|

시장보고서

상품코드

2066495

항공기용 배터리 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aircraft Battery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

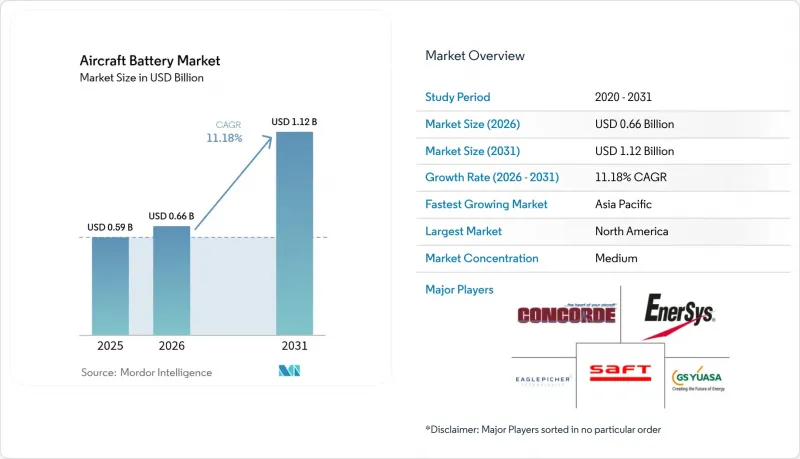

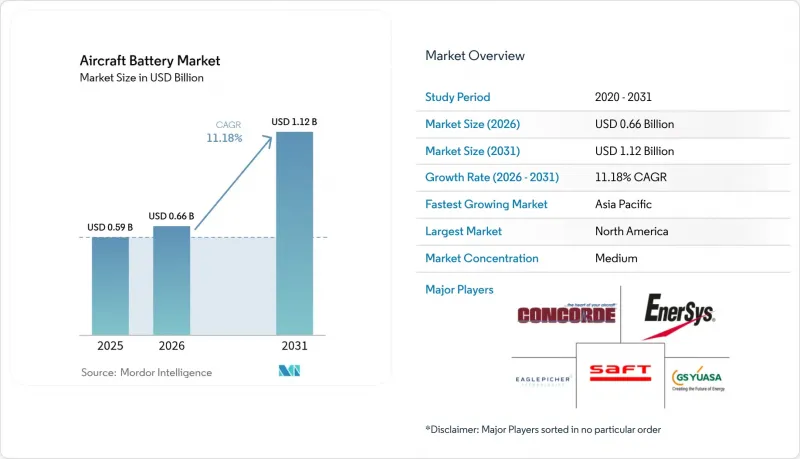

Mordor Intelligence에 의하면, 항공기용 배터리 시장 규모는 2025년 5억 9,000만 달러로 평가되었습니다. 2026년에는 6억 6,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 11.18%로 성장을 지속하여, 2031년까지 11억 2,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 배터리 유형(납산 배터리 등), 용도(추진용 등), 항공기 기술(기존 등), 항공기 유형(고정익, 회전익 등), 출력 밀도(100Wh/kg 미만 등), 최종 사용자(OEM(Original Equipment Manufacturer) 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공기용 배터리 시장 동향 및 분석

북미의 협폭기 프로그램에서 ‘모어 일렉트릭’ 항공기의 도입

북미의 항공기 제조업체들은 공압식 아키텍처를 대체할 전기 서브시스템을 중심으로 단일 통로 제트기의 재설계를 추진하고 있으며, 이로 인해 항공기용 배터리 시장에서 이륙 및 상승 시의 피크 부하가 3배로 증가하고 있습니다. RTX사의 1MW 모터 등 실증 장비는 연료 소비량을 30% 줄이는 것을 목표로 하고 있으며, 고성능 배터리 연구에 공동 투자하는 ‘클린 에비에이션(Clean Aviation)’ 이니셔티브와 같은 방향을 지향하고 있습니다. 각 항공사는 정비 비용 절감과 탄소 배출 규제 대응의 가치를 기대하고 있으며, 이것이 조기 개조를 촉진하고 있습니다. 연방항공청(FAA)의 지침에 따라, 급속 충전 및 고사이클 배터리 팩의 검증이 가능한 배터리 제조업체는 장기 공급 계약을 체결할 수 있을 것으로 보입니다.

아시아에서 고부하 항공전자 장비용 리튬 이온 배터리로의 OEM 전환

중국, 일본, 한국의 각 OEM 업체들은 항공기용 배터리 시장에서 니켈카드뮴 전지를 단계적으로 폐지하고, 리튬이온 팩으로의 전환을 추진하고 있습니다. 조사 결과에 따르면, 이를 통해 공급망의 복잡성이 72% 감소하고 이산화탄소 배출량이 75% 감소하는 것으로 나타났습니다. CATL이나 Gotion High-Tech와 같은 국내 공급업체들은 이미 각각 500 Wh/kg 및 300 Wh/kg을 달성했으며, 지역 제조업체들은 첨단 화학 기술을 확실하게 활용할 수 있게 되었습니다. 소프트뱅크가 전고체 배터리 시제품으로 350 Wh/kg을 달성했다고 보고함에 따라 경쟁 압력이 커지면서, 해당 지역 내 기술 경쟁이 격화되었습니다. 이러한 전환은 비행 제어 컴퓨터, 레이더, 갤리 시스템에도 영향을 미쳐 경량화를 실현하는 동시에 추가 적재량을 위한 공간을 확보하게 될 것입니다.

과열 사고가 와이드바디 기종의 도입을 지연시키고 있습니다.

2024년, 미국 연방항공청(FAA)은 여객기 내에서 리튬 배터리로 인한 연기 발생 또는 발화 사고 69건을 기록했으며, 이에 따라 각 항공사는 대형 배터리 팩에 대한 경계를 강화하고 있습니다. 이에 이어 EASA는 프라운호퍼 연구소에 LOKI-PED 시험을 의뢰하여 객실 및 조종실의 화재 위험을 정량화하고 있으며, 그 결과는 2025년에 발표될 예정입니다. 규제 당국은 새로운 취급 절차를 마련 중이지만, 조사 결과에 따르면 보호 장치가 없는 파우치형 배터리는 추락 시의 충격으로 인해 파열될 가능성이 있으므로 견고한 케이스 사용이 의무화되어 있습니다. 따라서 와이드바디기 개발 프로그램에서는 기존 배터리 시스템을 장기간에 걸쳐 계속 사용하고 있으며, 단일 통로기나 지역 노선용 항공기가 전기화되는 상황에서도 시장 규모 확대는 제한적인 수준에 그치고 있습니다.

부문별 분석

2025년, 리튬 이온 배터리는 항공기용 배터리 시장 점유율의 52.34%를 차지했습니다. 이는 공급망이 성숙해 있고, 성능 범위가 충분히 파악되어 있기 때문입니다. 설계자들은 스타터·발전기 용도 및 증가하는 하이브리드 전기 추진 수요에 대응하기 위해, 이 소재의 높은 질량 에너지 밀도를 높이 평가했습니다. 실리콘을 풍부하게 함유한 음극재 등, 최근 용량 향상으로 인해 사이클 수명이 2,000회 이상의 심방전까지 연장되면서, 항공사의 조달 결정에 영향을 미치는 총소유비용(TCO) 지표가 낮아지고 있습니다. 한편, 니켈-카드뮴 전지나 납축전지는 저온 내성이 중량 효율보다 우선시되는 극지 노선이나 회전익기 임무 등, 가혹한 환경에서도 계속해서 실용적으로 사용할 수 있습니다.

항공기용 배터리 시장에서는 리튬-황 배터리에 대한 관심이 높아지고 있으며, 셔틀 효과로 인한 내구성 문제가 공동 연구를 통해 해결됨에 따라 2031년까지 연평균 23.72%의 복합 성장률이 예상됩니다. 초기 비행 시험 결과, 경량 드론의 항속 거리가 20% 향상된 것으로 나타나, 성능에 대한 주장이 입증되었습니다. 미국 해군의 자금 지원을 받고 있는 나트륨 이온 배터리 솔루션은 항공모함 운용에 있어 열적으로 안정된 화학 조성을 가진 배터리가 향후 틈새 시장을 개척할 가능성을 시사하고 있습니다. 이러한 발전에 따라 경쟁의 폭이 넓어지면서, 소규모 혁신 기업들이 항공 업계의 엄격한 안전 기준에 최적화된 셀 구조에 대한 라이선스를 취득하려는 움직임이 가속화되고 있습니다.

2025년 기준으로, 항공기용 배터리 시장 규모의 37.85%를 백업 및 비상용 시스템이 차지했습니다. 이는 인증을 받은 모든 항공기가 발전기 고장 시에도 중요한 무선 장비와 플라이-바이-와이어 제어 시스템에 전력을 공급해야 하기 때문입니다. 그러나 eVTOL 항공기 추진 부문은 두바이, 로스앤젤레스, 싱가포르에서 진행된 도시 모빌리티 시범 운영을 바탕으로 연평균 성장률(CAGR) 28.91%를 기록하며, 다른 모든 부문을 앞지르는 속도로 성장하고 있습니다. 파워 일렉트로닉스 분야의 무어의 법칙에 따른 비용 곡선은 경제적 이점을 더욱 강화하여, 운항사는 200km 미만의 비행에서 좌석 마일당 비용이 지역 터보프롭 항공기보다 낮아질 것으로 예측할 수 있게 되었습니다.

보조 동력 장치(APU)와 항공전자 장비 팩은 경량 리튬 이온 배터리를 채택함으로써 이점을 얻고 있으며, 항공기용 배터리 시장에서 정기 유지보수 빈도를 줄이고 연료 소비량을 절감하고 있습니다. BAE 시스템즈가 하이브리드형 협폭기체 실증기를 위해 개발한 200 kWh 배터리 팩과 같이, 열 관리 하드웨어와 통합된 첨단 배터리 시스템은 모듈식이며 교체 가능한 유닛으로의 전환을 시사하고 있습니다. 이러한 아키텍처의 발전으로 인해 항공사는 기체 자체를 대대적으로 개조하지 않고도 배터리 화학 성분을 업그레이드할 수 있게 되어, 잔존 가치를 높게 유지할 수 있게 됩니다.

지역별 분석

2025년 북미의 매출액은 전체의 30.12%를 차지했습니다. 이는 ‘인플레이션 억제법’ 등의 연방 정책에 따라 국내 배터리 셀 생산 및 전기 항공기 실증 프로그램에 자금이 투입되었기 때문입니다. FAA(연방항공청)의 ‘Innovate28’ 로드맵은 단계적 통합의 주요 단계를 제시하고 있으며, 항공사들은 인증을 받은 전기 항공기 및 하이브리드 항공기 모델을 중심으로 기체 교체 계획을 수립할 수 있게 됩니다. 그러나 수입 리튬 및 희토류에 대한 과도한 의존은 공급망상의 위험을 드러내고 있으며, 장기적인 성장을 저해할 가능성이 있습니다.

아시아태평양은 2026년부터 2031년에 걸쳐 9.72%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 이는 중국의 저고도 경제 구상과, 전 세계 리튬 이온 배터리 생산량의 약 85%를 차지하는 제조 규모가 뒷받침한 결과입니다. 일본의 전고체 배터리 분야의 기술적 돌파구와 한국의 양극재에 관한 전문 지식이 지역의 자급자족 능력을 강화하고 있으며, 이를 통해 현지 OEM 기업들은 경쟁력 있는 가격을 확보할 수 있게 됩니다. 인도 항공 업계의 호황과 드론 배송 시범 운영이 수요를 더욱 끌어올리며, 지역 배터리 공급업체의 고객 기반을 확대되고 있습니다.

유럽은 에어버스, 레오나르도, 그리고 긴밀한 1차 공급업체 네트워크를 기반으로 확고한 입지를 유지하고 있습니다. EU의 배터리 규제는 재활용 소재 함유율 기준 및 탄소 발자국 공개를 의무화하고 있으며, 제품 설계를 순환 경제의 원칙에 부합하도록 이끌고 있습니다. ‘클린 에이비에이션’의 자금 지원으로 하이브리드형 지역 실증기 개발이 가속화되는 한편, 각국의 에너지 전략이 스칸디나비아에서 스페인에 이르는 기가팩토리 건설을 뒷받침하고 있습니다. 이러한 시너지 효과를 가져오는 노력을 통해 유럽은 고가형 지속 가능한 항공 분야에서 입지를 확고히 다지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the aircraft battery market size is expected to grow from USD 0.59 billion in 2025 to USD 0.66 billion in 2026 and is forecast to reach USD 1.12 billion by 2031 at 11.18% CAGR over 2026-2031.

This report is Segmented by Battery Type (Lead Acid, and More), Application (Propulsion, and More), Aircraft Technology (Traditional, and More), Aircraft Type (Fixed-Wing, Rotary Wing, and More), Power Density (Less Than 100Wh/Kg, and More), End-User (Original Equipment Manufacturer (OEM) and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Battery Market Trends and Insights

Adoption of More-Electric Aircraft in North American Narrow-Body Programs

North American airframers are redesigning single-aisle jets around electrical subsystems that replace pneumatic architecture, tripling peak loads during take-off and climb in the aircraft battery market. Demonstrators such as RTX's 1 MW motor aim to cut fuel burn by 30%, aligning with the Clean Aviation initiative that co-funds high-performance battery research. Airlines see lower maintenance costs and carbon compliance value, motivating early retrofits. Battery makers that can validate rapid-charge, high-cycle packs under Federal Aviation Administration (FAA) guidance stand to secure long-term supply contracts.

OEM Shift to Li-ion Batteries for High-Load Avionics in Asia

Chinese, Japanese, and Korean OEMs are phasing out nickel-cadmium units in favor of lithium-ion packs in the aircraft battery market, which study results show reduce supply-chain complexity by 72% and carbon emissions by 75%. Domestic suppliers such as CATL and Gotion High-Tech already reach 500 Wh/kg and 300 Wh/kg, respectively, giving regional manufacturers secure access to advanced chemistries. Competitive pressure intensified when SoftBank reported 350 Wh/kg in all-solid-state prototypes, spurring a regional technology race. The shift will ripple across flight-control computers, radar, and galley systems, cutting weight and freeing space for additional payload.

Thermal-Runaway Incidents Slowing Wide-Body Adoption

In 2024, the FAA logged 69 lithium-battery smoke or fire events aboard passenger aircraft, reinforcing airline caution on large-format packs. EASA followed by commissioning Fraunhofer's LOKI-PED tests to quantify cabin and cockpit fire risk, with results due in 2025. Regulators prepare new handling protocols, while research shows that unprotected pouch cells can shatter at crash speeds, making robust housing mandatory. Wide-body programs, therefore, keep legacy battery systems longer, limiting volume growth even as single-aisle and regional platforms electrify.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Certification Pipeline for eVTOL Air Taxis in Europe

- Military UAV Modernization Driving High-Rate Cells in Middle East

- Scarce Aerospace-Grade Li-S Production Capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion held 52.34% of the aircraft battery market share in 2025, owing to mature supply chains and well-understood performance envelopes. Designers favor its high gravimetric energy for starter-generator duties and growing hybrid-electric thrust demands. Recent capacity enhancements, including silicon-rich anodes, push cycle life past 2,000 deep discharges, lowering total-cost-of-ownership metrics that sway airline procurement. Conversely, nickel-cadmium and lead-acid remain serviceable in hostile environments such as polar routes or rotary-wing missions where low-temperature resilience trumps weight efficiency.

Momentum is shifting toward lithium-sulfur in the aircraft battery market, forecast to compound at 23.72% annually through 2031 as collaborations resolve shuttle-effect durability hurdles. Early flight tests show 20% range gains on light drones, validating performance claims. Sodium-ion solutions under US Navy funding indicate a future niche for thermally stable chemistries in carrier operations.These developments widen the competitive field, encouraging smaller innovators to license cell architectures optimized for aviation's stringent safety codes.

Back-up and emergency systems occupied 37.85% of the aircraft battery market size in 2025 because every certified aircraft must power vital radios and fly-by-wire controls during generator loss. Yet the propulsion segment for eVTOL aircraft is outpacing all categories with 28.91% CAGR, to urban-mobility trials across Dubai, Los Angeles, and Singapore. Moore's law-style cost curves in power electronics amplify the economic case, allowing operators to forecast per-seat-mile costs below regional turboprops for missions under 200 km.

Auxiliary power units (APUs) and avionics packs benefit from lighter lithium-ion formats that cut scheduled maintenance and decrease fuel burn in the aircraft battery market. Advanced battery systems integrated with thermal-management hardware, such as BAE Systems' 200 kWh pack for a hybrid narrow-body demonstrator, signal a shift toward modular, swappable units. This architectural evolution enables airlines to upgrade chemistries without major airframe modifications, keeping residual values high.

Geography Analysis

North America secured 30.12% revenue in 2025 as federal policies such as the Inflation Reduction Act channeled funding into domestic cell production and electric-aircraft demonstration programs. The FAA's Innovate28 roadmap provides step-by-step integration milestones, allowing airlines to plan fleet renewals around certified electric or hybrid models. Yet material reliance on imported lithium and rare-earths exposes a supply-chain risk that could constrain longer-term expansion.

Asia-Pacific posts the fastest 9.72% CAGR during 2026-2031, propelled by China's low-altitude economy blueprint and manufacturing scale, which produces roughly 85% of global lithium-ion output. Japanese all-solid-state breakthroughs and Korean cathode expertise reinforce regional self-sufficiency, allowing local OEMs to lock in competitive pricing. India's aviation upswing and drone-delivery trials add incremental volume, broadening the customer base for regional battery suppliers.

Europe maintains a stronghold built on Airbus, Leonardo, and a dense tier-one supplier network. The EU Battery Regulation mandates recycled-content thresholds and carbon footprint declarations, steering product design toward circular-economy principles. Funding lines from Clean Aviation accelerate hybrid-regional demonstrators, while national energy strategies underwrite gigafactory construction from Scandinavia to Spain. These converging initiatives secure Europe's relevance in premium-priced sustainable aviation segments.

- Saft Groupe SAS

- EnerSys

- EaglePicher Technologies, LLC

- GS Yuasa International Ltd.

- HBL Engineering Limited

- True Blue Power (Mid-Continent Instrument Co., Inc)

- Teledyne Technologies Incorporated

- Sichuan Changhong Battery Co., Ltd.

- Meggitt PLC

- Cella Energy Ltd.

- Kokam Co. Ltd.

- Epsilor-Electric Fuel Ltd.

- Securaplane Technologies Inc.

- Tesla Industries, Inc.

- Concorde Battery Corporation

- InoBat

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Adoption of More-Electric Aircraft (MEA) architecture in North American narrow-body programs

- 4.1.2 OEM shift to Li-ion batteries for high-load avionics in Asia

- 4.1.3 Rapid certification pipeline for eVTOL air-taxis in Europe

- 4.1.4 Military UAV modernization driving high-rate cells in Middle East

- 4.1.5 Government policy support and clean aviation funding

- 4.1.6 Solid-state battery technology breakthroughs

- 4.2 Market Restraints

- 4.2.1 Thermal-runaway incidents slowing wide-body adoption

- 4.2.2 Scarce aerospace-grade Li-S production capacity

- 4.2.3 Nickel and Cobalt price volatility compressing OEM margins

- 4.2.4 Supply chain vulnerabilities and geopolitical tensions

- 4.3 Value Chain Analysis

- 4.4 Regulatory or Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Buyers

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Battery Type

- 5.1.1 Lead-Acid

- 5.1.2 Nickel-Cadmium (NiCd)

- 5.1.3 Lithium-ion (Li-ion)

- 5.1.4 Lithium-sulfur (Li-S)

- 5.2 By Application

- 5.2.1 Propulsion

- 5.2.2 Auxiliary Power Unit (APU)

- 5.2.3 Emergency/Backup

- 5.2.4 Avionics and Flight-Control Actuation

- 5.2.5 Adavanced Battery System

- 5.3 By Aircraft Technology

- 5.3.1 Traditional

- 5.3.2 More-Electric

- 5.3.3 Hybrid-Electric

- 5.3.4 Fully Electric

- 5.4 By Aircraft Type

- 5.4.1 Fixed-Wing

- 5.4.1.1 Commercial Aviation

- 5.4.1.1.1 Narrow-body Aircraft

- 5.4.1.1.2 Wide-Body Aircraft

- 5.4.1.1.3 Regional Jets

- 5.4.1.2 Business and General Aviation

- 5.4.1.2.1 Business Jets

- 5.4.1.2.2 Light Aircraft

- 5.4.1.3 Military Aviation

- 5.4.1.3.1 Fighter Aircraft

- 5.4.1.3.2 Transport Aircraft

- 5.4.1.3.3 Special Mission Aircraft

- 5.4.1.1 Commercial Aviation

- 5.4.2 Rotary Wing

- 5.4.2.1 Commercial Helicopters

- 5.4.2.2 Military Helicopters

- 5.4.3 Unmanned Aerial Vehicles

- 5.4.4 Advanced Air Mobility

- 5.4.1 Fixed-Wing

- 5.5 By Power Density

- 5.5.1 Less than 100 Wh/kg

- 5.5.2 Between 100-300 Wh/kg

- 5.5.3 More than 300 Wh/kg

- 5.6 By End-User

- 5.6.1 Original Equipment Manufacturer (OEM)

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 South Korea

- 5.7.3.4 India

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Saft Groupe SAS

- 6.3.2 EnerSys

- 6.3.3 EaglePicher Technologies, LLC

- 6.3.4 GS Yuasa International Ltd.

- 6.3.5 HBL Engineering Limited

- 6.3.6 True Blue Power (Mid-Continent Instrument Co., Inc)

- 6.3.7 Teledyne Technologies Incorporated

- 6.3.8 Sichuan Changhong Battery Co., Ltd.

- 6.3.9 Meggitt PLC

- 6.3.10 Cella Energy Ltd.

- 6.3.11 Kokam Co. Ltd.

- 6.3.12 Epsilor-Electric Fuel Ltd.

- 6.3.13 Securaplane Technologies Inc.

- 6.3.14 Tesla Industries, Inc.

- 6.3.15 Concorde Battery Corporation

- 6.3.16 InoBat

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment