|

시장보고서

상품코드

2072473

항공기 엔진 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Aircraft Engines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

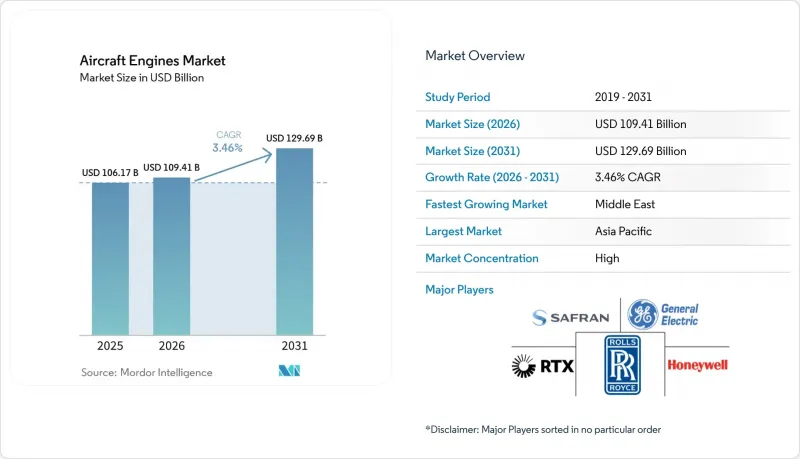

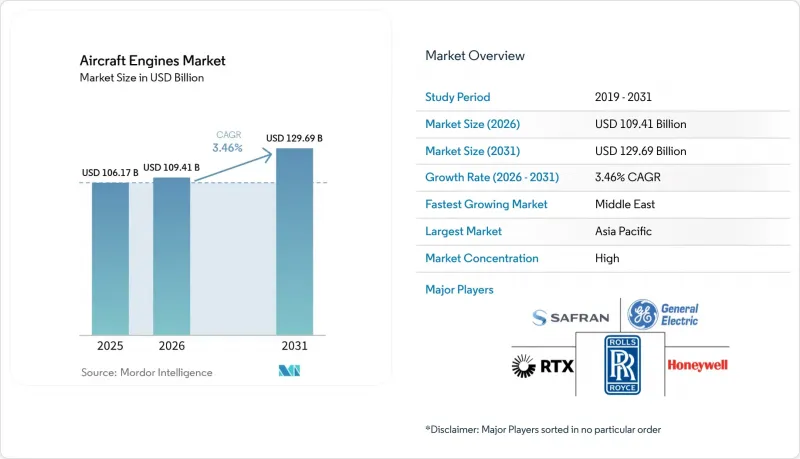

Mordor Intelligence에 의하면, 항공기 엔진 시장 규모는 2025년 1,061억 7,000만 달러로 평가되었습니다. 2026년에는 1,094억 1,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 3.46%로 성장을 지속하여, 2031년에는 1,296억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 엔진 유형(터보팬, 터보프롭 등), 항공기 유형(민간 항공기 등), 기술(기어드 터보팬 등), 추력 등급(10,000 Lbf 미만 등), 구성품(압축기, 터빈 등), 최종 사용자(OEM 공장 장착 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 항공기 엔진 시장 동향 및 인사이트

공급망 회복에 따른 트윈 아일 항공기 생산 확대

보잉과 에어버스는 2025년 말 시점에서 생산 속도가 여전히 팬데믹 이전의 최고치를 밑돌고 있었지만, 두 회사 모두 2026년부터 2028년에 걸쳐 월간 생산량을 늘릴 계획입니다. 리스 회사는 와이드바디 항공기의 리스료가 두 자릿수 증가를 기록했다고 보고했으며, 이는 B787, A350 및 향후 출시될 화물기 모델을 구동하는 고추력 엔진에 대한 프리미엄 수요를 시사합니다. 각 OEM 업체들은 이익률이 낮은 협폭기체의 생산량과 수익성이 높은 광폭기체의 애프터마켓 전망 간의 균형을 맞추기 위해 생산 능력 재조정을 추진하고 있습니다. 엔진 공급업체들은 현재 25년에 걸친 수명 주기 동안 정비 입고의 연쇄적 영향에 영향을 미치는 배분 결정에 직면해 있습니다. 그 결과로 발생하는 생산 확대는 터빈, 노즐, 기어박스 각 가치 흐름에서 수요의 시점을 재구성하게 됩니다.

급성장하는 아시아 항공사들의 전체 기단을 대상으로 한 LEAP 및 GTF 엔진으로의 전환

아시아태평양의 항공사들은 2024년부터 2025년에 걸쳐 1,200대 이상의 협폭기체를 발주했으며, 그중 에어 인디아와 비엣젯 항공만으로도 발주량의 3분의 2를 차지하고 있습니다. GE 에어로스페이스는 2026년 LEAP 엔진의 인도 대수가 1,688대를 넘어설 것이며, 그중 40%가 아시아 항공사들의 기단에 도입될 것으로 전망하고 있습니다. 플랫 앤드 휘트니사가 개선한 분말 야금 공정을 통해 2027년까지 PW1100G공급 체계를 회복하는 것을 목표로 하고 있습니다. 현재 항공사의 기종 계획 담당자들은 엔진 선정 시 명목상의 연료 소비량 차이보다 운영 리스크를 더 중요하게 여기고 있습니다. 단기적으로는 CFM이 경쟁 우위를 유지하고 있지만, PW1100G의 신뢰성이 향상된다면 중기적인 개조 기간 동안 시장 점유율의 균형이 재조정될 가능성이 있습니다.

수소 연소 엔진 아키텍처 표준화의 지연

경쟁 관계에 있는 액체 및 기체 수소 저장 방식에는 통일된 인증 체계가 부재하여, 확장 가능한 투자가 지연되고 있습니다. 에어버스사의 “"ZEROe" 이 프로젝트에서는 극저온 탱크에 대한 연구가 진행되고 있는 한편, CFM사의 “"RISE" 이 프로젝트에서는 SAF(지속 가능한 항공 연료)에 우선순위를 두는 것을 이유로, 수소 연소기 시험은 부차적인 위치에 놓여 있습니다. ICAO(국제민간항공기구)의 지침이 없기 때문에 각 OEM 업체들은 독자적인 규정 준수 대책에 자금을 투입할 수밖에 없으며, 그 결과 프로그램의 리스크가 높아지고 있습니다. 롤스로이스와 플랫 앤 휘트니는 벤치 테스트를 진행 중이지만, 인프라가 명확해질 때까지 제품 출시 결정을 미루고 있습니다. 통일된 기준이 없기 때문에 항공기 엔진 시장은 개발 비용의 불확실성에 직면해 있으며, 이로 인해 수소 관련 분야의 단기적인 성장세가 주춤하고 있습니다.

부문별 분석

터보팬 엔진은 2025년 매출의 64.67%를 차지하며, 민간 및 국방 항공기 기단의 중·장거리 운항을 뒷받침했습니다. 하이브리드 전기식 유닛은 현재 시장 점유율이 5% 미만이지만, 인증 절차가 진행됨에 따라 7.17%라는 가장 높은 연평균 성장률(CAGR)을 보일 것으로 전망됩니다. 초기 eVTOL(전기 수직 이착륙기)의 승인은 규제 당국의 수용성을 보여주고 있으며, 경량 배터리 기술의 발전으로 단거리 비행 시 적재량도 확대되고 있습니다. 터보프롭 엔진은 지역 간 이동 수단으로서 여전히 중요한 역할을 하고 있지만, 효율 향상 폭은 기어드 터보팬 엔진에 미치지 못하는 실정입니다. 터보샤프트 엔진 수요는 해양용 헬리콥터 수요 주기에 따라 증가하고 있지만, 피스톤 엔진은 터보프롭 엔진으로의 개조에 따라 점차 시장 점유율을 내주고 있습니다. 롤스로이스사의 “"펄" 이 시리즈에 채택된 기어드 액세서리 모듈은 기존과 하이브리드형 아키텍처의 융합을 보여줍니다. 이러한 변화들이 맞물리면서 항공기 엔진 시장은 점차 다양화되고 있지만, 터보팬 엔진의 우위는 여전히 흔들리지 않을 것입니다.

최종 사용자를 대상으로 한 자금 조달도 비슷한 추세를 보이고 있습니다. 리스 회사는 eVTOL 프로그램을 지원하며, 분산된 포트폴리오 전반에 걸쳐 위험을 분산시키고 있습니다. 공급망은 사이클 수가 많은 전기 모터와 파워 일렉트로닉스를 중심으로 재편되어, 자동차 등급의 제조 공정과 조화를 이루고 있습니다. 각 OEM 업체들은 하이브리드 전기 시스템의 틀 안에서 연소 코어의 업그레이드를 가능하게 하는 모듈식 설계를 활용하고 있습니다. 공급업체들에게 있어 기어박스의 윤활 및 열 관리는 여전히 최우선 연구 개발 목표로 남아 있으며, 이는 항공기 엔진 시장 전체에서 이 부문이 뛰어난 실적을 올리는 데 기여하고 있습니다.

2025년 매출에서 민간용 협폭기(narrow-body)가 차지하는 비중은 43.12%로, 이는 B737 MAX 및 A320neo의 인도에 힘입은 결과입니다. 그러나 최첨단 항공 모빌리티(AAM) 기종은 8.64%라는 가장 높은 연평균 성장률(CAGR)을 기록했습니다. Joby사와 Archer사의 인가는 도시 간 노선의 경제성을 입증하는 것으로, 시간 엄수가 필수인 물류 분야에 주력하는 화물 운송 분야의 혁신 기업들을 끌어들이고 있습니다. 와이드바디 항공기 생산은 기체 및 엔진 공급의 병목 현상으로 인해 제약을 받고 있어, 회복 속도는 완만합니다. 단기적으로는 군용 수송기 및 급유기의 현대화 수요가 전투기 생산량을 상회하여, 터보팬 생산 라인의 가동률을 안정적으로 유지하고 있습니다. 비즈니스 제트기 수주는 초장거리 기종 분야에 집중되어 있습니다. 이 분야에서 Pearl 및 Passport 엔진은 분양 소유 고객들로부터 높은 평가를 받는 객실 고도 및 속도 성능을 실현하고 있습니다. ISR(정보·감시·정찰) 및 공격 플랫폼 분야에서 UAV(무인 항공기)용 추진 시스템의 성장은 꾸준히 이어지고 있습니다. 부문 간의 상호작용으로 인해 애프터마켓의 복잡성이 증가하고 있으며, MRO(정비·수리·오버홀) 사업자들은 추력 등급이나 임무 유형별로 전문화를 추진하고 있습니다.

AAM(첨단 항공 모빌리티) 차량의 통합으로 인해 서브시스템의 전동화가 가속화되면서, 소형 가스 터빈과 결합되는 고출력 밀도 발전기에 대한 수요가 증가하고 있습니다. 이와 동시에, 와이드바디 여객기를 화물기로 개조하는 작업이 고추력 엔진의 생산 라인을 뒷받침하고 있습니다. 각 항공사는 항속 거리별 회복 궤도를 대비하기 위해 기체 구성의 다양화를 추진하고 있습니다. 따라서 항공기 엔진 시장은 성숙한 양산 분야와 신흥 성장 틈새 시장 간의 균형을 유지하고 있습니다.

지역별 분석

아시아태평양은 중국의 항공기 보유 대수 증가와 인도의 제조 거점 확장에 힘입어 2025년에도 33.19%의 점유율을 유지했습니다. 한편, 중동에서는 대형 쌍발 항공기의 대량 발주에 더해, 극심한 주변 온도로 인한 짧은 정비 주기로 인해 연평균 성장률(CAGR)이 6.38%를 나타낼 것으로 예측됩니다. 북미는 B737 MAX의 생산량과 NGAP(차세대 항공기 프로그램)의 자금 지원으로 혜택을 보고 있습니다. 유럽은 공급망 제약과 GTF 엔진의 운항 중단에 직면해 있어 성장세가 둔화되고 있습니다. 남미와 아프리카에서는 운영리스를 활용하여 기단을 현대화하고 있으며, 자본 리스크를 분산시키면서 효율성을 높이고 있습니다. 라고스, 나이로비, 아디스아바바의 현지 MRO 인프라에 대한 투자가 해당 지역의 역량 확대의 기반이 되고 있습니다. 중국과 인도의 국산 엔진 개발 프로그램은 진전을 보이고 있지만, 수입 엔진을 대규모로 대체하기까지는 아직 몇 년이 더 걸릴 것으로 보입니다. 이처럼 지역적 분산이 항공기 엔진 시장 전체의 회복력을 뒷받침하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the aircraft engines market size is expected to grow from USD 106.17 billion in 2025 to USD 109.41 billion in 2026 and is forecasted to reach USD 129.69 billion by 2031 at a 3.46% CAGR over 2026-2031.

This report is Segmented by Engine Type (Turbofan, Turboprop, and More), Aircraft Type (Commercial Aviation, and More), Technology (Geared Turbofan, and More), Thrust Class (Less Than 10, 000 Lbf, and More), Component (Compressor, Turbine, and More), End-User (OEM Factory-Fit, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Aircraft Engines Market Trends and Insights

Twin-Aisle Production Ramp-Up Post Supply-Chain Recovery

Boeing and Airbus exited 2025 with production rates still below their pre-pandemic peaks, yet both plan to increase monthly output between 2026 and 2028. Lessors reported double-digit leasing rate increases for widebody aircraft, signaling a premium for high-thrust engines that power the B787, A350, and forthcoming freighter variants. OEMs are recalibrating their capacity to balance the thin-margin, narrowbody volume with lucrative widebody aftermarket prospects. Engine suppliers now face allocation decisions that influence shop-visit cascades over 25-year service lives. The resulting production ramp reshapes demand timing across turbine, nozzle, and gearbox value streams.

Fleet-Wide Shift Toward LEAP and GTF Engines in Fast-Growing Asian Carriers

Asia-Pacific carriers placed more than 1,200 narrowbody orders in 2024-2025, with Air India and VietJet Aviation alone accounting for two-thirds of the volume. GE Aerospace expects LEAP deliveries to exceed 1,688 units in 2026, with 40% of these units entering Asian fleets. Pratt & Whitney's revised powder-metallurgy process aims to restore PW1100G availability by 2027. Airline fleet planners now weigh operational risk more heavily than nominal fuel-burn deltas when selecting engines. The competitive edge remains with CFM in the near term; however, improved PW1100G reliability could rebalance the share during mid-period retrofits.

Slow Standardization of Hydrogen-Combustion Engine Architectures

Competing liquid and gaseous hydrogen storage concepts lack harmonized certification frameworks, delaying scalable investment. Airbus ZEROe explores cryogenic tanks, while CFM RISE tests hydrogen combustors secondary to SAF priorities. The absence of ICAO guidance forces OEMs to fund bespoke compliance pathways, which in turn inflate program risk. Rolls-Royce and Pratt & Whitney conduct bench tests but defer launch decisions pending clarity on infrastructure. Without aligned standards, the aircraft engines market faces development cost uncertainty that moderates near-term momentum for hydrogen.

Other drivers and restraints analyzed in the detailed report include:

- NATO Transport and Tanker Fleet Modernization Programs Boosting Military Engine Demand

- Helicopter Fleet Renewal for Offshore Energy Operations Raising Turboshaft Deliveries

- Margin Pressure from Independent MRO Capacity Growth

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Turbofans accounted for 64.67% of 2025 revenue, underpinning medium- and long-haul activity across both civil and defense fleets. Hybrid-electric units, although currently at sub-5% market share, are projected to secure the fastest 7.17% CAGR as certification efforts progress. Early eVTOL approvals highlight regulatory receptiveness, and lightweight battery advances extend short-range payload. Turboprops maintain relevance for regional mobility, yet incremental efficiency gains lag those of geared turbofans. Turboshaft demand climbs with offshore helicopter cycles, while piston engines gradually cede share to turboprop retrofits. Geared accessory modules appearing on Rolls-Royce Pearl variants illustrate convergence between traditional and hybrid architectures. These shifts collectively diversify the aircraft engine market without displacing the primacy of turbofans.

End-user financing reflects the same pattern. Leasing firms backstop eVTOL programs, spreading risk across diversified portfolios. Supply chains reposition around high-cycle electric motors and power electronics, aligning with automotive-grade manufacturing. OEMs leverage modular designs that allow combustion core upgrades within hybrid-electric envelopes. For suppliers, gearbox lubrication and thermal management remain priority R&D targets, supporting the segment's outperformance within the broader aircraft engines market.

Commercial narrowbodies represented 43.12% of 2025 revenue, supported by B737 MAX and A320neo deliveries; however, advanced air mobility (AAM) vehicles showed the highest 8.64% CAGR. Joby and Archer approvals validate urban-route economics and attract cargo innovators focused on time-critical logistics. Widebody output recovers more slowly, constrained by fuselage and engine supply bottlenecks. Military cargo and tanker modernization outpaces fighter production in the near term, stabilizing turbofan line utilization. Business-jet orders concentrate at the ultra-long-range end of the spectrum, where Pearl and Passport engines deliver cabin altitude and speed metrics valued by fractional-ownership clients. UAV propulsion growth continues steadily within ISR and strike platforms. Cross-segment interplay widens aftermarket complexity, prompting MROs to specialize by thrust class and mission type.

AAM vehicle integration accelerates the electrification of subsystems, feeding demand for high-power-density generators that couple with small gas turbines. In parallel, widebody cargo conversions sustain production lines for high-thrust engines. Airlines diversify fleet compositions to hedge against range-specific recovery trajectories. The aircraft engines market, therefore, balances mature volume drivers with emergent growth niches.

Complete Report Scope:

- By Engine Type

- Turbofan

- Turboprop

- Turboshaft

- Piston

- Hybrid-Electric

- By Aircraft Type

- Commercial Aviation

- Narrowbody Aircraft

- Widebody Aircraft

- Regional Aircraft

- Military Aviation

- Combat Aircraft

- Non-combat Aircraft

- General Aviation

- Business Jets

- Helicopters

- Turboprop Aircraft

- Piston Engine Aircraft

- Unmanned Aerial Vehicles (UAVs)

- Advanced Air Mobility Vehicles (AAM)

- Commercial Aviation

- By Technology

- Conventional Turbofan/Turboprop

- Geared Turbofan (GTF)

- Contra-Rotating Open Rotor

- Adaptive-Cycle Engines

- Hybrid-Electric Propulsion

- By Thrust Class

- Less than 10,000

- 10,001 to 25,000

- 25,001 to 50,000

- Greater than 50,000

- By Component

- Compressor

- Turbine

- Nozzle

- Gearbox

- Other Components (Fan, Combustor,FADEC and Control Electronics, etc.)

- By End-User

- OEM Factory-Fit

- Replacement/Aftermarket

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific retained a 33.19% share in 2025, supported by China's fleet growth and India's manufacturing expansions. The Middle East, however, is expected to experience a 6.38% CAGR due to significant twin-aisle commitments and short maintenance cycles resulting from extreme ambient temperatures. North America benefits from B737 MAX volume and NGAP funding. Europe confronts supply-chain constraints and GTF groundings, softening its trajectory. South America and Africa use operating leases to modernize fleets, spreading capital risk while accessing efficiency gains. Local MRO infrastructure investment in Lagos, Nairobi, and Addis Ababa anchors regional capability growth. Indigenous engine programs in China and India are progressing but remain several years away from displacing imported power plants at scale. Geographic diversification thus supports resilience across the overall aircraft engine market.

- General Electric Company

- RTX Corporation

- CFM International

- Rolls-Royce Holdings plc

- Safran SA

- Honeywell International Inc.

- MTU Aero Engines AG

- IAE International Aero Engines AG

- IHI Corporation

- Mitsubishi Heavy Industries Aero Engines, Ltd. (Mitsubishi Heavy Industries, Ltd.)

- Textron Inc.

- United Engine Corporation (Rostec)

- China Aviation Industry Corporation Limited (AECC)

- Kawasaki Heavy Industries, Ltd.

- Hanwha Corporation

- Williams International Co., L.L.C.

- Honda Motor Co., Ltd.

- PBS International Trading,a.s.

- GKN Aerospace Services Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Emerging twin-aisle production ramp-up post-supply-chain recovery

- 4.2.2 Fleet-wide shift toward LEAP and GTF engines in fast-growing Asian carriers

- 4.2.3 NATO transport- and tanker-fleet modernization programs boosting military engine demand

- 4.2.4 Helicopter fleet renewal for offshore energy operations raising turboshaft deliveries

- 4.2.5 EU mandates for 100% SAF-ready engines in new type certificates

- 4.2.6 Leasing-driven expansion of African regional-jet operators

- 4.3 Market Restraints

- 4.3.1 Slow standardization of hydrogen-combustion engine architectures

- 4.3.2 High-temperature durability issues in hot-and-high Middle-East operations

- 4.3.3 Slow standardization of hydrogen-combustion engine architectures

- 4.3.4 Margin pressure from independent MRO capacity growth

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Engine Type

- 5.1.1 Turbofan

- 5.1.2 Turboprop

- 5.1.3 Turboshaft

- 5.1.4 Piston

- 5.1.5 Hybrid-Electric

- 5.2 By Aircraft Type

- 5.2.1 Commercial Aviation

- 5.2.1.1 Narrowbody Aircraft

- 5.2.1.2 Widebody Aircraft

- 5.2.1.3 Regional Aircraft

- 5.2.2 Military Aviation

- 5.2.2.1 Combat Aircraft

- 5.2.2.2 Non-combat Aircraft

- 5.2.3 General Aviation

- 5.2.3.1 Business Jets

- 5.2.3.2 Helicopters

- 5.2.3.3 Turboprop Aircraft

- 5.2.3.4 Piston Engine Aircraft

- 5.2.4 Unmanned Aerial Vehicles (UAVs)

- 5.2.5 Advanced Air Mobility Vehicles (AAM)

- 5.2.1 Commercial Aviation

- 5.3 By Technology

- 5.3.1 Conventional Turbofan/Turboprop

- 5.3.2 Geared Turbofan (GTF)

- 5.3.3 Contra-Rotating Open Rotor

- 5.3.4 Adaptive-Cycle Engines

- 5.3.5 Hybrid-Electric Propulsion

- 5.4 By Thrust Class

- 5.4.1 Less than 10,000

- 5.4.2 10,001 to 25,000

- 5.4.3 25,001 to 50,000

- 5.4.4 Greater than 50,000

- 5.5 By Component

- 5.5.1 Compressor

- 5.5.2 Turbine

- 5.5.3 Nozzle

- 5.5.4 Gearbox

- 5.5.5 Other Components (Fan, Combustor,FADEC and Control Electronics, etc.)

- 5.6 By End-User

- 5.6.1 OEM Factory-Fit

- 5.6.2 Replacement/Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 United Kingdom

- 5.7.2.2 France

- 5.7.2.3 Germany

- 5.7.2.4 Russia

- 5.7.2.5 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 India

- 5.7.3.3 Japan

- 5.7.3.4 South Korea

- 5.7.3.5 Rest of Asia-Pacific

- 5.7.4 South America

- 5.7.4.1 Brazil

- 5.7.4.2 Rest of South America

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 United Arab Emirates

- 5.7.5.1.2 Saudi Arabia

- 5.7.5.1.3 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 Egypt

- 5.7.5.2.2 Rest of Africa

- 5.7.5.1 Middle East

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Electric Company

- 6.4.2 RTX Corporation

- 6.4.3 CFM International

- 6.4.4 Rolls-Royce Holdings plc

- 6.4.5 Safran SA

- 6.4.6 Honeywell International Inc.

- 6.4.7 MTU Aero Engines AG

- 6.4.8 IAE International Aero Engines AG

- 6.4.9 IHI Corporation

- 6.4.10 Mitsubishi Heavy Industries Aero Engines, Ltd. (Mitsubishi Heavy Industries, Ltd.)

- 6.4.11 Textron Inc.

- 6.4.12 United Engine Corporation (Rostec)

- 6.4.13 China Aviation Industry Corporation Limited (AECC)

- 6.4.14 Kawasaki Heavy Industries, Ltd.

- 6.4.15 Hanwha Corporation

- 6.4.16 Williams International Co., L.L.C.

- 6.4.17 Honda Motor Co., Ltd.

- 6.4.18 PBS International Trading,a.s.

- 6.4.19 GKN Aerospace Services Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment