|

시장보고서

상품코드

2066604

디지털 경험 플랫폼 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Digital Experience Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

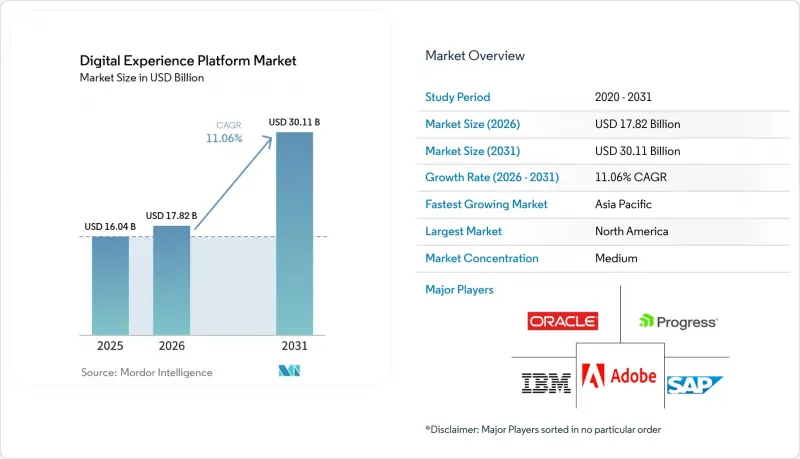

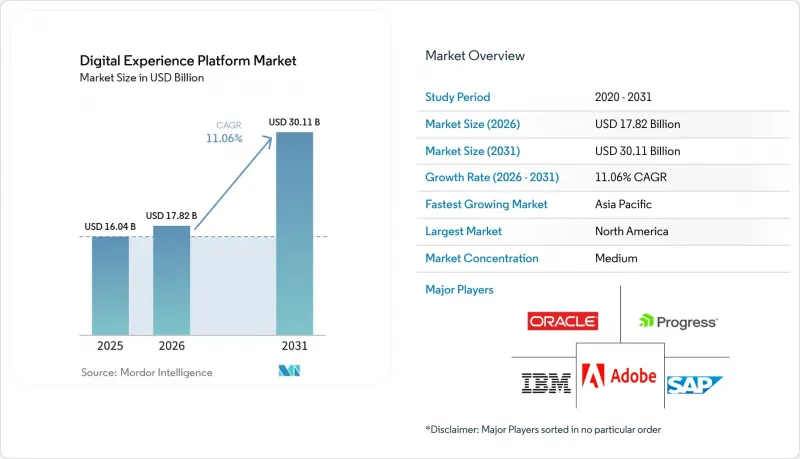

Mordor Intelligence에 의하면, 디지털 경험 플랫폼 시장 규모는 2026년에 178억 2,000만 달러에 이르고, 2031년까지 301억 1,000만 달러까지 확대한다고 예측되고 있어 예측 기간중은 CAGR 11.06%로 성장할 전망입니다.

본 보고서는 구성 요소(플랫폼 및 서비스), 도입 형태(On-Premise 및 클라우드), 최종 사용 산업(소매 및 전자상거래, IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어, 제조, 기타 최종 사용 산업), 조직 규모(대기업 및 중소기업), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

전 세계 디지털 경험 플랫폼 시장 동향 및 인사이트

‘클라우드 퍼스트’ 기업 IT 전략이 DXP 도입을 가속화

각 조직은 On-Premise 라이선스를 컴퓨팅, 스토리지, 컨텐츠 전송 대역폭이 묶인 SaaS(Software-as-a-Service) 모델로 지속적으로 전환하고 있으며, 이를 통해 5년 동안 총 소유 비용(TCO)을 최대 40% 절감하고 있습니다. 또한, 클라우드 플랫폼은 지속적인 배포를 가능하게 하여, 팀이 유지보수 시간을 기다릴 필요 없이 하루에 여러 번 코드 업데이트를 배포할 수 있게 됩니다. Microsoft Azure와 Amazon Web Services는 원클릭으로 이용할 수 있는 마켓플레이스를 제공하여, 개념 검증(PoC) 주기를 몇 개월에서 몇 주로 단축하고 있습니다. 멀티 클라우드 지원 덕분에 벤더 종속성에 대한 우려가 더욱 완화되고 데이터 주권 요건도 충족됨에 따라, 대기업들은 미션 크리티컬 워크로드의 이전을 가속화하고 있습니다.

옴니채널 및 AI 주도형 개인화로의 급속한 전환

현재 소비자들은 구매 전에 6-8개의 접점을 통해 브랜드와 상호작용하고 있으며, 이로 인해 정체성, 행동, 실시간 맥락을 통합하는 플랫폼에 대한 수요가 발생하고 있습니다. 2025년 매출을 주도한 것은 소매 및 전자상거래 분야였습니다. 이는 사업자가 밀리초 단위로 관련 상품을 제안하는 추천 엔진을 도입했기 때문입니다. 어도비는 Firefly의 생성 모델을 통합하여 29개 언어로 된 상품 설명문을 자동으로 생성할 수 있게 되었습니다. 이를 통해 캠페인 반복 주기를 단축하고, 전환율 향상을 도모하고 있습니다. BFSI(은행 및 금융 및 보험) 기관들은 오픈 뱅킹 API를 활용하여 잔액 통합 및 맞춤형 대출 제안을 제공함으로써, 고객 확보 비용 절감과 전환 주기 단축을 실현하고 있습니다.

레거시 스택에 따른 통합의 복잡성

대기업에서는 독자적인 사양의 API나 배치 처리에 기반한 통합에 의존하는 15-20개의 마케팅 및 상거래 용도를 운영하고 있습니다. 구성 가능한 DXP로 플랫폼을 전환하려면 데이터 스키마 매핑, 중복 레코드 조정, 트랜잭션 일관성 확보가 필요하며, 이로 인해 프로젝트 기간이 18개월에 달하거나 예산의 40%를 소모하는 경우가 종종 있습니다. 금융 기관들은 막대한 현대화 투자 없이는 메인프레임 기반 핵심 시스템에서 RESTful API를 공개할 수 없기 때문에 또 다른 과제에 직면해 있습니다. 기성 커넥터는 일반적인 이용 사례를 포괄하고 있지만, 맞춤형 워크플로우나 규정 준수 요건을 충족하기 위해서는 여전히 수작업으로 코딩된 미들웨어가 필요하며, 이로 인해 전문 시스템 통합 업체에 대한 수요가 증가하고 있습니다.

부문별 분석

서비스 부문은 2025년 매출의 31.27%를 차지하며 연평균 성장률(CAGR) 12.34%로 성장을 지속하고, 있어, 구성 요소 그룹 중 가장 빠른 성장세를 보이고 있습니다. 이러한 성장 추세는 기업들이 디지털 경험 플랫폼(DXP) 시장 예산의 40-50%를 시스템 통합, 관리형 운영 및 전략적 컨설팅에 할당하고 있기 때문인 것으로 분석됩니다. 이 플랫폼은 2025년에도 정기 구독, 컨텐츠 배포 기능 및 API 호출에 대한 과금을 통해 매출의 68.73%를 창출했습니다. 그러나 컴포저블 스택으로의 전환에 따라 타사와의 접점이 두 배로 늘어나면서, 크로스 플랫폼 노하우를 갖춘 통합 업체에 대한 수요가 높아지고 있습니다. 전 세계 컨설팅 기업들은 헤드리스 컨텐츠 관리, 고객 데이터 플랫폼, 마케팅 자동화 분야의 전문가를 채용함으로써 DXP(디지털 경험 플랫폼) 사업을 확대했습니다. 현재 교육 프로그램에서는 마케팅 팀을 대상으로 로우코드 개발, API 관리, 실험 기법을 지도하고 있으며, 과거에는 기술 부서에 한정되었던 업무가 점차 일반화되고 있습니다. 또한, 클라이언트가 브랜드 및 규제 요건을 준수하기 위해 프롬프트와 가드레일을 미세 조정하는 과정에서 이 서비스에는 생성형 AI 모듈의 지속적인 최적화도 포함되어 있습니다.

라이선스 수익은 여전히 필수적이지만, 사용량에 따른 과금 모델로의 꾸준한 전환이 수익 포트폴리오의 재구성을 이끌어내고 있습니다. 각 벤더사는 현재 세심한 도입 지원, 성능 튜닝, 지속적인 실험을 프리미엄 플랜으로 묶어, 높은 수익률을 자랑하는 지속적인 수익원을 육성하고 있습니다. 동시에, 매니지드 서비스는 연중무휴 24시간 사이트의 안정성을 확보하고 최적화함으로써 인력 부족 문제를 해결하며, 고객이 인프라 유지보수 대신 컨텐츠 및 상거래 전략에 집중할 수 있도록 지원합니다. 이러한 추세에 따라, 이 서비스는 시장에서 지속적인 지갑 점유율을 확보하기 위한 주요 수단으로서의 입지를 확고히 하고 있습니다.

클라우드 부문은 2025년에 매출의 57.83%를 차지해, 연간 13.11%의 성장률을 기록하며 On-Premise 구축을 크게 앞지르고 있습니다. 탄력적인 확장성, 사용량 기반 과금 방식, 자동화된 보안 패치 적용은 예측 가능한 비용과 신속한 실험을 추구하는 조직에게 매력적입니다. 보안에 민감한 업계조차도 기밀 데이터를 On-Premise에 보관하면서 컨텐츠 배포 및 분석 작업을 퍼블릭 클라우드로 이전하는 하이브리드 프레임워크를 시범 운영하고 있으며, 규정 준수 및 민첩성 간의 균형을 맞추고 있습니다. Oracle의 멀티클라우드 지원은 워크로드 이식성에 대한 수요가 증가하고 있음을 보여주며, 기업들은 주권 관련 규정을 준수하면서도 공급업체 간에 유리한 조건을 협상할 수 있게 되었습니다.

컨테이너 오케스트레이션 및 인프라스트럭처 애즈 코드(Infrastructure as Code)를 통해 구현되는 지속적 통합(CI) 파이프라인 덕분에 하루에 여러 번 코드를 푸시할 수 있게 되었으며, 이를 통해 실시간 재고 동기화 및 AI를 활용한 개인화가 지원되고 있습니다. 그러나 타사의 가동 시간에 의존하고 있기 때문에 서비스 수준 위반의 위험에 노출되어 있습니다. 기업들은 다중 리전에서의 장애 전환, API 사용량 제한 모니터링, 그리고 가동 중단에 대한 계약상 위약금을 통해 위험을 완화하고 있습니다. 도구의 성숙도에 따라 하이브리드 모델 시장 점유율은 점차 확대될 것으로 예상되지만, 퍼블릭 클라우드는 계속해서 시장의 성장 동력으로 남을 것입니다.

지역별 분석

북미는 2025년 매출의 38.73%를 차지하며, 그 원동력은 포춘 500대 기업이 엔터프라이즈급 거버넌스, SOC 2 Type II 및 ISO 27001 인증, 멀티테넌트 아키텍처에 투자하는 지출입니다. 14개 주에 걸쳐 분산되어 있는 미국의 개인정보 보호 관련 법규는 지역별 동의 획득 및 데이터 보존 정책 수립을 의무화하고 있으며, 이로 인해 소규모 공급업체의 진입 장벽은 낮아지는 반면, 규정 준수 전문가들에게는 컨설팅 수익 창출의 기회가 생기고 있습니다. 캐나다 기업들은 프랑스어와 영어로 된 이중 언어 컨텐츠 제공을 우선시하고 있는 반면, 멕시코 소매업체들은 미국·멕시코·캐나다 무역 회랑에 걸친 재고, 과세, 물류를 연계하는 국경을 초월한 전자상거래 체계에 투자하고 있습니다.

아시아태평양은 12.74%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 인도의 모바일 상거래 시장은 2025년 12월 Unified Payments Interface(UPI)를 통한 134억 건의 거래에 힘입어 2025년에는 1,500억 달러 규모에 달했습니다. 인도네시아, 베트남, 필리핀에서 나타나는 ‘스마트폰 우선’ 행동 양상은 현지 언어 컨텐츠, 현지 결제 게이트웨이, 그리고 저지연 전송에 대한 수요를 이끌고 있습니다. 중국에서는 미니 프로그램 API 및 ‘개인정보보호법’ 준수가 필요한 슈퍼앱 생태계를 중심으로 도입이 진행되고 있습니다. 일본과 한국에서는 전각 문자 세트를 지원하기 위해 레거시 시스템을 클라우드로 이전하고 있는 반면, 싱가포르, 말레이시아, 태국에서는 크로스보더 전자상거래 체계를 활용하여 통관 절차와 결제의 상호 운용성을 간소화하고 있습니다.

유럽은 상호 운용성과 명시적 동의를 의무화하는 GDPR(EU 개인정보보호규정) 및 데이터 법에 힘입어 큰 시장 점유율을 차지하고 있으며, 오픈소스 기반의 API 중심 플랫폼이 선호되고 있습니다. 독일, 영국, 프랑스는 자동차, 명품, 금융 등 각 분야에서 옴니채널 경험에 대한 대규모 투자를 지속하고 있습니다. '상호운용 가능한 유럽법'은 공공기관에 표준화된 API의 채택을 의무화하고 있으며, 이를 준수하는 공급업체의 조달 기회를 확대되고 있습니다. 남유럽 국가들은 유럽연합(EU)의 부흥 기금을 활용하여 현대화를 가속화하고 있는 반면, 북유럽에서는 완전한 서버리스 구축이 진행되고 있습니다. 남미, 중동 및 아프리카는 여전히 신흥 시장이며, 브라질은 소매 및 핀테크 분야에 대한 투자를 통해 라틴아메리카를 주도하고 있고, 사우디아라비아와 아랍에미리트는 스마트시티 구상을 최우선 과제로 삼고 있으며, 남아프리카공화국은 인프라 측면의 과제가 있음에도 불구하고 사하라 이남 지역의 기술 거점으로서의 역할을 수행하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the digital experience platform market size reached USD 17.82 billion in 2026 and is projected to climb to USD 30.11 billion by 2031, advancing at an 11.06% CAGR during the forecast period.

This report is Segmented by Component (Platform and Services), Deployment Mode (On-Premises and Cloud), End-User Industry (Retail and E-Commerce, IT and Telecom, BFSI, Healthcare, Manufacturing, and Other End-User Industries), Organization Size (Large Enterprises and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Digital Experience Platform Market Trends and Insights

Cloud-First Enterprise IT Strategies Accelerate DXP Adoption

Organizations continue to replace on-premises licenses with software-as-a-service models that bundle compute, storage, and content-delivery bandwidth, trimming total cost of ownership by up to 40% over five years. Cloud platforms also enable continuous delivery, letting teams deploy code updates multiple times per day instead of waiting for maintenance windows. Microsoft Azure and Amazon Web Services offer one-click marketplaces that shorten proof-of-concept cycles from months to weeks. Multi-cloud support further reduces vendor-lock-in fears and satisfies sovereignty requirements, spurring large enterprises to migrate mission-critical workloads.

Rapid Shift to Omnichannel, AI-Driven Personalization

Consumers now engage across six to eight touchpoints before purchase, creating demand for platforms that unify identity, behavior, and real-time context. Retail and e-commerce dominated 2025 revenue because merchants deploy recommendation engines that surface relevant items within milliseconds. Adobe integrated Firefly generative models to automate product copy in 29 languages, accelerating campaign iterations and boosting conversion potential. BFSI institutions leverage open-banking APIs to deliver balance aggregation and personalized loan offers, trimming acquisition costs and shortening conversion cycles.

Integration Complexity with Legacy Stacks

Large enterprises run 15 to 20 marketing and commerce applications that rely on proprietary APIs and batch integrations. Re-platforming to composable DXPs requires mapping data schemas, reconciling duplicate records, and ensuring transaction consistency, often stretching projects to 18 months and absorbing 40% of budgets. Financial institutions face additional hurdles because mainframe cores cannot expose RESTful APIs without expensive modernization. Pre-built connectors cover standard use cases, but custom workflows and compliance rules still demand hand-coded middleware, fueling demand for specialized systems integrators.

Other drivers and restraints analyzed in the detailed report include:

- Gen-AI Content Operations Cut Time-to-Market for Campaigns

- Mobile-Commerce Boom in Emerging Asia Drives Mid-Market Demand

- Escalating Data-Privacy Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The services segment accounted for 31.27% of 2025 revenue and is on track for a 12.34% CAGR, the quickest growth among component groups. This trajectory stems from enterprises allocating 40-50% of Digital Experience Platform market budgets to systems integration, managed operations, and strategic consulting. Platforms still generated 68.73% of sales in 2025 through recurring subscriptions, content-delivery capacity, and API-call metering. Yet the pivot toward composable stacks multiplies third-party touchpoints, escalating demand for integrators with cross-platform credentials. Global consultancies broadened their DXP practices by onboarding specialists in headless content management, customer data platforms, and marketing automation. Training engagements now teach marketing teams low-code development, API management, and experimentation methods, democratizing tasks once reserved for technical departments. Services also encompass ongoing optimization for generative-AI modules, as clients fine-tune prompts and guardrails to comply with brand and regulatory requirements.

While license revenue remains essential, a steady shift toward usage-driven billing models is poised to reshape earnings portfolios. Vendors now bundle white-glove onboarding, performance tuning, and continuous experimentation as premium tiers, cultivating high-margin annuity streams. At the same time, managed-service offerings address talent shortages by providing 24/7 site reliability and optimization, enabling customers to focus on content and commerce strategy rather than infrastructure maintenance. This dynamic positions services as the primary lever for sustained wallet share in the market.

The cloud segment secured 57.83% revenue in 2025 and is expanding at 13.11% annually, well ahead of on-premises deployments. Elastic scalability, consumption-based pricing, and automated security patching appeal to organizations seeking predictable costs and rapid experimentation. Even security-sensitive industries now pilot hybrid frameworks that keep sensitive data on-premises while offloading content delivery and analytics to public clouds, balancing compliance with agility. Oracle's multi-cloud support illustrates growing demand for workload portability, letting enterprises negotiate favorable terms across providers while meeting sovereignty rules.

Continuous integration pipelines, enabled by container orchestration and infrastructure-as-code, enable multiple code pushes daily, supporting real-time inventory synchronization and AI personalizers. However, reliance on third-party uptime exposes the service to service-level breaches. Enterprises mitigate risks through multi-region failovers, API rate-limit monitoring, and contractual penalties for downtime. As tooling matures, hybrid models should capture incremental share, but public cloud is set to remain the growth engine for the market.

Geography Analysis

North America generated 38.73% of 2025 revenue, anchored by Fortune 500 spend on enterprise-grade governance, SOC 2 Type II and ISO 27001 certifications, and multi-tenant architectures. United States privacy legislation, fragmented across 14 states, compels geo-fenced consent and retention policies, lifting entry barriers for smaller vendors but opening advisory revenue for compliance specialists. Canadian enterprises prioritize bilingual French-English content delivery, while Mexican retailers invest in cross-border e-commerce frameworks linking inventory, taxation, and logistics across United States-Mexico-Canada trade corridors.

Asia Pacific is forecast to post the highest 12.74% CAGR. India's mobile-commerce sector hit USD 150 billion in 2025, fueled by the Unified Payments Interface's 13.4 billion December 2025 transactions. Smartphone-first behavior in Indonesia, Vietnam, and the Philippines drives demand for vernacular content, local payment gateways, and low-latency delivery. China centers adoption on super-app ecosystems that require mini-program APIs and Personal Information Protection Law compliance. Japan and South Korea migrate legacy systems to cloud to support double-byte character sets, while Singapore, Malaysia, and Thailand leverage cross-border e-commerce frameworks to simplify customs and payment interoperability.

Europe commands significant share, underpinned by GDPR and the Data Act, which mandate interoperability and explicit consent, favoring open-source, API-centric platforms. Germany, the United Kingdom, and France continue heavy investment in omnichannel experiences across automotive, luxury, and finance sectors. The Interoperable Europe Act obliges public agencies to adopt standardized APIs, expanding procurement opportunities for compliant vendors. Southern European nations accelerate modernization using European Union recovery funds, while the Nordic region advances fully serverless deployments. South America, the Middle East, and Africa remain emerging markets; Brazil leads Latin America through retail and fintech investments, Saudi Arabia and the United Arab Emirates prioritize smart-city initiatives, and South Africa acts as the sub-Saharan technology hub despite infrastructure challenges.

- Adobe Inc.

- Salesforce, Inc.

- Sitecore Holding II A/S

- SAP SE

- Oracle Corporation

- IBM Corporation

- Microsoft Corporation

- Progress Software Corporation

- OpenText Corporation

- Acquia Inc.

- Optimizely Inc.

- RWS Holdings plc

- Liferay, Inc.

- Kentico Software s.r.o.

- Bloomreach, Inc.

- Crownpeak Technology Inc.

- Magnolia International Ltd.

- Jahia Solutions Group SA

- Ibexa AS

- Squiz Pty Ltd

- Contentstack Inc.

- CoreMedia AG

- Contentful GmbH

- Pimcore GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first enterprise IT strategies accelerate DXP adoption

- 4.2.2 Rapid shift to omnichannel, AI-driven personalisation

- 4.2.3 Democratization of composable / headless DXPs

- 4.2.4 Gen-AI content-operations cuts time-to-market for campaigns

- 4.2.5 Mobile-commerce boom in emerging Asia drives mid-market demand

- 4.2.6 EU Data Act and US Open Data initiatives mandate interoperability

- 4.3 Market Restraints

- 4.3.1 Integration complexity with legacy stacks

- 4.3.2 Escalating data-privacy compliance costs

- 4.3.3 Shortage of skilled MACH-architecture talent

- 4.3.4 Proprietary schema lock-in raises migration risk

- 4.4 Indusy Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of Macroeconomic Trends on Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premises

- 5.2.2 Cloud

- 5.3 By End-User Industry

- 5.3.1 Retail and E-commerce

- 5.3.2 IT and Telecom

- 5.3.3 Banking, Financial Services and Insurance (BFSI)

- 5.3.4 Healthcare

- 5.3.5 Manufacturing

- 5.3.6 Other End-User Industries

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 Salesforce, Inc.

- 6.4.3 Sitecore Holding II A/S

- 6.4.4 SAP SE

- 6.4.5 Oracle Corporation

- 6.4.6 IBM Corporation

- 6.4.7 Microsoft Corporation

- 6.4.8 Progress Software Corporation

- 6.4.9 OpenText Corporation

- 6.4.10 Acquia Inc.

- 6.4.11 Optimizely Inc.

- 6.4.12 RWS Holdings plc

- 6.4.13 Liferay, Inc.

- 6.4.14 Kentico Software s.r.o.

- 6.4.15 Bloomreach, Inc.

- 6.4.16 Crownpeak Technology Inc.

- 6.4.17 Magnolia International Ltd.

- 6.4.18 Jahia Solutions Group SA

- 6.4.19 Ibexa AS

- 6.4.20 Squiz Pty Ltd

- 6.4.21 Contentstack Inc.

- 6.4.22 CoreMedia AG

- 6.4.23 Contentful GmbH

- 6.4.24 Pimcore GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment