|

시장보고서

상품코드

2066493

컨포멀 코팅 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Conformal Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

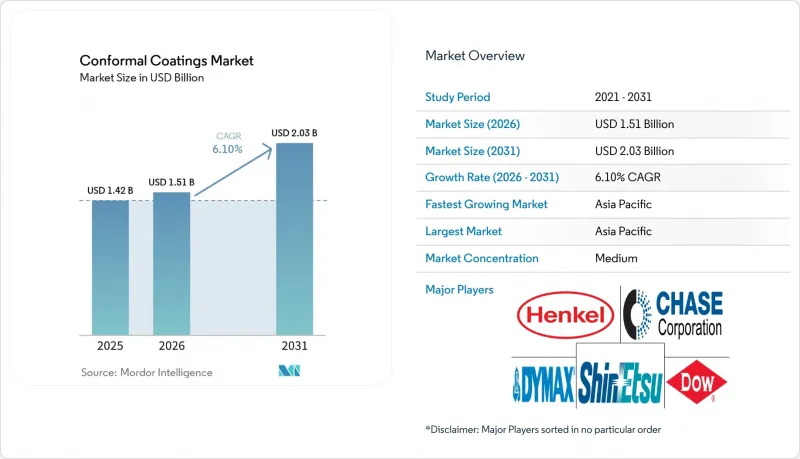

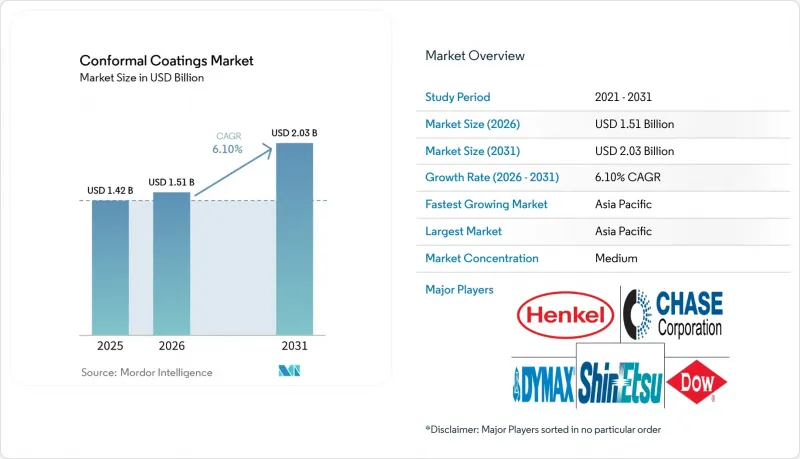

Mordor Intelligence에 의하면, 컨포멀 코팅 시장 규모는 2025년 14억 2,000만 달러로 평가되었고, 2026년에는 15억 1,000만 달러로 추정되고, 2026-2031년 CAGR 6.10%로 성장을 지속할 전망이며, 2031년에는 20억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 재료 유형별(아크릴, 에폭시, 실리콘 등), 기술별(용제형, 수성형, UV 경화형, 하이브리드 및 기타 첨단 시스템), 시공 방법별(스프레이 코팅, 딥 코팅 등), 최종 사용자 산업별(소비자용 전자기기, 자동차 등), 지역별(아시아태평양, 북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 컨포멀 코팅 시장 동향 및 인사이트

5G 스마트폰 및 IoT 웨어러블 기기에는 미세 회로의 보호가 필수적입니다.

10 mm² 미만의 RF 프런트엔드나 적층 수동 부품의 경우 클리어런스가 거의 없기 때문에 임피던스 드리프트를 방지하려면 유전율이 3 미만이고 두께를 ±5µm 이내로 제어할 수 있는 코팅이 필수적입니다. 웨어러블 기기에는 10만 회의 굽힘 주기를 견디면서도 IPC-CC-830C 클래스 3의 신뢰성을 유지할 수 있는 생체 적합성 필름이 요구되고 있습니다. 베트남과 인도의 수탁 조립 제조업체들은 선택적 로봇 디스펜싱 방식으로 전환함으로써, 카메라 모듈 및 플렉서블 OLED 드라이버 보드에서 수작업으로 진행되던 마스킹 공정을 없애고 자재 사용량을 40% 절감했습니다. 듀폰의 인터커넥트 솔루션즈는 이러한 생산 확대를 바탕으로 2024년 3분기에 저 2자리 수의 유기적 성장을 기록했습니다. 또한, 각 제조업체는 경화를 가속화하고 AOI의 가시성을 유지하기 위해 UV 경화형 탑코트와 투명한 아크릴 재질의 하층을 조합하고 있습니다.

LEO 위성 및 항공 전자 장비에는 고성능 코팅이 요구됩니다.

2024년부터 2030년 사이에 발사될 예정인 1만 기 이상의 LEO 위성은 각각 50-200장의 기판을 탑재하고 있으며, 이 기판들은 원자 상태의 산소, -150°C-+125°C의 온도 사이클, 그리고 100 krad의 방사선 환경을 견뎌내야 합니다. 파릴렌 및 불소 수지 나노 코팅은 5 kV/mm를 초과하는 절연 내력과 총 질량 손실 1% 미만의 아웃가스 성능을 실현하여, AR형 아크릴 소재를 능가합니다. 헨켈은 2024년 중국 내 전자 사업 부문에서 두 자릿수 매출 성장을 기록했는데, 그 원인 중 하나는 항공 전자 장비 프로그램 때문입니다. 항공우주 OEM 업체들은 현재, 저기압으로 인해 코로나 방전이 발생하기 쉬운 고도 15,000 m에서의 플라이-바이-와이어 제어를 위해 실리콘 시스템의 인증 절차를 진행하고 있습니다. ±0.1 mm의 정밀도를 갖춘 자동 진공 증착 라인을 통해 페이즈 어레이 모듈의 초기 수율이 98%로 향상되었습니다.

UV 경화형 불투명 필름의 재작업 및 검사의 복잡성

불투명한 UV 코팅은 몇 초 만에 경화되지만, IPC-A-610 클래스 3에서 요구하는 납땜 접합부 검증을 AOI 카메라로 수행할 수 없게 만듭니다. 도포 오류로 인한 필름을 제거하려면 대부분의 경우 기계적 연마나 플라즈마 처리밖에 방법이 없으며, 파인 피치 QFN의 경우 패드 리프트의 위험이 발생합니다. 현재 하이브리드 라인에서는 AOI에서 중요한 영역에는 투명한 UV 재료를, 기타 영역에는 착색 코팅을 도포하고 있으며, 이로 인해 지그와 레시피에 15%의 오버헤드가 추가되고 있습니다. 노드슨의 ‘Select Coat SL-1040’은 노즐의 유량과 UV 조사량을 기록하여 재작업률을 1% 미만으로 억제합니다. EMS 업체 측에서는 용제 기반 시스템에서 UV 시스템으로 전환하는 기술자에게 여전히 2-4시간의 숙련 기간이 필요하다는 의견이 나오고 있습니다.

부문별 분석

2025년에는 아크릴계 컨포멀 코팅이 시장 점유율 44.24%를 차지하며 컨포멀 코팅 시장을 주도했습니다. 조립 제조업체들이 저비용, 폭넓은 호환성, 그리고 손쉬운 재작업 가능성을 중시하고 있기 때문에 해당 시장은 연평균 성장률(CAGR) 6.88%로 성장할 것으로 전망됩니다. 한편, 실리콘계 소재는 -60°C에서 +200°C에 이르는 온도 범위에서 안정성을 유지하며, 열 사이클 조건에서도 솔더 접합부의 무결성을 유지하는 낮은 탄성 계수를 갖추고 있어, 그 높은 가격 책정이 정당화됩니다. 에폭시 계열은 내화학성 덕분에 자동차 엔진룸 내의 박스 용도로 여전히 널리 사용되고 있지만, 취성 때문에 채택률은 제한적입니다. 우레탄 및 폴리우레탄 계열은 10만 사이클 이상의 굴곡 수명이 요구되는 접이식 기기에서 뛰어난 성능을 발휘하고 있습니다. 신흥 불소 수지 나노 코팅은 웨어러블 기기에서 땀을 튕겨내는 110° 이상의 접촉각을 가진 10µm 미만의 필름에 대한 수요가 증가하고 있습니다.

2024년에 신에츠 화학공업이 출시한 실리콘 수지 ‘KRW-6000’은 수분산성과 150°C에서 30분간 경화되는 특성을 모두 갖추고 있어, 생산성을 저해하지 않으면서 RoHS 준수를 요구하는 OEM 업체들의 요구를 충족시키고 있습니다. 현재 총소유비용(TCO)이 소재 선정의 결정 요인으로 작용하고 있으며, 원자재 가격 외에도 설비 투자, 경화에 필요한 에너지 소비량, 그리고 유럽 및 일본의 확대 생산자 책임(EPR) 규정에 따른 사용 후 제품 처리 비용이 고려되고 있습니다. IPC-CC-830C의 Type AR 및 Type SR 제품은 시장 점유율의 75%를 차지하고 있지만, 2024년 개정판인 IPC-HDBK-830A에서는 불소수지에 관한 지침이 공식적으로 추가되어 차세대 소재의 도입이 예상됩니다. 듀얼 경화형 에폭시-아크릴레이트 블렌드 등 첨단 하이브리드 제품은 4 kV/mm의 절연 내력 및 1 W/mK 이상의 열전도율을 요구하는 BMS 파워 모듈을 대상으로 합니다.

용제계 제품은 폭넓은 습윤성과 자동차 업계의 PPAP(생산 전 승인)에서 확립된 승인을 바탕으로, 2025년에도 컨포멀 코팅 시장 규모의 55.78%를 계속 차지하고 있습니다. 한편, UV 경화형은 VOC가 전혀 발생하지 않는다는 점, 1초 만에 경화되는 점, 그리고 오븐 전력 소비를 80% 절감하는 에너지 절약 효과에 힘입어 2031년까지 연평균 성장률(CAGR) 7.13%로 급성장하고 있습니다. 수성 시스템은 규제가 처리 능력보다 우선시되는 분야에서 지지를 얻고 있으며, 80°C에서 건조하는 데 60분이 소요됨에도 불구하고 시장 점유율이 5분의 1 가까이까지 확대되고 있습니다. 하이브리드 화학제품은 고전압 인버터에서 포팅 및 밀봉 역할을 수행합니다.

베트남의 주요 EMS 기업들은 2024년에 스마트폰 안테나 및 무선 충전 코일의 코팅 공정에 200대 이상의 UV-LED 터널을 도입하여 설치 면적을 30% 줄였습니다. LiDAR 모듈에 대한 자동차 업계의 시험 결과, UV 실리콘을 사용하면 MIL-STD-810H의 성능을 유지하면서 턱프리 시간을 45분에서 60초로 단축할 수 있는 것으로 나타났습니다. 노드슨의 2024년 2분기 실적 발표에 따르면, 반도체 부문 수요가 22% 감소한 반면, 산업용 정밀 솔루션 부문은 코팅 장비의 호조에 힘입어 2%의 매출 증가를 기록했습니다. 여전히 남아 있는 과제로는 불투명 필름의 AOI(자동 광학 검사)에 따른 제한을 들 수 있지만, 인시투 형광 측정 기술을 통합함으로써 50µm 두께를 실시간으로 검증할 수 있게 되어, 경화 전 결함을 줄일 수 있게 되었습니다.

지역별 분석

아시아태평양은 2025년에 컨포멀 코팅 시장 매출의 42.35%를 차지한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 7.67%로 성장을 가속화하고 있습니다. 중국은 스마트폰 및 데이터센터 프로젝트가 재개됨에 따라 2024년에 회복세를 보였으며, 헨켈사는 전자 분야에서 두 자릿수 성장을 기록했다고 밝혔습니다. 아세안(ASEAN) 국가들은 2024년에 전자 분야에서 310억 달러 규모의 외국인 직접투자(FDI)를 유치하며, 반도체 후공정 허브로서의 입지를 공고히 했습니다. 인도의 PLI(생산 연계형 인센티브) 제도와 5G 기지국 구축은 인도 표준국(BIS)의 승인을 준수하는 RoHS 대응 코팅 라인의 도입을 촉진하고 있습니다. 한국과 일본은 플렉서블 디스플레이 및 자동차 전자 분야의 혁신 거점으로 자리매김하고 있으며, 이는 각 공급업체들이 서울과 도쿄에 기술 센터를 개설하는 계기가 되고 있습니다.

북미 수요는 항공우주, 방위 및 전기차(EV) 제조업에 의해 뒷받침되고 있습니다. ‘CHIPS and Science Act’ 및 ‘Inflation Reduction Act’에 따라 2030년까지 1,000억 달러 이상이 국내 팹에 투자될 예정이며, 이에 따라 IPC 인증 코팅에 대한 수요가 증가할 것으로 전망됩니다. 3M의 전자 사업부는 2024년에 169종의 신제품을 출시하며, 반도체 패키징용 보호 소재 분야에 주력할 것임을 보여주었습니다. 멕시코의 바하 캘리포니아 회랑은 전기차용 전자기기 생산 거점으로 자리매김하고 있는 반면, 캐나다의 몬트리올 클러스터는 아비오닉스용 코팅 수요를 충족시키고 있습니다.

유럽에서는 독일, 프랑스, 영국이 엄격한 RoHS 및 REACH 기준을 시행하고 있으며, 이로 인해 수성 및 UV 경화형 코팅 기술의 보급이 촉진되고 있습니다. 다우의 퍼포먼스 머티리얼즈 앤 코팅 부문은 2023년에 84억 9,700만 달러의 매출을 기록했으며, 실리콘 제품은 유럽의 자동차 및 산업 분야 고객들에게 공급되고 있습니다. 북유럽의 전기차용 배터리 기가팩토리나 해상 풍력 발전용 컨버터에는 내염안개성 코팅이 요구되고 있습니다. 남미, 중동 및 아프리카는 여전히 개발도상국이지만, 브라질의 자동차 부문이나 사우디아라비아의 스마트시티 프로젝트에서 혹독한 기후에 대응하는 보호 필름이 지정되는 등 성장을 이어가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the conformal coatings market size is expected to grow from USD 1.42 billion in 2025 to USD 1.51 billion in 2026 and is forecast to reach USD 2.03 billion by 2031 at 6.10% CAGR over 2026-2031.

This report is Segmented by Material Type (Acrylic, Epoxy, Silicone and More), Technology (Solvent-Based, Water-Based, UV-Cured, and Hybrid/Other Advanced Systems), Operation Method (Spray Coating, Dip Coating, and More), End-User Industry (Consumer Electronics, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Conformal Coatings Market Trends and Insights

5G Smartphones and IoT Wearables Require Mini-Circuit Protection

Sub-10 mm2 RF front-ends and stacked passives leave little clearance, compelling coatings with dielectric constants below 3 and +-5 µm thickness control to prevent impedance drift. Wearables demand biocompatible films that survive 100,000 flex cycles yet retain IPC-CC-830C Class 3 reliability. Contract assemblers in Vietnam and India saved 40% of material by switching to selective robotic dispensing, eliminating manual masking on camera modules and flexible OLED driver boards. DuPont's Interconnect Solutions reported low-double-digit organic growth in Q3 2024 on the back of these ramps. Manufacturers also pair UV-cured topcoats with transparent acrylic under-layers to speed cure and preserve AOI visibility.

LEO Satellites and Avionics Electronics Need High-Performance Coatings

More than 10 000 LEO satellites slated for launch between 2024 and 2030 each carry 50-200 boards that must withstand atomic oxygen, -150 °C to +125 °C cycling, and 100 krad radiation environments. Parylene and fluoropolymer nano-coatings deliver dielectric strength above 5 kV/mm and outgassing below 1% total mass loss, surpassing Type AR acrylics. Henkel logged double-digit electronics growth in China during 2024, partially tied to avionics programs. Aerospace OEMs now qualify silicone systems for fly-by-wire control at 15 000 m where low pressure invites corona discharge. Automated vacuum deposition lines with +-0.1 mm accuracy improve first-pass yield to 98% on phased-array modules.

Rework/Inspection Complexity of UV-Cured Opaque Films

Opaque UV coatings cure within seconds, yet block AOI cameras from verifying solder joints required under IPC-A-610 Class 3. Mechanical abrasion or plasma is often the only route to remove misapplied films, risking pad lift on fine-pitch QFNs. Hybrid lines now apply transparent UV material on AOI-critical zones and pigmented coating elsewhere, adding 15% overhead in fixtures and recipes. Nordson's Select Coat SL-1040 logs nozzle flow and UV dose to cut rework under 1%. EMS players still cite 2-4 hour training curves for technicians switching from solvent to UV systems.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift to RoHS-Compliant Low-VOC Water/UV Systems

- Expansion of Telecom Infrastructure and 5G Rollout

- Silicone-Monomer Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics led the conformal coatings market with 44.24% share in 2025 and are forecast to grow at 6.88% CAGR as assemblers value low cost, broad compatibility, and easy rework. Silicone chemistries, meanwhile, deliver -60 °C to +200 °C stability and low modulus that preserves solder joint integrity under thermal cycling, justifying premium pricing. Epoxies remain entrenched in under-hood automotive boxes for their chemical resistance, although brittleness limits take-rate. Urethanes and polyurethanes win in foldable devices demanding flex life above 100,000 cycles. Emerging fluoropolymer nano-coatings are logging demand for sub-10 µm films with contact angles more than 110° that repel sweat in wearables.

Silicone's KRW-6000, launched by Shin-Etsu in 2024, marries water dispersibility with 30-minute cure at 150 °C, answering OEM calls for RoHS compliance without throughput penalties. Total cost-of-ownership now dictates material decisions, blending raw resin price with capital, cure-energy loads, and end-of-life disposal under extended producer rules in Europe and Japan. IPC-CC-830C Type AR and Type SR products account for 75% of market qualifications, yet the 2024 IPC-HDBK-830A update formally added fluoropolymer guidance, foreshadowing next-gen adoption. Advanced hybrids, such as dual-cure epoxy-acrylate blends, target BMS power modules requiring 4 kV/mm dielectric strength and >=1 W/mK thermal conductivity.

Solvent-based still occupy 55.78% of the conformal coatings market size in 2025, owing to broad wetting and established approvals across automotive PPAPs. UV-cured, however, are accelerating at 7.13% CAGR through 2031, driven by zero-VOC status, one-second cures, and energy savings that cut oven power by 80%. Water-based systems gain favor where regulation trumps throughput, rising to nearly one-fifth of volume despite 60-minute dry times at 80 °C. Hybrid chemistries serve potting and encapsulation roles in high-voltage inverters.

EMS giants in Vietnam installed over 200 UV-LED tunnels in 2024 to coat smartphone antennas and wireless charging coils, trimming floor space 30%. Automotive trials on LiDAR modules show UV silicones slicing tack-free time from 45 minutes to 60 seconds while sustaining MIL-STD-810H performance. Nordson's Q2 2024 saw Industrial Precision Solutions rise 2% on coatings equipment even as semiconductor demand sagged 22% in its Advanced Technology arm. Persistent barriers include opaque-film AOI limits, but integration of in-situ fluorometry now validates 50 µm thickness in real time, mitigating defects before cure.

Geography Analysis

Asia-Pacific generated 42.35% of conformal coatings market revenue in 2025 and is accelerating at 7.67% CAGR through 2031. China rebounded in 2024 as smartphone and data center projects resumed, with Henkel citing double-digit electronics growth. ASEAN nations secured USD 31 billion electronics FDI in 2024, cementing their role as back-end semiconductor hubs. India's PLI incentives and 5G base-station buildout are spurring RoHS-compliant coating lines tied to Bureau of Indian Standards approvals. South Korea and Japan remain innovation centers for flex displays and automotive electronics, prompting suppliers to open tech centers in Seoul and Tokyo.

North America's demand is supported by aerospace, defense, and EV manufacturing. The CHIPS and Science Act and Inflation Reduction Act will funnel more than USD 100 billion toward domestic fabs through 2030, boosting demand for IPC-qualified coatings . 3M's Electronics division launched 169 new products in 2024, showing a push for protective materials in semiconductor packaging. Mexico's Baja California corridor is becoming an EV electronics hot spot, while Canada's Montreal cluster services avionics coating needs.

In Europe, Germany, France, and the United Kingdom enforce strict RoHS and REACH standards, propelling water-based and UV chemistries. Dow's Performance Materials & Coatings reported USD 8.497 billion sales in 2023, with silicones serving European auto and industrial clients. Nordic EV battery gigafactories and offshore wind converters need salt-fog-resistant coatings. South America and the Middle East and Africa remain nascent but are growing as Brazil's auto sector and Saudi smart-city projects specify protective films for harsh climates.

- 3M

- Actnano Inc.

- Altana AG

- Bostik (Arkema)

- Chase Corp.

- Chemtronics (KEMET)

- CHT UK Ltd

- Dow

- Dymax

- Electrolube

- Europlasma NV

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Illinois Tool Works Inc.

- MG Chemicals

- Nordson Corporation

- Panacol-Elosol GmbH

- PVA

- Shin-Etsu Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G Smartphones and IoT Wearables Require Mini-Circuit Protection

- 4.2.2 LEO Satellites and Avionics Electronics Need High-Performance Coatings

- 4.2.3 Regulatory Shift to Rohs-Compliant Low-VOC Water/UV Systems

- 4.2.4 Expansion of Telecom Infrastructure and 5G Rollout

- 4.2.5 Increasing Aerospace and Defence Electronics Applications

- 4.3 Market Restraints

- 4.3.1 Rework/Inspection Complexity of UV-Cured Opaque Films

- 4.3.2 Silicone-Monomer Price Volatility

- 4.3.3 Scarcity of High-Purity Parylene Dimer

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Acrylic

- 5.1.2 Epoxy

- 5.1.3 Urethane/Polyurethane

- 5.1.4 Silicone

- 5.1.5 Other Material Types (Fluoropolymer, Nano-coatings)

- 5.2 By Technology

- 5.2.1 Solvent-Based

- 5.2.2 Water-Based

- 5.2.3 UV-Cured

- 5.2.4 Hybrid/Other Advanced Systems

- 5.3 By Operation Method

- 5.3.1 Spray Coating (Atomised/Film)

- 5.3.2 Dip Coating

- 5.3.3 Brush Coating

- 5.3.4 Other Operation Methods (Selective/Robotic Dispense and Chemical Vapour Deposition (CVD))

- 5.4 By End-user Industry

- 5.4.1 Consumer Electronics

- 5.4.2 Automotive (ICE, EV, ADAS)

- 5.4.3 Aerospace and Defense

- 5.4.4 Medical and Life-Sciences Electronics

- 5.4.5 Other End-user Industries (Industrial, Power and Energy)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 NORDIC Countries

- 5.5.3.6 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Actnano Inc.

- 6.4.3 Altana AG

- 6.4.4 Bostik (Arkema)

- 6.4.5 Chase Corp.

- 6.4.6 Chemtronics (KEMET)

- 6.4.7 CHT UK Ltd

- 6.4.8 Dow

- 6.4.9 Dymax

- 6.4.10 Electrolube

- 6.4.11 Europlasma NV

- 6.4.12 H.B. Fuller Company

- 6.4.13 Henkel AG & Co. KGaA

- 6.4.14 Illinois Tool Works Inc.

- 6.4.15 MG Chemicals

- 6.4.16 Nordson Corporation

- 6.4.17 Panacol-Elosol GmbH

- 6.4.18 PVA

- 6.4.19 Shin-Etsu Chemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment