|

시장보고서

상품코드

2066753

신경기술 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Neurotechnology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

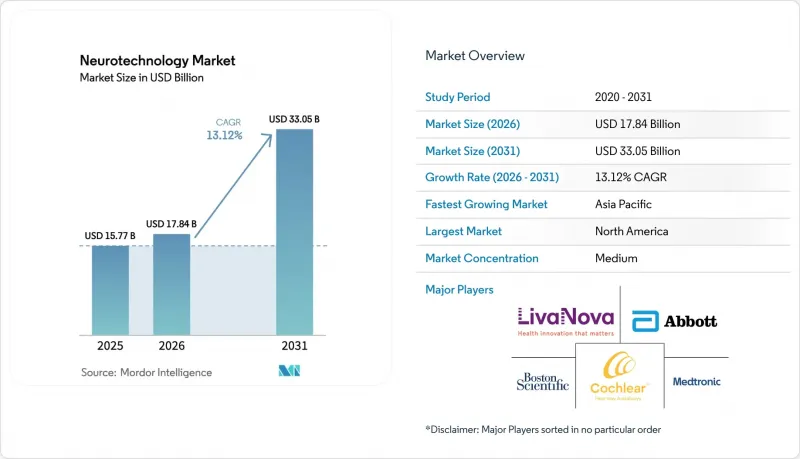

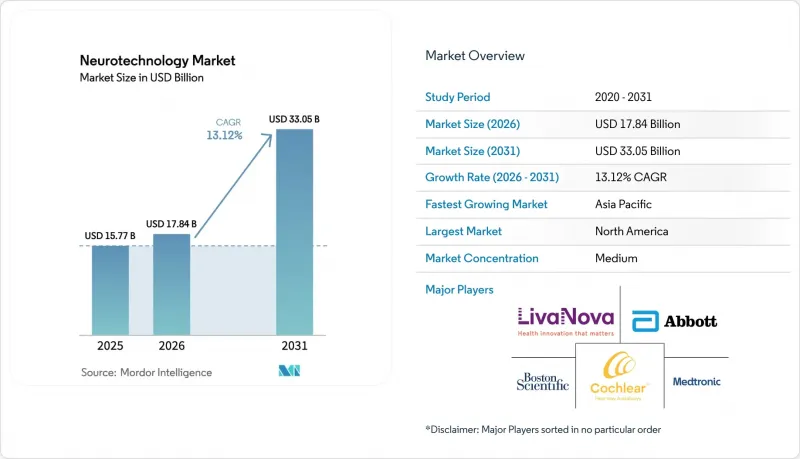

Mordor Intelligence에 의하면, 신경기술 시장 규모는 2025년 157억 7,000만 달러로 평가되었고, 2026년에는 178억 4,000만 달러로 추정되고, 2026-2031년 CAGR 13.12%로 성장을 지속할 전망이며, 2031년에는 330억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품별(신경 자극 장치, 뇌-컴퓨터 인터페이스, 신경 의수·의족, 기타 제품), 용도별(파킨슨병, 간질, 알츠하이머병 및 치매, 만성 통증 관리 등), 최종 사용자별(병원, 전문 클리닉, 재택 간호 환경 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 신경기술 시장 동향 및 인사이트

신경계 질환 유병률 증가

신경퇴행성 질환으로 인한 전 세계 환자 수는 5,000만 명을 넘어섰으며, 고령화에 따라 계속 증가하고 있습니다. 미국에서만 해도 파킨슨병은 매년 고령 인구의 5%-10%에게 영향을 미치고 있으며, 연간 약 50만 명의 신규 환자가 진단받고 있습니다. 의료 시스템 기획 담당자들은 기능 저하의 진행을 늦추고 장기 요양 비용을 절감할 수 있는 조기 개입용 기기에 자금을 투입하고 있습니다. 이러한 인구 통계학적 현실이, 미래의 예방 프로토콜을 염두에 둔 초기 단계의 뇌 모니터링 플랫폼에 대한 적극적인 투자의 배경이 되고 있습니다.

신경과학과 기술의 비약적인 발전

마이크로 스케일 전극 어레이 분야의 획기적인 발전 덕분에, 센서를 모낭 사이에 배치하더라도 장기간 사용 시 96.4%의 신호 감지 정확도를 유지할 수 있게 되었습니다. 또한, 대규모 언어 모델을 활용한 디코딩 기술의 병행적인 발전으로 인해, 대뇌 피질의 신호를 선명한 음성으로 변환할 수 있는 프로토타입이 개발되었습니다. 이러한 혁신은 일반 소비자용 웨어러블 기기와 규제 대상인 의료기기라는 두 영역에 걸쳐 있는 하이브리드 제품 카테고리를 창출하며, 신경기술 시장의 확장을 촉진하고 있습니다.

초기 장비 및 시술 비용이 높아, Tier 1 병원 이외의 곳에서는 도입이 제한됨

첨단 신경 조절 플랫폼의 비용은 10만 달러를 초과할 수 있으며, 환자 1인당 2만-5만 달러의 이식형 부품 비용이 추가로 발생합니다. 이러한 지출로 인해 도입이 학술 기관으로만 국한되어, 지역 의료 현장에의 확산이 저해되고 있습니다. 보험 적용 범위는 지역에 따라 차이가 있어, 본인 부담금을 늘리고, 자원이 제한된 시장에서 보급을 저해하고 있습니다. 각 제조업체들은 위험 분담형이나 성과 연동형 계약을 시범적으로 도입하고 있지만, 이러한 체계는 아직 형성 단계에 있습니다.

부문별 분석

북미는 성숙한 임상 인프라, 활발한 벤처 캐피털, 그리고 가속화되고 있는 FDA의 ‘브레이크스루 디바이스’ 프로그램을 배경으로, 2025년에는 전 세계 매출의 39.10%를 차지했습니다. 파킨슨병 환자를 위한 세계 최초의 적응형 심부 뇌 자극 시스템의 승인 등은 규제 당국이 혁신적인 해결책을 신속하게 승인하겠다는 의지를 보여주고 있습니다. 병원 시스템과 기술 기업 간의 전략적 제휴가 급증하고 있어, 신경 데이터를 기반으로 한 디지털 치료법의 신속한 검증이 가능해졌습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR)이 14.94%에 달할 전망이며, 뉴로테크놀로지 시장에서 가장 빠르게 성장하고 있는 지역입니다. 중국의 국가 BCI 전략은 학술 연구소와 반도체 제조업체를 연결하는 분야 간 컨소시엄을 촉진했으며, 그 결과 100밀리초 미만의 지연 시간으로 중국어 실시간 해독이 가능해졌습니다. 정부의 자금 지원, 제조의 민첩성, 그리고 국내의 방대한 환자층 덕분에 제품 개발 주기가 단축되고 있습니다. 일본과 한국에서는 센서 소형화에 관한 전문 지식을 활용한 병행 혁신이 진행되고 있으며, 수출이 가능한 비침습형 신경 모니터링 기기가 개발되고 있습니다.

유럽에서는 엄격한 규제 감독이 유지되고 있지만, 장기적인 안전성 데이터에 중점을 두는 것이 운동 장애에 대한 선구적인 신경 조절 프로토콜의 개발을 촉진하고 있습니다. 영국의 국민보건서비스(NHS)는 800만 달러 규모의 프레임워크에 따라 기분 조절을 목적으로 하는 초음파 기반 BCI에 대한 임상시험을 진행하고 있습니다. 각국의 보험 급여 기관들은 성과 기준치가 충족될 경우 보다 광범위한 도입으로 이어질 가능성이 있는 비용 대비 효과 모델을 적극적으로 평가했습니다.

지역별 분석

2025년, 신경 자극 장치는 신경기술 시장의 45.21%를 차지했으며, 수십 년에 걸친 임상 경험과 확립된 보험 급여 제도의 유효성이 입증되었습니다. 적응형 알고리즘이 자극 매개변수를 실시간으로 미세 조정하여, 내성이나 부작용을 줄여줌에 따라 도입이 계속해서 증가하고 있습니다. 메드트로닉사의 ‘Inceptiv’ 시스템은 1초에 50회씩 신체의 반응을 감지하여 치료 임계치를 유지합니다. 이러한 감지 및 자극 기술의 융합으로 인해, 임플란트형 시스템과 관련된 신경기술 시장 규모는 10%대 중반의 꾸준한 성장세를 보이고 있습니다.

뇌-컴퓨터 인터페이스(BCI)는 저침습 전극 설계와 클라우드 기반 디코딩 기술의 발전에 힘입어 더욱 빠르게 확산되고 있습니다. 이 부문의 예상 연평균 성장률(CAGR)은 15.98%에 달하며, 신경기술 시장에서 가장 빠르게 성장하는 분야로 부상하면서 의료기기 제조업체와 소비자용 전자기기 주요 기업간의 제휴를 촉진하고 있습니다. 혼합현실(MR) 헤드셋과의 통합은 주류 건강 모니터링 분야로 확대될 가능성을 시사하며, 임상 신경학의 범위를 넘어선 새로운 수익 채널을 창출하고 있습니다. 하드웨어, 펌웨어, 데이터 분석 분야의 지적 재산(IP)을 공유하고 반복 주기를 가속화하는 공동 개발 체계도 등장하고 있습니다.

만성 통증 관리는 뉴로테크놀로지 시장 규모에서 가장 큰 비중을 차지하고 있으며, 2025년 매출의 40.05%를 차지하고 있습니다. 폐쇄 루프 방식의 척수 자극 시스템은 통증 완화 지속 시간을 연장하여, 많은 환자가 오피오이드에 의존하지 않고 직장으로 복귀할 수 있게 해줍니다. 보험사는 중독 발생률 하락 및 입원 건수 감소와 같은 하류 비용 절감을 보험 적용을 정당화하는 근거로 간주하고 있으며, 이를 통해 해당 부문의 수익 기반이 유지되고 있습니다.

우울증 및 더 광범위한 신경정신과 적응증 시장은 외래 진료 환경에서 시행 가능한 비침습적 신경 자극 요법의 확산에 힘입어 2031년까지 연평균 15.07%의 성장률을 보이고 있습니다. 무작위 배정 임상시험에서 전두엽과 소뇌에 대한 경두개 펄스 전류 자극은 자폐 스펙트럼 장애를 가진 소아의 사회적 기능을 개선하는 데 기여했습니다. 정신과용 의료기기에 대한 규제 움직임이 거세지고 있으며, 현재 진행 중인 연구에서는 투여 프로토콜의 표준화를 목표로 하고 있어, 이를 통해 대상 환자층이 더욱 확대될 전망입니다.

이 병원은 의료기기 이식, 프로그래밍 및 급성기 모니터링 분야의 전문 지식을 바탕으로 2025년 매출의 65.79%를 계속 차지하고 있습니다. 주요 학술 의료 센터에서는 신경내과, 정신과, 재활의학을 통합한 진료팀을 활용하여 치료 성과를 최적화하고 있습니다. 그러나 비용 압박과 인력 부족으로 인해 의료 제공업체들은 적절한 사후 관리를 외래 진료 환경으로 전환하고 있습니다.

재택 간호 환경에서는 소형이며 네트워크에 연결된 신경기술 기기의 등장으로 대면 방문 없이도 임상의의 감독이 가능해졌으며, 연평균 성장률(CAGR)은 14.02%로 성장을 지속하고 있습니다. 고령 환자의 경우, 가족 간병인이 동석해 있을 때 원격 모니터링을 받아들이려는 의향이 높아지고 있습니다. BCI와 기능적 전기 자극을 결합한 원격 재활 플랫폼은 뇌졸중 환자에서 80% 이상의 참여율과 88%에 가까운 지속율을 보이고 있습니다. 이러한 결과는 분산형 신경 치료 모델을 뒷받침하는 증거가 축적되고 있음을 입증하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.30According to Mordor Intelligence, the neurotechnology market size is expected to grow from USD 15.77 billion in 2025 to USD 17.84 billion in 2026 and is forecast to reach USD 33.05 billion by 2031 at 13.12% CAGR over 2026-2031.

This report is Segmented by Product (Neurostimulation Devices, Brain-Computer Interfaces, Neuro-Prosthetics, Other Products), Application (Parkinson's Disease, Epilepsy, Alzheimer's and Dementia, Chronic Pain Management, and More), End User (Hospitals, Specialty Clinics, Home-Care Settings and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Neurotechnology Market Trends and Insights

Rising Prevalence of Neurological Disorders

The global burden of neurodegenerative diseases has surpassed 50 million cases and continues to climb in tandem with aging populations. In the United States alone, Parkinson's disease affects 5%-10% of the geriatric population each year, with roughly 500,000 new diagnoses annually. Health-system planners are moving capital toward early-intervention devices that can slow functional decline and lessen long-term care costs. This demographic reality underpins aggressive investment in early-stage brain-monitoring platforms positioned for future preventive protocols.

Surging Advancements in Neuroscience and Technology

Breakthroughs in microscale electrode arrays now allow sensors to sit between hair follicles while maintaining 96.4% signal-detection accuracy over prolonged use. Parallel gains in large-language-model-powered decoding have yielded prototypes capable of translating cortical signals into coherent speech. These innovations are widening the neurotechnology market by creating hybrid product classes that straddle consumer wearables and regulated medical devices.

High Up-front Device & Procedure Costs Limiting Adoption Beyond Tier-1 Hospitals

Advanced neuromodulation platforms may cost more than USD 100,000, with implantable components adding USD 20,000-50,000 per patient. This expenditure confines deployments to academic centers and limits penetration in community settings. Insurance coverage is uneven, amplifying out-of-pocket burdens and dampening uptake in resource-constrained markets. Manufacturers are piloting risk-sharing and outcomes-based contracts, but these frameworks remain in formative stages.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Improved Treatment Options

- Rising Public & Private Funding for Neurotechnology R&D and Commercialization

- Complex, Multiregional Regulatory Approvals Delaying Market Entry

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

North America generated 39.10% of global revenue in 2025 on the strength of a mature clinical infrastructure, active venture capital, and an accelerating FDA Breakthrough Devices program. Approvals such as the world's first adaptive deep-brain stimulation system for Parkinson's patients illustrate regulators' willingness to fast-track transformative solutions. Strategic alliances linking hospital systems with technology firms are proliferating, enabling rapid validation of neural-data-driven digital therapeutics.

Asia-Pacific is the neurotechnology market's fastest-growing region at a 14.94% CAGR through 2031. China's national BCI strategy has catalyzed cross-sector consortia that pair academic labs with semiconductor manufacturers, resulting in real-time decoding of Chinese speech at sub-100-millisecond latency. Government funding, manufacturing agility, and large domestic patient pools are shortening product-development cycles. Parallel innovation in Japan and South Korea, leveraging sensor miniaturization expertise, is producing export-ready non-invasive neuro-monitoring devices.

Europe maintains stringent regulatory oversight, but its emphasis on long-term safety data has fostered pioneering neuromodulation protocols for movement disorders. The United Kingdom's National Health Service is trialing an ultrasound-enabled BCI for mood modulation under an USD 8 million value-based framework. National reimbursement agencies are actively evaluating cost-effectiveness models that could unlock broader adoption once outcome thresholds are met.

Geography Analysis

Neuro-stimulation devices held 45.21% of the neurotechnology market in 2025, validating decades of clinical experience and established reimbursement. Adoption continues to rise as adaptive algorithms refine stimulation parameters in real time, reducing habituation and side-effects. Medtronic's Inceptiv system senses bodily responses 50 times per second to maintain therapeutic thresholds. This convergence of sensing and stimulation is nudging the neurotechnology market size associated with implantable systems toward steady mid-teens expansion.

Brain-computer interfaces (BCIs) are scaling faster, supported by advances in minimally invasive electrode design and cloud-based decoding. The segment's 15.98% projected CAGR makes it the neurotechnology market's fastest mover, attracting partnerships between medical device firms and consumer electronics leaders. Integration with mixed-reality headsets signals potential spill-over into mainstream health monitoring, providing fresh revenue channels beyond clinical neurology. Co-development frameworks are emerging in which hardware, firmware, and data-analytics IP are shared to accelerate iteration cycles.

Chronic pain management commands the largest slice of the neurotechnology market size, accounting for 40.05% of 2025 revenue. Closed-loop spinal-cord systems extend pain relief durability and have allowed many patients to return to work without opioid reliance. Payers view the reduced downstream costs-lower addiction rates and fewer hospitalizations-as justification for coverage, safeguarding the segment's revenue base.

Depression and broader neuro-psychiatric indications are growing at 15.07% through 2031, catalyzed by non-invasive neuro-stimulation modalities that can be administered in outpatient settings. Prefrontal-cerebellar transcranial pulsed-current stimulation improved social functioning in children with autism spectrum disorder during randomized trials. Regulatory momentum is building for psychiatric devices, and ongoing studies aim to formalize dosing protocols, further broadening the addressable population.

Hospitals retained 65.79% of 2025 revenue owing to their expertise in device implantation, programming, and acute monitoring. Leading academic centers leverage integrated care teams that combine neurology, psychiatry, and rehabilitation to optimize outcomes. However, cost pressures and staffing constraints are motivating providers to shift appropriate follow-up to outpatient settings.

Home-care environments exhibit a 14.02% CAGR as compact, connected neurotechnology devices enable clinician oversight without requiring in-person visits. Elderly patients show a rising willingness to adopt remote monitoring when family caregivers are present. Telerehabilitation platforms that pair BCIs with functional electrical stimulation have demonstrated recruitment rates above 80% and retention rates near 88% in stroke populations. These results underscore a growing evidence base supporting decentralized neurological care models.

- Medtronic

- Abbott Laboratories

- Boston Scientific

- LivaNova

- Cochlear

- Nevro

- NeuroPace

- Neuronetics

- Curonix LLC

- Aleva Neurotherapeutics

- Synapse Biomedical

- Synchron

- Blackrock Neurotech LLC

- Paradromics Inc.

- g.tec medical engineering GmbH Austria

- MindMaze SA

- Kernel

- BrainCo Inc.

- Sonova

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Neurological Disorders

- 4.2.2 Surging Advancements in Neuroscience and Technology

- 4.2.3 Growing Demand for Improved Treatment Options

- 4.2.4 Rising Public & Private Funding for Neurotechnology R&D and Commercialisation

- 4.2.5 Shift Toward Minimally & Non-invasive Neuro-interventions Enhancing Patient Acceptance

- 4.2.6 Emergence of Consumer Neurotechnology

- 4.3 Market Restraints

- 4.3.1 High Up-front Device & Procedure Costs Limiting Adoption Beyond Tier-1 Hospitals

- 4.3.2 Complex, Multiregional Regulatory Approvals Delaying Market Entry

- 4.3.3 Reimbursement Gaps & Limited Skilled Workforce in Emerging Economies

- 4.3.4 Limited Clinical Evidence and Long-Term Data

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Neuro-stimulation Devices

- 5.1.1.1 Deep Brain Stimulation (DBS)

- 5.1.1.2 Spinal Cord Stimulation (SCS)

- 5.1.1.3 Vagus Nerve Stimulation (VNS)

- 5.1.1.4 Sacral Nerve Stimulation (SNS)

- 5.1.1.5 Transcranial Magnetic Stimulation (TMS)

- 5.1.1.6 Others

- 5.1.2 Brain-Computer Interfaces

- 5.1.2.1 Invasive BCI

- 5.1.2.2 Semi-invasive BCI

- 5.1.2.3 Non-invasive BCI

- 5.1.3 Neuro-prosthetics

- 5.1.3.1 Output Neural Prosthetics

- 5.1.3.2 Input Neural Prosthetics

- 5.1.4 Other Products

- 5.1.1 Neuro-stimulation Devices

- 5.2 By Application

- 5.2.1 Parkinson's Disease

- 5.2.2 Epilepsy

- 5.2.3 Alzheimer's and Dementia

- 5.2.4 Chronic Pain Management

- 5.2.5 Stroke and Motor Rehabilitation

- 5.2.6 Depression and Other Neuro-psychiatric Disorders

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Clinics

- 5.3.3 Home-care Settings

- 5.3.4 Research and Academic Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Medtronic PLC

- 6.3.2 Abbott Laboratories

- 6.3.3 Boston Scientific Corporation

- 6.3.4 LivaNova PLC

- 6.3.5 Cochlear Limited

- 6.3.6 Nevro Corp.

- 6.3.7 NeuroPace Inc.

- 6.3.8 Neuronetics Inc.

- 6.3.9 Curonix LLC

- 6.3.10 Aleva Neurotherapeutics

- 6.3.11 Synapse Biomedical Inc.

- 6.3.12 Synchron Inc.

- 6.3.13 Blackrock Neurotech LLC

- 6.3.14 Paradromics Inc.

- 6.3.15 g.tec medical engineering GmbH Austria

- 6.3.16 MindMaze SA

- 6.3.17 Kernel

- 6.3.18 BrainCo Inc.

- 6.3.19 Sonova

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment