|

시장보고서

상품코드

2066619

게이밍 GPU 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Gaming GPU - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

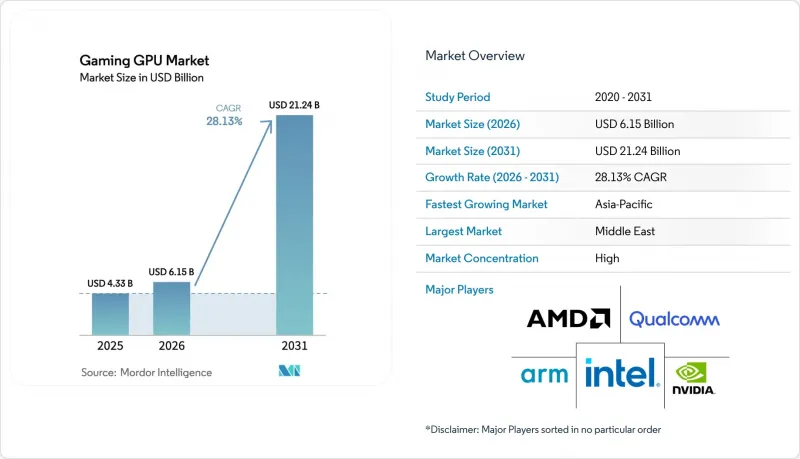

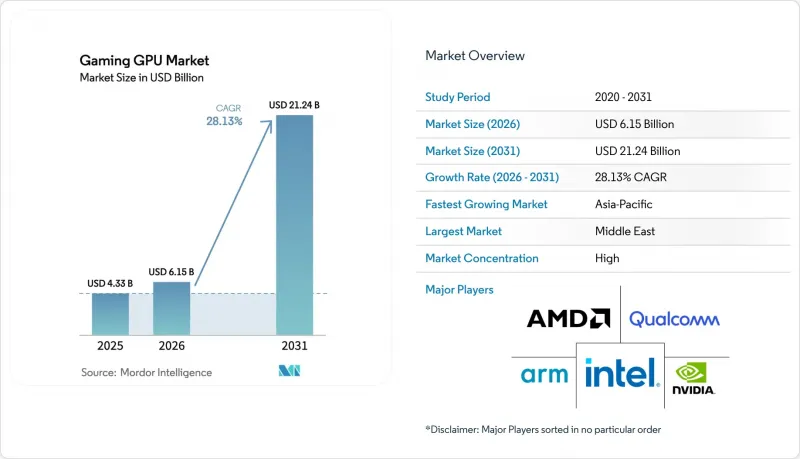

Mordor Intelligence에 의하면, 게이밍 GPU 시장 규모는 2025년 333억 2,000만 달러에서 2026년에는 387억 2,000만 달러로 확대되어 2031년까지 662억 4,000만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 11.34%로 성장할 전망입니다.

본 보고서는 GPU 유형(디스크리트 GPU 및 통합형 GPU), 기기 유형(게이밍 데스크톱, 게이밍 노트북, 스마트폰 및 태블릿), 최종 사용자 유형(캐주얼 게이머 및 애호가/프로 게이머), 메모리 유형(GDDR6, GDDR6X, 통합 메모리, 기타 메모리 유형), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 게이밍 GPU 시장 동향과 인사이트

AI 업스케일링과 레이 트레이싱을 통한 업데이트 주기

게이밍 GPU 시장에서 AI 업스케일링과 뉴럴 렌더링은 가장 강력한 수요 요인 중 하나입니다. NVIDIA는 트랜스포머 기반 렌더링 파이프라인과 멀티프레임 생성 기능을 갖춘 DLSS 4를 도입했으며, 2025년 5월까지 125개 이상의 게임에서 이 기능 세트를 이용할 수 있게 될 것이라고 발표했습니다. 이러한 변화가 중요한 이유는 소프트웨어 튜닝을 통해 구형 그래픽 카드를 한계까지 활용하던 게이머라 할지라도, Blackwell 기반 하드웨어로 전환하지 않으면 더 이상 동일한 성능 수준에 도달할 수 없게 되었기 때문입니다. AMD 역시 RDNA 4 출시 당시 이와 같은 방향성을 강화하여, 더 높은 레이 트레이싱 처리량과 AI 지원 그래픽 기능을 프리미엄급 추가 기능이 아닌 표준적인 기대치로 자리매김했습니다. 이로 인해 신형과 구형 하드웨어 간의 성능 격차가 더욱 벌어지게 되었으며, 주요 아키텍처의 각 릴리스는 단순한 정기적인 업데이트를 넘어 상업적으로 더 큰 의미를 갖게 되었습니다.

e스포츠 및 경쟁형 FPS 게임에서의 업그레이드 수요

시장은 여전히 e스포츠용 게임에 의해 주도되고 있으며, 이 분야에서는 화질과 마찬가지로 프레임 안정성과 낮은 지연 시간이 중요하게 여겨지고 있습니다. NVIDIA는 ‘Reflex 2’를 강력히 강조하며, 이 기술을 통해 입력 지연 시간을 최대 75%까지 줄일 수 있다고 밝혔습니다. 이는 e스포츠나 빠른 반응이 요구되는 게임 장르의 요구 사항에 직접 부합하는 것입니다. 실제로, 이로 인해 업그레이드의 판단 기준이 해상도뿐만 아니라 모션 반응이나 조작의 정밀도로 옮겨가고 있습니다. 게이밍용 그래픽 처리 장치(GPU) 시장이 혜택을 보는 이유는 열성적인 게이머들이 단순한 업데이트만으로는 구형 플랫폼에서 재현할 수 없는 측정 가능한 지연 시간상의 이점을 새로운 하드웨어가 제공할 경우, 아직 정상적으로 작동하는 그래픽 카드라도 교체하려는 의지가 높아지기 때문입니다. 이로 인해 가전 시장 전체가 신중한 태도를 보이는 상황에서도 프리미엄 제품에 대한 수요는 유지될 것입니다.

프리미엄 GPU의 가격 책정과 긴 교체 주기

게이밍 GPU 시장은 프리미엄 부문의 높은 가격 책정으로 인해 여전히 뚜렷한 수요 한계에 직면해 있습니다. NVIDIA는 GeForce RTX 5090을 1,999달러에 출시했으며, 그 밖의 Blackwell 시리즈 역시 최고 성능 대역 전반에 걸쳐 가격대를 상향 조정했습니다. AMD는 중급 제품군에서 보다 공격적인 가격 책정으로 대응했으나, 이러한 포지셔닝을 통해 합리적인 가격이 시장 내 경쟁 전략의 핵심 요소임을 알 수 있습니다. 많은 구매자들은 특히 기존 설치 기반에서 기능 지원이 이미 광범위하게 이루어지고 있는 경우, 최근 출시된 GDDR6X 탑재 그래픽 카드가 현재 출시된 게임의 대부분에 대해 여전히 충분하다고 느끼고 있습니다. 이로 인해 하이엔드 시장에서는 견조한 실적이 유지되고 있지만, 가격에 민감한 시장 부문에서는 제품 교체 주기가 둔화되고 있습니다.

부문별 분석

2025년, 게이밍 GPU 시장에서 디스크리트 GPU는 77.83%의 점유율을 차지하고 있으며, 이는 전용 그래픽 하드웨어가 수익과 성능에 대한 기대치를 얼마나 크게 좌우하고 있는지를 보여줍니다. 시장에서는 4K 게이밍, 고성능 레이 트레이싱, AI를 활용한 렌더링 워크로드 분야에서 여전히 별도의 GPU에 의존하고 있으며, 통합형 솔루션은 하이엔드 분야에서 이를 따라잡는 데 어려움을 겪고 있습니다. NVIDIA는 2025년에 Blackwell 제품군의 가격대를 확대하여 RTX 5090부터 RTX 5050 데스크톱 제품에 이르기까지를 아우르게 되었습니다. AMD는 RDNA 4를 통해 가성비를 중시하는 부문에서 경쟁을 심화시켰으며, 동급 가격대에서 연산 유닛당 레이 트레이싱 처리량 향상과 메모리 용량 확대를 강조했습니다.

또한, 고성능 렌더링 기능에 대한 소프트웨어 지원이 지속적으로 확대되고 있어, 시장은 여전히 디스크리트 GPU에 유리한 상황입니다. NVIDIA에 따르면, 800개 이상의 게임 및 용도이 RTX 기술을 지원하고 있으며, 이로 인해 광범위한 도입 기반을 바탕으로 디스크리트 GPU의 상업적 수명이 연장되고 있습니다. 통합 그래픽은 주류 게임 분야에서 그 성능과 중요성이 점점 더 커지고 있지만, 그 영향은 프리미엄층보다 시장의 저가형 부문에서 더욱 두드러지게 나타나고 있습니다. 즉, 업계에서는 디스크리트 GPU의 주도권이 흔들리지 않을 것으로 보이지만, 보급형 시장에서의 경쟁은 점차 치열해지고 있습니다. 실제로, 열성적인 게이머와 크리에이터, 고성능 노트북 구매자들은 통합형 솔루션에서는 일관되게 제공되기 어려운 성능 여유를 여전히 원하고 있기 때문에 독립형 GPU는 여전히 지출액 중 가장 높은 가치를 차지하는 부분을 차지하고 있습니다. 그 결과, 하위 계층의 동향이 유동적으로 변하고 있음에도 불구하고, 시장의 핵심 수익 기반은 여전히 전용 하드웨어에 머물러 있습니다.

2025년에는 게이밍 데스크톱이 매출의 48.37%를 차지했으나, 게이밍 노트북은 2026년부터 2031년까지 연평균 성장률(CAGR) 11.94%로 성장할 것으로 전망됩니다. 이러한 추세는 게이밍용 그래픽 처리 장치(GPU) 시장에서 데스크톱이 여전히 최대의 수익원인 반면, 현재의 성장세는 휴대용 시스템으로 이동하고 있음을 보여줍니다. NVIDIA는 Blackwell Max-Q를 탑재한 RTX 50 노트북용 GPU를 출시함으로써 이러한 전환을 뒷받침했습니다. 이를 통해 모바일 효율 향상과 배터리 사용 시간 연장, 그리고 프리미엄 OEM 제조업체들에 대한 폭넓은 지원이 실현되었습니다. 한때 수많은 열성 게이머들을 데스크톱 타워에 묶어두었던 성능 격차가 줄어들면서, 시장이 그 혜택을 누리고 있습니다.

노트북의 성장은 단순한 하드웨어 설계의 변화뿐만 아니라, 구매 논리의 변화도 반영하고 있습니다. 구매자들은 최신 AI 렌더링 기능을 포기하지 않으면서도 게임, 업무, 공부, 여행 등 다양한 용도로 활용할 수 있는 단일 기기를 점점 더 많이 찾고 있습니다. NVIDIA가 DLSS 4 및 Blackwell의 기능을 노트북 시스템으로 확장한 것은 고정된 데스크톱 환경 이외의 곳에서도 고급 그래픽 기능을 활용할 수 있게 함으로써 이러한 변화를 뒷받침하고 있습니다. 모바일 게임 기기도 시장에 새로운 고객층을 확보하고 있습니다. 프리미엄 태블릿이나 스마트폰에는 과거에는 더 큰 규모의 플랫폼에만 한정되었던 그래픽 기능이 탑재되게 되었기 때문입니다. 미디어텍의 2026년 플래그십 제품 발표는 모바일 기기가 더 높은 프레임 속도와 레이 트레이싱 지원을 향해 나아가고 있음을 보여주며, 이로 인해 기기 간의 경계가 이전보다 더 모호해지고 있습니다.

지역별 분석

아시아태평양은 2025년에 게이밍 GPU 시장 점유율의 52.88%를 차지할 것으로 예상되며, 2031년까지 연평균 성장률(CAGR) 12.31%로 성장할 것으로 전망됩니다. 이 지역에서 시장이 가장 견조한 이유는 e스포츠에 대한 깊은 관심, 방대한 게이머 인구, 그리고 프리미엄 PC, 노트북, 모바일 게이밍 기기에 대한 수요 증가가 복합적으로 작용한 결과입니다. 한국과 일본은 여전히 고사양 하드웨어 지출 측면에서 중요한 시장인 반면, 인도와 동남아시아에서는 게이밍 스마트폰과 중급형 노트북의 보급 확대에 힘입어 시장 규모가 커지고 있습니다. 또한, 아시아태평양의 게이밍 GPU 시장은 단일 플랫폼에 국한되지 않고 다양한 기기를 자유롭게 오가는 데 거부감이 없는 젊은 게이머층으로부터도 지지를 얻고 있습니다. 한편, 수출 규제로 인해 중국에서 프리미엄 GPU를 구하기가 어려워지고 있으며, 이로 인해 지역 전체의 제품 포지셔닝과 공급업체의 비즈니스 기회가 재편될 가능성이 있습니다.

북미는 높은 평균 판매 가격, 성숙한 PC 게임 문화, 그리고 캐주얼 게이머보다 더 자주 하드웨어를 교체하는 열성적인 사용자들로부터의 강력한 수요에 힘입어, 여전히 지역별 매출 2위 자리를 유지하고 있습니다. 미국 시장은 하이엔드 디스크리트 그래픽 카드에 있어 특히 중요하며, 최상급 고성능 제품에 대한 수요는 여전히 막대합니다. NVIDIA의 ‘Blackwell’ 제품 출시와 폭넓은 OEM 지원은 하이엔드 제품의 출시 및 조기 도입에 있어 북미가 여전히 얼마나 중요한 역할을 하고 있는지를 보여줍니다. 유럽도 비슷한 수요 양상을 보이고 있으며, e스포츠와 PC 하드웨어에 대한 관심이 높아지고 있는 것이 하이엔드 제품의 안정적인 시장을 뒷받침하고 있습니다.

남미, 중동 및 아프리카는 매출 규모 면에서는 작지만, 이 세 지역은 모두 게임 산업에서 실질적인 중요성 측면에서 지속적인 성장을 보이고 있습니다. 남미에서는 하드웨어 선택에 있어 가격의 합리성이 여전히 주요 요인으로 작용하고 있기 때문에 수요는 중급형 시스템과 모바일 게임에 집중되고 있습니다. 중동 및 아프리카에서는 e스포츠 경기장에 대한 투자와 특정 시장에서 고가 제품에 대한 소비자 수요가 증가함에 따라, 프리미엄 게이밍 환경의 존재감이 커지고 있습니다. 또한, 많은 사용자에게는 하이엔드 PC보다 프리미엄 스마트폰을 통해 더 뛰어난 그래픽 기능을 손쉽게 이용할 수 있기 때문에 Arm의 모바일 GPU IP가 지속적으로 확대되고 있는 점도 이들 지역 시장을 뒷받침하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the gaming GPU market size is expected to increase from USD 33.32 billion in 2025 to USD 38.72 billion in 2026 and reach USD 66.24 billion by 2031, growing at a CAGR of 11.34% over 2026-2031.

This report is Segmented by GPU Type (Discrete GPUs, and Integrated GPUs), Device Type (Gaming Desktops, Gaming Laptops, and Smartphones and Tablets), End-User Type (Casual Gamers, and Enthusiast/Professional Gamers), Memory Type (GDDR6, GDDR6X, Unified Memory, and Other Memory Types), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Gaming GPU Market Trends and Insights

AI Upscaling and Ray Tracing Refresh Cycle

The gaming GPU market is seeing one of its strongest demand triggers from AI upscaling and neural rendering. NVIDIA introduced DLSS 4 with a transformer-based rendering pipeline and Multi Frame Generation, and stated that the feature set would be available across more than 125 titles by May 2025. That change matters because gamers who had stretched older cards through software tuning could no longer reach the same performance threshold without moving to Blackwell-based hardware. AMD reinforced the same direction when it launched RDNA 4, positioning higher ray tracing throughput and AI-ready graphics capabilities as standard expectations rather than premium extras. This creates a wider performance gap between new and older hardware, making each major architecture launch more commercially meaningful than a routine refresh.

Esports and Competitive FPS Upgrade Demand

The market continues to be driven by competitive gaming, where frame consistency and low latency matter as much as visual quality. NVIDIA placed strong emphasis on Reflex 2, saying the technology can reduce input latency by up to 75%, which directly aligns with the needs of esports and fast-response game genres. In practice, that shifts upgrade logic away from resolution alone and toward motion response and control precision. The gaming graphics processing unit (GPU) market benefits because serious players are more willing to replace still-functional cards when new hardware offers a measurable latency advantage that older platforms cannot replicate through simple updates. This also keeps premium products relevant even when the broader consumer electronics environment becomes more cautious.

Premium GPU Pricing and Long Replacement Cycles

The gaming GPU market still faces a clear demand limit from high selling prices at the premium end. NVIDIA launched the GeForce RTX 5090 at USD 1,999, while the rest of the Blackwell stack also established a higher price ladder across top performance tiers. AMD responded with more aggressive pricing in the mid-range, but its positioning also showed that affordability has become a central part of competitive strategy in the market. Many buyers still find that recent GDDR6X-based cards remain sufficient for a large share of current titles, especially when feature support is already broad across the installed base. That keeps revenue healthy at the high end but slows unit replacement in more price-sensitive parts of the market.

Other drivers and restraints analyzed in the detailed report include:

- Gaming Laptop and Handheld Pc Proliferation

- Mobile Ray Tracing and Premium Smartphone GPU Adoption

- GDDR7 and Advanced Memory Tightness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Discrete GPUs held 77.83% of the gaming GPU market in 2025, which shows how strongly dedicated graphics hardware still shapes revenue and performance expectations. The market continues to rely on discrete cards for 4K gaming, advanced ray tracing, and AI-assisted rendering workloads, while integrated solutions still struggle to match them at the top end. NVIDIA expanded the pricing range for its Blackwell lineup in 2025, stretching from the RTX 5090 down to the RTX 5050 desktop product. AMD added pressure in the value-oriented part of the segment with RDNA 4, emphasizing higher ray tracing throughput per compute unit and greater memory capacity at comparable price points.

The market also remains favorable to discrete cards, as software support continues to expand for advanced rendering features. NVIDIA stated that more than 800 games and applications support RTX technologies, which helps extend the commercial life of dedicated cards across a wide installed base. Integrated graphics are becoming more capable and more relevant in mainstream gaming, but they are influencing the lower end of the market more than the premium end. That means the industry is not seeing discrete leadership collapse, but it is seeing the entry tier become more contested. In practical terms, discrete GPUs still anchor the highest-value portion of spending because serious players, creators, and premium laptop buyers continue to look for a performance margin that integrated solutions rarely deliver consistently. The result is that the market keeps its core revenue base in dedicated hardware even as the lower tiers become more fluid.

Gaming desktops held 48.37% of revenue in 2025, while gaming laptops are projected to expand at an 11.94% CAGR from 2026 to 2031. That pattern shows that the gaming graphics processing unit (GPU) market still depends on desktops for its largest revenue pool, but current growth is shifting toward portable systems. NVIDIA supported that transition when it rolled out RTX 50 Laptop GPUs with Blackwell Max-Q, tying higher mobile efficiency to longer battery life and broader premium OEM coverage. The market benefits because this narrows the historical performance gap that once kept many serious players tied to desktop towers.

Laptop growth also reflects a change in purchase logic rather than only a change in hardware design. Buyers increasingly want a single device that can handle gaming, work, study, and travel without sacrificing access to newer AI rendering features. NVIDIA's extension of DLSS 4 and Blackwell capabilities into laptop systems supports that shift by making advanced graphics features available beyond fixed desktop setups. Mobile gaming devices add another layer to the market, as premium tablets and smartphones now feature graphics capabilities once limited to larger platforms. MediaTek's 2026 flagship launch showed how mobile devices are moving toward higher frame rates and ray tracing support, which keeps the overall device boundary more fluid than before.

Geography Analysis

Asia-Pacific held 52.88% of the gaming GPU market share in 2025 and is projected to grow at a 12.31% CAGR through 2031. The market is strongest in this region because it combines deep esports engagement, large gamer populations, and rising demand for premium PCs, laptops, and mobile gaming devices. South Korea and Japan remain important for high-end hardware spending, while India and Southeast Asia add scale through broader adoption of gaming smartphones and mid-range laptops. The gaming GPU market also draws support in Asia-Pacific from a younger gaming base that is comfortable moving across device types rather than staying within a single platform. At the same time, export controls have made it more difficult for China to obtain premium GPUs, potentially reshaping product positioning and vendor opportunities across the region.

North America remains the second-largest regional revenue base, supported by high average selling prices, a mature PC gaming culture, and strong demand from enthusiasts who replace hardware more often than casual players. The United States market is especially important for premium discrete cards, where top-tier performance products still find buyers at scale. NVIDIA's Blackwell product rollouts and broad OEM support show how central North America remains for premium launches and early adoption. Europe follows a similar demand pattern, with interest in competitive gaming and PC hardware supporting a steady market for higher-end products.

South America, the Middle East, and Africa are smaller in terms of revenue, but all three regions continue to grow in practical gaming relevance. In South America, demand is more concentrated in mid-range systems and mobile gaming because affordability remains a major factor in hardware choice. In the Middle East and Africa, premium gaming setups are gaining visibility through esports venue investment and higher-end consumer demand in selected markets. Arm's continued expansion of mobile GPU IP also supports market in these regions, as premium smartphones remain a more accessible path to advanced graphics features than top-tier PCs for many users.

- NVIDIA Corporation

- Advanced Micro Devices, Inc.

- Intel Corporation

- Qualcomm Technologies, Inc.

- Apple Inc.

- Samsung Electronics Co., Ltd.

- Arm Limited

- MediaTek Inc.

- Imagination Technologies Limited

- ASUSTeK Computer Inc.

- Micro-Star International Co., Ltd.

- GIGA-BYTE Technology Co., Ltd.

- Acer Inc.

- Lenovo Group Limited

- Dell Technologies Inc.

- HP Inc.

- Razer Inc.

- ZOTAC Technology Limited

- SAPPHIRE Technology Limited

- TUL Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI Upscaling and Ray Tracing Refresh Cycle

- 4.2.2 Esports and Competitive FPS Upgrade Demand

- 4.2.3 Gaming Laptop and Handheld PC Proliferation

- 4.2.4 Mobile Ray Tracing and Premium Smartphone GPU Adoption

- 4.2.5 PC Development Focus and Steam Deck Optimization

- 4.2.6 Creator-Centric UGC and Real-Time Modding Workloads

- 4.3 Market Restraints

- 4.3.1 Premium GPU Pricing and Long Replacement Cycles

- 4.3.2 Cloud Gaming and Good-Enough Integrated Graphics Substitution

- 4.3.3 GDDR7 and Advanced Memory Tightness

- 4.3.4 Export Controls and China-Specific Gaming SKU Fragmentation

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By GPU Type

- 5.1.1 Discrete GPUs

- 5.1.2 Integrated GPUs

- 5.2 By Device Type

- 5.2.1 Gaming Desktops

- 5.2.2 Gaming Laptops

- 5.2.3 Smartphones and Tablets (Mobile Gaming)

- 5.3 By End-User Type

- 5.3.1 Casual Gamers

- 5.3.2 Enthusiast / Professional Gamers

- 5.4 By Memory Type

- 5.4.1 GDDR6

- 5.4.2 GDDR6X

- 5.4.3 Unified Memory

- 5.4.4 Other Memory Types (GDDR5, Legacy)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 NVIDIA Corporation

- 6.4.2 Advanced Micro Devices, Inc.

- 6.4.3 Intel Corporation

- 6.4.4 Qualcomm Technologies, Inc.

- 6.4.5 Apple Inc.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Arm Limited

- 6.4.8 MediaTek Inc.

- 6.4.9 Imagination Technologies Limited

- 6.4.10 ASUSTeK Computer Inc.

- 6.4.11 Micro-Star International Co., Ltd.

- 6.4.12 GIGA-BYTE Technology Co., Ltd.

- 6.4.13 Acer Inc.

- 6.4.14 Lenovo Group Limited

- 6.4.15 Dell Technologies Inc.

- 6.4.16 HP Inc.

- 6.4.17 Razer Inc.

- 6.4.18 ZOTAC Technology Limited

- 6.4.19 SAPPHIRE Technology Limited

- 6.4.20 TUL Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment