|

시장보고서

상품코드

2066644

오픈 소스 전사적 자원 계획(ERP) 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Open Source Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

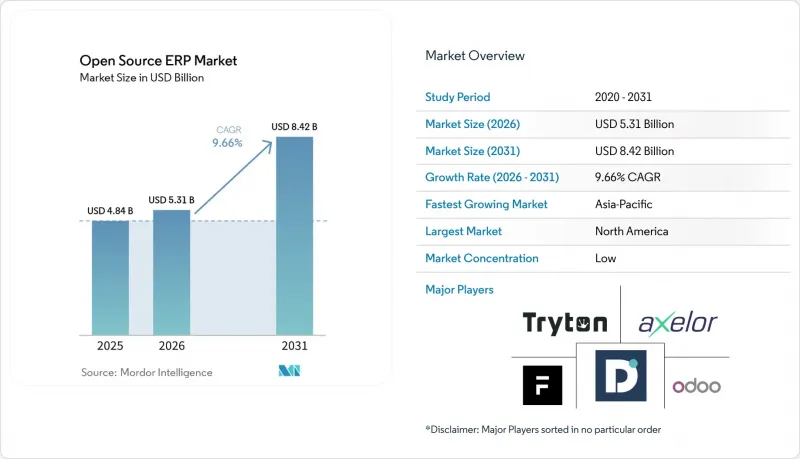

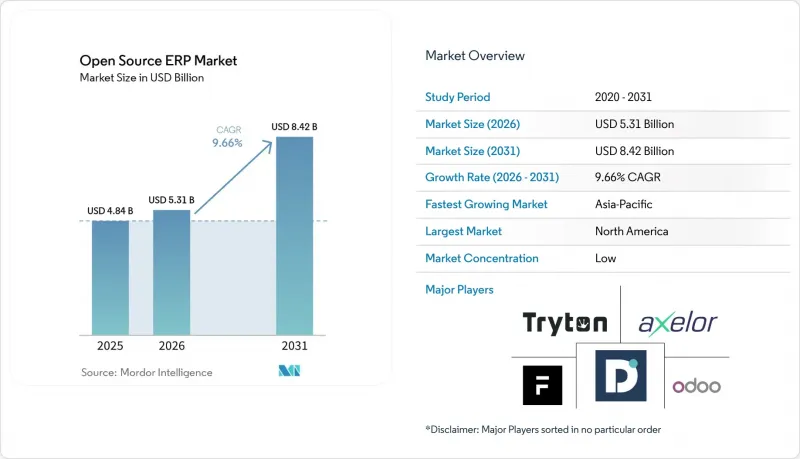

Mordor Intelligence에 의하면, 2026년 오픈 소스 전사적 자원 계획(ERP) 시장 규모는 53억 1,000만 달러에 달할 것으로 예상됩니다. 2025년 48억 4,000만 달러에서 증가하고 있습니다.

또한, 2031년의 예측치는 84억 2,000만 달러이며, 2026년부터 2031년까지 연평균 성장률(CAGR) 9.66%로 성장할 것으로 전망됩니다.

본 보고서는 배포 모델(클라우드, On-Premise, 하이브리드), 구성 요소(소프트웨어 및 서비스), 조직 규모(중소기업 및 대기업), 최종 사용자 산업(제조업, 의료, 은행 및 금융 서비스·보험(BFSI), 교육, 기타) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 오픈 소스 전사적 자원 계획(ERP) 시장 동향 및 인사이트

중소기업에서의 클라우드 도입 모델 보급 확대

구독형 인프라를 통해 서버가 더 이상 필요하지 않게 되고, ‘성장에 따른 종량제 과금’이 가능해짐에 따라 클라우드 호스팅형 솔루션이 On-Premise형을 점차 대체하고 있습니다. 특히 팀 구성원이 여러 지역에 흩어져 있는 경우, 중소기업은 재무, 재고, 고객 데이터에 대한 원격 접근을 중요하게 여깁니다. 하이브리드 방식은 기밀성이 높은 원장을 On-Premise에 유지하면서 조달 및 CRM을 퍼블릭 클라우드로 이전함으로써, GDPR(EU 개인정보보호규정) 및 이와 유사한 데이터 거주 규정을 준수하면서도 하드웨어 비용을 절감할 수 있는 가교 역할을 하는 전략을 제공합니다. 다중 테넌트 간 분리 기능이 향상됨에 따라, 현재는 대부분의 보안 지침을 충족하게 되었으며, 전문 서비스업과 같이 신중한 업계에서도 전환이 진행되고 있습니다. 전반적으로 볼 때, 클라우드의 성장은 오픈 소스 전사적 자원 계획(ERP) 시장에서 예상되는 매출 증가분의 5분의 1 이상을 차지하고 있습니다.

독점적 ERP와 비교한 총 소유 비용(TCO) 절감

커뮤니티 버전에서는 라이선스 비용이 들지 않아, 5년간의 총 소유 비용을 30-50% 절감할 수 있습니다. 소매, 섬유, 경공업 등 이익률이 낮은 기업들에게 있어 이러한 비용 절감은 결정적인 요소가 됩니다. 사내에 충분한 인력이 없는 경우, 외부 컨설턴트 비용이 발생하여 업그레이드 및 보안 대책에 소요되는 첫해 예산의 15-20%를 차지할 가능성이 있습니다. 그럼에도 불구하고, 독점 소프트웨어 제품군의 경우 변경 요청 수수료가 발생하여 그 비용이 당초 계약 금액을 초과하는 경우도 있지만, 오픈 소스라면 공급업체의 승인 없이도 반복적인 변경이 가능합니다. 인도네시아나 케냐 등 가격에 민감한 지역에서는 이러한 요인들이 구매 결정을 오픈 소스 ERP 쪽으로 기울게 하여, 매년 수천 건의 신규 도입을 통해 대상 시장을 확대되고 있습니다.

엔터프라이즈급 지원 서비스 이용 가능성의 제한

아프리카와 중동의 많은 기업들은 현지 시스템 통합 업체들이 24시간 지원 체계를 갖추거나 공인 컨설턴트를 충분히 확보하지 못하고 있어, 커뮤니티 주도형 플랫폼 도입을 주저하고 있습니다. 케냐와 나이지리아의 금융 서비스 기업들로부터는 가동 중단으로 인한 벌금이 라이선스 비용 절감 효과를 상회하기 때문에 독자적인 ERP 제품군을 일부 유지할 수밖에 없다는 보고가 접수되고 있습니다. 일부 업체들이 관리형 호스팅 및 프리미엄 SLA 패키지를 확대하고 있지만, 2선 도시에서는 여전히 서비스 제공의 사각지대가 남아 있습니다. 전 세계 공급업체와 지역 재판매업체간의 제휴를 통해 서비스 부족 현상은 점차 해소되고 있습니다. 보다 폭넓은 전문가층이 자리 잡을 때까지는 이러한 제약으로 인해 전체 연평균 성장률(CAGR)이 1퍼센트포인트 이상 낮아지게 될 것입니다.

부문별 분석

클라우드는 2025년에 오픈 소스 전사적 자원 계획(ERP) 시장 점유율의 45.12%를 차지했으며, 연평균 성장률(CAGR) 10.05%로 가장 빠르게 성장할 전망입니다. 공장 현장의 엣지 컴퓨팅 노드는 현재 클라우드 분석과 연동되어 생산 라인의 지연을 최소화하고 있습니다. 구독형 호스팅을 통해 서버 조달 및 유지보수가 필요 없어지므로, 고객 확보 및 연구 개발(R&D)에 투입할 자금을 확보할 수 있습니다. 하이브리드 전략에서는 기밀성이 높은 원장이나 제품 처방을 On-Premise에 배치하는 한편, 조달 및 CRM을 오프사이트로 이전함으로써 데이터 주권 관련 법규 준수를 용이하게 합니다. 이러한 단계적 접근 방식을 통해 가동 중단 시간을 최소화하고 기술을 점진적으로 전환할 수 있게 되므로, 클라우드는 오픈 소스 전사적 자원 계획(ERP) 시장의 향후 투자를 위한 기반이 됩니다.

중소기업이 주요 도입 주체입니다. 이는 몇 시간 이내에 샌드박스 환경을 구축하고, 실제로 사용한 리소스에 대해서만 비용을 지불할 수 있기 때문입니다. 관리형 호스팅 제공업체는 자동 백업, 암호화, 패치 적용을 하나의 패키지로 제공하여 관리 부담을 줄여줍니다. 운송 및 물류 분야에서는 클라우드 ERP가 텔레매틱스 데이터를 통합하여 배차 계획 및 연료 최적화를 개선하고 있습니다. 방위 관련 기업이나 제약 연구소에서는 지적 재산권 보호를 이유로 여전히 On-Premise 환경을 선호하고 있지만, 보안이 강화된 테넌트 분리 모델의 시범 운영이 진행되고 있습니다. 인증 제도가 성숙해짐에 따라, 클라우드의 매력은 과거에는 이용이 불가능하다고 여겨졌던 분야로까지 확대될 것이며, 이 부문의 성장세는 지속될 것입니다.

2025년에는 벤더들이 자체 현지화 버전과 급여 계산, 세무 확장 기능을 통해 수익을 창출함에 따라 소프트웨어 모듈이 매출의 58.62%를 차지했습니다. 그러나 ERP 엔진을 결제 게이트웨이, 데이터 레이크, IoT 피드에 통합하는 데 필요한 노력을 반영하여, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 9.74%를 기록하며 성장할 것으로 전망됩니다. 이전에 Python이나 Java 전문가를 보유하지 않았던 조직들은 현재 업그레이드, 맞춤형 보고서 작성, 보안 감사를 위해 시스템 통합 업체를 고용하고 있습니다. 커뮤니티 라이선스로 인해 소프트웨어 비용이 발생하지 않게 되면, 일반적인 5년간의 총 소유 비용(TCO)에서 서비스 비용이 지출의 최대 70%를 차지하게 됩니다. 사용자가 단일 모놀리식 시스템이 아닌 여러 개의 조합 가능한 용도를 다루게 됨에 따라, 교육 및 변경 관리로 인해 서비스 예산은 더욱 확대됩니다.

4시간 이내의 응답 시간을 보장하는 프리미엄 지원 계약이 인기를 끌고 있으며, 특히 가동 중단이 매출 손실로 이어지는 소매 업계에서는 이러한 경향이 두드러집니다. 이전 서비스는 독자적인 맞춤 설정을 개방형 플러그인으로 변환하여 벤더 종속성을 완화합니다. 컴포저블 아키텍처로 인해 모듈 교체 속도가 빨라짐에 따라, 지속적인 통합 리테이너 계약에 대한 수요는 계속 증가할 것이며, 이는 컨설팅 파트너에게 지속적인 수익원이 될 것입니다. 따라서 소프트웨어 및 서비스 간의 상호작용이 오픈 소스 전사적 자원 계획(ERP) 시장 전체에서 장기적인 가치 창출의 기반이 되고 있습니다.

지역별 분석

아시아태평양은 인도의 중소기업 및 소규모 기업(MSME)을 위한 디지털화 기금과 중국 내 공장에서의 스프레드시트 회계 폐지 추진에 힘입어 연평균 성장률(CAGR) 10.55%라는 가장 빠른 성장 궤도를 그리고 있습니다. 한국의 ‘스마트 제조’ 프로그램 보조금을 통해 ERP 도입 비용의 최대 50%가 지원되고 있으며, 부품 공급업체들 사이에서 시범 프로젝트가 활발히 진행되고 있습니다. 동남아시아에서는 베트남과 인도네시아가 현지 통합 업체를 활용해 다국어 세무 신고에 대응할 수 있도록 오픈 소스 모듈을 맞춤화하고 있으며, 이를 통해 수출 기업의 도입을 가속화하고 있습니다. 북미는 성숙한 SaaS 생태계와 풍부한 솔루션 파트너의 지원을 바탕으로 36.40%의 점유율을 차지하고 있습니다. 중견 기업들이 기존의 On-Premise 시스템에서 이전을 완료함에 따라 성장이 꾸준히 이어지고 있습니다. 미국의 제조업체들은 오픈 소스 스택을 활용하여 기계 모니터링과 재무 관리를 연계하고 있으며, 캐나다의 소매업체들은 옴니채널 기능을 활용하여 온라인과 오프라인 매장의 재고를 통합하고 있습니다. 벤처 캐피털은 계속해서 이 지역에 거점을 둔 상용 벤더들을 지원하고 있으며, 이는 오픈 소스 전사적 자원 계획(ERP) 시장에 대한 신뢰도가 높음을 입증하고 있습니다.

유럽에서는 이러한 흐름 속에서 양극화가 나타나고 있습니다. 독일과 프랑스는 국산 소프트웨어를 우대하는 ‘인더스트리 4.0’ 보조금 제도를 통해 진전을 보이고 있습니다. 동유럽과 러시아는 수입 대체 정책으로 인해 국가 예산이 국내 생산에 투입되고 있기 때문에 더욱 빠르게 성장하고 있습니다. 러시아의 프로그램에 따르면, 2024년에 12개 산업 역량 센터에 자금을 지원하고 해외 공급업체로부터의 전환을 지도함으로써 라이선스 비용 유출을 줄였습니다. 한편, 스칸디나비아 국가들에서는 투명성 제고와 조달 비용 절감을 목적으로 공공 부문에서 오픈 소스 ERP 도입이 진행되고 있습니다.

라틴아메리카에서는 규제 지원이 호재로 작용하고 있습니다. 브라질에서는 전자 청구서 의무화로 인해, 기업들이 실시간 세무 보고에 대응할 수 있도록 ERP 업그레이드가 요구되고 있습니다. 아르헨티나와 볼리비아도 이와 유사한 의무화 조치를 도입함에 따라, 규제를 준수하는 오픈스택에 대한 수요가 증가하고 있습니다. 해당 지역의 클라우드 인프라 확충으로 지연 현상이 완화됨에 따라, 더 많은 기업이 워크로드를 오프사이트로 이전하도록 장려되고 있습니다. 아프리카는 도입 단계로서는 아직 초기 단계이지만, 장래성은 밝습니다. TradeMark Africa의 보고서에 따르면, 이미 50만 개 이상의 기업이 첨단 디지털 도구를 도입하고 있습니다. 케냐와 나이지리아에서는 도입을 가속화하기 위한 보조금 및 교육 프로그램을 시행하고 있으며, 이는 오픈 소스 전사적 자원 계획(ERP) 시장에 향후 기여할 것으로 기대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the open source enterprise resource planning market size in 2026 is estimated at USD 5.31 billion, up from USD 4.84 billion in 2025, with 2031 projections showing USD 8.42 billion, growing at a 9.66% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premises, and Hybrid), Component (Software and Services), Organization Size (Small and Medium Enterprises and Large Enterprises), End-User Industry (Manufacturing, Healthcare, Banking, and Financial Services and Insurance (BFSI), Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Open Source Enterprise Resource Planning Market Trends and Insights

Rising Adoption of Cloud Deployment Models Among SMEs

Cloud-hosted solutions are replacing on-premises installations because subscription-based infrastructure eliminates the need for servers and enables pay-as-you-grow pricing. Smaller firms value remote access to finance, inventory, and customer data, especially when teams are distributed across regions. Hybrid rollouts provide a bridge strategy by keeping sensitive ledgers on-premises while shifting procurement or CRM to public cloud, satisfying GDPR or similar residency rules while reducing hardware costs. Improved multi-tenant isolation now meets most security guidelines, encouraging even cautious sectors such as professional services to migrate. Overall, cloud growth accounts for more than one-fifth of the incremental revenue expected in the open source enterprise resource planning market.

Lower Total Cost of Ownership Compared to Proprietary ERP

Community editions eliminate license fees and reduce five-year ownership costs by 30-50%. Savings are decisive for firms with thin margins in retail, textiles, and light manufacturing. Expenses reappear if in-house talent is scarce, because external consultants can absorb 15-20% of first-year budgets for upgrades and security. Even so, proprietary suites impose change-order fees that can surpass initial contracts, whereas open code allows iterative changes without vendor approval. In price-sensitive regions such as Indonesia and Kenya, these factors tilt purchase decisions toward open-source ERP, widening the addressable market by thousands of new installations each year.

Limited Availability of Enterprise-Grade Support Services

Many African and Middle Eastern enterprises hesitate to deploy community platforms because local integrators lack 24-hour support and certified consultants. Financial services firms in Kenya and Nigeria report that downtime penalties outweigh license savings, driving partial retention of proprietary suites. Several vendors are expanding managed hosting and premium SLA packages, yet coverage gaps persist in tier-2 cities. Partnerships between global providers and regional resellers are gradually closing the service deficit. Until a broader bench of experts exists, this restraint will subtract more than a single percentage point from overall CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Digital Transformation Initiatives in Manufacturing Sector

- Growing Preference for AI-Ready Open Source Stacks for Composable ERP

- Persistent Security and Compliance Concerns Around Community Versions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud captured 45.12% of the open-source ERP market share in 2025 and will expand the fastest, with a 10.05% CAGR. Edge computing nodes on factory floors now sync with cloud analytics to limit latency on production lines. Subscription hosting removes the need for server procurement and maintenance, freeing capital for customer acquisition or R&D. Hybrid strategies position sensitive ledgers or product formulas on-premises while moving procurement or CRM off-site, easing compliance with data sovereignty statutes. This phased approach minimizes downtime and enables gradual skills transfer, making the cloud the cornerstone of future spending in the open source enterprise resource planning market.

SMEs are the primary adopters because they can spin up sandboxes within hours and pay only for the resources they consume. Managed hosting providers bundle automatic backups, encryption, and patching, lowering administrative overhead. In transportation and logistics, cloud ERP integrates telematics data to improve dispatch planning and fuel optimization. Defense contractors and pharmaceutical labs still prefer on-premises instances for intellectual property protection, but pilots of secure tenant isolation models are underway. As certifications mature, the cloud's appeal will broaden to sectors once considered off-limits, maintaining momentum for this segment.

Software modules accounted for 58.62% of revenue in 2025, as vendors monetize proprietary localizations, payroll, and tax extensions. Yet services will grow at 9.74% CAGR through 2031, reflecting labor required to knit ERP engines into payment gateways, data lakes, and IoT feeds. Organizations that lacked Python or Java experts now hire integrators for upgrades, custom reports, and security audits. A typical five-year total cost of ownership shows services consuming up to 70% of spending once community licenses erase software fees. Training and change management further expand service budgets as users navigate multiple composable applications rather than a single monolith.

Premium support contracts that guarantee response times under four hours are gaining popularity, especially in retail, where downtime means lost sales. Migration services convert proprietary customizations into open plug-ins, mitigating vendor lock-in. As composable architecture accelerates module churn, demand for ongoing integration retainer agreements will continue to rise, adding sustained revenue streams for consulting partners. The interplay between software and services, therefore, anchors long-term value capture across the open-source ERP market.

Geography Analysis

Asia-Pacific has the fastest trajectory, advancing at a 10.55% CAGR, driven by India's MSME digitization funds and China's push to retire spreadsheet accounting in factories. Subsidies in South Korea's Smart Manufacturing program reimburse up to 50% of ERP deployment costs, spurring pilot projects among component suppliers. In Southeast Asia, Vietnam and Indonesia leverage local integrators to customize open-source modules for multilingual tax filings, speeding up rollouts for exporters. North America holds 36.40% share, supported by mature SaaS ecosystems and abundant solution partners. Growth is steady as mid-market firms finish migrations from legacy on-premises systems. U.S. manufacturers use open-source stacks to connect machine monitoring with finance, while Canadian retailers leverage omnichannel capabilities to harmonize online and in-store inventory. Venture capital continues to back commercial vendors based in the region, underscoring confidence in the open source ERP market.

Europe shows bifurcated momentum. Germany and France advance through Industry 4.0 grants that favor domestic software. Eastern Europe and Russia grow faster because import-substitution policies channel state budgets toward domestic production. Russia's program funded 12 Industrial Competence Centers in 2024 to guide migrations away from foreign vendors, reducing licensing outflows. Meanwhile, Scandinavian nations are adopting open-source ERP in the public sector to improve transparency and reduce procurement costs.

Latin America rides regulatory catalysts. Brazil's mandatory electronic invoicing requires companies to upgrade their ERPs to support real-time tax reporting. Argentina and Bolivia follow similar mandates, creating a rising tide for compliant open stacks. The region's cloud infrastructure expansion reduces latency, encouraging more firms to shift workloads off-site. Africa is earlier in the curve, but promising. TradeMark Africa reports that over half a million firms already employ sophisticated digital tools. Programs in Kenya and Nigeria provide grants and training to accelerate adoption, ensuring future contributions to the open source enterprise resource planning market.

- Odoo SA

- Frappe Technologies Private Limited

- Axelor SAS

- Dolibarr Foundation

- Tryton Foundation

- iDempiere Association a.s.b.l.

- Metasfresh AG

- ADempiere Global Community

- Openbravo S.L.U.

- xTuple LLC

- DSXtreme LLC (BlueSeer ERP)

- Nexedi SA (ERP5)

- inoLink International Limited (inoERP)

- FrontAccounting LLC

- LedgerSMB Inc.

- WebERP Project Association

- OpenPro Inc.

- The Apache Software Foundation (Apache OFBiz)

- MixERP Inc.

- Compiere Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Cloud Deployment Models Among SMEs

- 4.2.2 Lower Total Cost of Ownership Compared to Proprietary ERP

- 4.2.3 Rapid Digital Transformation Initiatives in Manufacturing Sector

- 4.2.4 Growing Preference for AI-Ready Open Source Stacks for Composable ERP

- 4.2.5 Government-Led Import Substitution Policies Boosting Open Source Uptake in Russia and Latin America

- 4.2.6 Integration of Low-Code Platforms Accelerating Custom Module Development

- 4.3 Market Restraints

- 4.3.1 Limited Availability of Enterprise-Grade Support Services

- 4.3.2 Persistent Security and Compliance Concerns Around Community Versions

- 4.3.3 Shortage of Skilled Contributors to Maintain Critical OSS ERP Modules

- 4.3.4 Rising Fragmentation of Project Forks Creating Upgrade Complexity

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By Component

- 5.2.1 Software

- 5.2.2 Services

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-Use Industry

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-Commerce

- 5.4.3 Healthcare

- 5.4.4 Banking, Financial Services and Insurance (BFSI)

- 5.4.5 Information Technology and Telecom

- 5.4.6 Education

- 5.4.7 Government and Public Sector

- 5.4.8 Other End-Use Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products AND Services, and Recent Developments)

- 6.4.1 Odoo SA

- 6.4.2 Frappe Technologies Private Limited

- 6.4.3 Axelor SAS

- 6.4.4 Dolibarr Foundation

- 6.4.5 Tryton Foundation

- 6.4.6 iDempiere Association a.s.b.l.

- 6.4.7 Metasfresh AG

- 6.4.8 ADempiere Global Community

- 6.4.9 Openbravo S.L.U.

- 6.4.10 xTuple LLC

- 6.4.11 DSXtreme LLC (BlueSeer ERP)

- 6.4.12 Nexedi SA (ERP5)

- 6.4.13 inoLink International Limited (inoERP)

- 6.4.14 FrontAccounting LLC

- 6.4.15 LedgerSMB Inc.

- 6.4.16 WebERP Project Association

- 6.4.17 OpenPro Inc.

- 6.4.18 The Apache Software Foundation (Apache OFBiz)

- 6.4.19 MixERP Inc.

- 6.4.20 Compiere Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment