asia-Pacific is the fastest-growing region, projected to post a 20.43% CAGR as India, China, Australia, and Japan modernize payments infrastructure. India's UPI handled 16.73 billion transactions in December 2025, catalyzing Reserve Bank mandates for additional authentication on high-ticket transfers RBI.ORG.IN. China's digital-yuan pilots expand cashless ecosystems to rural counties, adding novel fraud vectors such as identity spoofing in offline wallets. Japan's revised AML guidelines emphasize continuous monitoring over rule-based checks, stimulating demand for AI platforms such as. Australia's New Payments Platform processed 1.2 billion instant transfers in 2024, exposing gaps in fraud-analytics stacks built for batch ACH files.

Europe maintains significant share on the strength of PSD2 Strong Customer Authentication mandates, yet card-not-present losses still reached EUR 4.2 billion (USD 4.5 billion) in 2024. Fragmented interpretations across 27 member states complicate multinational rollouts, prompting banks to deploy configurable policy engines capable of local overrides. South America gains momentum as Brazil's Pix clocked 42 billion transactions in 2024, leading the Central Bank to impose transaction caps and nightly cooling-off periods. The Middle East and Africa regions accelerate adoption of mobile-money fraud analytics to protect unbanked populations joining digital ecosystems.

- SAP SE

- IBM Corporation

- SAS Institute Inc.

- ACI Worldwide Inc.

- Fiserv Inc.

- Experian PLC

- DXC Technology Company

- BAE Systems PLC

- RSA Security LLC (Dell Technologies)

- Oracle Corporation

- NICE Ltd

- Equifax Inc.

- LexisNexis Risk Solutions

- Fair Isaac Corporation (FICO)

- Cybersource Corporation (Visa)

- Global Payments Inc.

- Feedzai SA

- Signifyd Inc.

- Riskified Ltd.

- Kount Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Digital Payments and E-Commerce Transaction Volumes

- 4.2.2 Stringent Regulatory Compliance for AML and PSD2 SCA

- 4.2.3 AI and Machine Learning Models Increasing Real-Time Detection Accuracy

- 4.2.4 Tokenization and EMV 3-D Secure 2.3 Adoption Reducing Card-Not-Present Fraud

- 4.2.5 Proliferation of Open Banking and Instant-Payment Rails Creating New Fraud Vectors

- 4.2.6 Generative AI Deepfake and Synthetic Identity Attacks Pushing Adaptive FDP Investments

- 4.3 Market Restraints

- 4.3.1 High False-Positive Rates Undermining Customer Experience

- 4.3.2 Integration Complexity with Fragmented Legacy Core Systems

- 4.3.3 Scarcity of Labeled Fraud Datasets for Advanced ML Training

- 4.3.4 Data-Sharing Constraints Imposed by GDPR and CCPA

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.1.1 Fraud Analytics

- 5.1.1.2 Authentication

- 5.1.1.3 Reporting

- 5.1.1.4 Visualization

- 5.1.1.5 Other Components

- 5.1.2 Services

- 5.1.1 Solutions

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-premises

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 Retail and E-Commerce

- 5.4.3 IT and Telecom

- 5.4.4 Healthcare

- 5.4.5 Energy and Utilities

- 5.4.6 Manufacturing

- 5.4.7 Government and Public Sector

- 5.4.8 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 IBM Corporation

- 6.4.3 SAS Institute Inc.

- 6.4.4 ACI Worldwide Inc.

- 6.4.5 Fiserv Inc.

- 6.4.6 Experian PLC

- 6.4.7 DXC Technology Company

- 6.4.8 BAE Systems PLC

- 6.4.9 RSA Security LLC (Dell Technologies)

- 6.4.10 Oracle Corporation

- 6.4.11 NICE Ltd

- 6.4.12 Equifax Inc.

- 6.4.13 LexisNexis Risk Solutions

- 6.4.14 Fair Isaac Corporation (FICO)

- 6.4.15 Cybersource Corporation (Visa)

- 6.4.16 Global Payments Inc.

- 6.4.17 Feedzai SA

- 6.4.18 Signifyd Inc.

- 6.4.19 Riskified Ltd.

- 6.4.20 Kount Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment