|

시장보고서

상품코드

2066647

탄산리튬 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Lithium Carbonate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

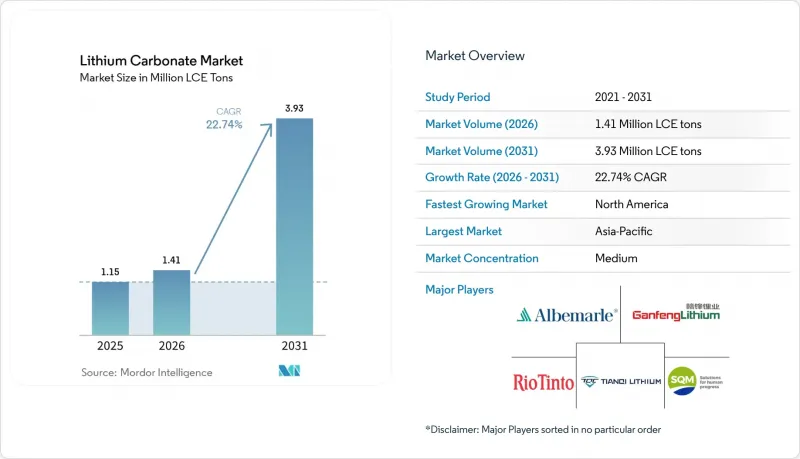

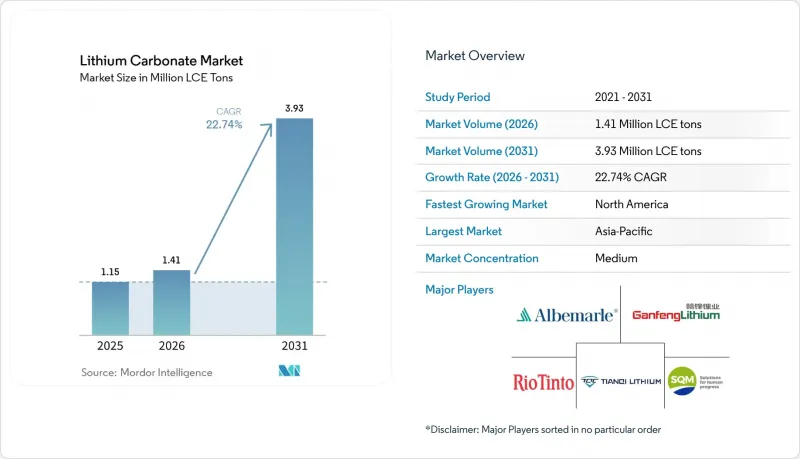

Mordor Intelligence에 의하면, 탄산리튬 시장 규모는 2025년 115만 LCE 톤으로 평가되었습니다. 2026년에는 141만 LCE 톤으로 확대되어 2031년까지 393만 LCE 톤에 이를 것으로 예상되고 2026년부터 2031년에 걸쳐 CAGR 22.74%로 성장할 전망입니다.

본 보고서는 등급(배터리 등급, 테크니컬 등급, 산업용 등급), 원료(염수, 스포듀멘 등), 용도(리튬 이온 배터리, 유리 및 세라믹 등), 최종 사용자 산업(자동차, 소비자용 전자기기 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(LCE 톤)으로 표시되어 있습니다.

세계의 탄산리튬 시장 동향 및 분석

전기자동차 보급 가속화와 배터리 생산 능력 확대

2025년 전 세계 승용 전기자동차 인도 대수는 1,500만 대를 넘어섰으며, 2026년에 발표된 생산 계획에 따라 배터리 셀 생산 능력은 600 GWh 더 증가할 것으로 예측됩니다. 2025년 1월부터 11월까지 중국 내 전기자동차 판매 대수에서 LFP(인산철리튬) 배터리가 차지하는 비중은 80%를 넘어섰으며, 이러한 화학 성분의 편중 현상이 탄산리튬 시장에 대한 추가 수요를 견인하고 있습니다. 포드의 ‘블루 오벌 배터리 파크 미시간’은 2026년 미시간주에서 양산을 시작할 예정이며, 한편, 제너럴 모터스와 삼성SDI는 인디애나주에서 30GWh 규모의 LFP 공장 착공에 들어갔으며, 양사는 공동으로 수년에 걸친 탄산리튬 공급 계약을 체결했습니다. 자동차용 양극재 제조업체의 경우, 현재 장기 조달 계약이 현물 거래를 상회하고 있어 가격 형성에 기여하고 있는 한편, 유동성을 제한하는 요인이 되고 있습니다. 또한, 포드가 리튬 아메리카스의 ‘사커 패스’ 광산과 공급 계약을 체결한 사례에서 볼 수 있듯이, 자동차 제조업체들은 업스트림 자산에 대한 공동 투자도 진행하고 있으며, 이를 통해 원자재 가격 변동 위험을 완화하고 있습니다.

전력 계통의 안정화를 위한 에너지 저장 시스템의 신속한 도입

미국의 유틸리티급 배터리 도입량은 2025년에 57.6GWh에 달하고, 2022년 기준치의 4배가 되었습니다. 프론트 오브 미터(FOM) 공급업체들은 6,000회 이상의 사이클 수명과 kWh당 80-100달러의 가격 책정으로 인해 NMC보다 경제성이 뛰어나기 때문에 인산철 리튬(LFP) 모듈을 선호하여 채택하고 있습니다. 중국의 ‘제15차 5개년 계획’에서는 각 성이 재생에너지 최대 출력의 최소 10%에 해당하는 전력 저장 설비를 설치하도록 요구하고 있으며, 이에 따라 2026년에는 고정형 수요가 150-180 GWh에 달할 것으로 예측됩니다. 분석가들은 에너지 저장 시스템이 2035년까지 전 세계 리튬 소비량의 42%를 차지했으며, 이는 2020년의 8%에서 크게 증가한 수치로, 자동차 업계가 오랫동안 유지해 온 지배적 지위를 영구적으로 약화시킬 것으로 보입니다. 재생에너지와 관련된 다년간의 전력 구매 계약에서는 현재 확실한 저장 용량이 필수 요건으로 자리 잡고 있으며, 개발업체들이 설계·조달·시공(EPC) 계약에 탄산염 공급 조항을 포함시키는 사례가 늘어나고 있어, 사실상 향후 수년 치 원료를 확보하고 있는 실정입니다.

가격 변동과 공급망 혼란

2025년, 중국의 탄산염 현물 가격은 톤당 6만 위안에서 12만 위안 사이에서 거래되었으며, 연간 변동 폭이 100%에 달하면서 제련업체들의 이익률이 압박을 받았습니다. 2026년 초, 호주산 신규 정광이 시장에 유입되면서 선물 가격은 톤당 18만 위안에서 14만 4,000위안으로 조정되었으나, 중견 광산 2곳이 가동을 중단함에 따라 다시 반등했습니다. 이러한 급격한 가격 변동은 계약 구조의 유동성이 여전히 낮은 탓에 헤지 조치를 주저하게 만드는 요인이 되고 있으며, 중소 생산자들을 현금 원가의 손익분기점 이하로 몰아넣어 다음 상승 국면을 더욱 가속화하고 있습니다. 또한, 중국 정책 당국이 2026년부터 신에너지차 구매세 면제를 5% 과세로 대체함에 따라, 2025년 말에 수요가 앞당겨져 집중되었고, 그 후 수요는 바닥을 쳤습니다.

부문별 분석

2025년, 배터리 부문은 리튬 탄산염 시장 점유율의 82.62%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 23.95%로 확대될 것으로 예측됩니다. 순도 99.5%라는 기준에 따라, 덴드라이트 성장을 가속하는 금속 불순물이 최소화되어 셀의 고장률이 낮아지므로, 순도 99.0%의 산업용 등급에 비해 15-20%의 가격 프리미엄이 정당화됩니다. 현재 미국, 한국, 독일의 여러 기가팩토리 운영 기업들은 순도 보증을 ‘테이크 오어 페이(Take-or-Pay)’ 조항에 포함시키고 있으며, 이를 통해 고사양 공급업체를 위한 공급량을 사실상 확보하고 있습니다.

유리, 세라믹, 야금 분야에서 사용되는 산업용 등급 제품의 생산량은 연간 성장률이 한 자릿수 중반에 머물고 있습니다. 건설 수요는 전기자동차 판매 대수보다는 주택 및 인프라의 경기 사이클과 더 밀접한 상관관계가 있으므로, 이 부문은 변동성이 작은 반면 상승 여력도 제한적입니다. 의약품 등급의 탄산리튬은 탄산리튬 시장 규모의 1% 미만을 차지할 뿐이지만, 미국약전(USP) 기준을 준수함으로써 톤당 5만 달러가 넘는 가격을 유지하고 있습니다. 제조업체들은 교차 오염을 방지하기 위해 전용 생산 라인을 운영하는 경우가 많으며, 이로 인해 고정 비용은 높아지지만 틈새 시장에서는 안정적인 이익률을 확보하고 있습니다.

2025년에는 염수 광상이 생산량의 65.22%를 차지했으나, 서호주 및 신흥 북미 거점에서 생산되는 스포쥬움(경암)이 가장 빠르게 성장하는 공급원으로, 2031년까지 연평균 성장률(CAGR) 23.16%를 나타낼 것으로 전망됩니다. 염수 증발 방식의 경우, LCE 1톤당 운영 비용이 3,300-4,900달러이지만, 12-18개월의 연못 주기로는 수요의 급격한 변동에 신속하게 대응할 수 없어 공급의 유연성이 제한됩니다. 경암 농축물은 일반적으로 70-80%라는 높은 회수율을 달성하고 있으며, 새로운 파쇄 라인이 가동되면 6-12개월 이내에 생산량을 확대할 수 있지만, 비용이 3,600-8,000달러 범위인 탓에 광산 회사는 가격 하락의 영향을 받기 쉬운 상황입니다.

점토 및 레피도라이트 광상은 DLE 기술의 비약적인 발전으로 추출 수율이 90%를 넘기 전까지는 경제성이 낮은 상태가 지속되어 왔습니다. 센추리 리튬사의 네바다주 시범 공장에서는 현재 톤당 4,000달러 전후의 운영 비용을 기록하고 있으며, 물 사용량을 대폭 줄이고 있습니다. 현재 재활용 탄산리튬 시장 점유율은 약 3-4%로 추정되지만, 2026년 12월에 유럽연합(EU)이 비OECD 국가에 대한 블랙매스 수출 금지 조치를 시행함에 따라, 2031년까지 탄산리튬 시장 점유율이 10-12%에 달할 가능성이 있습니다.

지역별 분석

2025년, 아시아태평양은 세계 생산량의 79.13%를 차지했으며, 장시성과 쓰촨성에서의 정련부터 광둥성과 절강성에서의 셀 조립에 이르는 중국의 통합된 밸류체인이 이를 뒷받침하고 있습니다. 중국은 스포쥬움 정광의 80%를 호주에서 수입하고 있지만, 해당 지역에 광범위하게 분포해 있는 제련소들 덕분에 부가가치의 대부분은 국내에 남고 있습니다. 2025년에는 현물 가격이 하락하면서 이익률에 압박이 가해졌고, 여러 제련소의 가동률이 70% 아래로 떨어졌습니다. 일본과 한국은 파나소닉, LG 에너지솔루션, 삼성SDI에 공급할 배터리용 탄산염을 수입에 의존하고 있어, 중국의 수출 정책에 영향을 받기 쉬운 상황에 놓여 있습니다.

북미는 2031년까지 연평균 성장률(CAGR) 28.13%를 기록하며 성장을 주도하고 있습니다. IRA(인플레이션 억제법)에 따른 1kWh당 35달러의 셀 세액 공제로 인해, 미시간주, 오하이오주, 테네시주 및 온타리오주의 기가팩토리에게 있어 국내산 탄산리튬은 경제적으로 필수 불가결한 요소가 되었습니다. 연방 정부의 자금 지원에 힘입어 터커 패스, 킹스 마운틴, 피에몬테 리튬의 프로젝트가 실현되었으며, 이 3개사는 2028년까지 연간 총 10만 톤 이상의 생산을 목표로 하고 있습니다. 허가 지연은 여전히 큰 과제이지만, 포드 및 GM과의 구매 계약 덕분에 프로젝트 파이낸싱의 위험이 완화되었습니다.

유럽에서는 정제 및 재활용 인프라를 지원하는 15억 유로 규모의 ‘배터리 부스터 시설’의 혜택을 받고 있습니다. BASF의 슈바르츠하이데 공장과 ACC의 프랑스 사업장은 해당 지역 수요를 뒷받침하고 있습니다. 2026년 12월에 시행될 블랙마스 수출 금지 조치로 인해 재활용 업체들은 생산 능력을 현지화할 수밖에 없게 되며, 그 결과 탄산리튬이 기가팩토리공급망으로 역류하게 될 것입니다.

남미, 특히 칠레와 아르헨티나는 2025년에 해수 기반 생산량의 약 40%를 차지했습니다. 칠레의 40만 톤 할당량이 추가 확대를 제한하고 있지만, SQM사의 21만 톤 규모 ‘살라르 데 아타카마’와 알베마르사의 20만 톤 규모 ‘라 네그라 III’는 이 상한선 범위 내에서 가동되고 있습니다. 아르헨티나의 오랄로스 카우차리, 살 데 비다, 파스토스 그란데스 등 3개 광산의 생산량을 합치면 8만 7,500톤에 달하지만, 인프라 부족과 주 정부의 허가 절차 지연으로 인해 생산 확대 속도가 둔화될 가능성이 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the lithium carbonate market size is expected to increase from 1.15 Million LCE tons in 2025 to 1.41 Million LCE tons in 2026 and reach 3.93 Million LCE tons by 2031, growing at a CAGR of 22.74% over 2026-2031.

This report is Segmented by Grade (Battery Grade, Technical Grade, and Industrial Grade), Source (Brine, Spodumene, and More), Application (Li-Ion Battery, Glass and Ceramics, and More), End-User Industry (Automotive, Consumer Electronics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Volume (LCE Tons).

Global Lithium Carbonate Market Trends and Insights

Accelerating EV adoption and Battery Manufacturing Capacity Expansion

Global passenger-EV deliveries surpassed 15 million units in 2025, and production plans announced in 2026 will lift cell capacity additions by another 600 GWh. China's LFP penetration exceeded 80% of domestic EV sales between January and November 2025, a chemistry tilt that swings incremental demand toward the lithium carbonate market. Ford's BlueOval Battery Park Michigan entered mass production in Michigan during 2026, while General Motors and Samsung SDI broke ground on a 30 GWh LFP plant in Indiana, jointly locking up multi-year carbonate offtake. Long-term procurement contracts now outnumber spot transactions for automotive cathode manufacturers, helping price discovery but limiting liquidity. Automakers are also co-investing in upstream assets, as evidenced by Ford's offtake tie-up with Lithium Americas' Thacker Pass, reducing exposure to commodity swings.

Rapid Deployment of Energy Storage Systems for Grid Stabilization

Utility-scale battery additions in the United States rose to 57.6 GWh in 2025, four times the 2022 baseline. Front-of-meter providers favor lithium iron phosphate (LFP) modules because 6,000-plus cycle life and a USD 80-100 per kWh price point outperform NMC economics. China's 15th Five-Year Plan calls for every province to install storage equal to at least 10% of peak renewable output, elevating stationary demand to a projected 150-180 GWh in 2026. Analysts expect energy-storage systems to consume 42% of global lithium by 2035, up from 8% in 2020, permanently diluting the automotive industry's historical dominance. Multi-year power-purchase agreements for renewables now require firm storage capacity, and developers are increasingly embedding carbonate supply clauses in engineering-procurement-construction contracts, effectively reserving feedstock years ahead.

Price Volatility and Supply Chain Disruptions

Chinese spot carbonate traded between CNY 60,000 and CNY 120,000 per ton in 2025, a 100% intrayear range that squeezed converter margins. Futures corrected from CNY 180,000 per ton to CNY 144,000 per ton in early 2026 as new Australian concentrate cargoes hit the market, only to rebound when two mid-tier mines idled. Such whiplash discourages hedging because contract structures remain illiquid, pushing smaller producers below cash-cost breakeven and amplifying the next upward spike. Policymakers in China also replaced the new-energy-vehicle purchase-tax exemption with a 5% levy in 2026, causing a front-loaded demand rush in late 2025 and a subsequent trough.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives and Domestic Content Requirements Driving Localization

- Technology Innovations in Direct Lithium Extraction and Recycling

- Processing Capacity Bottlenecks and Geographic Concentration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery-grade controlled 82.62% of the lithium carbonate market share in 2025 and is expected to advance at a 23.95% CAGR through 2031. Purity thresholds of 99.5% minimize metal contaminants that catalyze dendrite growth, lowering cell failure rates and justifying a 15-20% price premium over 99.0% industrial grade. Multi-gigafactory operators in the United States, South Korea, and Germany now embed purity guarantees into take-or-pay clauses, effectively ring-fencing volume for high-spec suppliers.

Industrial-grade output, applied in glass, ceramics, and metallurgy, trails at mid-single-digit annual growth. Construction demand correlates with housing and infrastructure cycles rather than EV sales, so the segment experiences less volatility but lower upside. Pharmaceutical-grade carbonate represents under 1% of the lithium carbonate market size yet commands prices above USD 50,000 per ton because of U.S. Pharmacopeia compliance. Producers often maintain dedicated production lines to avoid cross-contamination, creating high fixed costs but steady niche margins.

Brine fields supplied 65.22% of output in 2025, but spodumene (hard-rock) from Western Australia and emerging North American hubs is the fastest-growing source, registering a 23.16% CAGR to 2031. Brine evaporation enjoys operating costs of USD 3,300-4,900 per ton LCE; however, 12-to-18-month pond cycles cannot respond quickly to demand surprises, limiting supply elasticity. Hard-rock concentrate delivers higher recovery rates, typically 70-80%, and can ramp within 6-12 months once a new crusher line is in place, though its USD 3,600-8,000 cost range makes miners sensitive to price dips.

Clay and lepidolite deposits stayed marginal until DLE breakthroughs improved extraction yields beyond 90%. Century Lithium's Nevada pilot now logs operating costs near USD 4,000 per ton and cuts water use dramatically. Recycled carbonate contributes an estimated 3-4% today, but could reach 10-12% of the lithium carbonate market share by 2031 because the European Union's export ban on black mass to non-OECD countries takes effect in December 2026.

Geography Analysis

Asia-Pacific retained 79.13% of global volume in 2025, anchored by China's integrated value chain from refining in Jiangxi and Sichuan to cell assembly in Guangdong and Zhejiang. Although China imports 80% of its spodumene concentrate from Australia, the region's extensive converter park keeps most value addition in-country. Margin pressure emerged in 2025 when spot prices cooled, dropping utilization below 70% in several converters. Japan and South Korea rely on imports of battery-grade carbonate for Panasonic, LG Energy Solution, and Samsung SDI, making them sensitive to Chinese export policy.

North America leads growth with a 28.13% CAGR to 2031. The IRA's USD 35 per kWh cell credit makes domestic carbonate an economic imperative for gigafactories in Michigan, Ohio, Tennessee, and Ontario. Federal loans unlocked Thacker Pass, Kings Mountain, and Piedmont Lithium, collectively targeting over 100,000 tons per year by 2028. Permitting delays remain material, but offtake contracts with Ford and GM de-risk project finance.

Europe benefits from the EUR 1.5 billion Battery Booster Facility supporting refinery and recycling infrastructure. BASF's Schwarzheide plant and ACC's unit in France underpin regional demand. The December 2026 export ban on black mass will compel recyclers to localize capacity, which will back-feed carbonate into gigafactory supply chains.

South America, primarily Chile and Argentina, controlled roughly 40% of brine-based output in 2025. Chile's 400,000 ton quota caps further expansion, while SQM's 210,000 ton Salar de Atacama and Albemarle's 200,000 ton La Negra III operate within that ceiling. Argentina's Olaroz-Cauchari, Sal de Vida, and Pastos Grandes together add 87,500 tons, yet infrastructure gaps and provincial permitting could slow ramp-ups.

- Albemarle Corporation

- Ganfeng Lithium Group Co., Ltd

- Jiangxi Jiuling Lithium Co., Ltd.

- LevertonHELM Limited.

- Lithium Americas Corp.

- Lithium Argentina AG

- Nemaska Lithium

- Pilbara Minerals Limited

- Rio Tinto

- Shandong Ruifu Lithium Co., Ltd.

- Shengxin Lithium Energy Group Co., Ltd.

- SQM

- Tianqi Lithium Corporation

- Xinjiang Zhicun Lithium Industry Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating EV adoption and battery manufacturing capacity expansion

- 4.2.2 Rapid deployment of energy storage systems for grid stabilization

- 4.2.3 Government incentives and domestic content requirements driving localization

- 4.2.4 Battery chemistry transition from NMC to LFP favoring lithium carbonate

- 4.2.5 Technology innovations in direct lithium extraction and recycling

- 4.3 Market Restraints

- 4.3.1 Price volatility and supply chain disruptions

- 4.3.2 Processing capacity bottlenecks and geographic concentration

- 4.3.3 Environmental and water resource constraints in lithium extraction

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Grade

- 5.1.1 Battery Grade

- 5.1.2 Technical Grade

- 5.1.3 Industrial Grade

- 5.2 By Source

- 5.2.1 Brine

- 5.2.2 Spodumene (Hard-rock)

- 5.2.3 Lepidolite/Clay

- 5.2.4 Recycled Lithium Carbonate

- 5.3 By Application

- 5.3.1 Li-ion Battery

- 5.3.2 Glass and Ceramics

- 5.3.3 Pharmaceuticals and Dental

- 5.3.4 Aluminum Production

- 5.3.5 Cement Industry

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Automotive

- 5.4.2 Consumer Electronics

- 5.4.3 Energy Storage Systems

- 5.4.4 Industrial and Metallurgy

- 5.4.5 Healthcare

- 5.4.6 Construction

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Albemarle Corporation

- 6.4.2 Ganfeng Lithium Group Co., Ltd

- 6.4.3 Jiangxi Jiuling Lithium Co., Ltd.

- 6.4.4 LevertonHELM Limited.

- 6.4.5 Lithium Americas Corp.

- 6.4.6 Lithium Argentina AG

- 6.4.7 Nemaska Lithium

- 6.4.8 Pilbara Minerals Limited

- 6.4.9 Rio Tinto

- 6.4.10 Shandong Ruifu Lithium Co., Ltd.

- 6.4.11 Shengxin Lithium Energy Group Co., Ltd.

- 6.4.12 SQM

- 6.4.13 Tianqi Lithium Corporation

- 6.4.14 Xinjiang Zhicun Lithium Industry Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment