|

시장보고서

상품코드

2072469

신경조절 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Neuromodulation - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

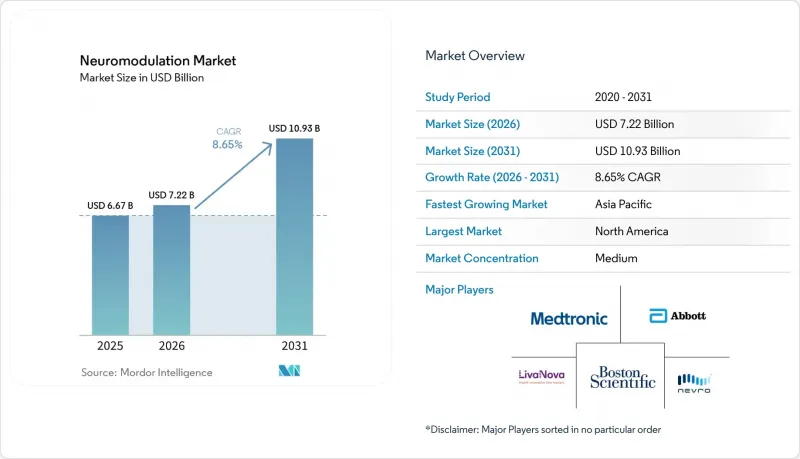

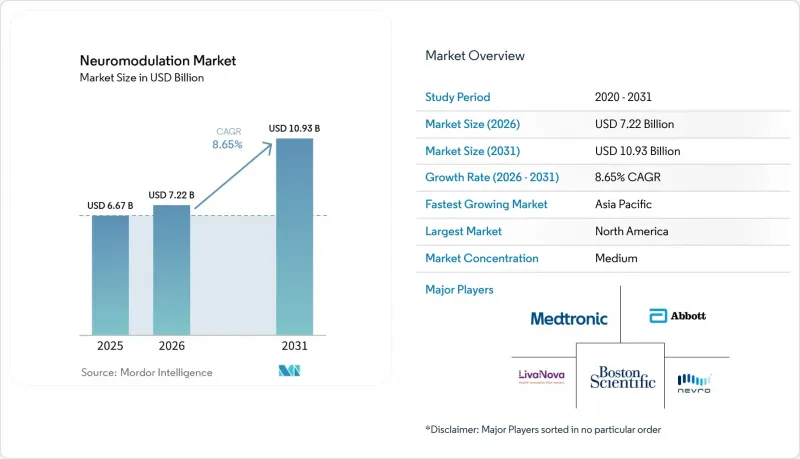

Mordor Intelligence에 의하면, 신경조절 시장 규모는 2025년 66억 7,000만 달러로 평가되었습니다. 2026년 72억 2,000만 달러에서 2031년까지 109억 3,000만 달러로 확대되며 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.65%를 나타낼 전망입니다.

본 보고서는 기술별(체내 신경조절 및 체외 신경조절), 용도별(통증 관리, 파킨슨병 등), 최종 사용자별(병원 및 외래수술센터(ASC) 등), 지역별(북미, 유럽, 아시아태평양, 중동 및 아프리카, 남미)로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 신경조절 시장 동향 및 인사이트

전 세계적으로 증가하는 만성 통증 및 신경 질환의 부담

만성 통증으로 고통받는 사람은 15억 명에 달하며, 그중 약물 내성 사례는 최대 30%를 차지하고 있어 지속적인 치료 수요가 확립되어 있습니다. 신경병성 통증 및 편두통으로 인한 장애 조정 생명 연수(DALY)는 2020년부터 2024년 사이에 12% 증가했는데, 그 원인 중 하나로 코로나19 이후 발생한 신경병증이 꼽힙니다. 아시아 전역에서 인구 고령화가 진행되는 가운데, 레보도파에 대한 접근성이 고르지 않은 지역에서는 파킨슨병 유병률이 2040년까지 2배인 1,700만 명에 달할 가능성이 있습니다. 전 세계 5,000만 명의 간질 환자 중 30%는 여전히 난치성입니다. 2024년 FDA가 청소년을 대상으로 한 반응형 신경 자극 요법을 승인함에 따라, 미국 내 적응증 대상자가 약 20만 명 증가했습니다. 의료 제도가 포괄지급제로 전환되는 가운데, 5년 이내에 약제비나 응급진료비와 같은 경상 비용을 상쇄할 수 있는 의료기기에 대한 일회성 지출에 대한 관심이 높아지고 있습니다.

폐루프 및 고주파 자극 기술의 지속적인 발전

2024년에 메드트로닉사의 "Percept RC" FDA의 승인을 받음에 따라, 적응형 심부 뇌 자극 요법이 도입되었습니다. 이 치료법은 실시간 베타파 대역 바이오마커를 바탕으로 치료 강도를 미세 조정하여, 파킨슨병 환자의 하루당 '오프' 시간을 2.6시간 단축했습니다. Nevro사가 선구적으로 개발하고, 애보트사와 보스턴 사이언티픽사가 채택한 10킬로헤르츠 척수 자극 요법은 감각 이상을 피할 수 있었으며, 수술 후 요통 증후군에 대한 임상시험에서 70%의 반응률을 달성했습니다. 뉴로스 메디컬사의 고주파 말초 치료 기기는 2024년에 환지통에 대한 승인을 획득했으며, 당뇨병성 신경병증 치료 분야에서 더욱 폭넓게 활용될 것으로 기대되고 있습니다. 이러한 혁신으로 인해 제품의 수명 주기가 단축되면서, 제조업체들은 무선으로 소프트웨어 업그레이드가 가능한 모듈식 하드웨어로 전환해야 하는 상황에 직면해 있습니다.

임베디드 시스템의 높은 초기 비용과 유지비

이식형 자극 장치의 가격은 2만-5만 달러에 달하며, 이는 대부분의 국가에서 1인당 연간 총 의료비를 웃도는 수준입니다. 충전식 배터리가 아닌 일반 배터리를 교체하는 데는 3-5년마다 8,000-1만 2,000달러의 비용이 들며, 2-5%의 감염 위험이 따릅니다. 2020년 이후, 메디케어의 진단 관련 정액 지급이 병원의 이익률을 압박하고 있는 반면, 중국에서는 DBS 기기 비용의 70%만 환급되어 환자의 본인 부담금이 상당한 수준에 달하고 있습니다. 각 제조업체들은 더 저렴한 '가치' 시스템에서 이에 대응하고 있지만, 이익률 하락으로 인해 차세대 기능 개발이 지연될 가능성이 있습니다.

부문별 분석

2025년, 신경 조절 시장의 70.12%를 이식형 플랫폼이 차지했습니다. 이는 척수 및 뇌 심부 치료에 대한 수십 년에 걸친 연구 결과를 바탕으로 한 것입니다. 메드트로닉사의 센싱 기능을 탑재한 "Percept RC"는 개방 루프 방식의 기존 기종과 비교했을 때, 증상의 '오프' 소요 기간을 최대 30% 단축합니다. 애보트사의 "Eterna" 이 발전기는 10년간 사용할 수 있는 충전식 배터리를 채택하여, 잦은 충전에 대한 환자의 우려를 덜어줍니다. 후근 신경절 시스템은 2024년 미국에서 전국적인 보험 적용이 승인된 것을 계기로 탄력을 받으며, 메디케어 수급자의 통증 관리 선택지를 넓혀가고 있습니다.

가정용 사용 승인 및 웰니스 제품의 소비자 확산을 배경으로, 체외·비침습적 치료법은 2031년까지 연평균 성장률(CAGR) 10.23%를 나타낼 것으로 전망됩니다. 뉴로발렌스사는 수술 없이도 의사 수준의 치료를 제공하는 500달러짜리 전정 신경용 헤드셋을 출시했습니다. FDA는 2024년에 가정용 경두개 자기 자극기를 승인함으로써, 36회의 외래 치료라는 접근성 장벽을 낮췄습니다. 증거에 대해서는 여전히 찬반이 엇갈리고 있지만(코크란 리뷰에 따르면, 경피적 전기 신경 자극 장치를 통한 통증 완화 효과는 미미한 것으로 나타났습니다), 이 장치를 원격 의료 지침과 병행함으로써 치료 순응도와 치료 성과가 향상되고 있습니다.

지역별 분석

북미는 2025년 매출의 45.21%를 차지했습니다. 이는 확립된 상환 경로, 집중된 임상시험 인프라, 그리고 획기적인 의료기기에 대해 단일군 데이터를 인정하는 FDA의 프로그램에 힘입은 결과입니다. CMS(미국 의료보험 및 의료서비스 센터)가 후근 신경절 자극 요법에 대해 내린 전국적인 결정에 따라, 약 4만 명의 메디케어 가입자에 대해 즉시 보험 적용이 시작된 한편, 민간 보험사들도 오피오이드 사용 장애 진단이 확인된 환자에 대한 사전 승인 요건을 철폐했습니다. 캐나다는 NeuroPace를 보조 기기 목록에 추가했으며, 2027년까지 이식 건수가 두 자릿수 성장할 것으로 전망됩니다.

유럽은 독일, 영국, 프랑스를 필두로 전 세계 매출의 약 3분의 1을 차지했습니다. EU의 MDR 규정에 따라 의료기기 승인 절차가 장기화되고 있는 상황에서도, 독일의 폐쇄형 DBS에 대한 등록부 연계형 자금 지원 모델은 가치 기반의 도입 사례로 주목받고 있습니다. 2024년, NICE(영국 국립의료기술평가기구)의 지침은 허용 범위 내에서의 척수 자극 요법의 비용 대비 효과를 인정함으로써, 이를 척추 수술 후 증후군에 대한 표준 치료법으로 확고히 자리매김하게 했습니다. 남유럽 및 동유럽에서의 보급은 예산 및 인력 부족으로 인해 여전히 제한적인 상황입니다.

아시아태평양은 가장 빠르게 성장하고 있으며, 2031년까지의 연평균 성장률(CAGR)은 9.90%로 예측됩니다. 중국은 2024년에 메드트로닉사의 폐쇄형 루프 DBS를 승인했으나, 환자 부담금이 30%에 달하기 때문에 이식 수술은 여전히 경제적으로 여유가 있는 도시 지역으로 한정되어 있습니다. 일본에서는 보스턴 사이언티피크사의 최신 DBS 플랫폼이 승인되었으나, 가격 상한선이 미국 수준보다 20% 낮게 설정되어 있어 이러한 가격 차이가 고급 제품의 출시를 저해하고 있습니다. 인도에서는 민간 보험의 보급률이 여전히 낮은 탓에, 2024년 척수 자극기 이식 건수는 500건 미만에 그쳤습니다.

중동 및 아프리카와 남미를 합친 2025년 매출액은 7% 미만에 그쳤으나, 일부 지역에 수요가 집중되는 현상이 나타났습니다. 아랍에미리트(UAE)는 척수 자극 요법을 필수 보장 목록에 추가했으며, 브라질의 민간 보험사는 남유럽과 동등한 수준으로 신경 조절 요법 비용을 보상하고 있지만, 공적 의료 제도를 통한 접근성은 여전히 제한적입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the neuromodulation market size is projected to expand from USD 6.67 billion in 2025 and USD 7.22 billion in 2026 to USD 10.93 billion by 2031, registering a CAGR of 8.65% between 2026 to 2031.

This report is Segmented by Technology (Internal Neuromodulation and External Neuromodulation), Application (Pain Management, Parkinson's Disease, and More), End-User (Hospitals & Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Neuromodulation Market Trends and Insights

Rising Global Burden of Chronic Pain and Neurological Disorders

Chronic pain affects 1.5 billion people, and drug-resistant cases represent up to 30%, establishing a durable treatment pool. Disability-adjusted life years attributable to neuropathic pain and migraine climbed 12% between 2020 and 2024, partly from post-COVID neuropathies. Parkinson's prevalence could double to 17 million by 2040 as populations age across Asia, where access to levodopa is uneven. Epilepsy remains refractory in 30% of 50 million global patients; 2024 FDA clearance of responsive neurostimulation for adolescents widened the U.S. eligible pool by roughly 200,000 candidates. Health-system moves toward bundled payments heighten interest in one-time device expenditures that offset recurring costs of drugs and emergency visits within five years.

Continuous Advancements in Closed-Loop and High-Frequency Stimulation Technologies

FDA clearance of Medtronic's Percept RC in 2024 introduced adaptive deep brain stimulation, which titrates therapy against real-time beta-band biomarkers, reducing daily "off" time by 2.6 hours in Parkinson's patients. Ten-kilohertz spinal cord stimulation, pioneered by Nevro and adopted by Abbott and Boston Scientific, avoids paresthesia and delivers 70% responder rates in failed-back-surgery syndrome trials. Neuros Medical's high-frequency peripheral device received 2024 clearance for phantom-limb pain, signaling broader use in diabetic neuropathy. Such innovations shorten product life cycles and push manufacturers toward modular hardware capable of software upgrades over the air.

High Capital and Maintenance Costs of Implantable Systems

Implantable stimulators range from USD 20,000 to USD 50,000, outpacing total annual per-capita health spending in most countries. Non-rechargeable battery replacements add USD 8,000-12,000 every 3-5 years and carry 2-5% infection risk[1]. Medicare's flat diagnosis-related payments since 2020 have squeezed hospital margins, while China reimburses only 70% of the DBS device cost, leaving sizable co-pays. Manufacturers are responding with lower-priced "value" systems; however, thinner margins may slow the development of next-generation features.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Approved Clinical Indications and Reimbursement Coverage

- Increasing Investments, M&A Activity, and Strategic Partnerships

- Stringent and Divergent Global Regulatory Approval Requirements

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Internal platforms accounted for a 70.12% neuromodulation market share in 2025, supported by decades of evidence in spinal cord and deep brain applications. Medtronic's sensing-enabled Percept RC shortens symptom "off" periods by up to 30% compared with open-loop predecessors. Abbott's Eterna generator utilizes a 10-year rechargeable cell, alleviating patient concerns about frequent recharges. Dorsal root ganglion systems gained momentum after U.S. national coverage in 2024, broadening pain-care options for Medicare beneficiaries.

External, non-invasive modalities are projected to post a 10.23% CAGR through 2031, driven by home-use clearances and consumer adoption of wellness products. Neurovalens launched a USD 500 vestibular-nerve headset that delivers physician-grade therapy without the need for surgery. FDA cleared at-home transcranial magnetic stimulators in 2024, reducing the access hurdle posed by 36-session clinic regimens. Evidence remains mixed - Cochrane reviews show only modest pain reduction for transcutaneous electrical nerve stimulators - but bundling devices with telehealth coaching is improving adherence and outcomes[3].

Complete Report Scope:

- By Technology

- Internal Neuromodulation

- Spinal Cord Stimulation (SCS)

- Deep Brain Stimulation (DBS)

- Vagus Nerve Stimulation (VNS)

- Sacral Nerve Stimulation (SNS)

- Gastric Electrical Stimulation (GES)

- Other Internal Neuromodulation

- External Neuromodulation (Non-Invasive)

- Transcutaneous Electrical Nerve Stimulation (TENS)

- Transcranial Magnetic Stimulation (TMS)

- Other External Neuromodulations

- Internal Neuromodulation

- By Application

- Pain Management

- Parkinson's Disease

- Epilepsy

- Depression

- Dystonia

- Other Applications

- By End-User

- Hospitals & Ambulatory Surgical Centers

- Clinics & Physiotherapy Centers

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America contributed 45.21% of 2025 revenues, driven by established reimbursement pathways, a concentrated clinical-trial infrastructure, and FDA programs that accept single-arm data for breakthrough devices. CMS's national determination for dorsal root ganglion stimulation immediately opened coverage to roughly 40,000 Medicare lives, while private insurers removed prior authorization hurdles for candidates with documented opioid use disorder. Canada has added NeuroPace to its roster of assistive devices, supporting expected double-digit implant growth through 2027.

Europe delivered roughly one-third of global sales, led by Germany, the United Kingdom, and France. Germany's registry-linked funding model for closed-loop DBS sets a template for value-based adoption, even as EU MDR rules lengthen device approval cycles. In 2024, NICE guidance affirmed the cost-effectiveness of spinal cord stimulation within accepted thresholds, thereby cementing its place as a standard intervention for failed-back-surgery syndrome. Uptake in Southern and Eastern Europe remains limited by budget and staffing shortages.

The Asia-Pacific region is the fastest-growing, with a projected 9.90% CAGR to 2031. China cleared Medtronic's closed-loop DBS in 2024, but 30% patient cost-sharing still restricts implants to wealthier urban areas. Japan approved Boston Scientific's latest DBS platform, yet maintains price caps 20% below U.S. levels; such margins discourage premium launches. India saw fewer than 500 spinal cord stimulators placed in 2024 because private insurance penetration is still low.

The Middle East, Africa, and South America collectively accounted for less than 7% of 2025 sales, but exhibit isolated hotspots. The United Arab Emirates has added spinal cord stimulation to its list of essential benefits, and Brazil's private insurers reimburse neuromodulation at rates comparable to those in Southern Europe, although public-sector access remains limited.

- Abbott Laboratories

- Boston Scientific

- Inspire Medical Systems

- LivaNova

- Medtronic

- MicroTransponder Inc.

- NeuroPace

- Neuronetics

- NeuroSigma

- Nevro

- Nuvectra

- Soterix Medical

- Synapse Biomedical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Burden of Chronic Pain and Neurological Disorders

- 4.2.2 Continuous Advancements in Closed-Loop and High-Frequency Stimulation Technologies

- 4.2.3 Expansion of Approved Clinical Indications and Reimbursement Coverage

- 4.2.4 Increasing Investments, M&A Activity, and Strategic Partnerships Across Neurotechnology Ecosystem

- 4.2.5 Emergence of AI-Powered Personalized Neuromodulation Algorithms

- 4.2.6 Growth of Wearable, Non-Invasive Neuromodulation for Home-Based Care

- 4.3 Market Restraints

- 4.3.1 High Capital and Maintenance Costs of Implantable Systems

- 4.3.2 Stringent and Divergent Global Regulatory Approval Requirements

- 4.3.3 Cybersecurity and Data-Privacy Risks In Connected Neurostimulators

- 4.3.4 Limited Long-Term Clinical Evidence For Novel Indications

- 4.4 Regulatory & Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat Of New Entrants

- 4.5.2 Bargaining Power Of Buyers

- 4.5.3 Bargaining Power Of Suppliers

- 4.5.4 Threat Of Substitute Products

- 4.5.5 Intensity Of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Technology

- 5.1.1 Internal Neuromodulation

- 5.1.1.1 Spinal Cord Stimulation (SCS)

- 5.1.1.2 Deep Brain Stimulation (DBS)

- 5.1.1.3 Vagus Nerve Stimulation (VNS)

- 5.1.1.4 Sacral Nerve Stimulation (SNS)

- 5.1.1.5 Gastric Electrical Stimulation (GES)

- 5.1.1.6 Other Internal Neuromodulation

- 5.1.2 External Neuromodulation (Non-Invasive)

- 5.1.2.1 Transcutaneous Electrical Nerve Stimulation (TENS)

- 5.1.2.2 Transcranial Magnetic Stimulation (TMS)

- 5.1.2.3 Other External Neuromodulations

- 5.1.1 Internal Neuromodulation

- 5.2 By Application

- 5.2.1 Pain Management

- 5.2.2 Parkinson's Disease

- 5.2.3 Epilepsy

- 5.2.4 Depression

- 5.2.5 Dystonia

- 5.2.6 Other Applications

- 5.3 By End-User

- 5.3.1 Hospitals & Ambulatory Surgical Centers

- 5.3.2 Clinics & Physiotherapy Centers

- 5.3.3 Other End Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest Of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East And Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East And Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products And Services, And Analysis Of Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Inspire Medical Systems

- 6.3.4 LivaNova PLC

- 6.3.5 Medtronic PLC

- 6.3.6 MicroTransponder Inc.

- 6.3.7 Neuropace Inc.

- 6.3.8 Neuronetics Inc.

- 6.3.9 Neurosigma Inc.

- 6.3.10 Nevro Corporation

- 6.3.11 Nuvectra

- 6.3.12 Soterix Medical

- 6.3.13 Synapse Biomedical Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment