|

시장보고서

상품코드

2066478

의료 사이버 보안 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Healthcare Cyber Security - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

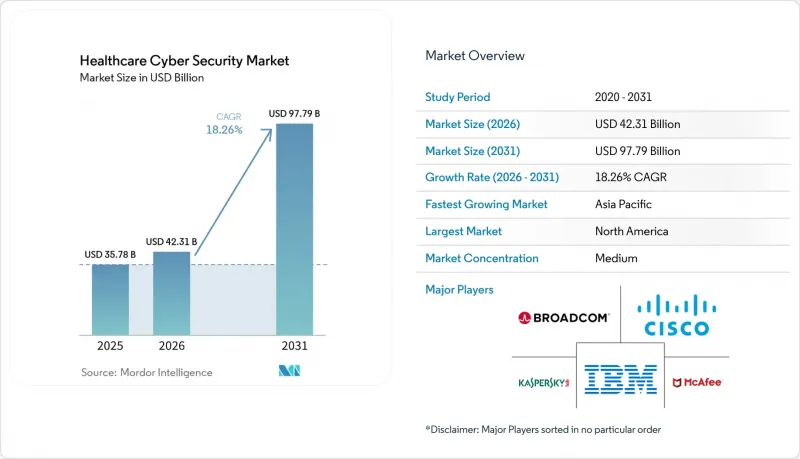

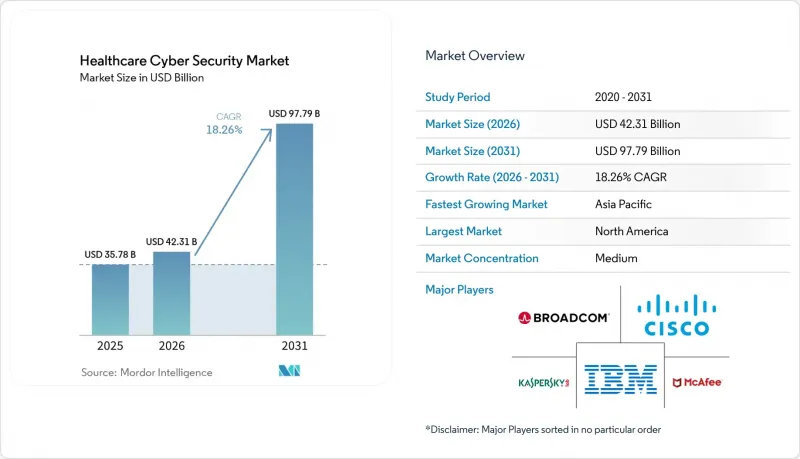

Mordor Intelligence에 의하면, 의료 사이버 보안 시장 규모는 2025년에 357억 8,000만 달러로 평가되었습니다. 2026년 423억 1,000만 달러에서 2031년까지 977억 9,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 18.26%를 나타낼 전망입니다.

본 보고서는 솔루션 유형(ID 및 액세스 관리, 위험 및 규정 준수 관리 등), 보안 유형(네트워크 보안, 엔드포인트 보안 등), 배포 모드(On-Premise 및 클라우드), 최종 사용자(병원 및 진료소 등), 조직 규모(대기업 및 중소기업), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 의료 사이버 보안 시장 동향 및 인사이트

사이버 공격의 빈도와 고도화 추세

보안 조사에 따르면, 2024년에는 러시아, 중국, 북한, 이란과 관련된 공격자들이 매일 병원 인프라를 정찰했으며, 그 결과 약 2억 5,900만 건의 의료 기록이 유출되는 사태에 이르렀습니다. 의료 기록은 보험 사기, 공갈, 첩보 활동에 이용되기 때문에 암시장에서 고가에 거래되고 있습니다. 이러한 이중적인 유용성 때문에 집요한 정찰 활동, 랜섬웨어, 공급망 공격이 조장되고 있습니다. 현재 인공지능(AI) 도구를 이용해 스피어 피싱이나 음성 딥페이크 사기가 자동화되면서, 사용자의 방어 체계가 약화되고 있습니다. 이에 반해, 의료 사이버 보안 시장의 서비스 제공업체들은 클라우드 워크로드와 연결된 모든 기기에 걸쳐 지속적인 모니터링, 다단계 인증, 최소 권한 원칙을 우선적으로 적용하고 있습니다.

규제 요건과 규정 준수 부담

제524B조에서는 2023년 3월 이후 FDA에 제출되는 모든 신규 의료기기에 대해 소프트웨어 부품 목록(SBOM), 보안 개발에 관한 증명서 및 조정된 취약점 공개 계획을 첨부할 것을 의무화하고 있습니다. 시판 전 승인 외에도, 제조업체는 제품의 상업적 수명 기간 동안 결함에 대한 패치를 적용해야 합니다. 따라서, 이러한 장비를 도입하는 병원에서는 펌웨어, 보안 권고 사항 및 패치 적용 현황을 실시간으로 추적할 수 있는 통합 위험 관리 플랫폼 도입 예산을 확보하고 있습니다. 동시에, HHS(미국 보건복지부)의 사이버 보안 성과 목표에는 불변 백업 및 특권 액세스 제어와 같은 기본적인 보호 조치가 명시되어 있으며, 많은 이사회에서는 이를 사실상 표준으로 간주하고 있습니다. 사이버보안·인프라보안청(CISA)이 권장하는 ID, 인증 정보 및 접근 관리 프레임워크는 비밀번호 중심 모델을 위험 기반의 인증서 주도형 인증으로 대체하고 있습니다.

소규모 의료기관의 예산 제약

소규모 병원의 경우, 영업이익률이 2% 미만에 그치는 경우가 많아, 다층적인 보안 도구와 연중무휴 24시간 감시에 투입할 충분한 예비 자금을 확보하지 못하고 있습니다. 최근 폐쇄 사례 조사에 따르면, 몸값 요구나 서비스 중단으로 인해 유동성이 저하될 경우, 사이버 사고가 영구적인 폐쇄로 이어질 가능성이 있는 것으로 나타났습니다. 의료 부문 조정 평의회는 사이버 보안을 메디케어의 인정 비용으로 분류할 것을 권고하고 있으나, 상환 정책은 여전히 검토 중입니다. 지속 가능한 자금 조달 수단이 확립될 때까지는 구독형 관리형 감지 및 대응(MDR) 서비스의 도입이 위험을 줄이기 위한 주요 수단이 될 것입니다.

부문별 분석

2025년, 의료 사이버 보안 시장 규모 중 25.80%를 ID 및 접근 관리(IAM) 도구가 차지했습니다. 이는 조직이 광범위한 임상 생태계 내에서 특권 인증 정보 관리에 주력했기 때문입니다. 그러나 수요는 보안 정보 및 이벤트 관리(SIEM) 플랫폼으로 이동하고 있으며, 해당 플랫폼은 2031년까지 연평균 성장률(CAGR) 18.72%를 나타낼 것으로 전망됩니다. 이러한 변화는 지속적인 로그 상관 분석과 행동 분석이 경계 방어만 사용하는 경우보다 침해 확산을 더 신속하게 차단할 수 있다는 공통된 인식을 반영한 것입니다. 예측 기간 동안 사이버 보안 로드맵에 따르면, 독립형 안티바이러스 소프트웨어에서 SIEM, SOAR 및 사용자·엔티티 분석을 통합한 통합 감지 스택으로 예산이 재분배될 것으로 나타났습니다.

리스크 및 규정 준수 솔루션은 HIPAA, GDPR(EU 개인정보보호규정) 및 의료기기 시판 후 감시 감사에 대비한 문서 작성을 효율화함으로써 안정적인 수요를 유지하고 있습니다. 암호화 및 데이터 유출 방지(DLP) 모듈은 제로 트러스트 아키텍처 내에서 보급이 확대되고 있으며, 특히 의료 서비스 제공업체가 여러 클라우드 테넌트 간에 방사선 영상이나 검사 데이터를 공유해야 하는 상황에서 수요가 증가하고 있습니다. 머신러닝을 활용한 새로운 행동 분석 솔루션은 ‘기타 솔루션’으로 분류되며, 정밀의료 워크로드를 시범적으로 도입하고 있는 연구 기관 등에서 자주 시범 도입되고 있습니다.

2025년, 네트워크 보안은 의료 사이버 보안 시장 점유율의 33.95%를 유지했습니다. 이는 병원이 수술실, 약제 자동화 시스템, 영상 아카이브 시스템을 연결하는 VLAN의 세분화을 계속하고 있기 때문입니다. 그렇긴 하지만, 클라우드 워크로드로의 전환은 우선순위를 재조정해 나가고 있습니다. EHR 인스턴스의 하이퍼스케일 제공업체로의 전환에 힘입어, 클라우드 보안 도구의 연평균 성장률(CAGR)은 18.58%를 나타낼 것으로 전망됩니다.

엔드포인트 보호는 병상 옆의 주입 펌프부터 임상의의 스마트폰에 이르기까지, 끊임없이 늘어나는 다양한 기기가 혼재되어 있는 문제에 직면해 있습니다. 사내 개발팀이 타사 API를 통합한 환자용 포털을 구축함에 따라 용도 보안의 중요성이 커지고 있으며, 런타임 보호 및 소프트웨어 구성 분석이 필요해지고 있습니다. 과거에는 뒷전으로 밀리기 일쑤였던 의료기기 및 IoMT 보안은 현재 이사회 차원의 문제로 대두되고 있습니다. 이는 1만 4,000건 이상의 의료 관련 IP 주소가 기기의 원격 측정 데이터를 공개 인터넷에 공개하고 있다는 통계에 기반한 것으로, 이러한 상황이 에이전트 없는 네트워크 감지 및 규제 대상 기기의 패치 적용 오케스트레이션에 대한 자금 조달을 뒷받침하고 있습니다.

지역별 분석

북미는 2025년, 세계에서 가장 엄격한 PHI(개인 건강 정보) 규제, 성숙한 보험 제도, 그리고 1인당 의료 IT 예산이 높은 점을 바탕으로 의료 사이버 보안 시장에서 34.12%의 점유율을 유지했습니다. 2025년 민간 사이버 보안 예산 배분을 포함한 연방 정부의 자금 지원에 힘입어, 전자 진료 기록의 현대화와 클라우드 도입이 뒷받침되고 있습니다. 또한, 미국에서는 2024년에 발생한 ‘체인지 헬스케어’ 사건이라는 현재까지 알려진 최대 규모의 데이터 유출 사고(1억 명이 피해를 입음)가 발생했으며, 이로 인해 제로 트러스트 로드맵과 제3자 위험 감사가 확고히 자리 잡게 되었습니다. 캐나다의 ‘전 캐나다 인공지능 전략’과 멕시코의 사회보장 디지털화 이니셔티브에 힘입어, SIEM 및 엔드포인트 감지 도구에 대한 지역적 수요는 더욱 확대되고 있습니다.

아시아태평양은 전 세계 의료 사이버 보안 시장에서 연평균 성장률(CAGR) 19.12%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 일본, 한국, 인도의 국가 차원 전자의료 정책에 따라 클라우드 기반 환자 등록 시스템과 안전한 ID 플랫폼이 통합되면서, 데이터 마스킹 및 암호화 서비스(Encryption-as-a-Service)에 대한 현지 수요가 증가하고 있습니다. 중국의 ‘건강중국 2030’ 구상에서는 사이버 보안이 스마트 병원을 뒷받침하는 6대 기반 중 하나로 자리매김하고 있으며, 국경을 넘는 데이터 유통 규제를 충족하는 국내 방화벽 및 취약점 관리 업체에 대한 수주가 확대되고 있습니다. 호주 연방 예산에는 지방 지역의 원격의료에 대한 보조금이 포함되어 있으며, 2022년부터 2024년에 걸쳐 디지털 헬스 분야의 제안 요청이 92% 급증했습니다.

유럽의 개인정보 보호 중심 체제는 GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)에 따른 과징금이 이사회 차원의 설명 책임을 명확히 함에 따라 꾸준한 성장을 보장하고 있습니다. 독일은 병원 디지털화에 30억 유로를 배정하고, 그중 최소 15%를 IT 보안 강화에 투입함으로써 ID 오케스트레이션 및 보안 이메일 게이트웨이 도입을 촉진하고 있습니다. 프랑스는 ‘MaSante 2025’ e-헬스 전략을 시행하고 있으며, 해당 전략의 사이버 보안 부속 문서에서는 지역 보건 기관 간 위협 정보 공유를 의무화하고 있습니다. 영국 국민보건서비스(NHS)의 ‘Data Saves Lives’ 프로그램에서는 ISO 27001 인증 취득을 조건으로, 구형 호출 시스템 및 영상 진단 플랫폼의 현대화에 자금이 지원되고 있습니다.

중동 및 아프리카에서는 걸프협력회의(GCC) 회원국들이 스마트 시티 병원을 건설하며, 국가사이버보안청(National Cybersecurity Authority)의 ‘의료 부문 관리 기준’ 준수를 목표로 하는 가운데, 관련 도입이 가속화되고 있습니다. 남아프리카공화국과 케냐에서는 환자 데이터를 익명화하는 토큰화 방식을 적용한 클라우드 기반 예방접종 등록 시스템의 시범 운영이 진행되고 있습니다. 남미에서는 브라질의 ‘오픈 헬스 이니셔티브’와 아르헨티나의 전자 처방전 도입을 필두로, 꾸준한 확대세가 나타나고 있습니다. 이들 모두 암호화 키 관리와 보안 API 게이트웨이가 필요합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the healthcare cybersecurity market size was valued at USD 35.78 billion in 2025 and estimated to grow from USD 42.31 billion in 2026 to reach USD 97.79 billion by 2031, at a CAGR of 18.26% during the forecast period (2026-2031).

This report is Segmented by Solution Type (Identity and Access Management, Risk and Compliance Management, and More), Security Type (Network Security, Endpoint Security, and More), Deployment Mode (On-Premises and Cloud), End User (Hospitals and Clinics, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Cyber Security Market Trends and Insights

Escalating Frequency and Sophistication of Cyber-Attacks

Security researchers confirmed that adversaries linked to Russia, China, North Korea, and Iran probed hospital infrastructure daily in 2024, culminating in breaches that touched an estimated 259 million medical records. Health records command a premium on illicit markets because they enable insurance fraud, blackmail, and espionage. This dual utility fuels relentless reconnaissance, ransomware, and supply-chain attacks. Artificial-intelligence tooling now automates spear-phishing and voice deep-fake scams, eroding user-based defenses. Providers respond by prioritizing continuous monitoring, multi-factor authentication, and least-privilege policies across cloud workloads and connected devices in the healthcare cybersecurity market.

Regulatory Mandates and Compliance Burden

Section 524B requires every new medical device submitted to the FDA after March 2023 to include a Software Bill of Materials, secure development attestations, and a plan for coordinated vulnerability disclosure. Beyond pre-market clearance, manufacturers must patch flaws for the product's commercial life. Hospitals integrating these devices, therefore, budget for integrated risk management platforms able to track firmware, security advisories, and patch status in real time. Simultaneously, the HHS Cybersecurity Performance Goals outline baseline safeguards-such as immutable backups and privileged access controls-that many boards treat as de facto standards. Identity, Credential, and Access Management frameworks endorsed by the Cybersecurity and Infrastructure Security Agency replace password-centric models with risk-based, certificate-driven authentication.

Budget Constraints in Small Providers

Smaller hospitals often run on operating margins below 2%, leaving inadequate reserves for layered security tooling and 24X7 monitoring. Investigations into recent closures show cyber incidents can trigger permanent shutdowns when ransom demands and downtime erode liquidity. The Healthcare Sector Coordinating Council recommends classifying cybersecurity as an allowable Medicare expense, yet reimbursement policy remains under review. Until sustainable funding emerges, adoption of subscription-based managed detection and response services is the primary avenue for risk reduction.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cloud-Based EHR and Tele-Health Adoption

- Low Security Penetration Among Smaller Providers

- Shortage of Specialized Cyber-Security Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Identity and Access Management tools accounted for 25.80% of the healthcare cybersecurity market size in 2025 as organizations focused on controlling privileged credentials inside sprawling clinical ecosystems. However, demand is shifting toward Security Information and Event Management platforms, which are forecast to grow at 18.72% CAGR to 2031. The change reflects a consensus that continuous log correlation and behavioral analytics offer faster breach containment than perimeter controls alone. Over the forecast period, cybersecurity roadmaps show budget reallocation from stand-alone antivirus toward converged detection stacks that integrate SIEM, SOAR, and user-entity analytics.

Risk and compliance suites remain steady because they streamline documentation for HIPAA, GDPR, and device post-market surveillance audits. Encryption and data-loss-prevention modules gain traction within zero-trust architectures, especially where providers must share radiology images and lab data across multiple cloud tenants. Emerging behavioral analytics solutions built with machine learning sit in the "other solutions" bucket and are frequently piloted in research institutes experimenting with precision medicine workloads.

Network security retained 33.95% of the healthcare cybersecurity market share in 2025 because hospitals continue to segment VLANs connecting operating rooms, pharmaceutical automation, and picture-archiving systems. The pivot to cloud workloads is nonetheless reshaping priorities: cloud security tools are poised for an 18.58% CAGR, propelled by migrations of EHR instances to hyperscale providers.

Endpoint protection confronts proliferating device heterogeneity, from bedside infusion pumps to clinician smartphones. Application security rises as in-house development teams build patient-facing portals that integrate third-party APIs, necessitating runtime protection and software composition analysis. Medical-device and IoMT security, once an afterthought, is now a board-level issue because more than 14,000 healthcare IP addresses expose device telemetry to the public internet-a statistic that rallies funding for agentless network detection and regulated device patch orchestration.

Geography Analysis

North America maintained 34.12% healthcare cyber security market share in 2025, backed by the world's strictest PHI regulations, a mature insurance system, and high per-capita health IT budgets. Federal funding, including the 2025 civilian cyber allocation, underwrites modernization of electronic health records and cloud adoption. The United States also endured the largest known breach the 2024 Change Healthcare incident affecting 100 million individuals which solidified zero-trust roadmaps and third-party risk audits. Canada's Pan-Canadian Artificial Intelligence Strategy and Mexico's social-security digitization initiatives further enlarge regional demand for SIEM and endpoint detection tools.

Asia-Pacific is the fastest-growing territory at 19.12% CAGR in the global healthcare cybersecurity market. National e-health mandates in Japan, South Korea, and India integrate cloud-hosted patient registries with secure identity platforms, spurring local demand for data-masking and encryption-as-a-service offerings. China's Healthy China 2030 blueprint designates cybersecurity one of six enabling pillars for smart hospitals, boosting orders for domestic firewall and vulnerability-management vendors that meet cross-border data flow restrictions. Australia's federal budget anchors subsidies for rural tele-health, leading to a 92% jump in digital-health solicitation requests from 2022-2024.

Europe's privacy-centric regime ensures steady growth as GDPR fines crystallize board-level accountability. Germany allocates EUR 3 billion to hospital digitization with at least 15% reserved for IT security enhancements, stimulating procurement of identity orchestration and secure email gateways. France implements its "MaSante 2025" e-health strategy with a cybersecurity annex that mandates threat-intelligence sharing among regional health agencies. The United Kingdom's NHS "Data Saves Lives" program directs funds to modernize legacy paging and imaging platforms, contingent upon ISO 27001 certification.

The Middle East and Africa exhibit accelerating adoption as Gulf Cooperation Council states build smart-city hospitals and seek compliance with the National Cybersecurity Authority's Healthcare Sector Controls. South Africa and Kenya pilot cloud-based immunization registries accompanied by tokenization schemes that de-identify patient data. South America registers steady expansion led by Brazil's open-health initiatives and Argentina's electronic prescription rollout, both of which require encryption key management and secure API gateways.

- Cisco Systems Inc.

- IBM Corporation

- AO Kaspersky Lab

- McAfee LLC

- Broadcom Inc. (Symantec)

- Trend Micro Inc.

- Palo Alto Networks Inc.

- Check Point Software Technologies Ltd.

- Fortinet Inc.

- CrowdStrike Holdings Inc.

- FireEye Inc. (Trellix)

- Imperva Inc.

- Claroty Ltd. (Medigate)

- Cynerio Ltd.

- Sophos Group plc

- Proofpoint Inc.

- Rapid7 Inc.

- CynergisTek Inc.

- Clearwater Compliance LLC

- Sensato Cybersecurity Solutions

- SecureLink Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating frequency and sophistication of cyber-attacks

- 4.2.2 Regulatory mandates and compliance burden

- 4.2.3 Rapid cloud-based EHR and tele-health adoption

- 4.2.4 Low security penetration among smaller providers

- 4.2.5 Medical-device security tied to value-based care models

- 4.2.6 Zero-trust frameworks for IoMT environments

- 4.3 Market Restraints

- 4.3.1 Budget constraints in small providers

- 4.3.2 Shortage of specialised cyber-security talent

- 4.3.3 Legacy system interoperability challenges

- 4.3.4 Vendor-liability ambiguity for FDA-regulated devices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assesment of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution Type

- 5.1.1 Identity and Access Management

- 5.1.2 Risk and Compliance Management

- 5.1.3 Antivirus and Antimalware

- 5.1.4 Security Information and Event Management (SIEM)

- 5.1.5 Intrusion Detection / Prevention (IDS/IPS)

- 5.1.6 Encryption and Data-Loss Prevention

- 5.1.7 Other Solutions

- 5.2 By Security Type

- 5.2.1 Network Security

- 5.2.2 Endpoint Security

- 5.2.3 Application Security

- 5.2.4 Cloud Security

- 5.2.5 Medical-Device / IoMT Security

- 5.3 By Deployment Mode

- 5.3.1 On-premise

- 5.3.2 Cloud

- 5.4 By End User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Pharmaceuticals and Biotechnology Firms

- 5.4.3 Health-insurance Providers

- 5.4.4 Diagnostic Laboratories

- 5.4.5 Other End Users

- 5.5 By Organisation Size

- 5.5.1 Large Enterprises

- 5.5.2 Small and Medium Enterprises

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Chile

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 France

- 5.6.3.3 United Kingdom

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Cisco Systems Inc.

- 6.4.2 IBM Corporation

- 6.4.3 AO Kaspersky Lab

- 6.4.4 McAfee LLC

- 6.4.5 Broadcom Inc. (Symantec)

- 6.4.6 Trend Micro Inc.

- 6.4.7 Palo Alto Networks Inc.

- 6.4.8 Check Point Software Technologies Ltd.

- 6.4.9 Fortinet Inc.

- 6.4.10 CrowdStrike Holdings Inc.

- 6.4.11 FireEye Inc. (Trellix)

- 6.4.12 Imperva Inc.

- 6.4.13 Claroty Ltd. (Medigate)

- 6.4.14 Cynerio Ltd.

- 6.4.15 Sophos Group plc

- 6.4.16 Proofpoint Inc.

- 6.4.17 Rapid7 Inc.

- 6.4.18 CynergisTek Inc.

- 6.4.19 Clearwater Compliance LLC

- 6.4.20 Sensato Cybersecurity Solutions

- 6.4.21 SecureLink Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment