|

시장보고서

상품코드

2072529

고순도 석영 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)High Purity Quartz - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

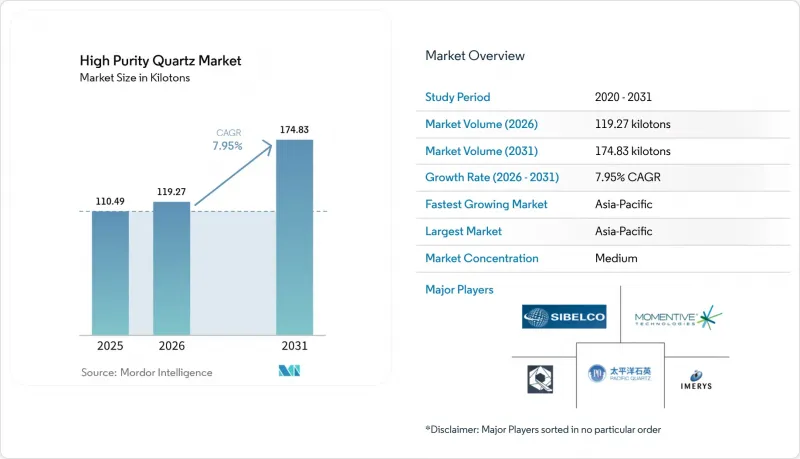

Mordor Intelligence에 의하면, 2026년 고순도 석영 시장 규모는 119.27 킬로톤에 이를 것으로 예상되며 2025년 110.49 킬로톤으로부터 확대해, 2031년에는 174.83 킬로톤에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 7.95%로 성장할 것으로 전망됩니다.

본 보고서는 원료 유형(천연 석영(페그마타이트), 합성 석영(열수법/CVD법), 정제 석영 모래(고상법)), 용도(반도체, 태양광 발전, 조명, 통신·광학, 기타), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 수량(톤) 단위로 제시되어 있습니다.

세계의 고순도 석영 시장 동향 및 분석

차세대 로직 및 메모리 팹에 대한 수요 급증

2025년부터 2027년에 걸쳐 예정된 신규 300mm 팹 건설을 위한 전 세계 설비 투자액 4,000억 달러에 힘입어, 석영 도가니, 튜브, 보트 등 고순도 공정 부품의 소비가 확대되고 있습니다. 2nm 로직 노드로 전환하는 파운드리 업체들은 10억 분의 1 수준에서 금속 오염 물질을 관리해야 하며, 이로 인해 웨이퍼 1장당 석영 사용량이 증가하고 있습니다. 고대역폭 모듈로의 확장을 추진하는 메모리 제조업체들은 더 대형의 결정 성장로를 채택하고 있으며, 이를 위해서는 더 엄격한 내열충격성을 갖춘 도가니가 필요합니다. 한국 및 대만의 거점에서 운영되는 인증 프로그램에서는 현재 4N+ 순도 기준이 규정되어 있으며, 이에 따라 업스트림 공급업체들은 아시아태평양의 팹 인근에서 정제 능력 확충을 추진하고 있습니다. 미국에서는 CHIPS법에 따른 지원을 받고 있는 공장들이 단일 광산에 대한 의존 위험을 분산하기 위해, 두 업체로부터 공급이 가능한 합성 대체재의 도입을 요구하며, 조달 계약에 장기적인 인수 조항을 포함시키고 있습니다.

태양광 발전용 잉곳 생산 능력 확대

세계 결정질 실리콘 모듈 수요를 배경으로, 2030년까지 태양광 등급 석영의 연평균 성장률(CAGR)은 12.40%를 나타낼 것으로 전망됩니다. 중국 및 동남아시아의 제조업체들은 1사이클당 더 큰 용광로를 소비하는 직경 2600 mm의 풀 장비를 도입하는 속도를 높이고 있어, 석영의 단위 부하량이 증가하고 있습니다. 유럽의 제조업체는 “‘인플레이션 억제법(IRA)’이를 본떠 우대 조치를 활용하여 웨이퍼의 현지 생산을 추진하고 있으며, 지역별 원료 수요가 확대되고 있습니다. 순도 기준은 여전히 엄격하며(철분 5ppm 미만, 총 불순물 300ppm 미만), 이에 따라 아시아의 선광 거점에서는 첨단 산 침출 공정의 도입이 진행되고 있습니다. 폐루프식 수처리 시스템을 도입하는 공급업체는 환경 승인을 신속하게 획득하여 시장 출시까지의 기간을 단축하고 있습니다.

페그마타이트 광업의 생산량 변동과 가격의 급등락

2024년, 중국 시장에서 발생한 극심한 가격 변동은 하류 제조업체들이 천연 고순도 석영공급 및 재고 관리에 직면한 과제를 여실히 드러냈습니다. 2024년 9월, 허리케인 ‘"헬렌" 스프루스파인의 가동 중단으로 인해, 공급 집중에 따른 위험이 드러났습니다. 시벨코사와 더 쿼츠 코퍼레이션사는 가동을 중단했으며, 더 쿼츠 코퍼레이션사는 CNBC와의 인터뷰에서 가동 재개 시기에 대해 “"전망이 보이지 않는다"라고 보고했습니다. 페그마타이트 광상의 지질학적 변동성으로 인해 지속적인 평가와 품위 관리가 필수적이지만, 소규모 광산 사업의 경우 기상 조건에 따른 가동 중단, 설비 고장, 인허가 지연 등으로 인해 더 큰 불확실성에 직면해 있습니다. 고순도 석영의 가격 변동은 반도체 및 태양전지 제조업체에 큰 영향을 미치고 있으며, 조달 팀은 공급 리스크를 완화하기 위해 이중 조달 전략 및 재고 완충 장치 도입을 추진하고 있습니다.

부문별 분석

천연 석영은 주로 도가니 및 튜브 제조업체들과의 탄탄한 공급 관계를 바탕으로, 2025년 고순도 석영 시장에서 61.12%의 점유율을 유지했습니다. 그러나 일본, 한국, 미국에서 열수법을 통한 생산 능력 확충에 힘입어 합성 석영의 생산량은 연평균 성장률(CAGR) 8.68%로 증가하고 있습니다. 합성 등급 고순도 석영 시장 규모 확대는 2nm 공정 라인에서 웨이퍼 불량률을 대폭 낮추는 일관된 불순물 프로파일에 힘입어 이루어지고 있습니다. 또한, 합성 석영 제조업체는 정치적 위험이 높은 광업권에 의존하지 않으면서도 유럽의 함유율 규정을 충족하고 있으며, 이는 ““중요 원자재법”에서 결정적인 요인으로 작용하고 있습니다.

천연 석영 공급업체들은 시장 점유율 하락을 막기 위해 선광 공정의 고도화에 주력하고 있습니다. 새로운 자력 분리 회로를 통해 운모와 장석 성분을 제거하고, 고온 염소화 장치를 통해 미량의 알칼리 성분을 저감하고 있습니다. 이러한 조합을 통해 달성 가능한 순도는 4N+까지 향상되었으며, 합성 석영과의 품질 격차가 줄어들고 있습니다. 그렇긴 하지만, 페그마타이트의 생산량은 여전히 기후 변화나 ‘"즉시 채굴 가능"매장량 고갈의 영향을 받기 쉬우므로, 하류 기업들은 조달 계약의 다각화를 추진하고 있습니다. 두 공급 경로의 비용 구조가 비슷해짐에 따라, 구매자들이 공급 안정성과 특수 광학 용도에 필요한 결정 크기 요건을 저울질하는 가운데, 협상 구도도 재편되고 있습니다.

지역별 분석

아시아태평양은 2025년 소비량의 64.40%를 차지했으며, 중국이 폴리실리콘 생산을 확대하고 대만이 2nm 로직 생산을 향해 착실히 나아가고 있는 가운데, 2031년까지 연평균 성장률(CAGR) 8.22%라는 최고 수준을 기록할 것으로 전망됩니다. 2025년 4월, 중국 정부가 고순도 석영을 전략적 광물로 지정하기로 결정함에 따라, 진링 산맥과 알타이 산맥에서의 탐사가 가속화되는 한편, 저금리 자금이 가공 거점으로 유입되었습니다. 일본의 소재 공급업체들은 국내 팹과의 협력을 강화하고, 단일 광산으로부터의 수입 의존도를 낮추기 위한 합성 경로를 중시하고 있습니다. 한국은 메모리 분야의 선도적 입지를 바탕으로 안정적인 수요를 유지하고 있는 반면, 호주는 아시아로의 운송 경로를 단축해 주는 해안가 실리카 프로젝트를 상용화하고 있습니다.

북미는 사용량 기준으로 2위를 차지하고 있습니다. 노스캐롤라이나주 스프루스파인은 천연 고순도 석영(HPQ) 블록의 세계 최대 공급처로 자리매김하고 있으며, 시벨코(Sibelco)사의 2억 달러 규모 생산 라인 현대화 사업을 통해 2025년까지 분쇄 처리 능력이 향상되었습니다. CHIPS 자금의 지원을 받는 현지 팹은 운송 시 배출량을 거의 제로로 내세우는 지역 내 합성 스타트업 기업을 활용하고 있습니다. 캐나다는 중요 광물에 대한 연방 정부의 허가 절차 효율화를 바탕으로, 대서양 연안의 석영 광맥을 전략적 원료로 자리매김하고 있습니다. 해당 지역 시장 동향은 미국의 팹이 3개의 새로운 300mm 생산 라인을 가동하는 속도에 좌우되며, 이러한 변동 요인으로 인해 연간 수요가 10킬로톤 정도 변동할 가능성이 있습니다.

유럽의 고순도 석영사 시장은 지원 정책의 혜택을 받고 있습니다. ““중요 원자재법”는 2030년까지 EU 역내에서 채굴량 10%, 가공량 40%라는 목표를 의무화하고 있습니다. 프랑스의 고순도 석영사 시장은 프랑스의 “'옵틱스 밸리' 와 독일의 마이크로일렉트로닉스 파크가 공동으로 실시하는 시범 프로젝트의 혜택을 받고 있습니다. 이 프로젝트에서는 지역 지열을 활용한 수열 반응로가 도입되어 에너지 집약도가 낮아졌습니다. 스칸디나비아의 광산 회사는 가공되지 않은 모래를 운송하는 대신 부가가치 창출 방안을 모색하고 있습니다. 남미와 중동의 신흥 시장은 규모는 작지만, 태양광 모듈 및 유리섬유 공급망과의 하류 통합을 추구하고 있어, 세계 공급에 대해 점진적이고 지속적인 수요 견인 효과가 기대됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, high purity quartz market size in 2026 is estimated at 119.27 kilotons, growing from 2025 value of 110.49 kilotons with 2031 projections showing 174.83 kilotons, growing at 7.95% CAGR over 2026-2031.

This report is Segmented by Source Type (Natural Quartz (Pegmatite), Synthetic Quartz (Hydrothermal/CVD), and Purified Quartz Sand (Solid-State)), Application (Semiconductor, Solar, Lighting, Telecom and Optics, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Global High Purity Quartz Market Trends and Insights

Surging Demand for Next-Gen Logic and Memory Fabs

Global equipment outlays of USD 400 billion for new 300 mm facilities scheduled between 2025 and 2027 intensify consumption of high-purity process components, including quartz crucibles, tubes, and boats. Foundries migrating to 2 nm logic nodes must control metallic contaminants at parts-per-billion thresholds, which lifts per-wafer quartz usage. Memory makers scaling high-bandwidth modules adopt larger crystal-growth furnaces requiring crucibles with tighter thermal-shock resistance. Qualification programs at Korean and Taiwanese sites now specify 4N + purity benchmarks, prompting upstream suppliers to broaden refining capacity near Asia-Pacific fabs. In the United States, CHIPS-supported plants request dual-sourced synthetic alternatives to hedge against single-mine risk, embedding long-term offtake clauses in procurement contracts.

Rising Solar-Grade Ingot Capacity Additions

Global crystalline-silicon module demand underpins a 12.40% CAGR for solar-class quartz to 2030. Chinese and Southeast Asian producers accelerate 2600 mm diameter pullers that consume larger crucibles per cycle, increasing unit quartz loadings. European manufacturers leverage Inflation Reduction Act-style incentives to localize wafers, widening regional raw-material pull. Purity criteria remain stringent-iron below 5 ppm and total impurities under 300 ppm-driving deployment of advanced acid-leach circuits in Asian beneficiation hubs. Suppliers installing closed-loop water treatment secure faster environmental approvals, shortening time-to-market.

Volatile Pegmatite Mining Output and Price Swings

In 2024, extreme price fluctuations in Chinese markets highlighted the challenges of managing a natural high purity quartz supply and inventory for downstream manufacturers. Hurricane Helene's impact on Spruce Pine operations in September 2024 exposed supply concentration risks, with Sibelco and The Quartz Corp halting operations and The Quartz Corp reporting "no visibility" on restart timelines to CNBC. The geological variability of pegmatite deposits necessitates continuous assessments and grade control, while smaller mining operations face added unpredictability from weather disruptions, equipment failures, and permitting delays. High purity quartz price volatility significantly affects semiconductor and solar manufacturers, prompting procurement teams to adopt dual-sourcing strategies and inventory buffers to mitigate supply risks.

Other drivers and restraints analyzed in the detailed report include:

- On-Shoring of Critical Mineral Supply Chains (U.S./EU)

- Emerging Ultrafast-Laser Optics Applications

- Stringent Environmental Licensing in APAC Mines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural quartz retained a 61.12% share of the high purity quartz market in 2025, mainly due to ingrained supply ties with crucible and tube fabricators. However, synthetic output is rising at an 8.68% CAGR, supported by hydrothermal capacity additions in Japan, South Korea, and the United States. The high purity quartz market size for synthetic grades is driven by consistent impurity profiles that slash wafer scrap rates in 2 nm process lines. Synthetic producers also meet European content rules without relying on politically exposed mining concessions, a decisive factor under the Critical Raw Materials Act.

Natural-grade suppliers concentrate on beneficiation upgrades to stave off share erosion. New magnetic-separation circuits remove mica and feldspar phases, while high-temperature chlorination units reduce alkali traces. The combination lifts achievable purity to 4N +, narrowing quality gaps with synthetic alternatives. Still, pegmatite output remains vulnerable to climatic events and shovel-ready reserve depletion, prompting downstream firms to diversify purchase contracts. The convergence of cost structures between the two routes reshapes bargaining dynamics as buyers weigh supply security against crystal-size requirements for specialty optics.

Complete Report Scope:

- By Source Type

- Natural Quartz (Pegmatite)

- Synthetic Quartz (Hydrothermal/CVD)

- Purified Quartz Sand (Solid-state)

- By Application

- Semiconductor

- Solar

- Lighting

- Telecom and Optics

- Microelectronics

- Other Applications

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Geography Analysis

Asia-Pacific accounted for 64.40% of 2025 consumption and is projected to post the highest 8.22% CAGR through 2031 as China expands polysilicon and Taiwan inches toward 2 nm logic production. Beijing's decision in April 2025 to classify high purity quartz as a strategic mineral accelerates exploration in Qinling and Altay while steering low-interest credit to processing hubs. Japan's materials suppliers deepen ties with domestic fabs, emphasizing synthetic routes to reduce dependence on single-mine imports. South Korea maintains a steady pull anchored by memory leadership, while Australia commercializes coastal silica projects that shorten Asian shipping lanes.

North America ranks second in usage. Spruce Pine, North Carolina, remains the world's largest source of natural HPQ blocks, and Sibelco's USD 200 million line upgrade will lift milling throughput by 2025. Local fabs under CHIPS funding tap regional synthetic startups that tout near-zero transportation emissions. Canada positions its Atlantic quartz veins as strategic feedstock, supported by streamlined federal permitting for critical minerals. The region's market trajectory hinges on the pace at which U.S. fabs ramp three new 300 mm lines, a swing factor that could shift 10 kilo tons of annual demand.

Europe high purity quartz sand market benefits from supportive policy. The Critical Raw Materials Act enforces a 10% extraction and 40% processing target within the Union by 2030. France high purity quartz sand market benefits from France's optics valley and Germany's microelectronics parks' joint pilot hydrothermal reactors that use local geothermal heat, lowering energy intensity. Scandinavian miners evaluate value addition instead of shipping crude sand. Emerging markets in South America and the Middle East start from a low base but pursue downstream integration with PV module and glass fiber chains, promising incremental yet persistent pull on global supply.

- Australian Silica Quartz Group Ltd

- Covia Holdings LLC

- Greentech Minerals Limited

- Imerys

- Jiangsu Pacific Quartz Co., Ltd

- Momentive Technologies

- Nihon Dempa Kogyo Co., Ltd.

- Russian Quartz LLC

- Sibelco

- SIMCOA

- The Quartz Corp

- ULTRA HPQ

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for next-gen logic and memory fabs

- 4.2.2 Rising solar-grade ingot capacity additions

- 4.2.3 On-shoring of critical mineral supply chains (U.S./EU)

- 4.2.4 Emerging ultrafast-laser optics applications

- 4.2.5 Synthetic-quartz cost parity vs. natural feedstock

- 4.3 Market Restraints

- 4.3.1 Volatile pegmatite mining output and price swings

- 4.3.2 Stringent environmental licensing in APAC mines

- 4.3.3 Slow qualification cycles for new HPQ vendors

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source Type

- 5.1.1 Natural Quartz (Pegmatite)

- 5.1.2 Synthetic Quartz (Hydrothermal/CVD)

- 5.1.3 Purified Quartz Sand (Solid-state)

- 5.2 By Application

- 5.2.1 Semiconductor

- 5.2.2 Solar

- 5.2.3 Lighting

- 5.2.4 Telecom and Optics

- 5.2.5 Microelectronics

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Australian Silica Quartz Group Ltd

- 6.4.2 Covia Holdings LLC

- 6.4.3 Greentech Minerals Limited

- 6.4.4 Imerys

- 6.4.5 Jiangsu Pacific Quartz Co., Ltd

- 6.4.6 Momentive Technologies

- 6.4.7 Nihon Dempa Kogyo Co., Ltd.

- 6.4.8 Russian Quartz LLC

- 6.4.9 Sibelco

- 6.4.10 SIMCOA

- 6.4.11 The Quartz Corp

- 6.4.12 ULTRA HPQ

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment