|

시장보고서

상품코드

2066560

냉각 통증 치료 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cold Pain Therapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

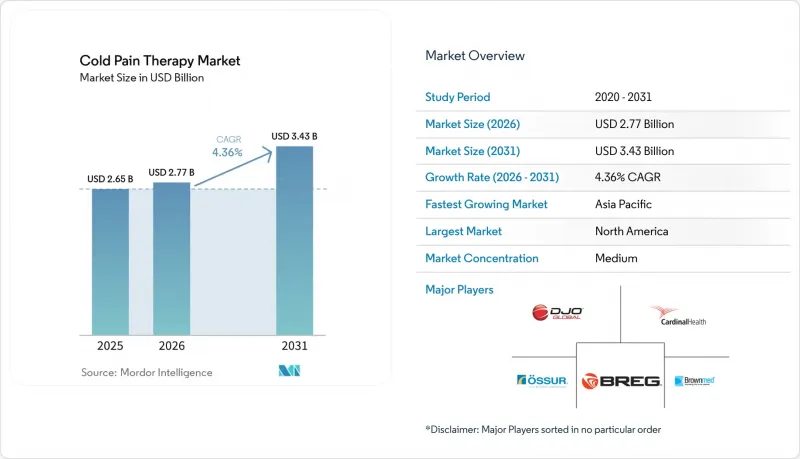

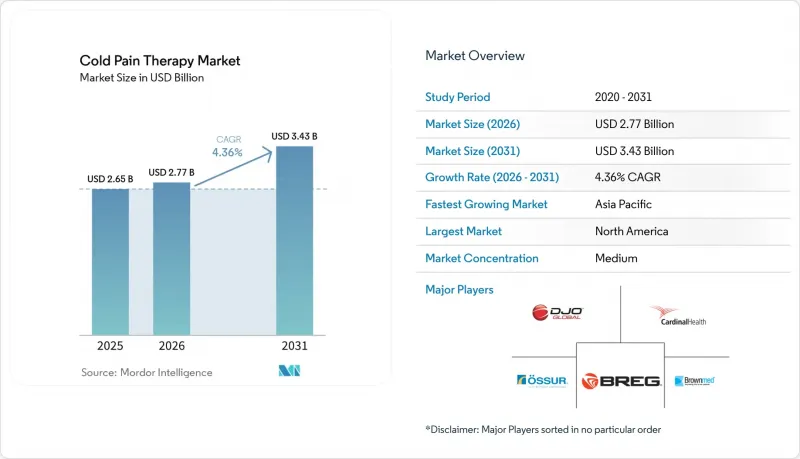

Mordor Intelligence에 의하면, 냉각 통증 치료 시장 규모는 2025년에 26억 5,000만 달러로 평가되었고 2026년 27억 7,000만 달러에서 2031년까지 34억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.36%를 나타낼 전망입니다.

본 보고서는 제품별(일반의약품 및 처방약), 용도별(스포츠 의학 등), 유통 채널별(소매 약국 및 드럭스토어 등), 연령대별(성인, 고령자, 소아), 지역별(북미, 유럽, 아시아태평양 등)로 분류되어 있습니다. 시장 세분화 및 전망은 금액(달러) 기준으로 표시되어 있습니다.

세계 냉각 통증 치료 시장 동향 및 인사이트

스포츠 및 교통사고로 인한 부상 발생률 증가

프로 리그 선수들과 아마추어 운동선수들은 현재, 체온을 신속하게 낮춤으로써 회복 효과가 향상된다는 연구 결과를 바탕으로, 휴대용 저온 요법 장치를 사용하여 급성 외상을 6시간 이내에 치료하고 있습니다. 스포츠 단체들은 현장에서의 냉각 요법을 의무화하고 있으며, 예산 사용처가 일회용 얼음에서 보충할 필요 없이 치료에 적합한 온도 범위를 유지할 수 있는 프로그래밍 가능한 기기로 전환되고 있습니다. 또한, 도시 지역의 교통 체증으로 인해 충돌 사고 발생률이 높아지고 있는 만큼, 소형 냉각 랩이 포함된 응급처치 키트 시장도 확대되고 있습니다. 그 결과, 냉각 통증 치료 시장은 신속하게 도입할 수 있는 솔루션을 통해 응급 의료 및 스포츠 경기장 등에서의 적용을 점점 더 확대되고 있습니다.

고령화 사회에서 관절염 및 기타 근골격계 질환(MSD)의 유병률 증가

지난 25년 동안 노동 연령층의 퇴행성 관절염 환자 수는 2배 이상 증가했으며, 만성 통증으로 인한 경제적 부담이 심화되고 있습니다. 고령 사용자들은 가볍고 착용하기 쉬우며, 설정 온도를 오랫동안 유지할 수 있는 랩형 기기를 선호하는 경향이 있습니다. 새롭게 등장한 크라이오뉴로리시스 기술은 대상 감각 신경을 냉각시켜 무릎 통증 완화를 도모하며, 전신 진통제를 사용하지 않고도 관절 가동 범위를 개선할 수 있게 해줍니다. 각 제조업체들은 이러한 장기적인 성장 요인을 포착하기 위해, 직관적인 조작이 가능한 고령자용 디자인을 선보이고 있습니다.

제3자에 의한 상환의 제한 또는 부재

미국 메디케어는 대부분의 냉각 장치를 ‘의학적으로 필요하지 않은’ 것으로 분류하고 있으며, 훌륭한 임상시험 데이터가 있음에도 불구하고 비용을 전액 환자에게 부담시키고 있습니다. 보험사는 결과에 편차가 있다는 점을 이유로 보험금 지급을 거부하고 있으며, 일부 지역 보험사는 전기식 시스템보다 더 간단한 얼음 냉각을 권장하는 정형외과학회의 견해를 근거로 삼고 있습니다. 그 때문에 병원에서는 구매를 제한하고 있어, 냉통요법 시장에서 고부가가치 기기의 도입이 지연되고 있습니다.

부문별 분석

2025년, OTC(일반의약품) 제품은 냉찜질 치료 시장의 64.60% 점유율을 차지했습니다. 이는 소비자들이 의료 감독 없이 구입할 수 있는 스프레이, 젤, 패치를 선호했기 때문입니다. 크림과 젤은 여전히 약국 진열대의 주력 상품으로 자리 잡고 있지만, 서방형 패치는 더 오래 지속되는 진통 효과를 선호하는 고객층을 확보하고 있습니다. 일반의약품(OTC) 분야의 냉찜질 치료 시장 규모는 꾸준히 성장할 것으로 예상되지만, 그 성장 속도는 기술적으로 고도의 전문성이 요구되는 처방전이 필요한 의료기기에 비해 완만합니다.

전동 순환 시스템을 필두로 하는 처방전 의료기기는 2031년까지 연평균 성장률(CAGR) 5.05%를 나타낼 것으로 전망됩니다. 병원에서는 정확한 온도 범위와 자동 정지 기능이 필요한 수술 후 프로토콜을 표준화하기 위해 이러한 플랫폼을 도입하고 있습니다. 소프트웨어와 연동되는 펌프는 사용 기록을 전자 차트에 전송하여, 의료진이 품질 지표 준수 여부를 확인하는 데 도움을 주고 있습니다. 그 결과, 냉통 요법 시장은 점점 더 양극화되고 있습니다. 대량 판매용 OTC 제품이 판매량을 주도하는 한편, 높은 이익률을 자랑하는 처방전용 기기는 성과 기반의 솔루션을 추구하는 의료기관의 예산을 확보하고 있습니다.

스포츠 의학 분야는 프로 리그에서 냉각 요법의 의무화 및 아마추어층의 참여 확대에 힘입어, 2025년 냉각 통증 요법 시장 매출의 37.95%를 차지했습니다. 무릎, 발목, 어깨에 착용할 수 있는 휴대용 슬리브 시스템은 현재 팀과 함께 이동하며, 사이드라인의 아이스 쿨러를 대체하고 있습니다. 한편, TRPM8에 대한 연구를 통해 복잡한 통증 기전에 대한 냉각 요법의 유효성이 입증됨에 따라, 신경병성 통증 및 만성 통증 사례가 연평균 성장률(CAGR) 5.12%로 증가하고 있습니다.

수술 후 관리는 여전히 중요하며, 부기를 줄이기 위해 교체 수술 후 냉찜질 처치를 병원 지침에 따라 의무화하고 있습니다. 외상·정형외과 분야에서는 고령화에 따라 골절 및 관절 복원 사례 수가 증가하고 있어, 내구성이 뛰어난 랩과 비전동식 냉찜질팩에 대한 수요가 높아지고 있습니다. 이러한 변화에 따라 급성 외상 관리부터 장기간에 걸친 만성 치료에 이르기까지 냉각 통증 요법의 도입이 확산되면서, 그 시장 범위는 스포츠 분야를 넘어 확대되고 있습니다.

지역별 분석

북미는 2025년, 높은 수준의 의료비 지출과 의료기기 신청에 관한 규제상의 불확실성을 해소한 FDA의 지침에 힘입어 냉각 통증 치료 시장의 39.95%를 차지했습니다. 미국은 처방전이 필요한 의료기기의 도입을 주도하고 있지만, 보험 급여 격차로 인해 병원에서의 도입이 저해되고 있습니다. 캐나다의 단일 지불자 모델은 의학적으로 필요한 냉각 시스템에 대해 보다 안정적인 자금을 지원하고 있는 반면, 멕시코에서는 확대되는 중산층이 OTC(일반의약품) 부문의 매출을 끌어올리고 있습니다.

유럽은 성숙한 유통망과 국경을 초월한 판매를 용이하게 하는 조화된 의료기기 규정(MDR)을 바탕으로 이에 뒤따르고 있습니다. 독일과 영국은 디지털 모니터링 플랫폼과 연동되는 커넥티드 랩의 도입을 선도하고 있으며, 이는 원격의료의 높은 보급률을 반영하고 있습니다. 남유럽 시장에서는 프로 축구와 사이클링 문화를 배경으로 스포츠 의학 분야가 확대되고 있으며, 유럽의약품청(EMA)의 디지털 헬스 관련 노력이 IoT 통합을 더욱 촉진하고 있습니다.

아시아태평양은 중국과 인도의 고령화, 그리고 일본과 한국의 높은 기술 수용성을 배경으로, 2031년까지 연평균 성장률(CAGR)이 5.30%에 달하며 가장 빠르게 성장하고 있는 지역입니다. 현지 투자자들은 지역 내 대형 전자상거래 업체를 통해 판매되는 합리적인 가격의 스마트 커프를 제조하는 스타트업 기업을 지원하고 있습니다. 호주는 스포츠 과학 분야의 전문 지식을 활용하여 차세대 냉각 웨어러블 기기의 임상시험 거점으로서의 역할을 수행하고 있습니다. 그러나 동남아시아 일부 지역에서는 보험 환급 체계가 제한적이어서 도입률이 잠재적 수준에 미치지 못하고 있으며, 이는 냉통요법 시장에서 교육 및 자금 조달 솔루션을 현지화하는 기업들에게 장기적인 성장 여지가 있음을 시사합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the cold pain therapy market size was valued at USD 2.65 billion in 2025 and estimated to grow from USD 2.77 billion in 2026 to reach USD 3.43 billion by 2031, at a CAGR of 4.36% during the forecast period (2026-2031).

This report is Segmented by Product (OTC Products and Prescription Products), Application (Sports Medicine and More), Distribution Channel (Retail Pharmacies & Drug Stores and More), Age Group (Adults, Geriatric, and Pediatric), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Global Cold Pain Therapy Market Trends and Insights

Rising Incidence of Sports & Road-Traffic Injuries

Professional leagues and amateur athletes now treat acute injuries within six hours using portable cryotherapy units because evidence shows that recovery outcomes improve when tissue temperature is lowered quickly. Sports bodies mandate on-site cold therapy, shifting budgets from disposable ice toward programmable devices that maintain therapeutic ranges without refills . Urban traffic congestion also raises collision rates, widening the market for first-response kits fitted with compact cooling wraps. As a result, the cold pain therapy market increasingly serves emergency care and sporting venues with quick-deployment solutions.

Growing Prevalence of Arthritis & Other MSDs in Ageing Population

During the last 25 years, osteoarthritis cases among working-age adults more than doubled, intensifying the economic burden of chronic pain. Elderly users gravitate toward wrap-around devices that are lightweight, easy to fasten and capable of maintaining set temperatures for extended periods . Emerging cryoneurolysis techniques offer knee-specific relief by cooling targeted sensory nerves, enabling mobility gains without systemic analgesics. Manufacturers position geriatric-friendly designs with intuitive controls to tap this long-term growth driver.

Limited or Absent Third-Party Reimbursement

US Medicare classifies most cooling devices as "not medically necessary," shifting full cost to patients despite favorable trial data. Insurers cite inconsistent outcomes to justify denials, while some regional payers rely on orthopedic society statements that favor simpler ice over motorized systems. Hospitals therefore limit purchases, slowing high-value device adoption in the cold pain therapy market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Consumer Shift Toward Self-Care & OTC Topical Analgesics

- Increase in Post-Surgical Procedures Requiring Cold Therapy

- Low Patient & Clinician Awareness in Emerging Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

OTC solutions controlled 64.60% of cold pain therapy market share in 2025 as consumers favored accessible sprays, gels and patches available without medical oversight. Creams and gels continue to anchor pharmacy aisles, while controlled-release patches win customers who prefer longer relief intervals. The cold pain therapy market size for OTC formats is projected to grow steadily but at a slower pace than technologically sophisticated prescription devices.

Prescription devices, led by motorized circulation systems, exhibit a 5.05% CAGR to 2031. Hospitals adopt these platforms to standardize postoperative protocols that demand precise temperature windows and automated shut-offs. Software-enabled pumps transmit usage logs to electronic health records, helping providers validate adherence for quality metrics. As a result, the cold pain therapy market increasingly bifurcates: mass-market OTC goods dominate volume, whereas high-margin prescription units capture institutional budgets seeking outcome-based solutions.

Sports medicine retained 37.95% of cold pain therapy market revenue in 2025, driven by mandatory cryotherapy access across professional leagues and expanding amateur participation. Portable sleeve systems that fit knees, ankles and shoulders now travel with teams, replacing ice coolers on the sidelines. However, neuropathic & chronic pain cases expand at a 5.12% CAGR as TRPM8 research validates cold modulation for complex pain mechanisms.

Post-operative therapy remains critical, with hospital protocols requiring cold application after replacement surgeries to curb swelling. In trauma & orthopedics, aging populations boost fracture and joint repair volumes, keeping demand high for durable wraps and non-motorized packs. These shifts spread adoption across acute injury management and long-duration chronic care, broadening the cold pain therapy market footprint beyond athletics.

Geography Analysis

North America held 39.95% of the cold pain therapy market in 2025, supported by high healthcare spending and FDA guidance that eliminates regulatory ambiguity for device submissions. The United States leads prescription device adoption, though reimbursement gaps temper hospital uptake. Canada's single-payer model provides steadier funding for medically necessary cooling systems, while Mexico's growing middle class boosts OTC category sales.

Europe follows with mature distribution networks and harmonized Medical Device Regulation that eases cross-border sales. Germany and the United Kingdom spearhead adoption of connected wraps that integrate with digital monitoring platforms, reflecting strong telehealth penetration. Southern European markets expand sports medicine segments due to professional football and cycling culture, while the European Medicines Agency's digital health initiatives encourage further IoT integration.

Asia-Pacific is the fastest-growing region with a 5.30% CAGR to 2031, driven by ageing populations in China and India and high technology acceptance in Japan and South Korea. Local investors back start-ups producing affordable smart cuffs marketed through regional e-commerce giants. Australia acts as a clinical-trial hub for next-generation cooling wearables, leveraging its sports-science expertise. However, limited reimbursement frameworks in parts of Southeast Asia keep adoption below potential, signaling long-run upside for companies that localize education and financing solutions in the cold pain therapy market.

- Breg

- Brownmed

- Cardinal Health

- Enovis Corp. (DJO Global)

- Ossur

- Performance Health

- Medline Industries

- IceWraps LLC

- Compass Health

- Hisamitsu Pharmaceutical Co.

- Romsons

- Unexo Life Sciences

- Sanofi

- Pfizer

- Johnson & Johnson (Chattanooga / Icy Hot)

- Solventum

- Zimmer MedizinSysteme

- BTL

- CoolSystems Inc. (Game Ready)

- CynoSure (Lutronic Cryo)

- Beiersdorf AG (Voltaren Emulgel)

- Metrum Cryoflex

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of sports & road-traffic injuries

- 4.2.2 Growing prevalence of arthritis & other MSDs in ageing population

- 4.2.3 Rapid consumer shift toward self-care & OTC topical analgesics

- 4.2.4 Increase in post-surgical procedures requiring cold therapy

- 4.2.5 IoT-enabled smart wearables offering real-time temperature control

- 4.2.6 Next-gen TRPM8-modulating cooling compounds in R&D pipeline

- 4.3 Market Restraints

- 4.3.1 Limited or absent third-party reimbursement

- 4.3.2 Low patient & clinician awareness in emerging economies

- 4.3.3 Dermatologic adverse events triggering tighter formulation rules

- 4.3.4 Substitution threat from laser, contrast & heat-alternation therapies

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 OTC Products

- 5.1.1.1 Creams

- 5.1.1.2 Gels

- 5.1.1.3 Patches

- 5.1.1.4 Sprays & Roll-ons

- 5.1.1.5 Wraps & Pack Systems

- 5.1.1.6 Other OTC Products

- 5.1.2 Prescription Products

- 5.1.2.1 Motorized Devices

- 5.1.2.2 Non-motorized Devices

- 5.1.1 OTC Products

- 5.2 By Application

- 5.2.1 Sports Medicine

- 5.2.2 Post-operative Therapies

- 5.2.3 Trauma & Orthopaedics

- 5.2.4 Neuropathic & Chronic Pain

- 5.2.5 Other Applications

- 5.3 By Distribution Channel

- 5.3.1 Retail Pharmacies & Drug Stores

- 5.3.2 Hospital Pharmacies

- 5.3.3 E-commerce

- 5.3.4 Sports & Specialty Stores

- 5.4 By Age Group

- 5.4.1 Adults

- 5.4.2 Geriatric

- 5.4.3 Pediatric

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Middle East

- 5.5.4.2 GCC

- 5.5.4.3 South Africa

- 5.5.4.4 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Breg Inc.

- 6.3.2 Brownmed Inc.

- 6.3.3 Cardinal Health Inc.

- 6.3.4 Enovis Corp. (DJO Global)

- 6.3.5 Ossur hf

- 6.3.6 Performance Health

- 6.3.7 Medline Industries LP

- 6.3.8 IceWraps LLC

- 6.3.9 Compass Health Brands

- 6.3.10 Hisamitsu Pharmaceutical Co.

- 6.3.11 Romsons

- 6.3.12 Unexo Life Sciences

- 6.3.13 Sanofi SA

- 6.3.14 Pfizer Inc.

- 6.3.15 Johnson & Johnson (Chattanooga / Icy Hot)

- 6.3.16 Solventum

- 6.3.17 Zimmer MedizinSysteme

- 6.3.18 BTL Industries

- 6.3.19 CoolSystems Inc. (Game Ready)

- 6.3.20 CynoSure (Lutronic Cryo)

- 6.3.21 Beiersdorf AG (Voltaren Emulgel)

- 6.3.22 Metrum Cryoflex

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment