|

시장보고서

상품코드

2072535

유럽의 바이오에탄올 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Bioethanol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

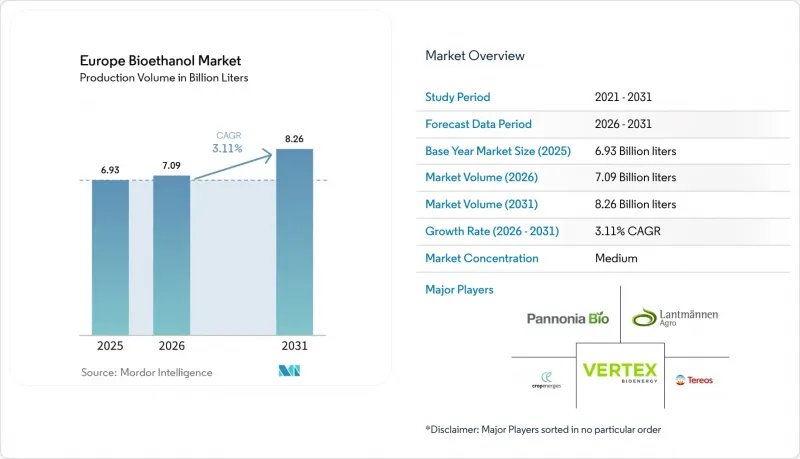

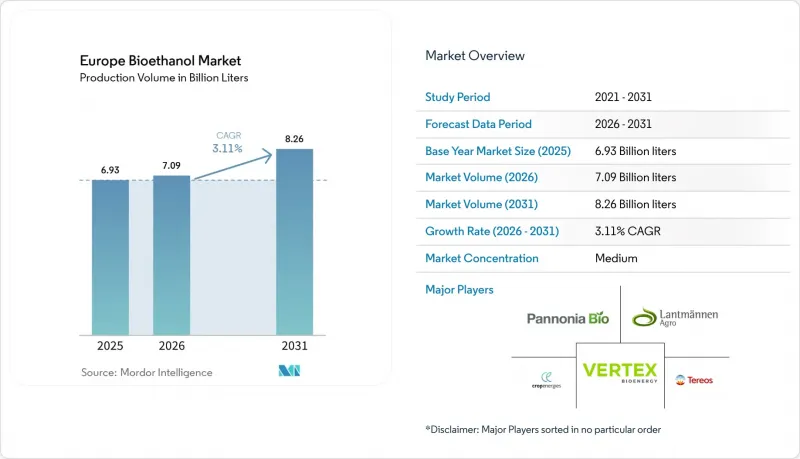

Mordor Intelligence에 의하면, 생산량 기반에서의 유럽의 바이오에탄올 시장 규모는 2025년 69억 3,000만 리터에서 2026년에는 70억 9,000만 리터로 확대되어 2026년부터 2031년에 걸쳐 CAGR 3.11%로 성장을 지속하여, 2031년에는 82억 6,000만 리터에 이를 것으로 예측됩니다.

본 보고서는 원료(밀, 옥수수, 설탕, 리그노셀룰로오스계 잔여물, 기타), 용도(연료 혼합, 식품 및 음료, 의약품, 화장품 및 퍼스널케어, 기타) 및 지역(독일, 영국, 프랑스, 스페인, 이탈리아, 북유럽 국가, 네덜란드, 폴란드 등)별로 분류되어 있습니다. 시장 규모 및 전망은 생산량(리터)으로 표시되어 있습니다.

유럽의 바이오에탄올 시장 동향 및 인사이트

RED III 의무화로 인해 재생 가능 연료 할당량이 증가

개정된 RED III에 따라 2030년까지 운송 부문의 재생에너지 비중이 29%로 높아지게 되며, 현재의 혼합 비율이 유지된다면 12억 리터의 에탄올에 대한 추가 수요가 발생할 것입니다. 프랑스와 독일은 이미 에탄올 규제 준수를 중시하는 국내 이행 로드맵을 발표한 바 있으며, 스페인과 이탈리아는 2026년까지 로드맵을 최종 확정할 예정입니다. 첨단 바이오연료의 세부 목표에서는 볏짚을 원료로 한 생산량에 대해 이중 산정이 허용되고 있으며, 이에 따라 의무 이행 주체와 프리미엄 임베디드 계약을 확실하게 체결할 수 있는 2세대 플랜트로 자본이 이동하고 있습니다. 따라서 ILUC(간접 토지 이용 변화)가 낮은 부산물임을 인증받은 생산자는 구조적인 이익률 우위를 누리며, 곡물 가격 변동에 대한 완충 역할을 하고 있습니다. 이러한 규제상의 확실성이 유럽의 바이오에탄올 시장의 꾸준한 성장을 뒷받침하고 있습니다.

EU의 다른 회원국에서의 E10/E85 도입

폴란드는 2024년 말에 전국적인 E10 주유기 전환을 완료하고, 8,000기의 주유기를 증설함에 따라 2025년 국내 바이오에탄올 사용량이 전년 대비 15% 증가했습니다. 스페인도 2025년 초에 이에 발맞추어, 레프솔(Repsol)과 세프사(Cepsa)가 판매 거점의 60%를 개보수했습니다. 이번 변경으로 인해 2027년까지 추가로 2억 리터 수요가 흡수될 것으로 예측됩니다. 독일은 2,000곳의 주유소를 E85 대응 시설로 개조하기 위한 지원 프로그램을 시작했으며, 플렉스 연료 네트워크를 프랑스와 스웨덴을 넘어 확대했습니다. 탄소 크레딧 이전 및 소비세 인하로 인해 E85는 경제적으로 매력적인 선택지가 될 것이며, 2025년에는 E10과의 가격 차이가 리터당 0.20유로로 확대되었습니다. 인프라 확충으로 블렌드 월의 제약이 해소됨에 따라, 유럽의 바이오에탄올 시장이 예상되는 연평균 성장률(CAGR) 3.11%를 뒷받침하게 될 것입니다.

원자재 가격 변동과 ‘식량 대 연료’ 논쟁

2025년, 유럽산 밀의 거래 가격은 톤당 210유로에서 280유로 사이에서 등락했으며, 30%에 달하는 가격 변동으로 인해 헤지 능력이 없는 공장의 이익률이 압박을 받았습니다. 남유럽의 가뭄으로 인해 ‘식량 대 연료’ 논쟁이 다시 불거졌으며, NGO 측에서는 곡물이 에탄올 생산에 전용되고 있다는 점에 대해 비판의 목소리가 제기되었습니다. RED III는 농작물 유래 바이오연료를 2020년 수준으로 제한하고 있지만, 2025년 중반에 빵용 밀 가격이 급등했던 스페인과 이탈리아에서는 여전히 정치적 감시가 엄격한 상황이 이어지고 있습니다. 대기업들은 수년에 걸친 곡물 계약을 체결하고 자사 부지 내에 저장 시설을 갖추고 있지만, 재무 기반이 취약한 소규모 증류업자들은 이익률 압박에 직면해 있으며, 이로 인해 업계 재편이 가속화되고 있습니다. 따라서 원자재 가격 변동은 유럽의 바이오에탄올 시장의 상승 여력을 제한하는 요인이 되고 있습니다.

부문별 분석

2025년, 헝가리, 루마니아 및 중부 유럽에 대규모 건식 제분 시설이 구축됨에 따라, 옥수수는 유럽의 바이오에탄올 생산량의 50.2%를 차지했습니다. 이러한 압도적인 점유율은 유럽의 바이오에탄올 산업에서 옥수수가 차지하는 지극히 중요한 역할을 여실히 보여주고 있습니다. 한편, 리그노셀룰로오스계 잔류물은 2031년까지 연평균 성장률(CAGR) 6.2%로 확대될 것으로 전망됩니다. 이러한 급증의 원동력은 점점 더 엄격해지는 탈탄소화 규제에 대응하기 위해 생산자들이 농업 폐기물 및 임산물 기반의 첨단 에탄올 생산을 확대하고 있기 때문입니다. 프랑스, 독일, 영국에서 주요 원료인 밀은 제분 인프라와의 통합 및 유연한 원료 경제성이라는 이점을 누리고 있습니다. 설탕은 사탕무 가공 및 지역 농업 관련 기업이 운영하는 시설에서의 공동 발효의 장점을 활용하고 있습니다. 또한, 그 밖의 원료로는 파일럿 규모 및 상업 규모 시설에서 처리되는 혼합 바이오매스와 특수 농업 잔여물이 포함됩니다.

2세대 바이오에탄올 생산은 이중 산입 크레딧의 혜택을 받아 높은 설비 투자 비용을 상쇄할 수 있는 가격 프리미엄을 얻을 수 있기 때문에 탄소 가격 규제가 엄격한 지역에서는 밀의 수익성 우위가 점차 약화되고 있습니다. Verbio사의 모듈식 접근 방식은 짚 수집과 기존 증류 라인을 통합한 것으로, 5만 톤 규모의 모듈당 1억 5,000만-2억 유로(약 1억 7,400만-2억 3,200만 달러)의 비용이 소요되며, 그린필드 건설에 비해 투자 장벽을 낮추고 있습니다. CropEnergies사는 자사의 차이츠(Zeitz) 사업장에서 이 모델을 재현하여, 2027년까지 3만 톤의 첨단 생산 능력을 추가할 계획입니다. 2031년까지는 옥수수가 유럽의 바이오에탄올 시장에서 가장 큰 점유율을 차지할 것으로 전망되지만, 탄소 감축 목표와 원료 다각화 전략에 힘입어 리그노셀룰로오스계 잔여물의 점유율이 확대됨에 따라 그 우위는 점차 약화될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the europe bioethanol market size in terms of production volume is expected to grow from 6.93 Billion liters in 2025 to 7.09 Billion liters in 2026 and is forecast to reach 8.26 Billion liters by 2031 at 3.11% CAGR over 2026-2031.

This report is Segmented by Feedstock (Wheat, Corn, Sugars, Lignocellulosic Residues, and Other), Application (Fuel Blending, Food and Beverages, Pharmaceuticals, Cosmetics and Personal Care, and Others), and Geography (Germany, United Kingdom, France, Spain, Italy, NORDIC Countries, Netherlands, Poland, and More). The Market Sizes and Forecasts are Provided in Terms of Production Volume (Liters).

Europe Bioethanol Market Trends and Insights

RED III Mandates Raise Renewable-Fuel Quotas

Revised RED III lifts the renewable share in transport to 29% by 2030, triggering incremental demand for 1.2 billion liters of ethanol if current blend levels persist. France and Germany have already published national transposition roadmaps that emphasize ethanol compliance, while Spain and Italy intend to finalize theirs in 2026. Advanced-biofuel sub-targets grant double counting for straw-based volumes, shifting capital toward second-generation plants that can lock in premium off-take contracts with obligated parties. Producers that certify low-ILUC residues therefore enjoy structural margin advantages, cushioning them against grain-price swings. This regulatory certainty underpins the steady expansion of the European bioethanol market.

Roll-Out of E10 / E85 Across Additional EU States

Poland completed nationwide E10 pump conversions in late 2024, adding 8,000 dispensers and lifting domestic bioethanol use by 15% year on year in 2025. Spain followed in early 2025 as Repsol and Cepsa upgraded 60% of their outlets, a change that is expected to absorb an extra 200 million liters by 2027. Germany launched a grant program to retrofit 2,000 stations for E85, broadening the flex-fuel network beyond France and Sweden. Carbon-credit transfers and lower excise taxes make E85 economically attractive, widening the price gap with E10 to €0.20 per liter in 2025. Expanded infrastructure removes blend-wall constraints, supporting the projected 3.11% CAGR of the European bioethanol market.

Feedstock-Price Volatility and Food-Versus-Fuel Debate

European wheat traded between €210 and €280 per ton in 2025, a 30% swing that compressed margins for plants lacking hedging capacity. Drought in Southern Europe rekindled the food-fuel debate as NGOs criticized the diversion of cereals to ethanol. RED III caps crop-based biofuels at 2020 levels, yet political scrutiny remains high in Spain and Italy, where bread-wheat prices spiked during mid-2025. Larger players lock multiyear grain contracts and build on-site storage, but small distillers without balance-sheet strength face margin squeezes that accelerate consolidation. Volatile feedstock, therefore, restricts upside for the European bioethanol market.

Other drivers and restraints analyzed in the detailed report include:

- Carbon-Pricing and GHG-Credit Premiums Enhance Economics

- Alcohol-to-Jet Pathway Inclusion in ReFuelEU Aviation

- ILUC-Factor Compliance Increases Certification Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, corn accounted for 50.2% of bioethanol production in Europe, bolstered by extensive dry-mill facilities in Hungary, Romania, and Central Europe. This dominance underscores corn's pivotal role in Europe's bioethanol landscape. Meanwhile, lignocellulosic residues are projected to grow at a 6.2% CAGR through 2031. This surge is driven by producers ramping up advanced ethanol production from agricultural waste and forestry by-products, all in a bid to align with tightening decarbonization mandates. Wheat, a key feedstock in France, Germany, and the UK, enjoys advantages from its integration with milling infrastructure and adaptable feedstock economics. Sugars benefit from sugar beet processing and co-fermentation perks at facilities run by local agribusinesses. Additionally, other feedstocks encompass mixed biomass and specialized agricultural residues, processed at both pilot and commercial-scale facilities.

Second-generation output enjoys double-counting credits and commands price premiums that offset higher capex, eroding wheat's margin advantage where carbon pricing is stringent. Verbio's modular approach, integrating straw collection with existing distillation trains at EUR 150-200 million (~ USD 174-232 million) per 50,000-ton module, lowers investment hurdles compared with greenfield builds. CropEnergies will replicate the model at its Zeitz site, adding 30,000 tons of advanced capacity by 2027. While corn is set to command the largest share of Europe's bioethanol market until 2031, its dominance will wane as lignocellulosic residues capture an increasing share, propelled by carbon reduction goals and strategies for feedstock diversification.

Complete Report Scope:

- By Feedstock

- Wheat

- Corn

- Lignocellulosic Residues

- Sugars

- Other

- By Application

- Fuel Blending (Transportation)

- Food and Beverages (Spirits, Extracts)

- Pharmaceuticals

- Cosmetics and Personal Care

- Others

- By Geography

- Germany

- United Kingdom

- France

- Spain

- Italy

- NORDIC Countries

- Netherlands

- Poland

- Russia

- Rest of Europe

List of Companies Covered in this Report:

- CropEnergies AG

- Vertex Bioenergy

- Tereos SCA

- Pannonia Bio Zrt.

- Lantmannen Agroetanol

- Abengoa

- ADM

- AGRANA Beteiligungs-AG

- Cargill

- ALCOGROUP SA

- Anora Group Plc

- BIOAGRA S.A.

- Verbio SE

- Clariant AG

- British Sugar plc

- Vivergo Fuels

- BioWanze SA

- Euro Ethyl Ltd.

- Essentica Ltd.

- Tereos Syral (France)

- Ryssen Alcool (France)

- Sekab E-Technology AB

- Green Biologics Ltd.

- Ryazan (Valio Biofuels)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 RED III mandates raise renewable-fuel quotas

- 4.2.2 Roll-out of E10/E85 across additional EU states

- 4.2.3 Carbon-pricing & GHG-credit premiums enhance ethanol economics

- 4.2.4 Alcohol-to-Jet pathway inclusion in ReFuelEU Aviation

- 4.2.5 Monetisation of "green" CO2 from fermentation streams

- 4.2.6 Protein-rich co-products boost integrated biorefinery margins

- 4.3 Market Restraints

- 4.3.1 Feedstock-price volatility & food-versus-fuel debate

- 4.3.2 ILUC-factor compliance increases certification costs

- 4.3.3 High energy-price swings hit distillation economics

- 4.3.4 EV & e-fuel policy signals cap long-term gasoline pool

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook (1G vs 2G, ATJ)

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Feedstock

- 5.1.1 Wheat

- 5.1.2 Corn

- 5.1.3 Lignocellulosic Residues

- 5.1.4 Sugars

- 5.1.5 Other

- 5.2 By Application

- 5.2.1 Fuel Blending (Transportation)

- 5.2.2 Food and Beverages (Spirits, Extracts)

- 5.2.3 Pharmaceuticals

- 5.2.4 Cosmetics and Personal Care

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Spain

- 5.3.5 Italy

- 5.3.6 NORDIC Countries

- 5.3.7 Netherlands

- 5.3.8 Poland

- 5.3.9 Russia

- 5.3.10 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 CropEnergies AG

- 6.4.2 Vertex Bioenergy

- 6.4.3 Tereos SCA

- 6.4.4 Pannonia Bio Zrt.

- 6.4.5 Lantmannen Agroetanol

- 6.4.6 Abengoa

- 6.4.7 ADM

- 6.4.8 AGRANA Beteiligungs-AG

- 6.4.9 Cargill

- 6.4.10 ALCOGROUP SA

- 6.4.11 Anora Group Plc

- 6.4.12 BIOAGRA S.A.

- 6.4.13 Verbio SE

- 6.4.14 Clariant AG

- 6.4.15 British Sugar plc

- 6.4.16 Vivergo Fuels

- 6.4.17 BioWanze SA

- 6.4.18 Euro Ethyl Ltd.

- 6.4.19 Essentica Ltd.

- 6.4.20 Tereos Syral (France)

- 6.4.21 Ryssen Alcool (France)

- 6.4.22 Sekab E-Technology AB

- 6.4.23 Green Biologics Ltd.

- 6.4.24 Ryazan (Valio Biofuels)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment