|

시장보고서

상품코드

2066742

유럽의 LED 조명 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe LED Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

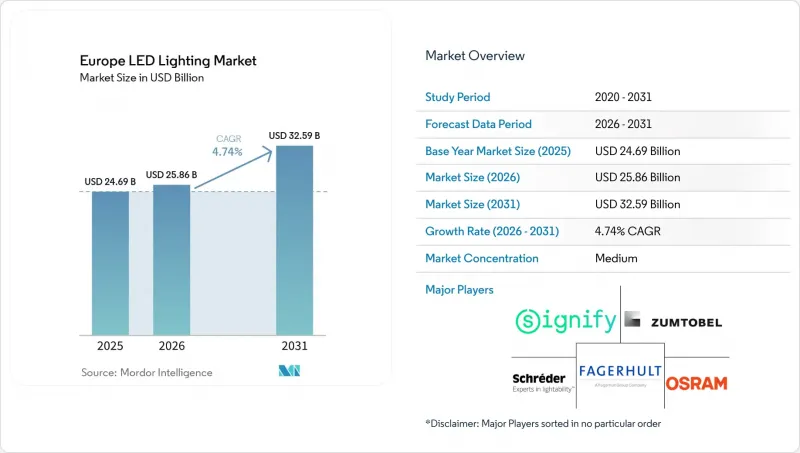

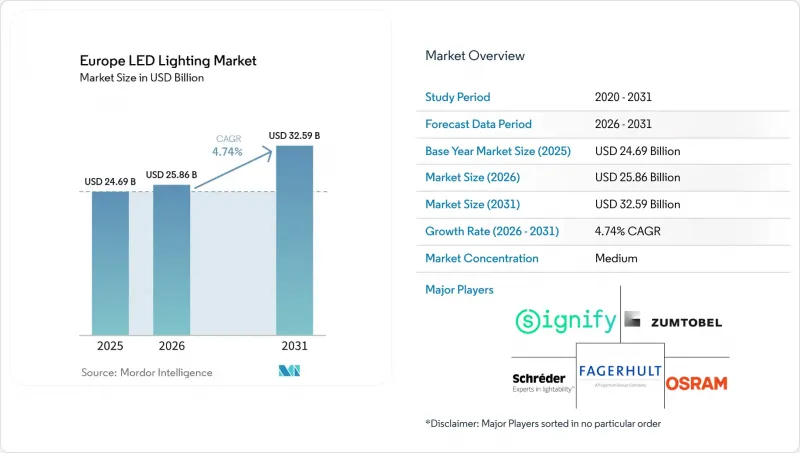

Mordor Intelligence에 의하면, 유럽의 LED 조명 시장 규모는 2025년에 246억 9,000만 달러로 평가되었고, 2026년 258억 6,000만 달러로 추정되고, 2031년까지 325억 9,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 4.74%를 나타낼 것으로 예측됩니다.

본 보고서는 제품 유형별(램프, 조명 기구), 유통 채널별(직접 판매, 도매·소매 등), 설치 유형별(신규 설치, 개보수 설치), 용도별(상업용 사무실, 소매점, 호텔 및 레스토랑, 산업용 등), 최종 사용자별(실내, 실외 등) 및 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 LED 조명 시장 동향 및 인사이트

EU의 엄격한 에너지 효율 규제가 기초 수요를 견인하고 있습니다.

유럽의 LED 조명 시장은 현재 효율성뿐만 아니라 제품 구조, 문서화, 수명 주기 성능에 이르기까지 포괄하는 규제 체계의 혜택을 받고 있습니다. 규정(EU) 2019/2020은 LED 램프의 최소 발광 효율 기준을 정하고 있으며, 보다 최근에 제정된 ‘지속 가능한 제품을 위한 에코디자인 규정’은 규정 준수 의무를 내구성, 수리 가능성 및 재활용 소재 함량 공개까지 확대했습니다. 이로 인해, 특히 EPREL 등록 및 데이터 검증이 지역 전체에서 더욱 강력한 집행 수단으로 자리 잡으면서, 규정 미준수에 따른 비용이 증가하고 있습니다. 유럽연합 집행위원회는 또한 현재의 에코디자인 및 에너지 표시 프로그램을 통해 2023년에 EU의 최종 에너지 소비량을 12% 감축하고, 1억 4,500만 톤의 CO2 배출을 방지하는 동시에 34만 6,000명의 일자리를 지탱했다고 밝혔으며, 이는 정책 지원이 일시적인 것이 아니라 계속해서 견고하게 유지되고 있음을 보여주는 이유입니다. 2026년 이후 ‘디지털 제품 여권’이 새로운 요건으로 추가됨에 따라, 유럽의 LED 조명 시장에서는 엔지니어링, 추적성, 규제 보고를 대규모로 관리할 수 있는 제조업체가 계속해서 우대받게 될 것입니다. 또한, 사양 주도형 프로젝트에서도 프리미엄 브랜드에 대한 지지가 높아지고 있습니다. 이는 플리커나 스트로보 효과에 관한 성능 기준이 강화됨에 따라 조달 단계에서 기술적 품질을 검증하기가 쉬워졌기 때문입니다.

할로겐 램프와 형광등의 급속한 단계적 폐지가 구조적인 대체 수요를 창출하고 있습니다.

유럽의 LED 조명 시장은 2023년 EU가 T5 및 T8 형광등 판매를 금지함에 따라 계속해서 수요를 끌어모으고 있습니다. 이는 교체 시기가 일반적으로 규정이 시행된 시점보다 몇 번의 정비 주기를 뒤따르기 때문입니다. 이러한 시간 차이는 중요한 의미를 지닙니다. 많은 사무실, 소매점, 병원, 공공시설에서는 판매 금지 조치가 시행된 직후 교체하지 않은 구형 설비를 여전히 계속 사용하고 있기 때문입니다. 슬로바키아의 한 병원에서 진행된 개보수 사례에서는 연간 에너지 사용량이 93,728 kWh에서 45,063 kWh로 52% 감소했으며, 연간 비용 절감액은 2만 3,000유로(2만 5,070달러)를 넘어섰습니다. 이로 인해 공공기관 및 기관의 구매 담당자들에게 투자 회수 전망이 명확해졌습니다. 또한, 많은 T8 조명을 LED로 교체하려면 제어 장치를 교체하고 시운전을 실시해야 하므로, 단순히 램프를 교체하는 데 그치지 않고 더 대규모의 교체 주기가 됩니다. 이에 따라 많은 프로젝트가 단순한 기본 유지보수 비용 지출에서 벗어나 네트워크 연결형 개보수로 전환되고 있습니다. 공공 입찰은 이러한 흐름을 더욱 촉진하고 있으며, 폴란드의 셰무드 코뮌(Szemud Commune) 프로젝트가 그 한 예입니다. 이 프로젝트에서는 지자체 현대화 프로그램의 일환으로, 2026년까지 436기의 조명을 LED로 교체하는 계약이 체결되었습니다. 이에 따라 유럽의 LED 조명 시장은 해당 지역의 비주거용 및 공공 인프라 시설에서 아직 완전히 진행되지 않은 교체 흐름에 힘입어 계속해서 성장하고 있습니다.

가격에 민감한 개보수 사업의 투자 회수 기간이 중소기업의 도입을 제약하고 있습니다.

유럽의 LED 조명 시장에서는 여전히 중소기업 간의 도입 격차가 두드러집니다. 이는 완전한 커넥티드 시스템으로의 개편을 위해서는 많은 중소기업이 한 번의 예산 주기 내에서 감당할 수 있는 범위를 초과하는 초기 투자가 필요하기 때문입니다. 아일랜드만 해도 24만 8,000개의 중소기업이 10만 9,000동의 건물을 사용하고 있지만, 2025년 시점에서 철저한 개보수를 실시한 곳은 고작 4%에 불과합니다. 이는 장기적인 효율성 측면의 이점이 분명함에도 불구하고, 소규모 이용자들의 움직임이 얼마나 더딘지를 여실히 보여주고 있습니다. 이러한 제약은 남유럽과 동유럽에서 더욱 두드러집니다. 이러한 지역에서는 전력 가격이 낮고 자본 예산이 빠듯하기 때문에 기본적인 개보수 공사에 대한 단기적인 투자 회수를 기대하기 어렵습니다. 자금 조달 모델은 도움이 되지만, 대부분의 경우 에너지 감사, 신용 심사, 계약 구조가 필요하기 때문에 많은 소규모 사업자들에게는 복잡하고 시간이 많이 소요되는 과정으로 여겨지고 있습니다. Whitecroft Lighting사가 Currys사를 대상으로 실시한 순환형 조명 교체 프로그램은 대규모 사업을 통해 무엇을 달성할 수 있는지를 보여주었습니다. 77개 매장을 리모델링하고 6,500개 이상의 조명 기구를 재사용함으로써 에너지 사용량과 온실가스 배출량을 40% 줄였습니다. 문제는 개인이 운영하는 중소기업의 경우 그러한 구매력을 갖춘 경우가 드물기 때문에 투자 결정이 단기 주기로 이루어지고 자금 사정에 극도로 민감한 상황에서 유럽의 LED 조명 시장이 여전히 일정한 전환 기회를 놓치고 있다는 점입니다.

부문별 분석

2025년, 유럽 LED 조명 시장에서 조명 기구 및 고정 장치는 57.63%의 점유율을 차지했으며, 금액 기준으로 램프를 확실히 앞질렀습니다. 이 리드는 단순한 광원 교체에 그치지 않고, 규정 준수, 제어, 수명 등이 제품 전체 차원에서 평가되는 통합형 조명 기구로의 업그레이드로 전환되고 있음을 반영하고 있습니다. 따라서 유럽의 LED 조명 시장에서는 특히 사양, 설치 시간 및 서류 작성이 모두 중요한 상업 및 공공 프로젝트의 경우, 그 가치의 상당 부분이 완전한 조명 기구 시스템으로 이동하고 있습니다. 츠무토벨사의 모듈식 연속 배열 시스템 ‘TECTON II’는 각 공급업체들이 생산량뿐만 아니라 작업 효율 측면에서도 경쟁하고 있음을 보여주고 있으며, 기존 구성에 비해 설치 시간을 71% 단축할 수 있는 것으로 알려져 있습니다. 도급업체 확보, 규정 준수 관련 서류 절차, 개보수로 인한 가동 중단 시간이 단가와 마찬가지로 조달 결정에 큰 영향을 미치는 경우가 많은 시장에서 이는 중요한 요소가 됩니다.

램프 부문의 규모는 작지만, 2031년까지 연평균 성장률(CAGR) 5.02%를 나타낼 것으로 예측되며, 유럽 LED 조명 시장에서 가장 빠르게 성장하는 제품 카테고리로 자리매김하고 있습니다. 이러한 성장은 사용이 금지된 형광등의 대체 수요와, 공공시설에서 구형 나트륨등 및 기존 조명 기구를 지속적으로 철거하는 지자체 프로그램과 밀접한 관련이 있습니다. 램프 카테고리는 조명 기구 전체를 아직 교체할 필요가 없는 경우나, 사업자가 당분간 설비 투자를 억제하기 위해 단계적인 전환을 희망하는 경우에 여전히 중요한 역할을 하고 있습니다. 또한, 규정(EU) 2019/2020에 따라 내구성 기준은 여전히 높은 수준으로 유지되고 있으며, 루멘 유지율 요건 등이 포함되어 있습니다. 이를 통해 성능이 떨어지는 제품이 배제되고, 공공 부문 조달에서 인증을 받은 공급업체가 지원받고 있습니다. EPREL에 등록된 광원 모델은 50만 유형 이상에 달하며, 유럽의 LED 조명 업계는 여전히 깊이와 활기를 띠고 있지만, 품질 검증은 감독 당국에게는 더 쉬워졌고, 구매자에게도 투명성이 더욱 높아지고 있습니다.

2025년에는 도매 및 소매 부문이 46.12%의 점유율을 차지했으며, 이는 유통망이 여전히 유럽 LED 조명 시장 활동의 상당 부분을 뒷받침하고 있음을 보여줍니다. 전기 기기 도매업체는 제조업체와 여전히 현지 재고 지원 및 기술 지도를 선호하는 도급업체, 설치업체, 유지보수 팀을 연결하는 역할을 수행하고 있기 때문에 여전히 중요한 존재로 남아 있습니다. 또한, 유럽의 LED 조명 시장에서는 대규모 상업시설, 의료시설, 공항, 지자체 프로젝트의 경우, 기성품을 구매하는 일반 소비자가 아닌 시설 관리자, 컨설턴트 또는 건축가가 사양을 결정하기 때문에 직접 판매도 여전히 중요한 위치를 차지하고 있습니다. 이러한 판매 경로가 견조한 모습을 유지하고 있는 이유는 복잡한 프로젝트의 경우 설계 지원, 시운전 관련 자문, 사후 서비스에 대한 책임이 요구되는 반면, 광범위한 온라인 채널에서는 이러한 서비스를 반드시 제공할 수 없기 때문입니다. 그렇긴 하지만, 브랜드 간 제품 데이터 비교가 쉬워짐에 따라 구매 행태는 더욱 투명해지고 표준화가 진행되고 있습니다.

전자상거래는 2031년까지 연평균 성장률(CAGR) 5.45%로 확대될 것으로 예상되며, 채널별 유럽 LED 조명 시장 규모 구성에서 가장 빠르게 성장하는 판매 채널이 될 전망입니다. EPREL의 QR 코드 기반 제품 정보는 구매자가 유통업체의 해석에만 의존하지 않고 성능이나 표시된 데이터를 직접 확인할 수 있게 되었기 때문에 이러한 변화를 뒷받침하고 있습니다. 반면, 온라인 비교가 가능해짐에 따라 네트워크 미연결형 LED 제품은 상품화되기 쉬워졌으며, 기본적인 하드웨어를 주요 경쟁력으로 삼는 공급업체에게는 가격 압박으로 이어질 가능성이 있습니다. 커넥티드 조명 기기의 경우, 설정 및 제어 기능의 통합, 그리고 시운전용 소프트웨어에 대해 판매점의 지원이나 제조업체 주도의 워크플로가 필요한 경우가 많기 때문에 중개자를 완전히 배제하기에는 아직 이릅니다. 디지털 제품 여권(Digital Product Passport) 규제의 도입이 다가옴에 따라, 유럽의 LED 조명 시장은 투명한 디지털 비교를 통해 판매되는 단순한 제품과, 여전히 사양 및 지원에 의존하는 시스템 주도형 제품 사이에서 더욱 명확하게 양극화될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the europe lED lighting market size was valued at USD 24.69 billion in 2025 and is forecasted to grow from USD 25.86 billion in 2026 to USD 32.59 billion by 2031, growing at a CAGR of 4.74% from 2026 to 2031.

This report is Segmented by Product Type (Lamps, and Luminaires/Fixtures), Distribution Channel (Direct Sales, Wholesale/Retail, and More), Installation Type (New Installation, and Retrofit Installation), Application (Commercial Offices, Retail Stores, Hospitality, Industrial, and More), End User (Indoor, Outdoor, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Lighting Market Trends and Insights

Stringent EU Energy-Efficiency Regulations Drive Baseline Demand

The Europe LED lighting market is benefiting from a regulatory framework that now reaches beyond efficiency and into product structure, documentation, and lifecycle performance. Regulation (EU) 2019/2020 set minimum efficacy thresholds for LED lamps, and the newer Ecodesign for Sustainable Products Regulation extended the compliance burden into durability, reparability, and recycled-content disclosure. This has raised the cost of non-compliance, especially as EPREL registration and data validation have become more visible enforcement tools across the region. The European Commission also stated that the current ecodesign and energy-labelling program helped cut final EU energy consumption by 12% in 2023, while avoiding 145 million tonnes of CO2 emissions and supporting 346,000 jobs, which shows why policy support remains firm rather than temporary. The Digital Product Passport will add another layer from 2026 onward, which means the Europe LED lighting market will continue to reward manufacturers that can manage engineering, traceability, and regulatory reporting at scale. Premium brands are also gaining support in specification-led projects because requirements such as stricter flicker and stroboscopic performance have made technical quality easier to verify during procurement.

Rapid Phase-Out of Halogen and Fluorescent Lamps Creates a Structural Replacement Pipeline

The Europe LED lighting market continues to draw demand from the 2023 EU phase-out of T5 and T8 fluorescent tubes because replacement behavior typically trails regulation by several maintenance cycles. That lag matters because many offices, retail sites, hospitals, and municipal facilities are still working through old installed bases that were not replaced immediately after the sales ban. A hospital retrofit in Slovakia showed a 52% reduction in annual energy use, falling from 93,728 kWh to 45,063 kWh, while yearly cost savings exceeded EUR 23,000 (USD 25,070), which keeps the payback case visible for public and institutional buyers. The replacement cycle is also larger than a simple lamp swap because many T8 conversions require control-gear updates and commissioning work, which pushes more projects toward connected retrofits instead of basic maintenance spend. Public tenders continue to reinforce that pipeline, as seen in the Szemud Commune project in Poland, where 436 LED replacements were contracted through 2026 under a municipal modernization program. This keeps the Europe LED lighting market supported by a replacement wave that has not yet fully worked through the region's non-residential and public infrastructure stock.

Price-Sensitive Retrofit Payback Periods Constrain SME Adoption

The Europe LED lighting market still faces a clear adoption gap among smaller businesses because full connected retrofits require higher upfront spending than many SMEs can absorb in one budget cycle. In Ireland alone, 248,000 SMEs occupied 109,000 buildings, yet only 4% had undergone deep retrofitting by 2025, which illustrates how slowly smaller occupiers move even when the long-term efficiency case is positive. This constraint is more visible in Southern and Eastern Europe, where lower electricity prices and tighter capital budgets weaken the near-term return case for basic retrofits. Financing models can help, but they often require energy audits, credit screening, and contract structures that many smaller operators see as complex or time-consuming. Whitecroft Lighting's circular relight program for Currys showed what scale can achieve, refurbishing 77 stores, reusing more than 6,500 luminaires, and reducing energy use and greenhouse gas emissions by 40%. The problem is that individually owned SMEs rarely have that purchasing leverage, so the Europe LED lighting market still loses some conversion volume where investment decisions remain short-cycle and highly cash sensitive.

Other drivers and restraints analyzed in the detailed report include:

- Falling LED Cost Per Lumen Expands The Addressable Market

- Corporate Net-Zero Commitments Accelerate Commercial Retrofits Beyond Minimum Compliance

- Supply-Chain Volatility for Rare-Earth Phosphors Introduces Margin and Availability Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Luminaires and fixtures held 57.63% of the Europe LED lighting market share in 2025, which kept this category firmly ahead of lamps in value terms. This lead reflects the shift from lamp-only replacement toward integrated fixture upgrades, where compliance, controls, and service life are assessed at the full-product level rather than through a simple source swap. The Europe LED lighting market has therefore moved more of its value into complete luminaire systems, especially in commercial and public projects where specification, installation time, and documentation all matter. Zumtobel's TECTON II modular continuous-row system showed how suppliers are competing on labor efficiency as much as on output, with a stated 71% saving in installation time compared with conventional configurations.That matters in a market where contractor availability, compliance paperwork, and retrofit downtime often shape procurement decisions as much as unit cost.

The lamps segment is smaller, but it is still forecasted to grow at a 5.02% CAGR through 2031, which makes it the fastest-moving product category in the Europe LED lighting market. This growth is tied to the replacement of banned fluorescent formats and to municipal programs that continue to remove older sodium and conventional lighting points from public estates. The lamp category remains relevant where full fixture replacement is not yet necessary, or where operators want a staged conversion that limits immediate capital spend. Regulation (EU) 2019/2020 also keeps durability standards high, including lumen-maintenance requirements that screen out weaker products and support certified suppliers in public-sector buying. With more than 500,000 light-source models registered in EPREL, the Europe LED lighting industry remains deep and active, but quality verification has become easier for surveillance authorities and more visible for buyers.

Wholesale and retail held 46.12% share in 2025, which shows that distributor networks still anchor a large part of Europe LED lighting market activity. Electrical wholesalers remain important because they connect manufacturers with contractors, installers, and maintenance teams that still prefer local inventory support and technical guidance. Direct sales also remained important in the Europe LED lighting market, where large commercial, healthcare, airport, and municipal projects are specified by facility managers, consultants, or architects instead of off-the-shelf buyers. Those routes stay resilient because complex projects need design support, commissioning input, and after-sales accountability that broad online channels do not always provide. Even so, purchasing behavior is becoming more transparent and more standardized as product data has become easier to compare across brands.

E-commerce is forecasted to expand at a 5.45% CAGR through 2031, making it the fastest-growing route to market in the Europe LED lighting market size mix by channel. EPREL's QR-based product information has helped this shift because buyers can verify performance and labeling data without relying only on distributor interpretation. The downside is that online comparison makes non-connected LED products easier to commoditize, which can compress pricing for suppliers that compete mainly on basic hardware. Connected luminaires still resist full disintermediation because configuration, controls integration, and commissioning software often require dealer-backed or manufacturer-led workflows. As Digital Product Passport rules move closer, the Europe LED lighting market is likely to sort itself more clearly between simple products that sell on transparent digital comparison and system-led products that still depend on specification and support.

List of Companies Covered in this Report:

- Signify N.V.

- Zumtobel Group AG

- Osram Licht AG (ams-Osram)

- Schreder SA

- Fagerhult Group

- Acuity Brands Lighting Inc.

- Havells Sylvania Europe Ltd.

- Legrand S.A.

- Eaton Corporation plc (Cooper Lighting)

- TRILUX GmbH and Co. KG

- Thorn Lighting Ltd.

- FW Thorpe Plc

- LEDVANCE GmbH

- Helvar Oy Ab

- iGuzzini illuminazione S.p.A.

- Glamox AS

- Cree Lighting Europe S.p.A.

- ITECH LED Lighting

- Hella GmbH and Co. KGaA

- Nichia Europe GmbH

- Siteco GmbH

- Disano Illuminazione S.p.A.

- Tridonic GmbH and Co KG

- Opple Lighting Europe B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent EU Energy-Efficiency Regulations

- 4.2.2 Rapid Phase-Out of Halogen and Fluorescent Lamps

- 4.2.3 Corporate Net-Zero Commitments Accelerating Retrofits

- 4.2.4 Falling LED Cost per Lumen

- 4.2.5 Smart-City Tenders Bundling IoT Sensors

- 4.2.6 On-Site Renewable and DC Micro-Grids Adoption

- 4.3 Market Restraints

- 4.3.1 Price-Sensitive Retrofit Payback Period in SMEs

- 4.3.2 Supply-Chain Volatility for Rare-Earth Phosphors

- 4.3.3 Complexity of EU Eco-design and WEEE Compliance

- 4.3.4 Shortage of Skilled Installers for Connected Lighting

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lamps

- 5.1.2 Luminaires / Fixtures

- 5.2 By Distribution Channel

- 5.2.1 Direct Sales

- 5.2.2 Wholesale / Retail

- 5.2.3 E-Commerce

- 5.3 By Installation Type

- 5.3.1 New Installation

- 5.3.2 Retrofit Installation

- 5.4 By Application

- 5.4.1 Commercial Offices

- 5.4.2 Retail Stores

- 5.4.3 Hospitality

- 5.4.4 Industrial

- 5.4.5 Highway and Roadway

- 5.4.6 Architectural

- 5.4.7 Public Places

- 5.4.8 Hospitals

- 5.4.9 Horticulture Gardens

- 5.4.10 Residential

- 5.4.11 Automotive

- 5.4.12 Other Applications (Chemicals, Oil and Gas, Agriculture)

- 5.5 By End User

- 5.5.1 Indoor

- 5.5.2 Outdoor

- 5.5.3 Automotive

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Sweden

- 5.6.8 Poland

- 5.6.9 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Zumtobel Group AG

- 6.4.3 Osram Licht AG (ams-Osram)

- 6.4.4 Schreder SA

- 6.4.5 Fagerhult Group

- 6.4.6 Acuity Brands Lighting Inc.

- 6.4.7 Havells Sylvania Europe Ltd.

- 6.4.8 Legrand S.A.

- 6.4.9 Eaton Corporation plc (Cooper Lighting)

- 6.4.10 TRILUX GmbH and Co. KG

- 6.4.11 Thorn Lighting Ltd.

- 6.4.12 FW Thorpe Plc

- 6.4.13 LEDVANCE GmbH

- 6.4.14 Helvar Oy Ab

- 6.4.15 iGuzzini illuminazione S.p.A.

- 6.4.16 Glamox AS

- 6.4.17 Cree Lighting Europe S.p.A.

- 6.4.18 ITECH LED Lighting

- 6.4.19 Hella GmbH and Co. KGaA

- 6.4.20 Nichia Europe GmbH

- 6.4.21 Siteco GmbH

- 6.4.22 Disano Illuminazione S.p.A.

- 6.4.23 Tridonic GmbH and Co KG

- 6.4.24 Opple Lighting Europe B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment