|

시장보고서

상품코드

2066572

의료용 포장 필름 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Medical Packaging Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

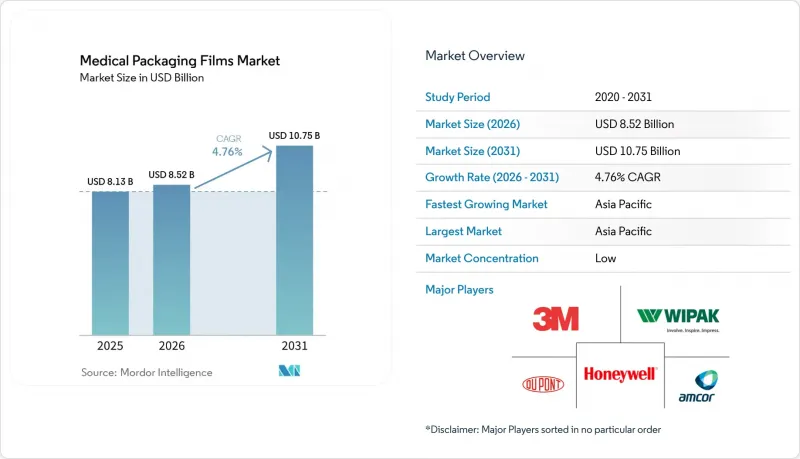

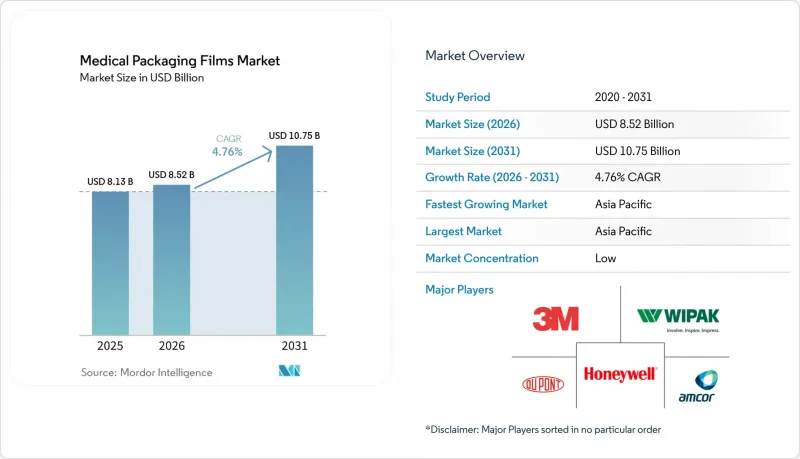

Mordor Intelligence에 의하면, 의료용 포장 필름 시장 규모는 2025년 81억 3,000만 달러에서 2026년에는 85억 2,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 4.76%로 성장을 지속하여, 2031년에는 107억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 소재 유형(플라스틱 필름, 금속 및 알루미늄 필름), 제품 유형(열성형 가능 필름, 고차단성 필름 등), 용도(가방·파우치, 블리스터 팩 등), 최종 사용자(제약 제조업체, 의료기기 제조업체 등), 기술(블로우 필름 압출 성형 등), 지역(북미, 유럽, 아시아태평양 등)

세계 의료용 포장 필름 시장 동향 및 인사이트

만성 질환 유병률 증가

비감염성 질환의 발생률이 증가함에 따라, 포장은 단순한 수동적인 용기에서 능동적인 복약 순응도를 돕는 도구로 변모하고 있습니다. 당뇨병 임상시험에서 달력형 블리스터 포장은 표준 포장에 비해 HbA1c 수치를 0.95% 낮추었으며, 이는 해당 포장의 임상적 가치를 입증하고 있습니다. 고령화가 진행됨에 따라 다제 병용이 증가하고 있으며, 제약사들은 e-헬스 플랫폼이나 스마트 복약 알림 기능과 연동되는 1회 투여 방식의 도입을 요구받고 있습니다. 규제 당국은 현재 라벨 표시와 포장 구성을 안전한 사용에 필수적인 요소로 간주하고 있으며, 이는 FDA 지침의 잇따른 개정에도 반영되어 있습니다. 그 결과, 환자 중심의 설계를 인증받을 수 있는 필름 공급업체는 의료용 포장 필름 시장 전체에서 장기적인 수요를 확보하고 있습니다.

바이오플라스틱 및 재활용 소재를 통한 지속가능성 추구

재활용 소재의 최소 함유율을 의무화하는 EU 지침에 따라 바이오 폴리머의 도입이 가속화되고 있습니다. Avient사의 바이오 제품 시리즈인 ‘Mevopur’는 ISO 10993 규격을 준수하면서도 탄소 발자국을 25% 줄여줍니다. Amcor사의 ‘SureForm Pro ICE’는 플라스틱 사용량을 전체적으로 40% 줄이면서도, 기존의 병원 폐기물 흐름에서 요구되는 드롭인 재활용 기준을 충족합니다. 문제는 멸균에 대한 내성입니다. 오토클레이브나 감마선 멸균 공정은 퇴비화 가능한 수지를 열화시킬 가능성이 있으므로, 차단 성능을 유지하는 PLA, PHA, EVOH의 합금 배합이 요구되고 있습니다. 미국의 의료 시스템 조달 팀은 현재 입찰 과정에서 환경 친화성을 평가 기준으로 반영하고 있으며, 이에 따라 지속 가능한 소재 분야의 선구자들은 의료용 포장 필름 시장에서 가격 면에서 우위를 점하고 있습니다.

석유 유래 폴리머 가격 변동

2024년, 에너지 가격의 급등에 따라 수지 원가가 파운드당 3-5센트 상승하면서, 의료용 등급 공급 계약에 묶여 있는 가공업체들의 이익률이 압박을 받았습니다. 헤지 여지가 없는 중소기업들은 최대 6개월에 달하는 비용 전가 지연에 직면해 있으며, 고객 이탈이나 생산 라인 중단 위험에 노출되어 있습니다. 의료 분야의 엄격한 변경 관리 규정이 수지의 신속한 대체를 방해하고 있어, 일반 포장 분야에 비해 위험이 커지고 있습니다. 대기업들은 선물 구매나 크래커 복합 시설 근처에 압출 성형 설비를 함께 설치하는 방식으로 대응하고 있지만, 이러한 자본 집약적인 노력이 의료용 포장 필름 시장의 경쟁 격차를 더욱 벌리고 있습니다.

부문별 분석

2025년 기준으로 플라스틱 필름은 84.72%의 점유율을 유지하고 있으며, 이 부문 내에서의 바이오 소재로의 전환이 연평균 성장률(CAGR) 7.12%를 견인하고 있습니다. 밀봉성과 감마선 조사에 대한 안정성으로 높이 평가받는 폴리에틸렌 등급은 대량 생산되는 의약품용 파우치의 기반이 되고 있습니다. EVOH 라이닝이 적용된 공압출 필름은 안구건조증스로 운송되는 생물학적 제제용 바이알에 필요한 산소 차단성 기준을 충족합니다. 이러한 구성 속에서 PLA/PHA 블렌드는 폐기물 발자국을 40% 줄이는 것을 목표로 하는 한 병원에서 시범 규모의 주문을 수주했습니다. 금속 박막은 경피 흡수 패치의 라이너 등, 산소 투과율(OTR)이 0.05 cc/m²/일 미만이어야 하는 특정 틈새 시장을 차지하고 있습니다. 또한, 의료용 포장 필름 업계의 각 기업은 다층 필름의 잔여물이 박리되지 않고 기계적 재활용 과정에 투입될 수 있도록, 상용화제의 화학 기술에 대한 투자를 확대되고 있습니다.

향후 발전을 위해서는 병원용 멸균제에 대한 열수분해 경로의 검증과 EN 13432 퇴비화 기준 준수 여부가 핵심이 될 것입니다. ‘크래들 투 크래들(C2C)’ 인증을 추진하는 공급업체는 조달 과정에서 우선적으로 선정되는 경향이 있지만, 그럼에도 불구하고 인장 강도의 저하 없이 121°C의 증기 멸균 및 60 kGy의 전자선 조사 주기를 통과해야 합니다. 그 결과, 의료용 포장 필름 시장의 다음 흐름은 기존의 수지와 바이오 유래 층을 융합한 하이브리드 구조에서 비롯될 가능성이 높으며, 가공성과 사용 후 폐기 편의성 간의 균형을 잘 맞춘 형태가 될 것으로 보입니다.

현재 매출의 24.55%를 차지하는 고차단 필름은 2031년까지 연평균 성장률(CAGR) 8.33%로 확대되며, 의료용 포장 필름 시장 전체를 상회하는 성장을 보일 것으로 전망됩니다. 이러한 수요는 산소 투과율을 0.1 cc/m²/일 미만으로 억제해야 하는 단일클론 항체의 보급과 밀접한 관련이 있습니다. TekniPlex사의 클린룸에서 제조된 7층 블로우 성형 구조는 EVOH와 고리형 올레핀 폴리머를 결합하여 콜드체인의 안정성을 72시간에서 120시간으로 연장합니다. 공압출 및 라미네이트 필름은 IV 백에서 진단용 파우치에 이르기까지 폭넓은 용도에 대응할 수 있는 범용성 덕분에 2025년 기준 43.05%의 시장 점유율을 차지하며, 여전히 판매량의 주류를 이루고 있습니다. 그럼에도 불구하고, 수증기 차단 성능 향상에 따른 가격 프리미엄은 매우 높은 수익성을 가져다주고 있어, 기존 제조업체들은 초박형 EVOH를 배치하기 위한 버블 케이지 시스템을 도입해 생산 라인을 개조하는 움직임을 가속화하고 있습니다.

또한, 공압출 제조업체들은 NFC 회로와 열변색 잉크를 통합하여 물리적 차단 기능과 디지털 인증 기능을 융합하고 있습니다. 앞으로 무균 충전 및 마무리 라인이 증기 멸균에서 기화 플라즈마 멸균으로 전환됨에 따라, 과산화수소 내성 코팅이 필수적일 것입니다.

지역별 분석

아시아태평양은 2025년에 매출 점유율 38.21%를 차지해, 2031년까지의 연평균 성장률(CAGR)도 6.11%로 최고 수준을 기록하며 의료용 포장 필름 시장을 주도하고 있습니다. 중국의 바이오의약품 생산 확대와 인도의 제네릭 의약품 보급 확대로 인해, 고차단성 리드 필름 및 열성형용 웹에 대한 수요가 증가하고 있습니다. 인도의 ‘생산 연계형 인센티브(PLI)’ 제도 등 정부의 우대 조치에 따라 제약 관련 포장 공장에 대한 설비 투자액의 최대 5%가 환급되므로, 구자라트주와 텔랑가나주에 새로운 생산 능력이 집중되고 있습니다. 필리핀의 FDA 인증 에코존은 필름 가공업체들이 동일한 거점에 집적함으로써 물류 비용을 대폭 절감하고 검증 주기를 단축하는 지역적인 모범 사례가 되고 있습니다. 일본에서는 초고청정실에서의 압출 성형에 대한 프리미엄 수요가 지속되고 있는 반면, 한국에서는 CDMO의 급속한 성장에 힘입어 양산형 파우치 라미네이트에 대한 안정적인 수주가 증가하고 있습니다.

북미는 DSCSA(의약품 안전 추적법)의 시행에 따라 2024년 11월까지 범용 일련번호 제도가 추진될 예정이므로, 여전히 매우 중요한 지역입니다. 해당 지역에서 바이오의약품의 비중이 높아지면서 콜드체인용 파우치 도입이 가속화되고 있으며, 특히 암콜과 베리의 통합 이후 미국과 멕시코 국경 일대에 11곳의 압출 성형 거점이 집중되어 있습니다. ‘지속 가능한 조달’을 가속화하는 병원에서는 PCR(소비 후 재활용) 소재가 혼합된 PE/PP 단일 소재를 선호하며, 이는 컨버터의 연구 개발 우선순위를 결정짓고 있습니다. 2027년에 도입될 예정인 캐나다의 전국 의약품 보험 제도는 만성 질환 치료에 대한 접근성을 확대할 것으로 예상되며, 간접적으로 블리스터 포장 수요를 증가시켜 의료용 포장 필름 시장의 성장세를 뒷받침할 것으로 전망됩니다.

유럽은 성숙한 시장이지만, 세계에서 가장 엄격한 에코디자인 규제를 시행하고 있습니다. 규제 당국이 염소계 기질을 엄격히 심사하는 가운데, 독일은 PVdC를 포함하지 않는 배리어 필름 분야의 고부가가치 수주 중심지로 자리 잡고 있습니다. 프랑스의 2025년 ‘확대 생산자 책임(EPR)’ 개정법은 재활용이 불가능한 형태에 대해 단계적으로 요금을 인상하도록 의무화하고 있으며, 단일 소재인 EVOH-PE로의 전환을 촉진하고 있습니다. 영국의 브렉시트 이후 MHRA(의약품 및 의료기기 규제청)가 적용하는 일련번호 부여 기준의 차이로 인해, EU와 영국 양쪽의 유통 경로를 모두 지원하는 포장에는 이중 코딩이 필요하게 되어 생산 라인의 구성이 복잡해지고 있습니다. 남유럽에서는 북유럽의 대형 제약사들에 의한 니어쇼어 아웃소싱이 활발히 이루어지고 있으며, 스페인의 블리스터 포장 공장에서는 2025년에 출하량이 5.4% 증가했습니다.

라틴아메리카에서는 브라질의 ANVISA가 2026년까지의 완전한 통합을 목표로 하는 RDC 680을 최종 확정함에 따라, 아직 초기 단계이긴 하지만 요구 사항이 급속히 강화되는 추세를 보이고 있습니다. 다국적 CDMO 기업들은 USMCA에 따른 미국 수요에 대응하기 위해 멕시코에 투자하고 있으며, 비용 절감과 니어쇼어링을 통한 사업 연속성을 동시에 확보하고자 하고 있습니다. 걸프협력회의(GCC)는 ‘비전 2030’에 따라 생물학적 제제의 충전 및 마무리 시설 현대화를 추진하고 있으며, 지역 내 압출 성형 능력이 확대될 때까지 고차단 필름의 수입을 단계적으로 늘리고 있습니다. 이러한 동향들이 복합적으로 작용함에 따라, 의료용 포장 필름 시장에서 사양의 미묘한 차이를 결정짓는 요인으로서 지역의 중요성이 확고해지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the medical packaging films market size is expected to grow from USD 8.13 billion in 2025 to USD 8.52 billion in 2026 and is forecast to reach USD 10.75 billion by 2031 at 4.76% CAGR over 2026-2031.

This report is Segmented by Material Type ( Plastic Films and Metallic and Aluminum Films), Product Type (Thermoformable Films, High-Barrier Films, and More), Application (Bags and Pouches, Blister Packs, and More), End-User (Pharmaceutical Manufacturing, Medical Device Manufacturers, and More), Technology(blown Film Extrusion, and More) and Geography (North America, Europe, Asia-Pacific, and More)

Global Medical Packaging Films Market Trends and Insights

Rising Prevalence of Chronic Diseases

Growing noncommunicable disease incidence is transforming packaging from passive containment into active adherence tools. Calendar blister designs lowered HbA1c by 0.95% versus standard packs in diabetes trials, underscoring packaging's clinical value. Aging demographics intensify polypharmacy, pushing drug makers to adopt unit-dose formats that synchronize with e-health platforms and smart pill reminders. Regulators now treat labeling and package configuration as integral to safe use, as reflected in successive FDA guidance updates. Consequently, film suppliers capable of certifying patient-centric designs secure long-term demand across the medical packaging films market.

Sustainability Push for Bioplastics and Recyclables

EU directives mandating minimum recycled content are accelerating biopolymer uptake. Avient's Mevopur bio-based series cuts carbon footprints by 25% while maintaining ISO 10993 compliance. Amcor's SureForm Pro ICE reduced overall plastic by 40% yet met drop-in recyclability thresholds across existing hospital streams. The challenge is sterilization resilience: autoclave and gamma cycles can degrade compostable resins, prompting alloyed formulations of PLA, PHA, and EVOH that preserve barrier integrity. Procurement teams in US health systems now assign environmental weighting in tenders, giving early movers in sustainable substrates a pricing premium within the medical packaging films market.

Volatile Petroleum-Based Polymer Prices

Resin costs climbed 3-5 cents per pound in 2024 amid energy spikes, compressing margins for converters locked into medical-grade supply contracts. Smaller firms, lacking hedging leverage, face pass-through lags of up to six months, risking account attrition or line shutdowns. Strict change-control rules in healthcare impede rapid resin substitution, amplifying exposure versus general packaging segments. Larger players respond by forward-buying and co-locating extrusion near cracker complexes, yet this capital intensity widens the competitive gap in the medical packaging films market.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Manufacturing Expansion in Asia-Pacific

- Surge in Home-Based Care and POC Diagnostic Kits

- High Regulatory Validation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic films retained 84.72% share in 2025, and their internal shift toward bio-derivatives is propelling a 7.12% CAGR. Polyethylene grades, valued for sealability and gamma stability, underpin high-volume pharma pouches. EVOH-lined co-extrusions meet oxygen barrier thresholds for biologic vials shipped on dry ice. Within this mix, PLA/PHA blends are capturing pilot-scale orders from hospitals that target a 40% waste-footprint reduction. Metallic foils hold isolated niches where sub-0.05 cc/m2/day OTR is non-negotiable, such as transdermal patch liners. Additionallyy, medical packaging films industry participants invest in compatibilizer chemistries so multilayer off-cuts enter mechanical recycling without delaminating.

Further gains hinge on validating hot-water disintegration paths for hospital sterilants and aligning with EN 13432 compostability standards. Suppliers promoting cradle-to-cradle certifications gain procurement preference, though they must still pass 121 °C steam sterilization and 60 kGy e-beam cycles without tensile loss. Consequently, the next wave of the medical packaging films market will likely derive from hybrid structures that fuse conventional resins with bio-derived tie layers, balancing processability with end-of-life compliance.

High-barrier films, currently 24.55% of revenue, will expand at 8.33% CAGR through 2031, outpacing the broader medical packaging films market. Demand tracks the proliferation of monoclonal antibodies that mandate oxygen transmission rates below 0.1 cc/m2/day. TekniPlex's cleanroom-produced, seven-layer blown structures integrate EVOH and cyclic olefin polymers, extending cold-chain stability from 72 hours to 120 hours. Co-extruded and laminated films remain the volume backbone, controlling 43.05% share in 2025 thanks to format versatility that spans IV bags to diagnostic pouching. Nevertheless, price premiums for vapor-barrier upgrades yield outsized profitability, encouraging incumbents to retrofit lines with bubble-cage systems for ultra-thin EVOH placement.

Co-extruders also embed NFC circuits and thermochromic inks, merging a physical barrier with digital authentication. Looking forward, hydrogen-peroxide-resistant coatings will be essential as aseptic fill-finish lines pivot from steam to vaporized-plasma sterilants.

Geography Analysis

Asia-Pacific dominates the medical packaging films market with 38.21% revenue share in 2025 and the highest 6.11% CAGR to 2031. China's biologics build-out and India's generics push intensify demand for high-barrier lidding and thermoform webs. Government incentives such as India's Production Linked Incentive scheme reimburse up to 5% of capital outlays on pharma-adjacent packaging plants, tilting fresh capacity toward Gujarat and Telangana. The Philippines' FDA-certified ecozone illustrates a regional blueprint where co-located film converters slash logistics costs and expedite validation cycles. Japan sustains premium demand for ultra-cleanroom extrusion, while South Korea's CDMO boom adds steady orders for serialized pouch laminate.

North America remains pivotal as DSCSA enforcement pushes universal serialization by November 2024. The region's biologics weightings lift cold-chain pouch uptake, especially post-Amcor-Berry consolidation that clusters 11 extrusion sites across the US-Mexico border. Hospitals accelerating "sustainable purchasing" prefer PCR-infused PE/PP mono-materials, shaping converter R&D priorities. Canada's national pharmacare plan, slated for 2027, is projected to widen access to chronic therapies, indirectly escalating blister demand and reinforcing the medical packaging films market trajectory.

Europe, although mature, enforces the world's strictest eco-design statutes. Germany anchors high-value orders for PVdC-free barrier films, as regulators scrutinize chlorine-based substrates. France's 2025 Extended Producer Responsibility amendment imposes escalating fees on unrecyclable formats, prompting a pivot to mono-material EVOH-PE. The UK's post-Brexit MHRA serialization divergence necessitates dual coding on packs servicing both EU and UK channels, complicating line configurations. Southern Europe enjoys near-shore outsourcing from Northern pharma giants; Spanish blistering plants recorded 5.4% shipment gains in 2025.

Latin America shows nascent but fast-rising requirements as Brazil's ANVISA finalizes RDC 680 for full aggregation by 2026. Multinational CDMOs invest in Mexico to service US demand under USMCA, blending cost savings with near-shoring resilience. The Gulf Cooperation Council is modernizing biologics fill-finish halls under Vision 2030, adding incremental high-barrier film imports until regional extrusion capacity scales. Collectively, these developments cement geography as a determinant of specification nuance across the medical packaging films market.

- Amcor Plc

- DuPont de Nemours Inc.

- 3M Company

- Honeywell International Inc.

- Klockner Pentaplast Group

- Wipak Oy

- Renolit Medical

- PolyCine GmbH

- Glenroy Inc.

- Toray Industries Inc.

- Dunmore Corporation

- Covestro AG

- Sealed Air Corporation

- Constantia Flexibles Group

- Tekni-Plex Inc.

- Mondi Group

- UFlex Ltd.

- Coveris Holding

- Aptar Group Inc.

- West Pharmaceutical Services

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of chronic diseases

- 4.2.2 Sustainability push for bioplastics and recyclables

- 4.2.3 Pharmaceutical manufacturing expansion in APAC

- 4.2.4 Surge in home-based care and POC diagnostic kits

- 4.2.5 Digital serialization and smart anti-counterfeit films

- 4.2.6 Growth of 3D-printed personalized drug devices

- 4.3 Market Restraints

- 4.3.1 Volatile petroleum-based polymer prices

- 4.3.2 High regulatory validation costs

- 4.3.3 Competition from paper-based sterile packs

- 4.3.4 Weak recycling infra for multi-layer films

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Plastic Films

- 5.1.1.1 Polyethylene (LDPE, HDPE, LLDPE)

- 5.1.1.2 Polypropylene

- 5.1.1.3 Polyvinyl Chloride

- 5.1.1.4 Polycarbonate

- 5.1.1.5 Polyethylene Terephthalate

- 5.1.1.6 Polyamide

- 5.1.1.7 Ethylene Vinyl Alcohol Copolymer (EVOH)

- 5.1.1.8 Bioplastics

- 5.1.2 Metallic and Aluminum Films

- 5.1.1 Plastic Films

- 5.2 By Product Type

- 5.2.1 Thermoformable Films

- 5.2.2 Breathable and Porous Films

- 5.2.3 High-Barrier Films

- 5.2.4 Co-extruded and Laminated Films

- 5.3 By Application

- 5.3.1 Bags and Pouches

- 5.3.2 Blister Packs

- 5.3.3 Tubes and Form-Fill-Seal

- 5.3.4 Lidding and Sachets/Stick Packs

- 5.3.5 Diagnostic Strip and Pouch Laminates

- 5.4 By End-user

- 5.4.1 Pharmaceutical Manufacturing

- 5.4.2 Medical Device Manufacturers

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Hospitals and Clinics

- 5.4.5 Home Healthcare Kit Assemblers

- 5.5 By Technology

- 5.5.1 Blown Film Extrusion

- 5.5.2 Cast Film Extrusion

- 5.5.3 Solvent / Extrusion Coating

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Russia

- 5.6.2.7 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 GCC

- 5.6.4.1.2 Turkey

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Amcor Plc

- 6.4.2 DuPont de Nemours Inc.

- 6.4.3 3M Company

- 6.4.4 Honeywell International Inc.

- 6.4.5 Klockner Pentaplast Group

- 6.4.6 Wipak Oy

- 6.4.7 Renolit Medical

- 6.4.8 PolyCine GmbH

- 6.4.9 Glenroy Inc.

- 6.4.10 Toray Industries Inc.

- 6.4.11 Dunmore Corporation

- 6.4.12 Covestro AG

- 6.4.13 Sealed Air Corporation

- 6.4.14 Constantia Flexibles Group

- 6.4.15 Tekni-Plex Inc.

- 6.4.16 Mondi Group

- 6.4.17 UFlex Ltd.

- 6.4.18 Coveris Holding

- 6.4.19 Aptar Group Inc.

- 6.4.20 West Pharmaceutical Services

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment