|

시장보고서

상품코드

2072545

우주 상황 인식 시스템 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Space Situational Awareness (SSA) Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

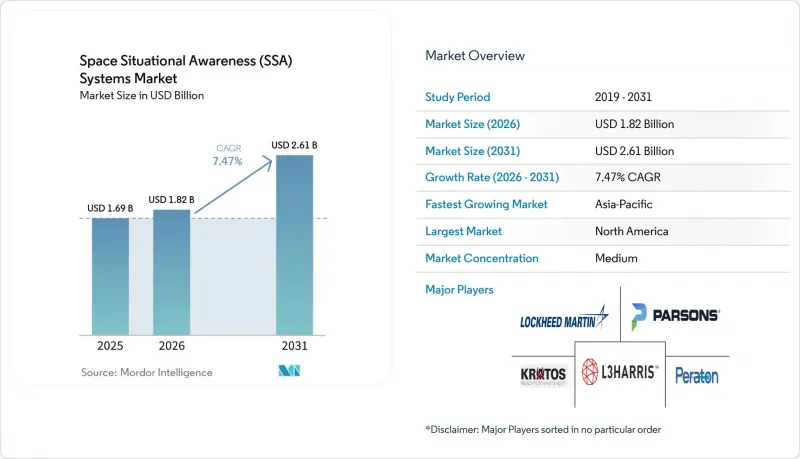

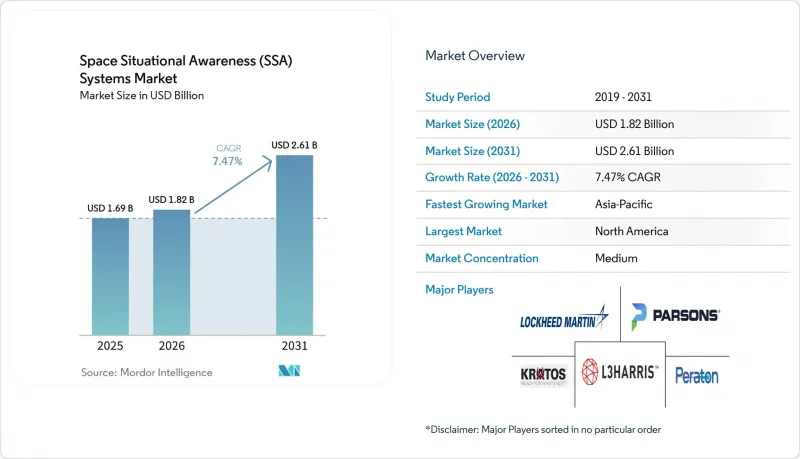

Mordor Intelligence에 의하면, 우주 상황 인식 시스템 시장 규모는 2025년 16억 9,000만 달러로 평가되었습니다. 2026년에는 18억 2,000만 달러로 확대할 것으로 예상되고 있습니다.

본 보고서는 솔루션별(서비스, 소프트웨어, 분석 플랫폼), 궤도 범위별(저지구 궤도, 심우주), 기능별(추적·모니터링 센서, 데이터 융합·예측 소프트웨어 등), 최종 사용자별(정부 및 군, 민간 기업), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 우주 상황 인식 시스템 시장 동향 및 인사이트

심우주 및 행성 탐사 임무의 빈도 증가

달 궤도 운용 및 달 표면 물류는 구상 단계에서 본격적인 프로그램 실행 단계로 전환되고 있으며, 감시 범위가 확대됨에 따라 지구와 달 사이의 거리를 아우르며 감시를 유지할 수 있는 추적 아키텍처에 대한 투자를 촉진하고 있습니다. NASA의 “'아르테미스'계획, 달 게이트웨이 건설, 그리고 지속적인 달 과학 우선 과제로 인해, 향후 10년 동안에도 심우주 관련 요구 사항이 계속해서 주목받고 있으며, 기존의 지구 근접 시스템으로는 완전히 대응하기 어려운 자율적인 궤도 결정 및 높은 지연 시간이 수반되는 작업 할당에 대한 수요가 증가하고 있습니다. 유럽우주국(ESA)이 제시한 유럽의 우선순위에서는 달 궤도 및 그보다 더 높은 궤도 영역에서 발생하는 가시성 공백을 메우는 보완적인 유럽 우주 영역 인식(Space Domain Awareness) 대책이 강조되고 있습니다.

달 탐사 임무의 통합과 발사가 진행됨에 따라, 운용 담당자들은 고출력·대구경 센서, 수 일에 걸친 상관 분석 알고리즘, 그리고 기존의 두 물체 문제라는 틀을 넘어선 섭동을 모델링하는 소프트웨어를 필요로 하고 있습니다. 이러한 기능들은 하드웨어의 복잡성과 높은 계산 부하로 인해 고가 제품군에 속합니다. 그러나 달 궤도 공간에서의 랑데부 운용이나 고가치 탑재체를 보호해야 하는 기관 및 기업에게 있어, 이러한 요소들은 지속적인 경쟁 우위를 가져다줍니다. 따라서 주요 국가 프로그램에서 달 물류 및 행성 탐사선이 안정적인 임무 라인으로 자리 잡아가면서, 우주 상황 인식 시스템 시장에서는 심우주에서의 관리 과제에 대응하기 위한 연구 개발이 진행되고 있습니다.

우주 영역 인식 능력에 대한 전략적 국방 투자

2026년도 국방 예산은 우주 영역 인식, 미사일 경계, 그리고 견고한 지상 부문에 계속해서 중점을 두고 있으며, 센서, 데이터 융합 플랫폼 및 상용 데이터 서비스에 대한 다년간의 조달을 지원하고 있습니다. 미국 우주군이 2026 회계연도에 요청한 399억 달러(전년 대비 113억 달러 증가) 규모의 예산에서는 지상 및 우주 영역 인식, 차세대 미사일 추적, 그리고 사이버 공격에 견딜 수 있는 인프라에 막대한 자원이 배정되어 있습니다. 다층적 추적 시스템과 적외선 감지 기술을 중심으로 한 조달 프로그램은 다중 궤도에서의 견고성과 신속한 업데이트로의 전환을 상징하며, 센서, 버스, 페이로드, 자율 제어 소프트웨어를 공급하는 산업 기반을 지원하는 계약이 체결되었습니다.

동맹국들의 현대화 노력은 주권적 센서 및 우주 쓰레기 감축 이니셔티브를 통해 이러한 방향성을 보완하고 있습니다. 이는 단일 국가의 네트워크에 대한 의존도를 줄이고, 연합형 SSA 데이터에 대한 접근성을 확대하기 위한 것입니다. 이러한 투자 환경은 기밀 유지가 가능한 솔루션을 제공하고, 동맹국의 네트워크와 통합할 수 있으며, 고정 가격 서비스 모델 하에서 엄격한 가용성 지표를 충족할 수 있는 공급업체에게 유리하게 작용하고 있습니다. 우주 상황 인식 시스템 시장은 이러한 지속적인 예산 배정의 혜택을 받고 있으며, 이에 따라 대기업은 물론 성장 단계에 있는 기업을 막론하고 첨단 망원경, 원정용 레이더, 저지연 알고리즘이 도입되고 있습니다.

지상형 센서 인프라에는 막대한 설비 투자가 필요합니다.

차세대 레이더 및 광학 네트워크를 구축하려면 수년에 걸친 자본 투자 프로그램과 전용 설치 장소가 필요하며, 이로 인해 공공 예산에 부담이 가중되고, 기존 인프라가 갖춰지지 않은 지역에서는 민간 주도의 구축이 지연되고 있습니다. NASA의 비용 평가에 따르면, 대규모 감시 시스템은 건설 및 전체 수명 기간에 걸친 유지 관리에 수억 달러가 소요될 수 있으며, 또한 다중 거점 구상에서는 운영 및 유지 보수 비용이 총 소유 비용에 급격히 가산된다는 사실이 밝혀졌습니다. 유닛이 모듈식이라 하더라도, 물류 및 설치 준비 작업이 일정에 큰 영향을 미치기 때문에 증가하는 접근 사건에 대응하기 위한 신속한 확장이 어려워집니다. 일부 기관이나 시스템 통합사업자는 비용을 자본 예산에서 운영 예산으로 전환하는 연방형 아키텍처나 종량제 구매 방식으로 대응하고 있지만, 이러한 방식에서도 데이터의 무결성을 유지하기 위해서는 여전히 안전한 네트워크와 거버넌스가 필요합니다. 광통신 시스템의 도입은 심우주 레이더에 비해 자본 집약도가 낮은 경우도 있지만, 기상 조건, 일조 시간, 위도의 제약을 상쇄하기 위해서는 전 세계적인 배치야말로 여전히 필수적이며, 그 결과 총비용과 조정의 복잡성이 증가합니다. 따라서 우주 상황 인식 시스템 시장에서는 개별 예산을 지나치게 부담시키지 않으면서도 커버리지를 확대하기 위해 민관 협력이나 ‘"센서-어-서비스(SaaS)" 에 대한 강한 관심이 쏠리고 있습니다.

부문별 분석

2025년에는 서비스 기반 제공이 61.28%의 점유율을 차지했습니다. 이는 사업자가 전담 분석가와 안전한 데이터 링크를 통한 지원을 바탕으로, 턴키 방식의 추적, 근접 충돌 스크리닝, 궤도 분석을 우선시했기 때문입니다. 각 기관은 센서 접근 권한, 카탈로그 유지 관리, 운영 시나리오에 대한 대응 매뉴얼이 포함된 관리형 서비스를 지속적으로 조달하고 있으며, 이를 통해 예산의 안정화와 업무 연속성 향상을 도모하고 있습니다. 동시에, 클라우드 네이티브 아키텍처와 API 중심의 데이터 통합을 통해 대규모 자동화가 실현됨에 따라, 소프트웨어 및 분석 플랫폼 시장은 2031년까지 연평균 성장률(CAGR) 8.88%를 기록하며 성장할 것으로 전망됩니다. 우주 교통 관제 시스템은 프로토타입 단계부터 접근 알림을 전송하고 운영자의 피드백을 수신하는 운영 서비스로 전환되고 있으며, 중소규모 위성 군집에서의 도입이 가속화되고 있습니다. 서비스 제공업체는 분석가의 지속적인 모니터링과 기밀 연결이 필요한 임무에서 우위를 점하고 있습니다. 소프트웨어 공급업체는 위성 군의 규모가 크고, 선별 및 기동 계획 수립 과정에서 자동화가 중시되는 운영 환경에서 우위를 점하고 있습니다. 라이선싱 모델은 다양해지고 있으며, 기밀 구역의 경우 On-Premise 방식이, 상용 위성 군의 경우 구독형 SaaS가 채택되고 있습니다.

2025년에는 지구 근접 천체 감시가 72.68%를 차지했습니다. 이는 저궤도(LEO) 및 중궤도(MEO)에 가동 중인 위성과 우주 쓰레기가 가장 많이 존재하여, 이에 따른 근접 사고 건수가 증가하고 규제 당국의 감시도 강화되고 있기 때문입니다. 심우주 감시 시장은 2031년까지 연평균 성장률(CAGR) 8.11%로 성장할 것으로 전망됩니다. 달 주위 물류, 달 표면 탐사 임무, 그리고 장기 탐사 궤도로 인해 국가 프로그램의 대상 영역이 확대되고 있기 때문입니다. “'아르테미스'계획의 우선순위나 “'루나 게이트웨이'이 계획에 따라, 관측 데이터가 부족하고 통신 지연 시간이 긴 지구와 달 사이의 거리에서도 감시를 유지할 수 있는 아키텍처에 대한 수요가 뒷받침되고 있습니다. 우주 안전성을 강화하기 위한 유럽의 노력에는 지상 네트워크를 보완하고, 달 궤도 및 더 높은 궤도에서 발생하는 관측 사각지대를 해결하기 위한 이니셔티브가 포함되어 있습니다. 이러한 변화로 인해 알고리즘의 견고성과 센서 성능에 대한 요구 사항이 높아지면서, 공급업체에게는 유리한 상황이 되고 있습니다. AI와 머신러닝(ML)은 섭동을 고려한 궤도 역학 모델을 통합하고, 며칠에 걸친 감시를 위한 상관 창을 개발하는 예측 궤도 분석 분야에서 새로운 역할을 수행하고 있습니다.

지구 근방 시스템에서는 넓은 시야각으로 물체를 감지하고, 신속한 작업 할당 및 낮은 지연 시간을 실현하는 검증된 레이더 및 광학 스택이 활용되고 있습니다. 대형 물체의 수와 파편 군 증가에 따라, 대규모 선별 작업과 운영자 콘솔과 통합된 표준화된 보고 형식에 대한 수요가 높아지고 있습니다. 심우주 아키텍처는 고감도 수신기와 개선된 천체측량 기술을 통해 진화하여, 긴 호 모양의 궤도나 월식 중에도 추적을 유지할 수 있게 되었습니다.

지역별 분석

2025년, 북미는 41.58%를 차지했으며, 이는 지역적 리더십을 뒷받침하는 도메인 인식, 미사일 경계 체계, 그리고 사이버 공격에 대한 내성을 갖춘 지상 부문에 대한 지속적인 투자를 반영한 것입니다. 우주개발청(SDA)은 2025년 12월, 72기의 추적 위성을 제작하기 위해 여러 업체와 계약을 체결함으로써 산업 기반을 강화하는 한편, 우주와 지상 양 분야에 걸친 북미의 시스템 통합을 심화시켰습니다. 캐나다는 우주에서 이루어지는 광학 관측 시 미확인 물체의 식별 정확도를 높이기 위해 우주 상황 인식(SSA) 데이터 처리 기능 강화에 자금을 지원하며, 카탈로그 용량과 관련된 지역적 협력을 표명했습니다. 북미 기업들은 레이더의 감지 범위를 확대하고, 상업용 물체 카탈로그에 대한 공동 라이선스 계약을 체결하는 한편, 민간 교통 조정 서비스와 연계함으로써 저궤도(LEO)에서의 안전성을 향상시켰습니다.

유럽은 관측 범위의 공백을 메우고, 유럽 외부의 네트워크에 대한 의존도를 낮추는 데 도움이 되는 독자적인 역량 및 우주 쓰레기 저감 프로그램을 추진했습니다. ESA가 주도하는 능동적 우주 쓰레기 제거 활동에는 세계 최초의 계약 기반 우주 쓰레기 제거 서비스와 운영 임무를 위한 궤도상 서비스에 대한 지속적인 노력이 포함됩니다. 각국의 프로그램은 유럽 SST 프레임워크와 연계된 개량형 망원경 및 데이터 통합 플랫폼을 통해 이러한 노력을 보완하고 있으며, 이를 통해 회원국 간의 상황 인식 공유가 향상되고 있습니다. 유럽의 한 공급업체는 주요 망원경의 개조 및 성능 향상과 관련된 계약을 수주하여, 고가치 궤도상의 소형 표적 감지 능력을 강화했습니다.

아시아태평양은 위성 군의 확대와 자국 개발 추적 능력에 대한 국가적 투자에 힘입어, 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 9.11%라는 가장 빠른 성장세를 기록할 것으로 전망됩니다. 레이더 배치와 우주 기반 감지 이니셔티브 덕분에 재관측 빈도가 높아지고, 지역 내외에서 사업자의 관할 범위가 확대되고 있습니다. 지역 내 동맹국들은 망원경 업그레이드와 데이터 공유에 협력하고 있는 반면, 국내 기업들은 자사의 서비스를 국가 안보 및 민간 우주 분야의 우선순위에 맞추어 조정하고 있습니다. 또한, 민간 공급업체들도 원정형 레이더 시스템의 규모를 확대하고 있으며, 이를 통해 태평양 회랑 전역에 걸친 추적 능력이 향상되어 발사 활동 증가에 대한 사업자들의 대응이 지원되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.03According to Mordor Intelligence, the space situational awareness systems market size is expected to grow from USD 1.69 billion in 2025 to USD 1.82 billion in 2026. This report is Segmented by Solution (Services and Software and Analytics Platforms), Orbital Range (Near-Earth and Deep Space), Capability (Tracking and Surveillance Sensors, Data Fusion and Predictive Software, and More), End-User (Government and Military and Commercial Operators), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Space Situational Awareness (SSA) Systems Market Trends and Insights

Rising Frequency of Deep-Space and Planetary Missions

Cislunar operations and lunar surface logistics are moving off the drawing board and into active program execution, expanding surveillance perimeters and driving investments in tracking architectures that can maintain custody across Earth-Moon distances. NASA's Artemis campaign, Lunar Gateway buildout, and sustained lunar science priorities keep deep-space requirements in focus for the remainder of the decade, prompting demand for autonomous orbit-determination and long-latency tasking that existing near-Earth systems do not fully address. European priorities outlined by the European Space Agency emphasize complementary European Space Domain Awareness measures that close visibility gaps for lunar orbits and higher regimes beyond.

As more lunar missions progress through integration and launch, operators seek higher-power-aperture sensors, multi-day correlation algorithms, and software that models perturbations beyond the classical two-body regime. These capabilities are priced at a premium due to the hardware complexity and compute demands. Yet, they provide a durable edge for agencies and firms that must safeguard rendezvous operations and high-value payloads in cislunar space. The space situational awareness systems market is therefore aligning R&D with deep-space custody challenges as lunar logistics and planetary probes mature into steady mission lines across leading national programs.

Strategic Defense Investments in Space Domain Awareness Capabilities

Defense budgets in 2026 maintain a strong focus on space domain awareness, missile warning, and resilient ground segments, supporting multi-year procurement of sensors, data fusion platforms, and commercial data services. The US Space Force's 2026 request of USD 39.9 billion, up USD 11.3 billion year over year, allocates significant resources to Ground and Space Domain Awareness, next-generation missile tracking, and cyber-hardened infrastructure. Procurement programs centered on proliferated tracking layers and infrared sensing exemplify the pivot to multi-orbit resilience and rapid refresh, with awards supporting industrial bases that supply sensors, buses, payloads, and autonomy software.

Allied modernization efforts complement this trajectory through sovereign sensors and debris mitigation initiatives that reduce reliance on single-nation networks and broaden access to federated SSA data. This investment climate favors vendors that can deliver classified-ready solutions, integrate with allied networks, and meet stringent availability metrics under firm fixed-price service models. The space situational awareness systems market is benefiting from this continuity of appropriations, which pulls through advanced telescopes, expeditionary radars, and low-latency algorithms from primes and growth-stage firms alike.

High Capital Expenditure Required for Ground-Based Sensor Infrastructure

Next-generation radar and optical networks require multi-year capital programs and specialized sites, which strain public budgets and slow private deployments in regions without legacy infrastructure. NASA's cost assessments show that large surveillance systems can demand hundreds of millions of dollars across construction and through-life sustainment, and that operations and maintenance quickly add to the total cost of ownership for multi-station concepts. Even when units are modular, logistics and site-readiness work drive timelines that complicate rapid expansion to meet rising conjunction volumes. Some agencies and integrators respond with federated architectures and consumption-based buying that shift costs from capital to operating budgets, but these still require secure networking and governance to maintain data integrity. While optical deployments can be less capital-intensive than deep-space radars, global distribution remains essential to offset weather, daylight, and latitude constraints, thereby increasing aggregate cost and coordination complexity. The space situational awareness systems market, therefore, sees strong interest in public-private partnerships and sensor-as-a-service to accelerate coverage without overextending individual budgets.

Other drivers and restraints analyzed in the detailed report include:

- Collision Avoidance Imperatives from Expanding Commercial Mega-Constellations

- Mandated Compliance with Global Space Traffic Coordination Frameworks

- Rising Vulnerability of SSA Networks to Cybersecurity Threats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Service-based offerings captured a 61.28% share in 2025, as operators prioritized turnkey tracking, conjunction screening, and orbital analysis, supported by dedicated analysts and secure data links. Agencies continue to procure managed services that bundle sensor access, catalog maintenance, and response playbooks for operational scenarios, stabilizing budgets and improving continuity. At the same time, software and analytics platforms are projected to grow at 8.88% CAGR through 2031 as cloud-native architectures and API-driven fusion unlock automation at scale. Traffic coordination systems for space are moving from prototypes to operational services that distribute conjunction notifications and accept operator feedback, accelerating adoption among small and mid-size fleets. Service providers maintain an edge in missions that require continuous analyst oversight and classified connectivity. Software vendors win where fleets are large, and operations favor automation for screening and maneuver generation. Licensing models are diversifying, with on-premises deployments for classified enclaves and subscription-based SaaS for commercial fleets.

Near-Earth monitoring accounted for 72.68% in 2025, as low-Earth orbit (LEO) and medium-Earth orbit (MEO) host the most active satellites and debris, driving higher conjunction volumes and stronger regulatory oversight. Deep-space surveillance is projected to grow at an 8.11% CAGR through 2031, with cislunar logistics, lunar surface missions, and extended exploration trajectories expanding the area of interest for national programs. Artemis priorities and Lunar Gateway planning sustain demand for architectures that can maintain custody at Earth-Moon distances under sparse observations and longer communication delays. European efforts to strengthen space safety include initiatives to address visibility gaps in lunar orbits and higher orbits to complement terrestrial networks. These shifts raise requirements for algorithmic robustness and sensor performance, favoring suppliers. The emerging role of AI and ML in predictive orbital analytics that integrate orbital mechanics models to account for perturbations and develop correlation windows for multi-day custody.

Near-Earth systems benefit from mature radar and optical stacks that detect objects across a wide field of view with rapid tasking and low latency. Large object counts and fragment populations increase demand for screening at scale and for standardized reporting formats that integrate with operator consoles. Deep-space architectures are evolving with higher sensitivity receivers and improved astrometric techniques to maintain custody over long arcs and during lunar occultations.

Complete Report Scope:

- By Solution

- Services

- Software and Analytics Platforms

- By Orbital Range

- Near-Earth

- Deep Space

- By Capability

- Tracking and Surveillance Sensors (TSS)

- Data Fusion and Predictive Software (DFPS)

- Collision Avoidance Services (CAS)

- By End-User

- Government and Military

- Commercial Operators

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- France

- Germany

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Geography Analysis

North America accounted for 41.58% in 2025, reflecting sustained investment in domain awareness, missile warning layers, and cyber-hardened ground segments that underpin regional leadership. The Space Development Agency made multi-award selections in December 2025 to build 72 tracking layer satellites, reinforcing the industrial base and deepening North American system integration across space and ground. Canada funded enhancements to SSA data processing to improve the identification of unknown objects in space-based optical observations, signaling regional coordination on catalog capacity. North American firms expanded their radar footprint and secured joint licensing arrangements for commercial object catalogs, integrating with civil traffic coordination services to enhance safety in LEO.

Europe advanced sovereign capabilities and debris-mitigation programs that help close coverage gaps and reduce reliance on non-European networks. ESA's leadership in active debris removal includes the world's first contracted debris removal service and follow-on initiatives for in-orbit services that progress toward operational missions. National programs complement these efforts with upgraded telescopes and data fusion platforms that interface with the European SST framework, which improves shared situational awareness across member states. European providers secured awards for refurbishment and performance enhancements at critical telescopes, strengthening detection of small targets in high-value orbits.

Asia-Pacific is projected to register the fastest growth at 9.11% CAGR from 2026 through 2031, underpinned by expanding satellite fleets and national investments in indigenous tracking capabilities. Radar deployments and space-based sensing initiatives improve revisit rates and expand operators' custody within and beyond the region. Regional allies are collaborating on telescope upgrades and data sharing, while domestic firms align their offerings with national security and civil space priorities. Commercial providers are also scaling expeditionary radar systems, with deployments that enhance tracking across Pacific corridors and support operators' responses to higher launch activity.

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Kratos Defense & Security Solutions, Inc.

- Parsons Corporation

- ExoAnalytic Solutions, Inc.

- NorthStar Earth and Space Inc.

- LeoLabs, Inc.

- Slingshot Aerospace, Inc.

- Vision Engineering Solutions, LLC

- GlobVision Inc.

- Peraton Corp.

- RTX Corporation

- Airbus SE

- ClearSpace SA

- Astroscale Holdings Inc.

- SpaceNav

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising frequency of deep-space and planetary missions

- 4.2.2 Strategic defense investments in space domain awareness capabilities

- 4.2.3 Collision avoidance imperatives from expanding commercial mega-constellations

- 4.2.4 Emerging role of AI and ML in predictive orbital analytics

- 4.2.5 Growth in in-orbit servicing and active debris removal requirements

- 4.2.6 Mandated compliance with global space traffic co-ordination frameworks

- 4.3 Market Restraints

- 4.3.1 High capital expenditure required for ground-based sensor infrastructure

- 4.3.2 Atmospheric and weather-dependent limitations of optical tracking systems

- 4.3.3 Rising vulnerability of SSA networks to cybersecurity threats

- 4.3.4 Talent shortages in orbital mechanics and space traffic analysis

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Services

- 5.1.2 Software and Analytics Platforms

- 5.2 By Orbital Range

- 5.2.1 Near-Earth

- 5.2.2 Deep Space

- 5.3 By Capability

- 5.3.1 Tracking and Surveillance Sensors (TSS)

- 5.3.2 Data Fusion and Predictive Software (DFPS)

- 5.3.3 Collision Avoidance Services (CAS)

- 5.4 By End-User

- 5.4.1 Government and Military

- 5.4.2 Commercial Operators

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lockheed Martin Corporation

- 6.4.2 L3Harris Technologies, Inc.

- 6.4.3 Kratos Defense & Security Solutions, Inc.

- 6.4.4 Parsons Corporation

- 6.4.5 ExoAnalytic Solutions, Inc.

- 6.4.6 NorthStar Earth and Space Inc.

- 6.4.7 LeoLabs, Inc.

- 6.4.8 Slingshot Aerospace, Inc.

- 6.4.9 Vision Engineering Solutions, LLC

- 6.4.10 GlobVision Inc.

- 6.4.11 Peraton Corp.

- 6.4.12 RTX Corporation

- 6.4.13 Airbus SE

- 6.4.14 ClearSpace SA

- 6.4.15 Astroscale Holdings Inc.

- 6.4.16 SpaceNav

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment