|

시장보고서

상품코드

2066519

고압 다이캐스트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)High-Pressure Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

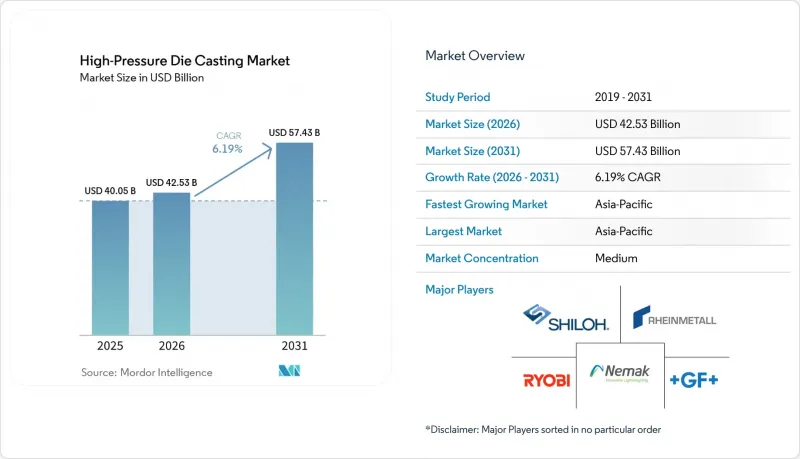

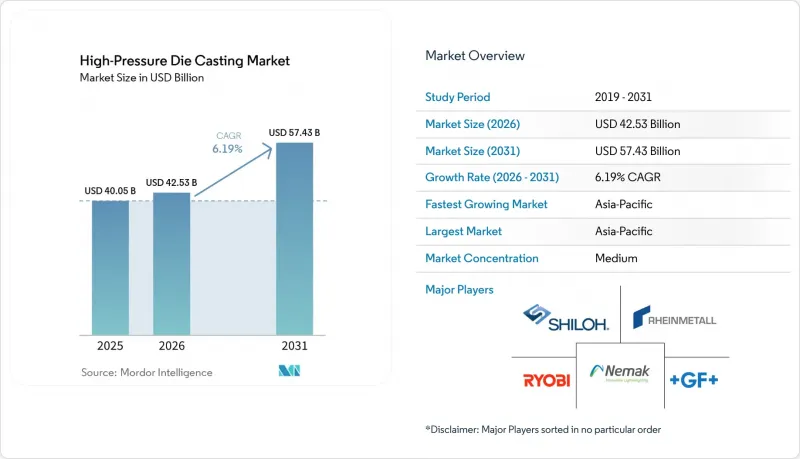

Mordor Intelligence에 의하면, 고압 다이캐스트 시장 규모는 2025년 400억 5,000만 달러로 평가되었습니다. 2026년에는 425억 3,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 6.19%로 성장을 지속하여, 2031년에는 574억 3,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 원자재 유형(알루미늄, 아연 등), 용도(자동차, 전기 및 전자기기 등), 생산 공정(진공 HPDC 및 스퀴즈 HPDC), 최종 용도 부품(엔진 및 파워트레인 부품 등), 지역(북미, 남미 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 고압 다이캐스트 시장 동향 및 인사이트

차세대 기가프레스 도입

각 자동차 제조업체는 6,000톤이 넘는 프레스 설비를 도입하여 차체 하부 전체를 한 번의 주조 공정으로 성형함으로써, 부품 수를 170개 이상의 프레스 성형품에서 5개 미만의 구조용 주조품으로 대폭 줄이고 있습니다. 테슬라는 프리몬트와 베를린에서 이 방식을 선구적으로 도입하여, 24시간 가동되는 9,000톤 규모의 생산 셀을 운영하고 있습니다. BYD나 NIO 등 아시아의 각 OEM 업체들도 그 후 유사한 프레스 설비를 도입했으며, 볼보 등 유럽 브랜드들도 슬로바키아에서 이에 발맞추고 있습니다. 이러한 통합을 통해 여러 개의 프레스 금형과 용접 스테이션이 불필요해지며, 라인 옆의 재고가 줄어들고 조립 시간이 대폭 단축됩니다. 그러나 프레스 한 대만 고장 나도 최종 조립 라인 전체가 중단되기 때문에 이중화 확보와 예측 유지보수 소프트웨어는 위험을 줄이기 위한 매우 중요한 수단이 되고 있습니다. 기가프레스 도입 자금을 확보하지 못하는 주조 업체들은 틈새 시장인 마그네슘 주조 분야로 전환하거나, 설비 공급업체와의 합작 사업을 모색하여 대량 생산 프로그램에 계속 참여하려고 하고 있습니다.

내연기관에서 전기자동차로의 전환을 통한 경량화 추진

배터리 팩은 차량에 400-700 kg의 무게를 더하기 때문에 엔지니어들은 다른 부위의 경량화를 도모할 수밖에 없습니다. 얇은 두께의 알루미늄 및 마그네슘 부품에 대한 고압 다이캐스트 시장 수요가 증가하고 있습니다. 이는 이러한 소재가 프레스 가공된 강재에 비해 30%-50%의 경량화를 실현하기 때문입니다. 2025년에 시행된 유로 7 미세먼지 배출 규제에 따르면, 브레이크나 타이어 마모로 인한 배출량이 적은 경량 차량이 우대받게 됩니다. 그 결과, 전 세계 주요 OEM 업체들은 다이캐스팅의 적용 범위를 엔진 블록에서 시트 프레임, 크로스 멤버, 배터리 트레이로 확대되고 있습니다. 마그네슘의 강도 대 중량 비율의 장점 덕분에 모터 하우징이나 내장용 브라켓에 마그네슘을 사용하는 사례가 늘고 있지만, 재료비와 갈바닉 부식의 위험이 여전히 도입의 걸림돌로 작용하고 있습니다. 중국의 신에너지차에 대한 엄격한 할당 제도와 인도의 수출 장려 정책에 힘입어 아시아태평양이 이러한 추세를 주도하고 있습니다.

복잡한 부품의 경우 막대한 초기 설비 투자가 필요합니다.

기가프레스 라인 1개의 비용은 약 3,000만 달러에 달하며, 대형 구조용 주조품의 금형에는 추가로 500만-1,000만 달러가 소요되고, 리드타임은 12-18개월이 걸립니다. 이러한 투자를 정당화할 수 있는 것은 재무 기반이 탄탄한 공급업체나, 합작 투자를 통해 위험을 분담하고 있는 공급업체로 한정됩니다. 대기업들이 틈새 시장을 공략하는 주조 업체를 인수하고, 여러 프로그램을 통해 금형 비용을 상각함으로써 업계 재편이 가속화되고 있습니다. 전기자동차 생산 대수가 확정되지 않은 상황에서 중소규모 사업자들은 설비 투자를 미루고 있으며, 그 결과 지역 생산 능력 확대가 제한되고 OEM공급망이 장기화되고 있습니다.

부문별 분석

알루미늄은 유동성, 내식성, 그리고 확립된 스크랩 공급망에 힘입어 2025년 시장 규모의 69.84%를 차지했습니다. 재활용 소재의 함유율은 평균 75%이며, 주요 자동차 제조업체들은 계약 체결 시 검증 증명서 제출을 요구하고 있습니다. 마그네슘은 모터 하우징 및 스티어링 브래킷의 대폭적인 경량화를 통해 연평균 성장률(CAGR) 8.32%를 기록하며 성장하고 있지만, 원자재 가격 급등과 갈바닉 부식 관리상의 제약으로 인해 고급 전기자동차 플랫폼에 한정적으로만 채택되고 있습니다. 아연은 소형 커넥터나 EMI 차폐 하우징에 여전히 선호되고 있지만, 현재는 폴리머로 대체될 압박에 직면해 있습니다.

폐쇄형 합금 프로그램은 알루미늄 원자재 비용을 절감하고 스코프 3 배출량을 대폭 줄여줌으로써, 일괄 생산을 수행하는 가공업체에 가격 면에서의 우위를 제공합니다. 마그네슘 재활용 노력은 일본과 독일에서 도입된 불활성 분위기 재용해로를 통해 진전을 보이고 있지만, 산화로 인한 손실은 여전히 10%를 초과하고 있습니다. 알루미늄 부품용 고압 다이캐스트 시장 규모는 한 자릿수 중반대의 성장세를 유지할 것으로 예상되는 반면, 마그네슘의 틈새 시장은 기반은 낮지만 2031년까지 가장 빠른 속도로 확대될 것으로 전망됩니다.

자동차 분야는 2025년 매출의 61.23%를 차지했으며, 이는 수십 년에 걸친 엔진 블록 및 변속기 케이스의 다이캐스팅 제조 실적을 반영한 것입니다. 전기자동차(EV) 및 전동 파워트레인 분야는 연평균 8.89%의 성장률이 예상되며, 고압 다이캐스트 시장의 확대에 따른 혜택을 누릴 것으로 전망됩니다. 전기 및 전자 분야의 성장 속도는 완만하지만, 이는 LED 방열판이나 커넥터 쉘이 압출 성형이나 사출 성형되는 사례가 늘어나고 있기 때문입니다. 반면, 산업용 장비의 경우 압력기나 펌프의 형상을 만드는 데 다이캐스팅이 필수적이지만, 자동차 분야에 필적할 만한 생산량에는 미치지 못하고 있습니다.

중국과 인도의 규제상 우대 조치가 자동차용 주조 수요를 뒷받침하고 있으며, 현지 공급업체들은 기가프레스를 확보하기 위해 합작회사를 설립하고 있습니다. 한편, 전자기기 분야 수요는 소형화와 복합 소재 및 플라스틱을 사용한 저전력 디바이스로의 전환에 따라 세분화가 진행되고 있습니다. 그 결과, 자동차 분야의 매출 점유율은 확대되는 반면, 그 밖의 용도는 저-중 한 자릿수 성장에 그칠 것으로 전망됩니다.

지역별 분석

아시아태평양은 2025년 매출의 47.37%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 7.57%로 확대될 것으로 전망되어, 모든 지역을 능가하는 성장률을 보이고 있습니다. 2025년 중국에서 1,500만 대를 넘어선 신에너지차의 보급은 배터리 인클로저와 기가프레스용 언더바디에 대한 전례 없는 수요를 창출했습니다. 인도에서는 수출 연계형 인센티브가 다이캐스팅 생산 능력 확대를 뒷받침한 반면, 일본과 한국의 파운드리들은 고부가가치 수주를 확보하기 위해 진공 셀로 설비를 현대화했습니다. 숙련된 노동력 부족과 전력 가격 상승에도 불구하고, 이 지역공급망은 여전히 비용 경쟁력을 갖추고 있으며 통합이 진행되고 있습니다.

유럽은 2025년에 견고한 기반을 다지고, 배터리 기가팩토리 투자에 따른 현지 조달률 규제의 뒷받침을 받아 2031년까지 연평균 5.19%의 성장률을 보일 것으로 전망됩니다. 탄소 국경 조정세로 인해 EU 역외 공급업체들은 용융 합금 생산 라인의 현지화를 추진하고 있으며, 슬로바키아와 스웨덴에 기가프레스를 도입함으로써 주요 OEM에 대한 공급이 확보되고 있습니다. 높은 에너지 비용이 이익률을 압박하고 있어, 자동화 및 재생에너지 구매 계약의 도입이 가속화되고 있습니다.

북미는 전기자동차의 꾸준한 보급을 반영하고 있음에도 불구하고, 프레스 설비 도입 속도는 둔화되고 있으며, 2031년까지 4.99%의 성장이 예상됩니다. 미국의 파운드리은 국내 조립 공장에 부품을 공급하기 위해 진공 셀을 도입한 반면, 멕시코의 시설은 낮은 인건비를 활용하고 있지만, 안전상 중요한 부품에 대해서는 설비 업그레이드가 요구되고 있습니다. 캐나다는 여전히 틈새 시장이지만, 온타리오주와 퀘벡주에 배터리 공급 거점이 생겨남에 따라 성장세가 가속화될 가능성이 있습니다. 남미의 예상 연평균 성장률(CAGR) 3.87%는 자동차 생산의 정체와 전기자동차 보급률의 저조를 반영하고 있으며, 브라질이 제한적인 성장의 주축을 이루고 있습니다. 중동 및 아프리카는 연평균 성장률(CAGR) 2.56%를 나타낼 것으로 예측되지만, 주목할 만한 다이캐스팅 산업 클러스터가 존재하는 곳은 튀르키예와 남아프리카공화국뿐입니다. 현지의 전기자동차 관련 노력은 아직 초기 단계에 있으며, 생산 대수도 적은 상황입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the high-pressure die casting market size is expected to grow from USD 40.05 billion in 2025 to USD 42.53 billion in 2026 and is forecast to reach USD 57.43 billion by 2031 at a 6.19% CAGR over 2026-2031.

This report is Segmented by Raw Material Type (Aluminum, Zinc, and More), Application (Automotive, Electrical and Electronics, and More), Production Process (Vacuum HPDC and Squeeze HPDC), End-Use Component (Engine and Powertrain Parts and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global High-Pressure Die Casting Market Trends and Insights

Next-Gen Giga-Press Installations

Automakers are rolling out over 6,000-ton presses to cast full underbodies in one shot, slashing part counts from over 170 stampings to fewer than five structural castings. Tesla pioneered this template at Fremont and Berlin and operates 9,000-ton cells that run 24-hour cycles. Asian OEMs such as BYD and NIO have since installed similar presses, while European brands like Volvo followed suit in Slovakia. This consolidation eliminates multiple stamping dies and welding stations, cuts line-side inventory, and reduces assembly time significantly. However, a single-press failure can halt an entire final-assembly line, so redundancy and predictive-maintenance software have become critical risk-mitigation tools. Foundries unable to fund giga-presses either move into niche magnesium castings or seek joint ventures with equipment suppliers to remain in high-volume programs.

Light-Weighting Push From ICE-to-EV Shift

Battery packs add 400-700 kg to a vehicle, driving engineers to cut mass elsewhere. High-pressure die casting market demand for thin-wall aluminum and magnesium parts is rising because these substrates deliver 30%-50% weight savings over stamped steel. Euro 7 particulate limits that took effect in 2025 reward lighter vehicles with lower brake- and tire-wear emissions. Major global OEMs are consequently transferring die-casting from engine blocks to seat frames, cross-members, and battery trays. Magnesium's strength-to-weight edge is boosting take-up for motor housings and interior brackets, though material cost and galvanic corrosion risks remain adoption hurdles. Asia-Pacific leads this trend due to China's stringent new-energy vehicle quotas and India's export incentives.

High Upfront Capex for Complex Parts

A single giga-press line can cost around USD 30 million, while dies for a large structural casting add USD 5-10 million with 12-18-month lead times. Only suppliers with strong balance sheets, or those sharing risk through joint ventures, can justify these investments. Consolidation is accelerating as large players acquire niche foundries to amortize tooling across multiple programs. Without committed EV volumes, smaller operators delay capex, which in turn limits regional capacity growth and elongates OEM supply chains.

Other drivers and restraints analyzed in the detailed report include:

- Battery-Housing Thermal-Management Requirements

- OEM Demand for Near-Net-Shape Parts

- Porosity and Weld-Line Quality Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Aluminum captured 69.84% of the 2025 market size, supported by fluidity, corrosion resistance, and mature scrap streams. Recycled content averaged 75%, and leading automakers require verification certificates when awarding contracts. Magnesium is rising at an 8.32% CAGR due to significant weight savings in motor housings and steering brackets, but higher raw-material costs and galvanic-corrosion management constraints confine it to premium EV platforms. Zinc remains favored for small connectors and EMI-shielded housings, but is now facing pressure to be replaced by polymers.

Closed-loop alloy programs lower aluminum feedstock costs and slash Scope 3 emissions, giving integrated processors a pricing edge. Magnesium recycling efforts are advancing via inert-atmosphere remelters launched in Japan and Germany, though oxidation losses still exceed 10%. The high-pressure die casting market size for aluminum parts is projected to sustain mid-single-digit growth, while the magnesium niche expands from a lower base but at the fastest rate through 2031.

Automotive contributed 61.23% of 2025 revenue, reflecting decades of die-cast engine blocks and transmission cases. The EV and electrified powertrain subset is forecast to grow 8.89% annually, capturing the expansion premium in the high-pressure die-casting market. Electrical and electronics applications grow at a slower clip because LED heatsinks and connector shells are increasingly extruded or molded. In contrast, industrial equipment requires die casting for compressor and pump geometries but lacks the volume to match automotive.

Regulatory incentives in China and India underpin automotive casting demand, with local suppliers forming joint ventures to secure giga-presses. Conversely, electronic demand is fragmenting due to miniaturization and the shift toward lower-power devices that use composites or plastics. As a result, automotive will deepen its revenue share, while other applications maintain low-to-mid-single-digit growth.

Geography Analysis

Asia-Pacific accounted for 47.37% of 2025 sales and is projected to rise at a 7.57% CAGR through 2031, outpacing all regions. China's over 15 million new-energy vehicles in 2025 created unprecedented pull for battery enclosures and giga-press underbodies. India's export-linked incentives galvanized die-cast capacity expansions, while Japanese and South Korean foundries upgraded to vacuum cells to win premium contracts. Despite skilled-labor shortages and rising power prices, regional supply chains remain cost-competitive and integrated.

Europe posted a solid 2025 base and will grow 5.19% through 2031, buoyed by local content rules tied to battery-gigafactory investments. Carbon-border tariffs are prompting non-EU suppliers to localize fused alloy lines, and giga-press installations in Slovakia and Sweden secure supply for leading OEMs. High energy costs pressurize margins, accelerating automation and renewable-power purchase agreements.

North America is set to expand 4.99% through 2031, reflecting steady EV adoption but slower press installations. U.S. foundries add vacuum cells to serve domestic assembly plants, while Mexican facilities leverage lower labor costs, yet must upgrade for safety-critical parts. Canada remains a niche market but may gain traction as battery supply hubs emerge in Ontario and Quebec. South America's 3.87% forecasted CAGR mirrors stagnant vehicle output and low EV penetration; Brazil anchors limited growth. Middle East and Africa will post 2.56% CAGR, with only Turkey and South Africa hosting notable die-casting clusters; local EV initiatives are nascent, and volumes are low.

- Buhler AG

- Idra Srl

- Dynacast International

- Ryobi Die Casting

- Nemak

- GF Casting Solutions

- Shiloh Industries

- Gibbs Die Casting

- Sundaram-Clayton

- Magna International

- Pace Industries

- Endurance Technologies

- Hitachi Astemo

- Ahresty

- Castwell Industries

- Aludyne

- Montupet (Linamar)

- Gibbs-Mexico

- TOYOTA Boshoku Die-Casting

- BOHAI Automotive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Next-Gen Giga-Press (Over 6,000 t) Installations by Automakers

- 4.2.2 Light-Weighting Push from ICE-to-EV Shift

- 4.2.3 Battery-Housing Thermal-Management Requirements

- 4.2.4 OEM Demand for Near-Net-Shape Parts to Cut Post-Machining

- 4.2.5 Regional Carbon-Border Tariffs Driving Local HPDC Capacity

- 4.2.6 Rising Alloy Price Volatility Favouring HPDC Scrap-Recycling Loops

- 4.3 Market Restraints

- 4.3.1 High Upfront Capex and Tooling Cost for Complex Parts

- 4.3.2 Porosity and Weld-Line Quality Issues vs. Counter Casting Routes

- 4.3.3 Energy-Intensive Furnaces Under Tightening ESG Mandates

- 4.3.4 Skilled-Operator Shortage for Multi-Cavity HPDC Cells

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Raw Material Type

- 5.1.1 Aluminum

- 5.1.2 Zinc

- 5.1.3 Magnesium

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Industrial Applications

- 5.2.4 Other Applications

- 5.3 By Production Process

- 5.3.1 Vacuum HPDC

- 5.3.2 Squeeze HPDC

- 5.4 By End-Use Component

- 5.4.1 Engine and Powertrain Parts

- 5.4.2 Body and Structural Parts

- 5.4.3 Transmission Parts

- 5.4.4 EV Battery Housing and Motor Components

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Buhler AG

- 6.4.2 Idra Srl

- 6.4.3 Dynacast International

- 6.4.4 Ryobi Die Casting

- 6.4.5 Nemak

- 6.4.6 GF Casting Solutions

- 6.4.7 Shiloh Industries

- 6.4.8 Gibbs Die Casting

- 6.4.9 Sundaram-Clayton

- 6.4.10 Magna International

- 6.4.11 Pace Industries

- 6.4.12 Endurance Technologies

- 6.4.13 Hitachi Astemo

- 6.4.14 Ahresty

- 6.4.15 Castwell Industries

- 6.4.16 Aludyne

- 6.4.17 Montupet (Linamar)

- 6.4.18 Gibbs-Mexico

- 6.4.19 TOYOTA Boshoku Die-Casting

- 6.4.20 BOHAI Automotive

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment