|

시장보고서

상품코드

2072539

특정 용도용 통신 아날로그 IC : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Application Specific Communications Analog IC - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

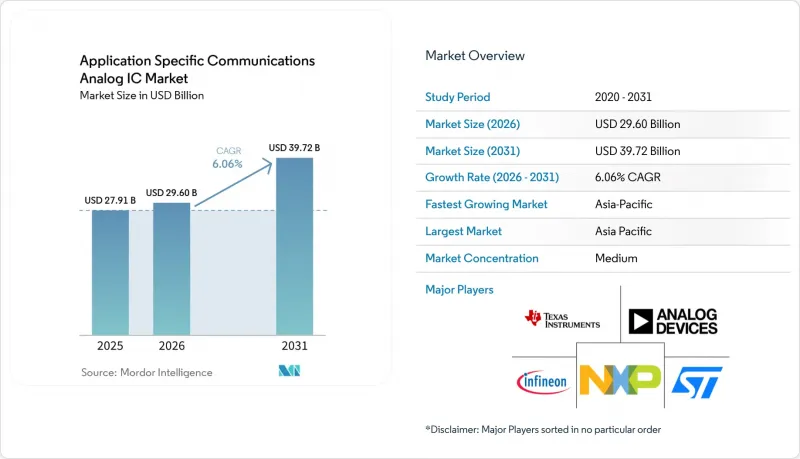

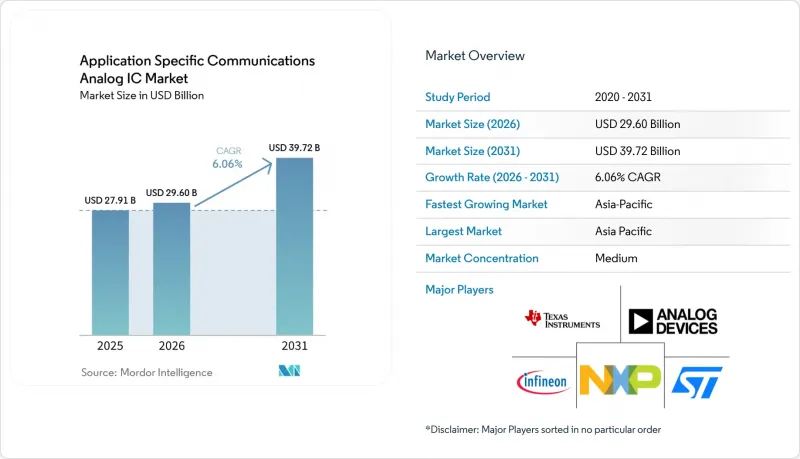

Mordor Intelligence에 의하면, 특정 용도용 통신 아날로그 IC시장 규모는 2025년에 279억 1,000만 달러로 평가되었습니다. 2026년 296억 달러에서 2031년까지 397억 2,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 6.06%를 나타낼 전망입니다.

본 보고서는 제품 유형(RF 트랜시버 IC, 전력 관리 IC, 기타), 통신 표준(5G NR, 4G LTE 및 LTE-Advanced, 기타), 용도(통신 인프라, 스마트폰 및 모바일 기기, 기타), 최종 사용자 산업(통신 사업자, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 특정 용도용 통신 아날로그 IC 시장 동향 및 인사이트

전 세계 5G 인프라의 보급

2024년에는 상용 5G 네트워크 구축 수가 329곳에 달했고, 21억 건의 연결을 제공했으며, 통신 사업자들은 2029년까지 이 수치가 86억 건을 넘어설 것으로 계획하고 있습니다. 새로운 기지국에는 노이즈 피겨가 1 dB 이하인 아날로그 프런트엔드 모듈과 내열성이 뛰어난 파워 앰프가 필요하며, 이로 인해 4G 무선 기기에 비해 부품 원가가 약 40% 증가했습니다. 차이나 모바일은 2024년에 5G 업그레이드에 1,800억 위안(252억 달러)을 투자한 반면, 버라이즌은 미국 내 미드밴드 커버리지 확대에 185억 달러를 배정했습니다. Open RAN 검사 시스템의 도입으로 인해, 타이밍 IC 및 인터페이스 컨트롤러에 사용되는 IC 소켓 솔루션에 대한 새로운 수요가 발생하고 있습니다. 한편, 에너지 효율에 대해서는 여전히 검토가 진행 중입니다. 네트워크 슬라이싱을 지원하는 엣지 컴퓨팅 엔진 덕분에, 광대역 데이터 컨버터를 좁은 선형성 범위 내에 유지하는 고정밀 전압 레퍼런스에 대한 수요가 더욱 증가하고 있습니다.

IoT 기기 도입의 급증으로 저전력 아날로그 프론트엔드 시장 확대

2024년 셀룰러 IoT 모듈 출하량은 4억 2,300만 대에 달했으며, NB-IoT 연결 건수는 2배인 19억 건으로, LoRa 연결 건수는 2030년까지 13억 건에 이를 것으로 전망됩니다. 현재 산업용 센서는 10년의 배터리 수명을 목표로 하고 있기 때문에 설계자들은 정지 전류를 1마이크로암페어 이하로 억제하고, 에너지 수확 기능을 칩에 통합하기 위해 노력하고 있습니다. 유럽과 아시아태평양의 스마트시티 계량 계약에서는 면허 대역의 신뢰성을 이유로 NB-IoT가 주류로 자리 잡고 있는 반면, 북미의 농업 및 물류 업체에서는 인프라 비용 절감을 위해 LoRa가 선호되고 있습니다. 20일 동안 출하된 Nordic Semiconductor의 nRF54 플랫폼은 멀티프로토콜 무선 기술이 부품 목록을 얼마나 간소화하는지 보여줍니다. 자산 추적 장치나 웨어러블 단말기에서는 AI 추론이 대두되고 있으며, 그 결과 동적 전압 스케일링 및 센서 인터페이스의 유연성을 갖춘 아날로그 프론트엔드에 대한 수요가 증가하고 있습니다.

설계의 복잡화와 검증 비용 증가

2024년에는 단일 다이 내에서 RF, 전원, 디지털 영역에 걸친 혼합 신호 검증이 수행됨에 따라, 고성능 아날로그 부품의 설계 주기가 최대 24개월에 달하게 되었습니다. 다중 표준 준수로 인해 트랜지스터 수가 증가하고 기생 상호작용도 발생함에 따라, 최첨단 무선 모듈의 비반복 설계 비용(NRE)은 500만 달러를 넘어섰습니다. 자동 레이아웃 도구는 디지털 EDA에 비해 약 10년 뒤처져 있으며, 수동 배치가 필요하기 때문에 엔지니어링 인건비가 증가하고 있습니다. 28nm 이하의 첨단 공정 노드에서는 일렉트로마이그레이션 및 핫 캐리어 주입에 대한 새로운 신뢰성 검사가 도입되었으며, 각각에 대해 철저한 코너 시뮬레이션이 요구됩니다. 소규모 팹리스 기업들은 심각한 자금난에 직면해 있으며, 폭넓은 제품 포트폴리오를 통해 비용을 상쇄할 수 있는 기존 기업들에게 고성능 부문을 양도하는 경우가 늘고 있습니다.

부문별 분석

RF 무전기 IC 부문은 2025년에 83억 달러 시장 규모를 기록했으며, 2031년까지 연평균 성장률(CAGR) 8.45%를 유지할 전망인데, 이는 특정 용도용 통신 아날로그 IC 시장 전체의 성장률을 상회하는 수치입니다. 5G 기지국, Wi-Fi 6E 라우터, 77GHz 자동차용 레이더에 탑재되는 Sub-6GHz 및 mm파 무선 기기가 이 카테고리의 용도 특화형 통신 아날로그 IC 시장 전체 규모를 끌어올리고 있으며, 노이즈 피겨 1 dB 이하와 출력 레벨 26 dBm을 실현하는 제품에 대한 프리미엄 가격 책정이 이를 뒷받침하고 있습니다. 각 벤더는 파워 앰프, 저잡음 증폭기, 필터를 불과 3mm×4mm 크기의 모듈에 집적하고 있으며, 이를 통해 휴대전화 단말기 및 CPE 설계자들은 기판 면적을 줄일 수 있게 되었습니다. 또한, 소프트웨어 업그레이드 시 현장 대응(트랙 롤)을 최소화하기 위해, 동일한 하드웨어 내에서 광대역 및 멀티캐리어 지원이 요구되는 Open RAN의 도입으로 인해 수요가 더욱 증가하고 있습니다.

2025년에는 파워 매니지먼트 IC가 용도 특화형 통신용 아날로그 IC 시장에서 31.68%의 점유율을 차지했으나, 저전압 조정기의 상품화 및 중국 IDM 기업들의 치열한 가격 압박으로 인해 매출 성장률은 시장 전체의 성장 속도를 약간 밑도는 수준에 그칠 것으로 전망됩니다. 데이터 변환기 IC는 여전히 틈새 시장이지만, 코히런트 광통신 및 검사 장비 분야에서는 채널당 150달러가 넘는 판매 가격을 실현하고 있습니다. 클럭·타이밍 IC는 5G 전송 네트워크에서 동기식 이더넷의 흐름에 편승하고 있는 반면, 인터페이스 IC는 10 Gbps 신호 전송으로 전환되는 USB-C 및 자동차용 이더넷 PHY의 보급에 따라 시장이 확대되고 있습니다.

5G NR은 연평균 성장률(CAGR) 12.1%를 기록하며, 특정 용도용 통신 아날로그 IC 시장에서 가장 빠르게 성장하는 부문으로서의 입지를 공고히할 것으로 보입니다. 독립형 5G 코어에는 서브 6GHz 대역과 mm파 대역을 모두 지원하는 무선 모듈이 필요하며, 대부분의 통신 사업자가 4G를 단계적으로 오버레이하는 방식 대신 플랫폼 전체를 교체하는 방식을 선택함에 따라 프런트엔드 매출을 견인하고 있습니다. 기업용 및 가정용 게이트웨이 분야의 Wi-Fi 6E 업데이트 주기도 추가적인 성장 동력을 제공하고 있는데, 특히 6GHz 대역에서는 간섭을 줄이기 위해 집적형 음향파 필터가 필요하기 때문입니다.

4G LTE와 LTE-Advanced는 여전히 큰 규모를 유지하고 있으며, 2025년에는 46.85%의 점유율을 차지하여 신흥 시장의 매크로셀에서 아날로그 IC 수요를 지속적으로 뒷받침했습니다. 저전력 광역 네트워크(LPWAN)는 규제 환경의 차이에 따라 NB-IoT와 LoRa로 나뉘며, 두 기술 모두 순수한 대역폭보다는 초저전력 프론트엔드가 요구됩니다. 따라서 비용 대비 성능의 최적화가 결정적인 차별화 요소가 됩니다. 위성 통신 및 미션 크리티컬 통신 링크는 규모는 작지만 수익성이 높은 부문을 차지하고 있으며, 내방사선성 GaN 전력 증폭기나 SiGe 저잡음 증폭기가 선호됩니다. 이 제품들의 수명은 5년 이상입니다.

지역별 분석

아시아태평양은 2025년 매출의 62.74%를 차지했습니다. 중국이 자급자족을 위해 지출을 확대하고, 대만이 특수 파운드리 부문에서 리더십을 유지하며, 인도가 100억 달러 규모의 인센티브 기금을 통해 신규 팹 건설에 자금을 투입하고 있는 만큼, 다른 어떤 지역보다 빠른 연평균 성장률(CAGR) 9.18%로 성장할 것으로 전망됩니다. 중국의 제3차 반도체 투자 펀드는 3,440억 위안(482억 달러)의 자본금을 보유하고 있으며, 아날로그 설계 회사와 화합물 반도체 파브에 자금을 지원하고 있습니다. 대만 반도체 제조 회사(TSMC)는 성숙한 공정 노드에서 이미 월20만 장 이상의 아날로그 웨이퍼 생산을 시작했으며, RF, 파워, 데이터 컨버터 분야의 고객사를 대규모로 지원하고 있습니다.

북미 시장 점유율은 약 18.41%였으나, 527억 달러 규모의 ‘“CHIPS법”에 의한 보조금이 국내 생산 능력을 강화할 것으로 전망됩니다. TSMC가 650억 달러를 투자한 애리조나 캠퍼스에서는 2024년에 28nm 및 16nm 아날로그 소자의 생산이 시작되었습니다. 인텔이 200억 달러를 투자한 오하이오주의 복합 시설은 180nm 및 130nm 자동차용 및 산업용 아날로그 노드를 대상으로 하고 있습니다. 유럽 시장 점유율은 약 12.16%이며, 프랑스의 자동차 수요를 뒷받침하기 위해 STMicroelectronics와 전 세계 파운드리 업체들의 공동 투자의 혜택을 받고 있습니다. 남미와 중동 시장 점유율은 여전히 작지만, 위성 지상국 구축 및 유전 원격 측정 분야는 견고한 아날로그 IC에 있어 수익성이 높은 틈새 시장으로 자리 잡고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the application-specific communications analog IC market size was valued at USD 27.91 billion in 2025 and estimated to grow from USD 29.6 billion in 2026 to reach USD 39.72 billion by 2031, at a CAGR of 6.06% during the forecast period (2026-2031).

This report is Segmented by Product Type (RF Transceiver ICs, Power Management ICs, and More), Communication Standard (5G NR, 4G LTE/LTE-A, and More), Application (Telecom Infrastructure, Smartphones and Mobile Devices, and More), End-User Industry (Telecommunication Operators, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Application Specific Communications Analog IC Market Trends and Insights

Proliferation of 5G Infrastructure Worldwide

Commercial 5G networks reached 329 deployments, serving 2.1 billion connections in 2024, and operators plan to surpass 8.6 billion by 2029.Each new base station requires analog front-end modules with sub-1 dB noise figures and thermally robust power amplifiers, increasing the bill of materials value over 4G radios by approximately 40%.China Mobile spent CNY 180 billion (USD 25.2 billion) on 5G upgrades in 2024, while Verizon allocated USD 18.5 billion to extend mid-band coverage in the United States. Open RAN trials add fresh demand for IC socket solutions used in timing ICs and interface controllers, even as energy efficiency remains under review. Edge computing engines that support network slicing further raise demand for precision voltage references that keep wide-bandwidth data converters within tight linearity windows.

Surge in IoT Device Deployments Driving Low-Power Analog Front-Ends

Cellular IoT module shipments reached 423 million units in 2024, with NB-IoT connections set to double to 1.9 billion and LoRa connections forecast to reach 1.3 billion by 2030.Industrial sensors now target ten-year battery life, so designers push quiescent current below one microamp and integrate energy-harvesting support on-chip. Smart-city metering contracts across Europe and the Asia Pacific tend toward NB-IoT for licensed-spectrum reliability, while agriculture and logistics operators in North America favor LoRa for lower infrastructure costs. Nordic Semiconductor's nRF54 platform, which shipped in 20 days, demonstrates how multi-protocol radio simplifies the bill of materials. AI inference is emerging in asset trackers and wearables, which in turn pulls in analog front-ends capable of dynamic voltage scaling and sensor-interface flexibility.

Escalating Design Complexity and Verification Costs

Design cycles for advanced analog parts stretched to up to 24 months in 2024 as mixed-signal verification spanned RF, power, and digital domains within a single die. Non-recurring engineering expenses exceeded USD 5 million for leading-edge radios, as multi-standard compliance increased transistor counts and parasitic interactions. Automated layout tools lag behind digital EDA by around ten years, necessitating manual placement that increases engineering labor costs. Advanced process nodes below 28 nm introduce fresh reliability checks for electromigration and hot-carrier injection, each demanding exhaustive corner simulations. Smaller fabless companies face a pronounced cash strain, often ceding high-performance segments to incumbents that can amortize costs across broad product portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for High-Speed Data Converters in Optical Networks

- Electrification and Connectivity in Automobiles Boosting In-Vehicle Analog ICs

- Geopolitical Export Controls on Advanced Process Nodes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The RF transceiver segment captured USD 8.3 billion in 2025 and is on track for an 8.45% CAGR, which outpaces the application-specific communications analog IC market through 2031. Sub-6 GHz and millimeter-wave radios inside 5G base stations, Wi-Fi 6E routers, and 77 GHz automotive radars lift the overall application-specific communications analog IC market size for this category, supported by premium pricing for sub-1 dB noise figures and 26 dBm output levels. Vendors merge power amplifiers, low-noise amplifiers, and filters in modules as small as 3 mm by 4 mm, shrinking board area for handset and CPE designers. Demand is further heightened by Open RAN deployments that require wide-bandwidth, multi-carrier support within the same hardware to minimize the need for truck rolls during software upgrades.

Although power management ICs held 31.68% of the application-specific communications analog IC market share in 2025, the commoditization of low-voltage regulators and intense price pressure from Chinese IDMs will likely limit their revenue growth to just shy of the market pace. Data converter ICs remain a niche, yet they fetch selling prices above USD 150 per channel in coherent optics or test equipment. Clock-and-timing ICs ride the synchronous Ethernet wave in 5G transport networks, while interface ICs expand with USB-C and automotive Ethernet PHYs that move toward 10 Gbps signaling.

5G New Radio will post a 12.1% CAGR, solidifying its position as the fastest riser within the application-specific communications analog IC market. Stand-alone 5G cores require radios that span both sub-6 GHz and millimeter-wave bands, driving front-end sales because most operators opt for complete platform swap-outs rather than incremental 4G overlays. Wi-Fi 6E refresh cycles in enterprise and residential gateways create further momentum, particularly as the 6 GHz band needs integrated acoustic-wave filters to mitigate interference.

4G LTE and LTE-Advanced still deliver scale, holding 46.85% share in 2025 and sustaining analog IC demand in emerging-market macro cells. Low-power wide-area networks are split between NB-IoT and LoRa by their regulatory environments, each calling for ultra-low-power front-ends rather than raw bandwidth, which makes price-performance optimization a decisive differentiator. Satellite and mission-critical links occupy a small but lucrative corner that prefers radiation-hardened GaN power amplifiers and SiGe low-noise amplifiers, where lifetimes extend five years or more.

Complete Report Scope:

- By Product Type

- RF Transceiver ICs

- Power Management ICs

- Data Converter ICs

- Clock and Timing ICs

- Interface ICs

- By Communication Standard

- 5G NR

- 4G LTE / LTE-A

- Wi-Fi 6 and 6E

- IoT LPWAN (NB-IoT, LoRa, Sigfox)

- Satellite and Critical Comms

- By Application

- Telecom Infrastructure

- Smartphones and Mobile Devices

- IoT Edge Devices

- Automotive Communication Systems

- Industrial Automation and Robotics

- By End-user Industry

- Telecommunication Operators

- Consumer Electronics OEMs

- Automotive OEMs and Tier 1s

- Industrial OEMs

- Aerospace and Defense Contractors

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Southeast Asia

- Oceania

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- North America

Geography Analysis

The Asia Pacific region accounted for 62.74% of 2025 revenue and is projected to compound at 9.18%, faster than any other region, as China increases its self-sufficiency spending, Taiwan maintains its leadership in specialty foundries, and India funds new fabs through its USD 10 billion incentive pool. China's third semiconductor investment fund, capitalized at CNY 344 billion (USD 48.2 billion), channels capital toward analog design houses and compound semiconductor fabs. Taiwan Semiconductor Manufacturing Company already exceeds 200,000 analog wafer starts per month on mature nodes, supporting RF, power, and data converter customers at scale.

North America held approximately an 18.41% share, but the CHIPS Act subsidies, valued at USD 52.7 billion, are expected to bolster domestic capacity. TSMC's USD 65 billion Arizona campus began production of 28 nm and 16 nm analog devices in 2024. Intel's USD 20 billion Ohio complex targets automotive and industrial analog nodes at 180 nm and 130 nm. Europe, at roughly 12.16%, benefits from STMicroelectronics' and GlobalFoundries' joint investments to support automotive demand in France. South America and the Middle East remain small, but satellite ground station deployment and oil-field telemetry provide profitable niches for rugged analog ICs.

- Texas Instruments Incorporated

- Analog Devices, Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- STMicroelectronics N.V.

- Skyworks Solutions, Inc.

- Qorvo, Inc.

- Microchip Technology Incorporated

- Renesas Electronics Corporation

- ON Semiconductor Corporation

- Broadcom Inc.

- Marvell Technology, Inc.

- Qualcomm Incorporated

- MediaTek Inc.

- Rohm Co., Ltd.

- Cirrus Logic, Inc.

- Silicon Laboratories Inc.

- Diodes Incorporated

- Semtech Corporation

- MaxLinear, Inc.

- Novosense Microelectronics Co., Ltd.

- Chipanalog Microelectronics Co., Ltd.

- SkyWater Technology Foundry, Inc.

- Nordic Semiconductor ASA

- Realtek Semiconductor Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 5G Infrastructure Worldwide

- 4.2.2 Surge in IoT Device Deployments Driving Low-Power Analog Front-Ends

- 4.2.3 Rising Demand for High-Speed Data Converters in Optical Networks

- 4.2.4 Growth of Software-Defined Radios and Open RAN Architectures

- 4.2.5 Electrification and Connectivity in Automobiles Boosting In-Vehicle Analog ICs

- 4.2.6 National Semiconductor Reshoring Initiatives Unlocking Capex Cycles

- 4.3 Market Restraints

- 4.3.1 Escalating Design Complexity and Verification Costs

- 4.3.2 Geopolitical Export Controls On Advanced Process Nodes

- 4.3.3 Analog Talent Shortage Slowing Time-to-Market

- 4.3.4 Supply-Chain Volatility in Specialty Wafers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 RF Transceiver ICs

- 5.1.2 Power Management ICs

- 5.1.3 Data Converter ICs

- 5.1.4 Clock and Timing ICs

- 5.1.5 Interface ICs

- 5.2 By Communication Standard

- 5.2.1 5G NR

- 5.2.2 4G LTE / LTE-A

- 5.2.3 Wi-Fi 6 and 6E

- 5.2.4 IoT LPWAN (NB-IoT, LoRa, Sigfox)

- 5.2.5 Satellite and Critical Comms

- 5.3 By Application

- 5.3.1 Telecom Infrastructure

- 5.3.2 Smartphones and Mobile Devices

- 5.3.3 IoT Edge Devices

- 5.3.4 Automotive Communication Systems

- 5.3.5 Industrial Automation and Robotics

- 5.4 By End-user Industry

- 5.4.1 Telecommunication Operators

- 5.4.2 Consumer Electronics OEMs

- 5.4.3 Automotive OEMs and Tier 1s

- 5.4.4 Industrial OEMs

- 5.4.5 Aerospace and Defense Contractors

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Taiwan

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Oceania

- 5.5.4.8 Rest of Asia Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Texas Instruments Incorporated

- 6.4.2 Analog Devices, Inc.

- 6.4.3 Infineon Technologies AG

- 6.4.4 NXP Semiconductors N.V.

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Skyworks Solutions, Inc.

- 6.4.7 Qorvo, Inc.

- 6.4.8 Microchip Technology Incorporated

- 6.4.9 Renesas Electronics Corporation

- 6.4.10 ON Semiconductor Corporation

- 6.4.11 Broadcom Inc.

- 6.4.12 Marvell Technology, Inc.

- 6.4.13 Qualcomm Incorporated

- 6.4.14 MediaTek Inc.

- 6.4.15 Rohm Co., Ltd.

- 6.4.16 Cirrus Logic, Inc.

- 6.4.17 Silicon Laboratories Inc.

- 6.4.18 Diodes Incorporated

- 6.4.19 Semtech Corporation

- 6.4.20 MaxLinear, Inc.

- 6.4.21 Novosense Microelectronics Co., Ltd.

- 6.4.22 Chipanalog Microelectronics Co., Ltd.

- 6.4.23 SkyWater Technology Foundry, Inc.

- 6.4.24 Nordic Semiconductor ASA

- 6.4.25 Realtek Semiconductor Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment