|

시장보고서

상품코드

2072509

원유 유동성 개선제 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Crude Oil Flow Improvers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

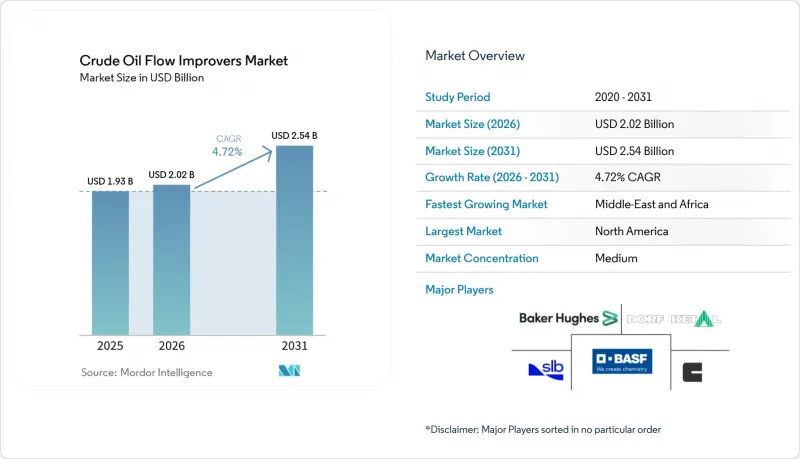

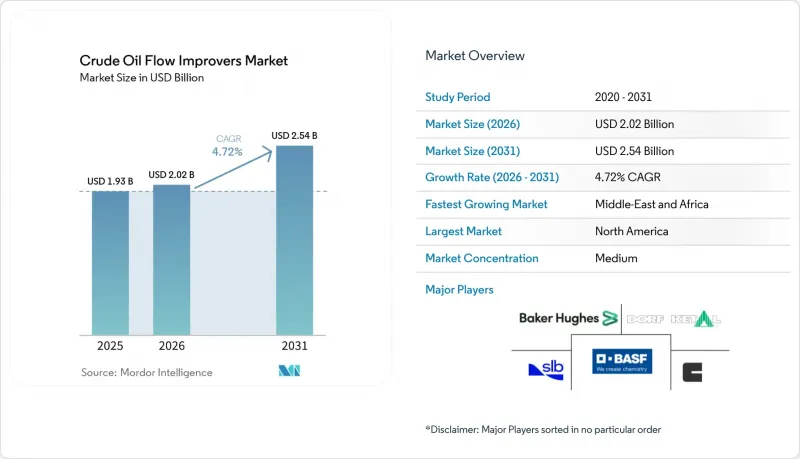

Mordor Intelligence에 의하면, 원유 유동성 개선제 시장 규모는 2025년 19억 3,000만 달러로 평가되었습니다. 2026년에는 20억 2,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 4.72%로 성장을 지속하여, 2031년까지 25억 4,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 첨가제의 유형(파라핀 및 아스팔텐 억제제, 항점도제, 스케일 및 부식 억제제 등), 원유의 유형(경질·중질, 중질·초중질), 도입 장소(육상·해상), 용도(채굴, 파이프라인 및 운송 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다.

세계의 원유 유동성 개선제 시장 동향 및 인사이트

셰일 및 타이트 오일 파이프라인 연장 거리 증가

북미의 셰일 생산량 증가로 인해 원유 수송망 내의 점도와 왁스 함량이 높아지고 있으며, 사업자들은 유동성을 경제적 임계치 이상으로 유지하기 위해 점도 저감제를 투입할 수밖에 없는 상황입니다. 초고분자량 폴리올레핀은 저온 성능을 향상시켜, 영하로 떨어지는 계절에 기존 화학 약품이 열화되는 캐나다와 다코타 주 일대의 파이프라인을 지탱하고 있습니다. 디지털 제어 주입 스키드를 통해 공정이 실시간으로 조정되게 되었으며, 원유 블렌드의 변동에 맞추어 투여량을 최적화함으로써 처리 능력을 저하시키지 않고도 화학약품 비용을 절감할 수 있게 되었습니다. 셰일 유정의 파이프라인 연장 거리가 늘어나고 기존 간선 파이프라인과 상호 연결됨에 따라 이러한 효율성은 더욱 확대되고 있으며, 이는 원유 유동성 개선제 시장의 성장세를 더욱 강화하고 있습니다.

수화 억제제가 필요한 심해 FPSO 프로젝트의 급증

수심 1,500m를 넘는 초심해 개발에서는 하이드레이트 형성 위험이 높아집니다. 저용량의 동적 억제제 및 응집 방지제는 부피가 큰 메탄올 처리 방식보다 뛰어난 성능을 발휘하여, 상부 구조물의 저장 공간을 줄이는 동시에 탄소 발자국을 감소시킵니다. 사워 가스에 대응하는 이 패키지는 70,000 ppm을 초과하는 황화수소 농도에서도 안정성을 보여주고 있으며, 브라질의 프레솔트층 유정 및 앙골라 연안의 신규 발견 유전 개발을 가능하게 하고 있습니다. 각 운영사는 해저 부스팅 유닛과 동기화되는 앰빌리컬 화학약품 라인을 도입하고 있으며, 이에 따라 원유 유동성 향상제 시장 전반에서 특수 배합 제품의 채택이 지속적으로 확대되고 있습니다.

PFAS 규제가 강화됨에 따라, 불소계 유동성 개선제의 사용이 제한되고 있습니다.

PFAS 규제의 확대에 따라 신속한 배합 변경이 시급해지고 있습니다. 오랫동안 극한 온도 용도로 사용되어 온 불소계 계면활성제가 단계적으로 폐지될 예정인 가운데, 각 제조업체들은 실리콘, 탄화수소 또는 바이오 유래 대체재에 대한 투자를 확대되고 있습니다. DIC 주식회사의 PFAS 무함유 소포 기술은 2024년에 상용화 준비가 완료되었으나, 당분간 공급 부족으로 인해 비용이 상승하면서 인증 절차가 장기화되고 있습니다. 불소 엘라스토머로 제작된 장비 부품도 대체가 필요해졌으며, 이러한 혼란은 순수한 화학물질의 범위를 넘어 원유 유동성 개선제 시장의 단기적인 성장을 둔화시키고 있습니다.

부문별 분석

파라핀 및 아스팔텐 억제제는 가장 높은 매출을 기록했으며, 2025년에는 시장 점유율의 38.62%를 차지했습니다. 이는 작업자가 저온 파이프라인 내부의 왁스 침적 문제를 해결하기 위해 노력했기 때문입니다. 중질 원유의 생산량이 증가하고, 해저를 통과할 때 심해 유체가 급격히 냉각되기 때문에 이러한 첨가제를 활용한 원유 유동성 향상제 시장 규모는 꾸준히 확대될 것으로 전망됩니다. 마찰 방지제는 매출 규모는 작지만, 자본 투자를 통한 확장을 하지 않고 노후화된 파이프라인의 처리 능력을 향상시켜야 할 필요성을 반영하여 연평균 성장률(CAGR) 7.41%로 가장 빠르게 성장하고 있습니다. 왁스 제어, 아스팔텐 분산, 오염 방지 특성을 결합한 다기능 패키지는 현장에서 사용되는 화학 약품의 SKU 수를 줄여주며, 통합 솔루션을 원유 유동성 개선제 시장의 최전선으로 끌어올리고 있습니다.

2025년에는 중질 및 초중질 원유가 47.02%의 점유율을 차지했으며, 연평균 성장률(CAGR) 6.08%를 기록해 경질 원유를 앞지를 것으로 전망됩니다. 이는 기존 유전이 성숙기에 접어들면서 전 세계 생산 구성이 점도가 높은 자원으로 전환되고 있기 때문입니다. 전단 안정성 폴리머는 압력 손실을 줄이고 파라핀의 결정화를 억제하기 때문에 트랜스 마운틴이나 안데스 지역을 연결하는 파이프라인 등 국경을 넘는 파이프라인을 뒷받침하고 있습니다. 실험실 테스트 결과, 기계적 캐비테이션 기술과 최적화된 첨가제 패키지를 결합함으로써 점도가 60% 이상 감소한다는 사실이 입증되었습니다. 이러한 하이브리드 방식을 통해 기존 파이프라인 경로에서도 고밀도 원유를 수송할 수 있다는 확신이 커지면서, 원유 유동성 향상제 시장에 대한 투자가 지속되고 있습니다.

중질 원유 역시 한랭 지역에서는 여전히 유동성 지원이 필요하며, 수요는 폭넓은 계층에 걸쳐 있습니다. 경질 블렌드 역시 초심해 환경에서 하이드레이트 억제 효과의 혜택을 받고 있으며, 이는 화학약품 수요가 가장 중질인 원유에만 국한되지 않고 원유 등급 전반에 걸쳐 확대되고 있음을 뒷받침하고 있습니다.

지역별 분석

2025년, 북미는 셰일 파이프라인과 멕시코만 인프라에 힘입어 전 세계 매출의 33.28%를 차지했습니다. 자동화와 고부하 폴리머는 영하 지역의 성능을 뒷받침하며, 원유 유동성 향상제 시장 전반에 걸친 교체 수요를 유지하고 있습니다.

중동 및 아프리카은 산성 원유의 수익화 및 서아프리카 심해 허브의 조기 구축을 목표로 하는 각국의 계획에 힘입어, 2031년까지 연평균 성장률(CAGR) 5.84%로 급성장할 전망입니다. 아시아태평양의 성장은 정유시설 확장 및 연안의 수입 터미널에 원유를 공급하는 새로운 국제 파이프라인 건설과 밀접한 관련이 있습니다. 유럽에서는 북해 파이프라인망의 교체 수요가 지속되고 있을 뿐만 아니라, 엄격한 PFAS 규제로 인해 불소 무함유 화학물질의 도입이 가속화되고 있습니다.

오만의 산성 가스 대응 억제제 및 인도의 하이브리드 왁스 제어 파이프라인과 관련된 최근 동향은 공급업체가 해당 지역에 더욱 깊이 진출하기 위해 습득해야 할 지역 특화 엔지니어링의 좋은 사례입니다. 국내 정제 자급자족을 장려하는 정부의 지침은 개발도상 지역 전체에서 견고한 유동성 보장 프로그램에 대한 수요를 더욱 높이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the crude oil flow improvers market size is expected to grow from USD 1.93 billion in 2025 to USD 2.02 billion in 2026 and is forecast to reach USD 2.54 billion by 2031 at 4.72% CAGR over 2026-2031.

This report is Segmented by Improver Type (Paraffin and Asphaltene Inhibitors, Drag Reducing Agents, Scale and Corrosion Inhibitors, and More), Oil Type (Light and Medium, Heavy and Extra-Heavy), Deployment Location (Onshore and Offshore), Application (Extraction, Pipelines and Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Global Crude Oil Flow Improvers Market Trends and Insights

Increased Shale and Tight-Oil Pipeline Mileage

North American shale output lifts viscosity and wax load in gathering networks, compelling operators to dose drag-reducing agents that keep flow above economic thresholds. Ultra-high-molecular-weight polyolefins enhance low-temperature performance, supporting lines in Canada and the Dakotas where sub-zero seasons degrade legacy chemistries. Digital injection skids now modulate treatment in real time, aligning dosage with crude blend variability to trim chemical cost without throttling capacity. These efficiencies are scaling as shale wellhead pipelines grow in mileage and interconnect existing trunk lines, reinforcing momentum in the crude oil flow improvers market.

Surge in Deep-Water FPSO Projects Requiring Hydrate Inhibitors

Ultra-deep developments past 1,500 m water depth intensify hydrate formation risk. Low-dosage kinetic and anti-agglomerant inhibitors outperform bulky methanol campaigns, easing topside storage and cutting carbon footprints. Sour-gas-compatible packages show stability at hydrogen sulfide levels above 70,000 ppm, unlocking pre-salt wells in Brazil and new finds off Angola. Operators deploy umbilical chemical lines that synchronize with subsea boosting units, driving sustained uptake of specialized formulations across the crude oil flow improvers market.

Stricter PFAS Bans Limiting Fluorinated Flow Improver Chemistries

Widening PFAS regulation compels rapid reformulation. Fluorinated surfactants that long served extreme temperature applications face phase-out, prompting manufacturers to invest in silicone, hydrocarbon, or bio-based alternatives. DIC Corporation's PFAS-free antifoam technology reached commercial readiness in 2024, but interim supply gaps elevate costs and prolong qualification cycles. Equipment components made of fluoro-elastomers also require substitution, extending disruption beyond pure chemicals and tempering near-term growth in the crude oil flow improvers market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand for Paraffin and Asphaltene Inhibitors

- Growing Adoption of Polymer-Based DRAs in Aging Trunk Lines

- Volatility in Upstream CAPEX Cycles Post-Energy Transition Pledges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Paraffin and asphaltene inhibitors generated the largest revenue, delivering 38.62% market share in 2025 as operators battled wax deposition in cooler pipelines. The crude oil flow improvers market size for these additives is forecast to expand steadily because heavy-crude output rises and deepwater fluids cool rapidly during seabed transit. Drag reducing agents, though smaller by revenue, advance fastest at 7.41% CAGR, mirroring the need to lift throughput in aging lines without capital expansion. Multifunctional packages that merge wax control, asphaltene dispersion, and anti-foul properties reduce chemical SKUs onsite, pushing integrated solutions to the forefront of the crude oil flow improvers market.

Heavy and extra-heavy feeds secured a 47.02% share in 2025 and outpace lighter grades with a 6.08% CAGR because the global production mix tilts toward viscous resources as conventional reservoirs mature. Shear-stable polymers cut pressure drop and stave off paraffin crystallization, supporting cross-border pipelines such as Trans Mountain and Andean links. Laboratory trials demonstrate over 60% viscosity reduction when mechanical cavitation technologies partner with tailored additive packages. Such hybrid methods bolster confidence that existing rights-of-way can carry denser barrels, sustaining investment in the crude oil flow improvers market.

Medium crudes still need flow support in frigid climates, keeping demand broad-based. Light blends also benefit from hydrate suppression in ultra-deep environments, confirming that chemical demand grows across the crude grade spectrum rather than relying solely on the heaviest cuts.

Complete Report Scope:

- By Improver Type

- Paraffin and Asphaltene Inhibitors

- Drag Reducing Agents

- Scale and Corrosion Inhibitors

- Hydrate and Hydrogen Sulfide Inhibitors

- Other Improver Types (Demulsifiers and Biocides, etc.)

- By Oil Type

- Light and Medium (Less than 25 wt% wax)

- Heavy and Extra-Heavy (Greater than 25 wt% wax)

- By Deployment Location

- Onshore

- Offshore (Shallow, Deep, Ultra-Deep)

- By Application

- Extraction

- Pipelines and Transportation

- Processing

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- Italy

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

North America controlled 33.28% of worldwide revenue in 2025, underwritten by shale pipelines and Gulf of Mexico infrastructure. Automation and high-load polymers buttress performance in below-freezing territories, sustaining replacement demand across the crude oil flow improvers market.

The Middle East and Africa surge at 5.84% CAGR through 2031, buoyed by national plans to monetize sour crudes and fast-track West African deepwater hubs. Asia-Pacific growth tracks refinery expansions and new transnational lines feeding coastal import terminals. Europe maintains replacement demand in North Sea networks and adheres to strict PFAS curbs that accelerate fluorine-free chemistry adoption.

Recent breakthroughs in sour-gas compatible inhibitors in Oman and hybrid wax-control pipelines in India exemplify the localized engineering that vendors must master to deepen geographic penetration. Government directives urging domestic refining self-sufficiency further amplify the call for robust flow assurance programs across developing regions.

- Ashland

- Baker Hughes

- BASF

- Clariant

- Croda International Plc

- Dorf Ketal

- Dow

- Evonik Industries AG

- Halliburton

- Innospec

- LiquidPower Specialty Products Inc.

- NuGenTec

- Oil Flux

- SLB (Schlumberger)

- The Lubrizol Corporation

- The Zoranoc Oilfield Chemical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increased shale and tight-oil pipeline mileage

- 4.2.2 Surge in deep-water FPSO projects requiring hydrate inhibitors

- 4.2.3 Growing Demand For Paraffin and Asphaltene Inhibitors

- 4.2.4 Growing adoption of polymer-based DRAs in aging trunk lines

- 4.2.5 Increasing Demand for Petroleum Based Products

- 4.3 Market Restraints

- 4.3.1 Stricter PFAS bans limiting fluorinated flow improver chemistries

- 4.3.2 Volatility in upstream CAPEX cycles post-energy transition pledges

- 4.3.3 Supply bottlenecks for high-molecular-weight poly-alpha-olefins

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Improver Type

- 5.1.1 Paraffin and Asphaltene Inhibitors

- 5.1.2 Drag Reducing Agents

- 5.1.3 Scale and Corrosion Inhibitors

- 5.1.4 Hydrate and Hydrogen Sulfide Inhibitors

- 5.1.5 Other Improver Types (Demulsifiers and Biocides, etc.)

- 5.2 By Oil Type

- 5.2.1 Light and Medium (Less than 25 wt% wax)

- 5.2.2 Heavy and Extra-Heavy (Greater than 25 wt% wax)

- 5.3 By Deployment Location

- 5.3.1 Onshore

- 5.3.2 Offshore (Shallow, Deep, Ultra-Deep)

- 5.4 By Application

- 5.4.1 Extraction

- 5.4.2 Pipelines and Transportation

- 5.4.3 Processing

- 5.4.4 Other Applications

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ashland

- 6.4.2 Baker Hughes

- 6.4.3 BASF

- 6.4.4 Clariant

- 6.4.5 Croda International Plc

- 6.4.6 Dorf Ketal

- 6.4.7 Dow

- 6.4.8 Evonik Industries AG

- 6.4.9 Halliburton

- 6.4.10 Innospec

- 6.4.11 LiquidPower Specialty Products Inc.

- 6.4.12 NuGenTec

- 6.4.13 Oil Flux

- 6.4.14 SLB (Schlumberger)

- 6.4.15 The Lubrizol Corporation

- 6.4.16 The Zoranoc Oilfield Chemical

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment