|

시장보고서

상품코드

2072503

주사기 및 바늘 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Syringe and Needle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

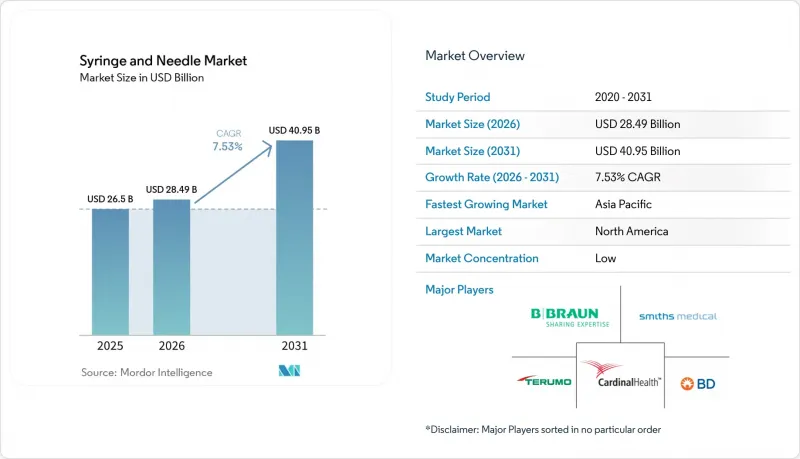

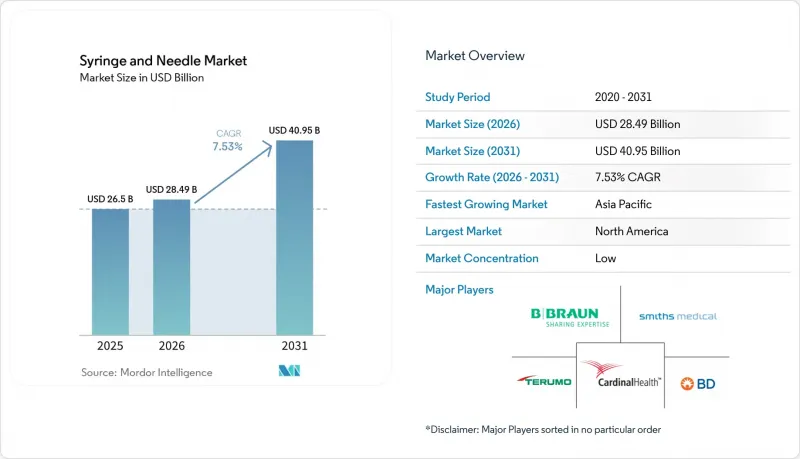

Mordor Intelligence에 의하면, 주사기 및 바늘 시장 규모는 2025년 265억 달러로 평가되었습니다. 2026년에는 284억 9,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 7.53%로 성장을 지속하여, 2031년에는 409억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 제품 카테고리(주사기(일회용 및 재사용 가능) 및 바늘(피하 주사용 등)), 소재(플라스틱, 유리 등), 용도(인슐린 투여, 백신 접종 등), 최종 사용자(병원 및 진료소, 외래수술센터(ASC) 등), 지역(북미, 유럽, 아시아태평양 등)별로 분류되어 있습니다. 시장 규모 및 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 주사기 및 바늘 시장 동향 및 인사이트

GLP-1 및 기타 생물학적 제제 주사제 파이프라인이 급증하고 있습니다.

고점도 생물학적 제제로의 전환에 따라, 각 제약사는 최대 30mL 용량의 제제로 인해 발생하는 압력을 견딜 수 있는 주사기 개발을 서둘러야 하는 상황에 놓여 있습니다. BD사의 “"Neopak XtraFlow"유리 플랫폼은 벽이 얇은 캐뉼라를 채택함으로써, 환자가 견딜 수 있는 범위 내에서 미끄러짐 저항을 유지하고 있습니다. 제약 기업들은 투여량의 정확도가 향상되는 프리필드 형식을 선호하고 있으며, 그 결과 전 세계 프리필드 주사기 시장은 2027년까지 2배로 확대될 전망입니다. 자동 주사기 수요도 증가하고 있으며, 만성 질환의 자가 관리 추세를 배경으로 이 부문은 2028년까지 196억 7,000만 달러에 달할 것으로 전망됩니다. 바이오의약품의 연구개발 파이프라인과월1회 투여 요법의 결합으로 인해, 주사기 및 바늘 시장 규모는 기존의 인슐린 중심 수요를 훨씬 뛰어넘는 규모로 확대되고 있습니다.

성인을 대상으로 한 대규모 추가 접종 프로그램

2024년 11월, 미국 성인을 대상으로 한 인플루엔자 및 코로나19 부스터 접종률은 각각 34.7%와 17.9%에 달했으며, 이로 인해 매년 이맘때면 나타나는 주사 기구에 대한 수요 급증이 발생했습니다. 자문 기구는 현재 75세 이상 성인을 대상으로 RSV 백신의 정기 접종을 권장하고 있으며, 이를 통해 호흡기 질환 유행 시즌마다 전 세계 주사기 수요의 기준선이 확보될 것입니다. 접종량이 많은 예방접종 현장에서는 준비 시간을 단축하고 의료진이 날카로운 기구에 노출되는 위험을 줄여주는 안전성을 중시하여 설계된 프리필드 제제가 선호되고 있습니다.

증가하는 바늘 찔림 사고와 교차 오염의 위험

OSHA의 추산에 따르면, 안전 장치 사용이 의무화되어 있음에도 불구하고 미국 병원에서는 연간 60만 건의 바늘 찔림 사고가 발생하고 있습니다. 오염된 주사기로 인한 집단 감염은 환자 간 감염 위험을 여실히 드러내고 있으며, 노출 후 예방 조치 및 소송과 관련된 비용을 증가시키고 있습니다.

부문별 분석

2025년, 주사기는 주사기 및 바늘 시장의 74.86%를 차지하며, 모든 치료 분야에서 없어서는 안 될 존재임을 보여주었습니다. 감염 관리 프로토콜에서는 일회용 제품을 권장하고 있기 때문에 일회용 제품이 주류를 이루고 있습니다. 재사용 가능한 주사기가 계속 사용되는 것은 멸균 관리가 경제적으로 타당할 경우에 한합니다. 이 바늘은 현재 매출 규모가 작지만, 병원에서 사용 직후 바늘 끝을 보호하는 수동 안전 장치를 채택하고 있는 점에 힘입어 2031년까지 연평균 성장률(CAGR) 8.12%를 나타낼 것으로 전망됩니다.

이러한 성장을 주도하고 있는 것은 바늘 하위 부문의 기술적 다양성입니다. 피하 주사용 모델은 백신 접종 및 약물 투여의 주력 제품으로 자리 잡고 있는 반면, 정맥 주사용 바늘은 외래에서의 수액 치료 확대에 힘입어 수요가 급증하고 있습니다. 안과 및 치과 전문의들은 정밀한 시술을 위해 극세 게이지 바늘이 필요하며, 이로 인해 틈새 시장인 고가 제품군이 형성되고 있습니다. 제조업체는 고가의 주사기에 RFID 태그를 부착하고 있으며, 이를 통해 병원 약국에서는 재고 상황을 실시간으로 파악할 수 있게 되어, 유통기한 만료로 인한 폐기량을 줄이는 데 기여하고 있습니다.

2025년, 플라스틱은 주사기 및 바늘 시장에서 52.05%의 점유율을 유지했습니다. 이는 폴리프로필렌, 폴리에틸렌 및 COC 블렌드가 저렴한 비용으로 성형성을 확보하고 감마선 멸균에 적합했기 때문입니다. 유리는 표면 반응성이 높은 바이오의약품에서 약제와 용기 간의 상호작용을 최소화하기 위해, 프리미엄 프리필드 제형 분야에서 여전히 주류를 차지하고 있습니다. 그러나 스테인리스 재질의 주사기 본체는 다시 주류로 자리 잡았으며, 주사기 본체의 변형 없이 점도가 높은 GLP-1 제제를 다룰 수 있는 견고한 투여 시스템에 대한 수요에 힘입어 2031년까지 연평균 성장률(CAGR) 8.01%를 기록하며 성장하고 있습니다. 원자재 가격의 급등과 수지 공급 충격은 의료기기 제조업체들이 자재 포트폴리오를 다각화하고 국내에서 전략적 재고를 확보하는 이유를 여실히 보여주고 있습니다.

유리 분야에 대한 투자는 업계의 자신감을 뒷받침하고 있습니다. 게레스하이머사는 스코피에 공장의 주사기 생산 능력 확장에 1억 유로를 투자했으며, 니프로사는 오토인젝터와 원활하게 연동되는 듀얼 플랜지(D2F) 형식에 대응하기 위해 독일의 생산 라인을 업그레이드했습니다. 이러한 프로젝트는 팬데믹 기간 동안 발생한 물류 병목 현상을 겪은 후 우선 과제로 부상한, 지리적 중복성을 확대하기 위한 것입니다.

지역별 분석

2025년, 북미는 39.18%의 점유율로 주사기 및 바늘 시장을 주도했습니다. 국내 제조업체들은 특정 중국산 수입품에 대한 제한을 담은 FDA의 안전성 관련 공지를 호기로 삼아, 규정을 준수하고 추적 가능성이 확보된 대체품에 대한 수요를 높였습니다. BD사는 1,000만 달러를 투자해 코네티컷주와 네브래스카주에서 생산을 확대함으로써, 안전 설계된 주사기의 생산 능력을 40%, 기존 주사기의 생산량을 50% 각각 늘려 지역 내 공급 탄력성을 강화했습니다.

유럽은 엄격한 품질 기준과 만성 질환 치료를 위한 주사제 수요를 끌어올리는 고령화 인구 덕분에 여전히 견고한 시장 기반을 유지하고 있습니다. 게레스하이머사의 유리 제품 라인 확장이나 니프로사의 D2F 업그레이드와 같은 투자는 고품질 생물학적 제제 투여 솔루션 분야에서 이 지역이 차지하는 역할을 부각시키고 있습니다. 지속가능성과 관련된 규제, 특히 확대 생산자 책임(EPR)의 의무화는 재활용 가능한 부품 및 폐기물이 적은 포장 분야의 혁신을 촉진하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 8.43%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. 인도는 2025년까지 의료기기 시장 규모가 500억 달러에 달했고, 해외 OEM 파트너십을 유치하기 위해 국내 규제를 ISO 규격에 부합하도록 조정했습니다. 중국 제조업체들은 양에서 질로의 전환을 도모하며, 클래스 III 의료기기 인증 취득에 투자하는 한편, 시장 리스크를 분산시키기 위해 동남아시아에 합작회사를 설립하고 있습니다. 만성 질환 치료가 필요한 대규모 환자층에 더해, 공립 병원의 현대화가 진행되고 있는 만큼, 해당 지역 전체에서 주사기 및 바늘에 대한 시장 수요는 계속해서 증가하는 추세입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the syringe and needle market size is expected to grow from USD 26.50 billion in 2025 to USD 28.49 billion in 2026 and is forecast to reach USD 40.95 billion by 2031 at 7.53% CAGR over 2026-2031.

This report is Segmented by Product Category (Syringes [Disposable and Reusable] and Needles [Hypodermic and More]), Material (Plastic, Glass, and More), Application (Insulin Administration, Vaccination, and More), End User (Hospitals and Clinics, Ambulatory Surgery Centers, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Global Syringe and Needle Market Trends and Insights

Surging GLP-1 & Other Biologic Injectables Pipeline

The shift toward high-viscosity biologics pushes manufacturers to develop syringes that can withstand pressures created by formulations up to 30 mL. BD's Neopak XtraFlow glass platform integrates thinner-wall cannulas to maintain glide force within patient-acceptable ranges . Pharmaceutical firms favor prefilled formats because they improve dose accuracy; as a result, the global prefilled syringe segment is on track to double by 2027. Autoinjector demand also rises, with the category forecast to hit USD 19.67 billion by 2028 on the back of chronic disease self-care. The combination of biologic R&D pipelines and monthly dosing regimens enlarges the syringe and needle market far beyond historical insulin-focused volumes.

Mass Adult Booster Immunization Programs

Influenza and COVID-19 booster uptake among U.S. adults reached 34.7% and 17.9% respectively in November 2024, creating recurring annual demand spikes for injection devices . Advisory bodies now recommend routine RSV vaccination for adults >=75 years, locking in baseline global syringe volumes each respiratory season. High-throughput immunization settings favor safety-engineered, prefilled devices that cut preparation time and reduce worker exposure to sharps.

Growing Cases of Needle-Stick Injuries & Risk of Cross-Contamination

OSHA estimates 600,000 needle-stick injuries occur annually in U.S. hospitals despite mandated safety devices. Outbreaks linked to contaminated syringes underscore patient-to-patient transmission risks, elevating costs tied to post-exposure prophylaxis and litigation .

Other drivers and restraints analyzed in the detailed report include:

- High and Rising Burden of Chronic & Infectious Diseases

- Increased Adoption of Injectable Drugs for Out-Patient Care

- Availability & Rapid Progress of Needle-Free Delivery Technologies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Syringes captured 74.86% of the syringe and needle market share in 2025, underlining their indispensability across therapeutic areas. Disposable variants predominate because infection-control protocols favor single-use devices. Reusable syringes persist only where sterilization controls are economically justified. Needles, though smaller in revenue today, post an 8.12% CAGR to 2031 as hospitals adopt passive safety mechanisms that shield the tip immediately after use.

Technological variety within the needle subsegment fuels this performance. Hypodermic models remain workhorses for vaccination and drug administration, whereas intravenous needles accelerate on the back of outpatient infusion growth. Ophthalmic and dental specialists demand ultra-fine gauges for precision procedures, creating niche premium-price categories. Manufacturers overlay RFID tags on high-value syringes, enabling real-time inventory visibility for hospital pharmacies and reducing wastage from expired stock.

Plastic retained 52.05% share of the syringe and needle market in 2025 as polypropylene, polyethylene and COC blends provided low-cost moldability and gamma-sterilization compatibility. Glass continues to rule premium prefilled formats because it minimizes drug-container interaction for biologics with high surface sensitivity. Yet stainless-steel barrels re-enter the mainstream, growing at 8.01% CAGR through 2031, buoyed by the need for rugged delivery systems that handle viscous GLP-1 formulations without barrel flex. Raw-material inflation and resin supply shocks illustrate why device firms diversify material portfolios and on-shore strategic inventory.

Glass investments reinforce confidence: Gerresheimer allocated EUR 100 million to scale syringe capacity at its Skopje plant, while Nipro upgraded German lines for dual-flange (D2F) formats that pair seamlessly with autoinjectors. Such projects broaden geographical redundancy, a priority after pandemic-era freight bottlenecks.

Complete Report Scope:

- By Product Category

- Syringes

- Disposable

- Reusable

- Needles

- Hypodermic

- Intravenous

- Intramuscular

- Others

- Syringes

- By Material

- Plastic

- Glass

- Stainless Steel

- By Application

- Insulin Administration

- Vaccination

- Osteoarthritis

- Botox

- Blood Collection

- Ophthalmic Procedures

- Dental

- Other Applications

- By End User

- Hospitals and Clinics

- Ambulatory Surgery Centers

- Diagnostic Laboratories

- Home Healthcare Settings

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Geography Analysis

North America led the syringe and needle market with 39.18% share in 2025. Domestic producers capitalized on FDA safety communications that curtailed certain Chinese imports, elevating demand for compliant, traceable alternatives. BD's USD 10 million expansion added 40% safety-engineered syringe capacity and 50% conventional syringe output across Connecticut and Nebraska, fortifying regional supply resilience.

Europe remained a stronghold owing to stringent quality norms and aging populations that boost chronic-care injections. Investments such as Gerresheimer's glass line scale-up and Nipro's D2F upgrades underscore the region's role in premium biologic delivery solutions. Sustainability rules, especially extended-producer responsibility mandates, spur innovation in recyclable components and low-waste packaging.

Asia-Pacific is the fastest-growing zone at 8.43% CAGR. India aims for a USD 50 billion medical-device economy by 2025 and has aligned domestic regulations with ISO standards to attract foreign OEM partnerships. Chinese manufacturers pivot from volume to value, investing in class-III device certification and building joint ventures in Southeast Asia to diversify market exposure. Large patient pools needing chronic therapy, coupled with public-hospital modernization, sustain a rising baseline for syringe and needle market demand across the region.

- Beckton Dickinson

- Terumo

- B. Braun

- Nipro

- Cardinal Health

- Gerresheimer

- Hindustan Syringes & Medical Devices

- SCHOTT

- Smiths Group

- Henry Schein

- DeRoyal Industries

- Connecticut Hypodermics

- Medtronic

- Retractable Technologies

- West Pharmaceutical Services

- Hamilton Company

- Vetter Pharma International

- Ultimed

- Jiangsu Delfu medical

- Zhejiang Jianfeng Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging GLP-1 & other biologic injectables pipeline

- 4.2.2 Mass adult booster immunization programs

- 4.2.3 High and rising burden of chronic & infectious diseases

- 4.2.4 Increased adoption of injectable drugs for out-patient care

- 4.2.5 Worsening antimicrobial resistance driving safety-engineered syringes

- 4.2.6 Expansion of point-of-care diagnostic testing using single-use needles

- 4.3 Market Restraints

- 4.3.1 Growing cases of needle-stick injuries & risk of cross-contamination

- 4.3.2 Availability & rapid progress of needle-free delivery technologies

- 4.3.3 Extended-producer-responsibility (EPR) rules raising compliance costs

- 4.3.4 Volatility in medical-grade plastic resin prices

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Category

- 5.1.1 Syringes

- 5.1.1.1 Disposable

- 5.1.1.2 Reusable

- 5.1.2 Needles

- 5.1.2.1 Hypodermic

- 5.1.2.2 Intravenous

- 5.1.2.3 Intramuscular

- 5.1.2.4 Others

- 5.1.1 Syringes

- 5.2 By Material

- 5.2.1 Plastic

- 5.2.2 Glass

- 5.2.3 Stainless Steel

- 5.3 By Application

- 5.3.1 Insulin Administration

- 5.3.2 Vaccination

- 5.3.3 Osteoarthritis

- 5.3.4 Botox

- 5.3.5 Blood Collection

- 5.3.6 Ophthalmic Procedures

- 5.3.7 Dental

- 5.3.8 Other Applications

- 5.4 By End User

- 5.4.1 Hospitals and Clinics

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Home Healthcare Settings

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 Terumo Corporation

- 6.3.3 B. Braun Melsungen AG

- 6.3.4 Nipro Corporation

- 6.3.5 Cardinal Health Inc.

- 6.3.6 Gerresheimer AG

- 6.3.7 Hindustan Syringes & Medical Devices

- 6.3.8 Schott AG

- 6.3.9 Smiths Medical (ICU Medical)

- 6.3.10 Henry Schein, Inc.

- 6.3.11 DeRoyal Industries

- 6.3.12 Connecticut Hypodermics Inc.

- 6.3.13 Medtronic plc

- 6.3.14 Retractable Technologies Inc.

- 6.3.15 West Pharmaceutical Services

- 6.3.16 Hamilton Company

- 6.3.17 Vetter Pharma International

- 6.3.18 UltiMed Inc.

- 6.3.19 Jiangsu Delfu medical

- 6.3.20 Zhejiang Jianfeng Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment