|

시장보고서

상품코드

2066552

현미외과용 기구 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Microsurgical Instruments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

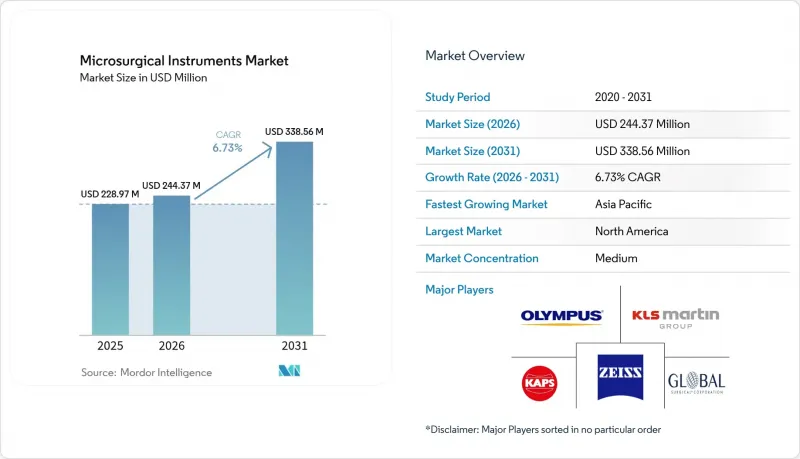

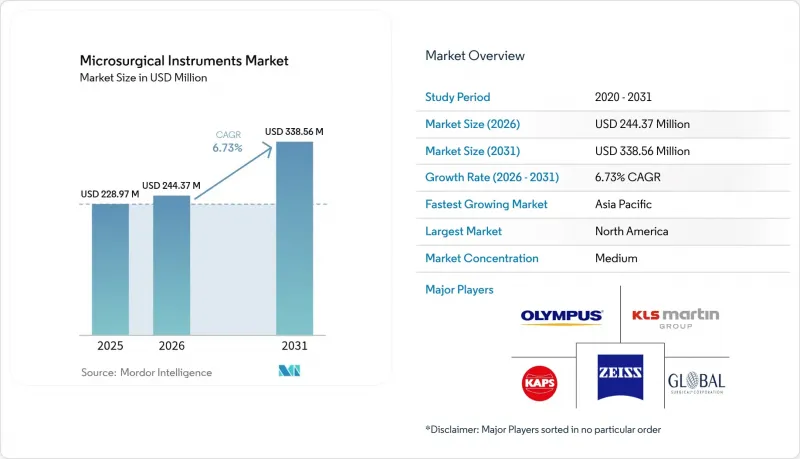

Mordor Intelligence에 의하면, 현미외과용 기구 시장 규모는 2025년에 2억 2,897만 달러로 평가되었습니다. 2026년 2억 4,437만 달러에서 2031년까지 3억 3,856만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.73%를 나타낼 전망입니다.

본 보고서는 제품별(마이크로 봉합사, 마이크로 집게, 수술용 현미경, 마이크로 가위, 마이크로 바늘 홀더 등), 마이크로서저리유형별(정형외과, 안과, 이비인후과, 신경외과 등), 최종 사용자별(병원, 외래수술센터(ASC) 등), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 현미외과용 기구 시장 동향 및 인사이트

기존 수술에 비해 미세수술의 장점

미세수술은 신경 복원이나 림프관 재건 분야에서 뛰어난 치료 성과를 보이기 때문에 고액의 보수가 지급되는 사례가 증가하고 있습니다. 2024년, 미국의 한 학술 기관은 자유 피판에 의한 유방 재건술의 성공률이 95%에 달했다고 보고했는데, 이는 유두부 피판의 성공률인 78%를 크게 웃도는 수치입니다. 그러나 펠로우십 수용 정원에는 여전히 병목 현상이 존재하며, 2024년 미국에는 인증된 미세수술 연수 정원이 고작 180개에 불과했습니다. 이러한 제약에 대응하기 위해 각 장비 공급업체들은 기술 습득을 가속화하고, 훈련을 받은 전문가층을 확대하기 위한 시뮬레이션 모듈에 투자하고 있습니다. 이처럼 숙련된 시술자 증가가 현미경, 클램프, 봉합사 등 필수 기구에 대한 수요 증가를 뒷받침하고 있습니다.

수술 건수 증가와 만성 질환의 발생률

인구 고령화와 전 세계적인 당뇨병 부담으로 인해 수술 건수가 증가하고 있으며, 현미외과용 기구 시장은 향후 몇 년간 성장이 예상됩니다. 2060년까지 중국의 의료 지출이 33조 4,000억 달러에 달할 것이라는 전망은 3차 의료기관에서의 대규모 의료기기 도입을 시사하고 있습니다. 당뇨병성 망막병증은 망막 현미경 수술의 기준을 크게 높이고 있는 반면, 관상동맥 우회술이나 종양 절제술의 경우, 기존의 기구로는 실현할 수 없는 신경 보존을 위한 정밀성이 요구되고 있습니다. 아시아 각국 정부는 안과 및 심혈관 외과 수술실을 위한 조달 예산을 배정하고 있어, 매력적인 일괄 구매 기회를 창출하고 있습니다. 서유럽의 의료 시스템은 이미 성숙 단계에 접어들었으나, 재수술 및 평균 수명의 연장으로 인해 여전히 성장이 예상됩니다. 이에 대응하여 의료기기 제조업체들은 중규모 시설에서의 도입 장벽을 낮추기 위해 현미경, 집게, 생체흡수성 봉합사를 세트로 구성한 스타터 키트를 맞춤형으로 제공하며 대응하고 있습니다.

첨단 현미경 수술 시스템의 높은 비용

고급 로봇 현미경의 정가는 100만 달러를 초과하며, 유지보수 계약과 멸균 처리된 소모품을 포함하면 10년간의 소유 비용은 2배로 늘어날 수도 있습니다. 신흥 시장의 병원에서는 제한된 자금을 필수적인 영상 진단 장비나 중환자실 병상에 할당하기 위해, 현미경 수술 시스템의 업그레이드는 미루는 경향이 있습니다. 북미의 소규모 지역 의료기관들도 시스템 일체를 도입하기 전에 수술 건수 기준을 신중하게 검토하고 있으며, 대신 기능이 제한된 재생 제품을 선택하는 경향이 있습니다. 각 벤더사는 이용료 기반 리스, 이익 분배 모델, 그리고 핵심인 광학 시스템부터 도입한 뒤 나중에 로봇 암을 추가할 수 있는 모듈식 구성 등을 통해 고가라는 점으로 인한 심리적 장벽을 완화하고 있습니다. 의료의 질과 관련된 목표에 연계된 정부의 조달 보조금은 설비 투자의 장벽을 부분적으로 상쇄하고 있지만, 저비용 수동식 세트와의 가격 경쟁력을 확보하기 위해서는 앞으로 몇 번의 주기가 더 필요할 가능성이 있습니다.

부문별 분석

2025년에는 수술용 현미경이 총매출의 29.12%를 차지하며, 초기 프로그램 투자에 대한 높은 투자 수익률을 반영했습니다. 한편, 마이크로 봉합사는 가장 빠른 성장이 예상되며, 2031년까지의 연평균 성장률(CAGR)은 8.92%로 전망됩니다. 재건 수술 및 소아 외과 수술 건수 증가에 따른 수요 증가에 힘입어, 마이크로 봉합사 시장은 예측 기간이 끝날 때까지 성장할 것으로 전망됩니다.

소모품 비용은 여전히 중요한 요소입니다. 예를 들어, 자유 피판 재건 수술 1건에는 1개당 150달러짜리 고품질 봉합사가 최대 15개가 필요할 수 있습니다. 한편, 마이크로 집게나 가위의 경우, ISO 인증을 획득한 중국산 수출품이 유럽 및 미국 브랜드 제품보다 최대 60% 저렴한 가격에 공급되고 있어, 심각한 상품화 압력에 직면해 있습니다. 디지털 기술의 발전으로 인해 현미경의 성능이 향상되고 수명이 연장되고 있습니다. 예를 들어, ZEISS사의 MICOR 700은 증강현실(AR) 오버레이 기능을 활용함으로써 프리미엄 가격 책정을 정당화하고 있습니다. 하드웨어 제품과 구독형 소모품을 효과적으로 통합하고 있는 제조업체는 끊임없이 진화하는 현미외과용 기구 시장에서 안정적인 수익원을 확보하는 데 유리한 입장에 있습니다.

지역별 분석

북미는 수술실의 디지털화가 정착되어 있고, 고가의 시각화 플랫폼 비용을 충당할 수 있는 유리한 보험 환급 제도의 지원을 받아 2025년 매출의 38.25%를 차지했습니다. 클리블랜드 클리닉과 광학 제조업체간의 제휴와 같은 지역적 교육 제휴를 통해 증강현실(AR) 기반 안내 시스템이 시범적으로 도입되었으며, 이는 제휴 병원 전체의 조달 프로세스에 직접 반영되고 있습니다. 수술 장소의 전환은 여전히 그 기세를 잃지 않고 있습니다. 현재 외래수술센터(ASC)에서는 어깨 회전근개 봉합술의 60% 이상이 시행되고 있으며, 이에 따라 소형 현미경 및 일회용 봉합 카트리지에 대한 수요가 확보되고 있습니다. 이 지역에서는 가치 기반 계약을 통해 현미외과용 기구 시장이 가격 결정력을 유지하고 있습니다. 이 계약에서는 재입원율 감소에 따라 보너스 지급이 보장되어, 고가의 의료기기 비용을 상쇄하고 있습니다.

유럽은 여전히 두 번째로 큰 구매 시장이며, 독일, 프랑스, 북유럽 국가들에서 도입이 활발히 이루어지고 있습니다. 해당 지역에서는 엄격한 외과 의사 자격 인증과 수명 주기 비용을 우선시하는 중앙집권적인 입찰 체계가 중시되고 있으며, 이로 인해 공급업체들은 보증 기간 연장이나 예측 유지보수 패키지 제공을 요구받고 있습니다. EU 의료기기 규정(MDR) 준수에 드는 비용은 신규 진입 장벽을 높여, 간접적으로 기존 기업의 시장 점유율을 지켜주고 있습니다. 그러나 남유럽에서는 여전히 긴축 재정 정책의 제약이 남아 있어, 성장률은 한 자릿수 중반에 머물고 있습니다. 이러한 부정적 요인은 폴란드와 체코 공화국에서 민간 병원 네트워크가 확대됨에 따라 부분적으로 상쇄되고 있습니다. 이 병원들은 독일의 기준을 따르는 경우가 많으며, 그 때문에 최고급 현미경을 구입하고 있습니다.

아시아태평양은 중국과 인도의 의료 인프라가 급속히 확대된 데 힘입어 9.14%라는 가장 높은 연평균 성장률(CAGR)을 기록하고 있습니다. 중국의 ‘건강중국 2030’ 계획이나 인도의 ‘아유슈만 바라트’ 보험 제도 등 정부 주도의 노력에 힘입어, 대상 환자층이 확대되고 있습니다. 중국의 3급 의료 구역에서는 현지 의료기기 조립에 대해 세제 혜택이 적용되고 있으며, 이를 통해 외국 브랜드는 리드타임을 단축하고 각 성의 입찰을 수주할 수 있게 되었습니다. 중산층의 기대감이 높아짐에 따라 백내장 수술 및 굴절 교정 수술의 보급이 가속화되면서 안과용 기기 수입이 늘어나고 있습니다. 귀국한 엔지니어를 다수 고용하고 있는 현지 스타트업은 3차 의료기관과 제휴하여 가성비가 뛰어난 현미경을 공동 개발하고 있으며, 이는 경쟁을 촉진하는 한편 전반적인 보급을 촉진하고 있습니다. 성숙기를 맞이하면서도 고령화가 진행되고 있는 일본과 한국에서는 의료기관들이 1세대 디지털 현미경을 로봇 연동형으로 교체함에 따라 교체 수요가 견인되어 지역별 출하 대수가 유지되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the microsurgical instruments market size was valued at USD 228.97 million in 2025 and is estimated to grow from USD 244.37 million in 2026 to reach USD 338.56 million by 2031, at a CAGR of 6.73% during the forecast period (2026-2031).

This report is Segmented by Product (Micro Sutures, Micro Forceps, Operating Microscopes, Micro Scissors, Micro Needle Holders, and More), Microsurgery Type (Orthopedic, Ophthalmic, ENT, Neurological, and More), End-User (Hospitals, Ambulatory Surgical Centers and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Microsurgical Instruments Market Trends and Insights

Microsurgery Advantage Over Conventional Surgery

Microsurgical procedures are increasingly being reimbursed at premium rates due to their superior outcomes in nerve repair and lymphatic reconstruction. In 2024, U.S. academic centers reported a 95% success rate for free-flap breast reconstruction, significantly surpassing the 78% success rate for pedicled flaps. However, a bottleneck persists in fellowship capacity, with only 180 accredited microsurgery training slots available in the U.S. in 2024. To address this limitation, equipment suppliers are investing in simulation modules to expedite skill acquisition and expand the pool of trained professionals. This increase in skilled practitioners is driving higher demand for essential tools such as microscopes, clamps, and sutures.

Rising Surgical Volumes and Chronic Disease Incidence

Population aging and the global diabetes burden underpin rising procedure counts, ensuring multi-year growth for the microsurgical instruments market. China's health expenditure outlook of USD 33.4 trillion by 2060 signals large equipment pools across tertiary centers. Diabetic retinopathy drives a high baseline of retinal microsurgery, while coronary artery bypass and tumor resections require nerve-sparing precision that legacy tools cannot deliver. Governments in Asia allocate procurement budgets for ophthalmic and cardiovascular suites, creating attractive bulk-purchase opportunities. Western systems, although mature, still see growth from revision surgeries and longer life expectancy. Device makers respond by tailoring starter kits that bundle microscopes, forceps, and bio-resorbable sutures to lower adoption friction in mid-tier facilities.

High Cost of Advanced Microsurgical Systems

Premium robotic microscopes command list prices exceeding USD 1 million, while maintenance contracts and sterile consumables can double ten-year ownership costs. Emerging-market hospitals divert limited capital toward essential imaging or ICU beds, leaving microsurgical upgrades on deferred wish lists. Smaller North American community facilities also weigh volume thresholds before committing to complete suites, opting instead for refurbished units that offer limited functionality. Vendors counteract sticker shock with pay-per-use leasing, profit-sharing models, and modular build-outs that start with core optics, then add robotic arms later. Government procurement grants tied to quality-of-care targets partially offset capex barriers, yet parity with lower-cost manual sets may take additional cycles.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Digital Microscopes and Robotics

- Growing Demand for Minimally Invasive Procedures

- Stringent Device-Approval Pathways (Class III)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, operating microscopes contributed 29.12% of total revenue, reflecting a strong return on initial program investments. At the same time, micro sutures are projected to grow the fastest, with an anticipated CAGR of 8.92% through 2031. Driven by increasing demand for high-volume reconstructive and pediatric cases, the microsuture market is expected to grow by the end of the forecast period.

Consumable economics remain a critical factor; for example, a single free-flap reconstruction may require up to 15 units of premium sutures, each priced at USD 150. Meanwhile, micro forceps and scissors face significant commoditization pressures, with ISO-certified Chinese exports offering prices up to 60% lower than Western brands. Digital advancements are enhancing capabilities and extending the life cycles of microscopes. For instance, ZEISS's MICOR 700 utilizes augmented-reality overlays to justify premium pricing. Manufacturers that effectively integrate hardware offerings with subscription-based consumables are well-positioned to secure consistent revenue streams in the evolving microsurgical instrument market.

Geography Analysis

North America generated 38.25% of 2025 revenue, supported by entrenched OR digitization and favorable reimbursement that covers high-ticket visualization platforms. Regional teaching alliances, such as Cleveland Clinic's collaboration with optics manufacturers, pilot augmented-reality guidance that feeds directly into procurement pathways across affiliated hospitals. Site-of-service migration continues unabated; ASCs now execute more than 60% of rotator cuff repairs, ensuring replacement demand for compact microscopes and single-use suture cartridges. The microsurgical instruments market maintains pricing power here due to value-based contracting, where lower readmission rates secure bonus payments that offset premium device costs.

Europe remains the second-largest buyer pool, with strong adoption in Germany, France, and the Nordics. The region leans on rigorous surgeon credentialing and centralized tender frameworks that prioritize lifecycle cost, pushing vendors to extend warranty periods and offer predictive maintenance packages. EU MDR compliance expenses elevate barriers for new entrants, indirectly protecting incumbent share. Growth, however, is more tempered at mid-single-digit rates as austerity constraints linger in Southern Europe. That drag is partially offset by expanding private hospital networks in Poland and the Czech Republic, which often emulate German standards and thus purchase top-tier microscopes.

Asia-Pacific posts the highest CAGR at 9.14%, buoyed by rapid healthcare infrastructure expansion in China and India. Government initiatives such as China's Healthy China 2030 blueprint and India's Ayushman Bharat insurance scheme enlarge addressable patient pools. Chinese class-III medical zones grant tax incentives for local device assembly, enabling foreign brands to shorten lead times and capture provincial tenders. Rising middle-class expectations accelerate penetrative depth in cataract and refractive surgery, bolstering ophthalmic instrument imports. Local start-ups, often staffed by returnee engineers, collaborate with tertiary hospitals to co-develop cost-effective microscopes, injecting competitive pressure yet broadening overall adoption. Japan and South Korea, mature but aging societies, drive replacement sales as facilities swap first-generation digital scopes for robotics-ready variants, preserving regional unit shipment volume.

- Alcon

- B. Braun

- Baxter

- Beaver-Visitec International, Inc.

- Danaher

- Global Surgical

- HAAG-Streit

- Integra LifeSciences

- Johnson & Johnson Services, Inc. (Ethicon)

- Karl Kaps

- Karl Storz SE

- KLS Martin Group

- Danaher

- Medical Microinstruments SpA

- Medtronic

- MicroSure BV

- Microsurgery Instruments Inc.

- Olympus

- Scanlan International

- Stille

- Stryker

- Teleflex

- Virtuoso Surgical Inc.

- Carl Zeiss

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Microsurgery Advantage Over Conventional Surgery

- 4.2.2 Rising Surgical Volumes & Chronic Disease Incidence

- 4.2.3 Technological Advances In Digital Microscopes & Robotics

- 4.2.4 Growing Demand For Minimally-Invasive Procedures

- 4.2.5 4K/3-D OR Integration Accelerating Micro-Instrument Upgrades

- 4.2.6 Emergence Of Bio-Resorbable Micro-Sutures

- 4.3 Market Restraints

- 4.3.1 High Cost Of Advanced Microsurgical Systems

- 4.3.2 Stringent Device-Approval Pathways (Class III)

- 4.3.3 Shortage Of Trained Microsurgeons In Emerging Markets

- 4.3.4 Budget Shift Toward Robotic Platforms Cannibalising Manual Sets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Micro Sutures

- 5.1.2 Micro Forceps

- 5.1.3 Operating Microscopes

- 5.1.4 Micro Scissors

- 5.1.5 Micro Needle Holders

- 5.1.6 Micro Vessel Clamps

- 5.1.7 Other Instruments

- 5.2 By Microsurgery Type

- 5.2.1 Orthopedic

- 5.2.2 Ophthalmic

- 5.2.3 Plastic & Reconstructive

- 5.2.4 ENT

- 5.2.5 Neurological

- 5.2.6 Gynecological & Urological

- 5.2.7 Other Types

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Academic & Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 B. Braun SE

- 6.3.3 Baxter International Inc.

- 6.3.4 Beaver-Visitec International, Inc.

- 6.3.5 Danaher Corporation (Leica Microsystems)

- 6.3.6 Global Surgical Corporation

- 6.3.7 Haag-Streit Surgical

- 6.3.8 Integra LifeSciences

- 6.3.9 Johnson & Johnson Services, Inc. (Ethicon)

- 6.3.10 Karl Kaps GmbH

- 6.3.11 Karl Storz SE

- 6.3.12 KLS Martin Group

- 6.3.13 Leica Microsystems

- 6.3.14 Medical Microinstruments SpA

- 6.3.15 Medtronic plc

- 6.3.16 MicroSure BV

- 6.3.17 Microsurgery Instruments Inc.

- 6.3.18 Olympus Corporation

- 6.3.19 Scanlan International

- 6.3.20 Stille AB

- 6.3.21 Stryker Corporation

- 6.3.22 Teleflex Inc.

- 6.3.23 Virtuoso Surgical Inc.

- 6.3.24 ZEISS International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment